Anti-infective Drugs Market Outlook:

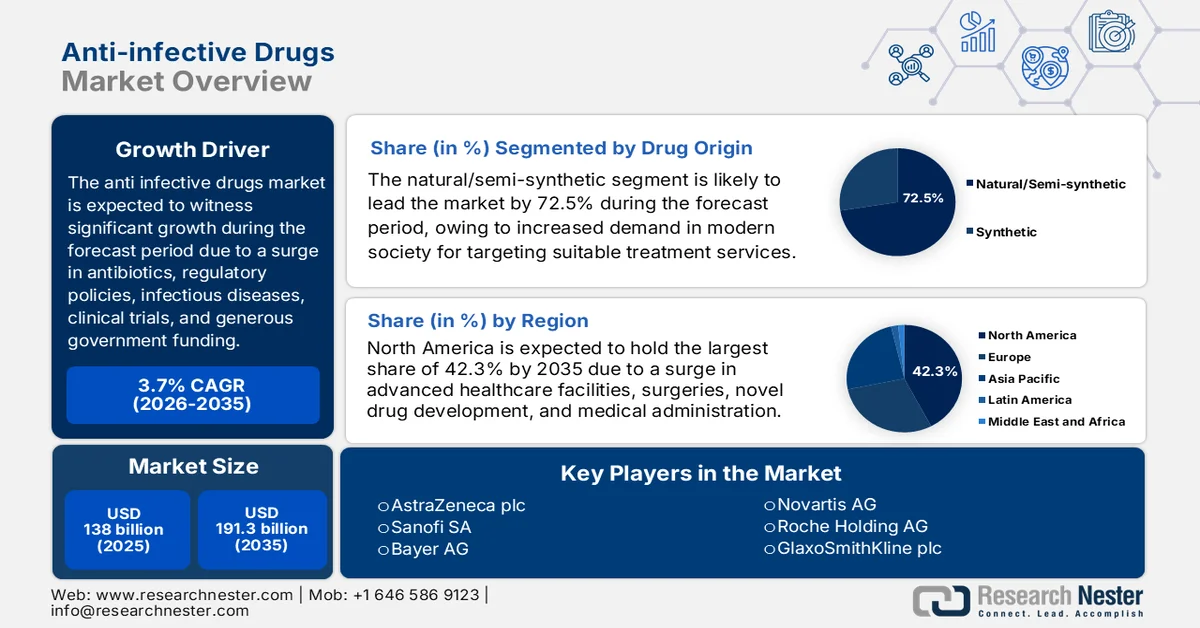

Anti-infective Drugs Market size was valued at over USD 138 billion in 2025 and is expected to reach USD 191.3 billion by the end of 2035, growing at a CAGR of 3.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of anti-infective drugs is estimated at USD 143.1 billion.

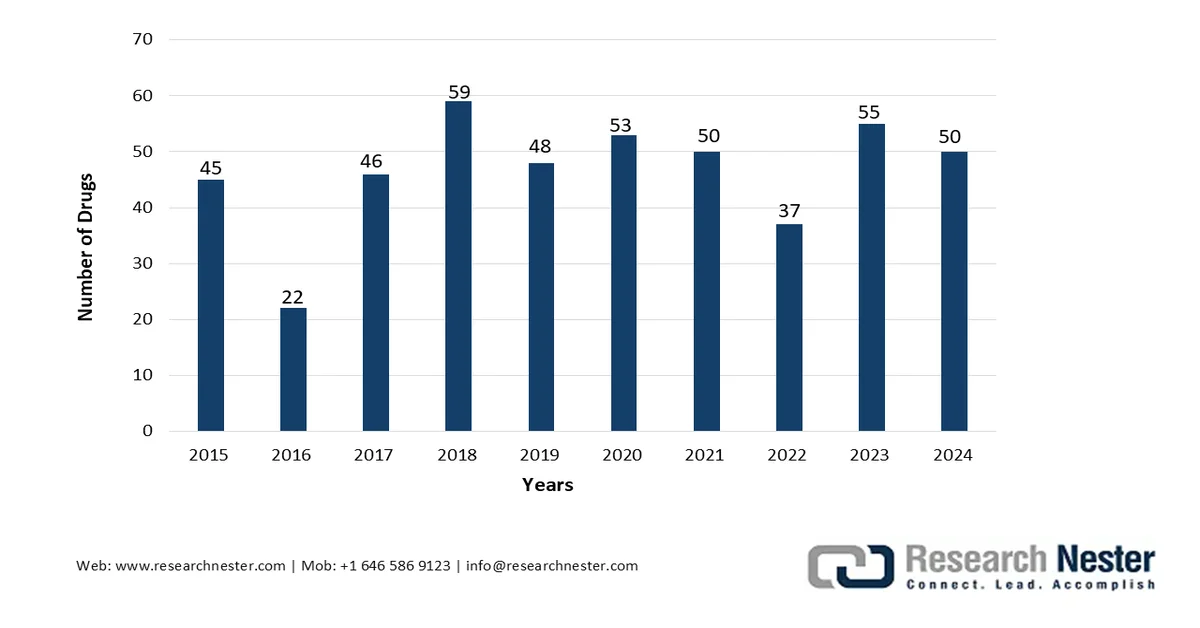

The worldwide anti-infective drugs market is positively influenced by factors including patient expiration for suitable antibiotics, regulatory harmonization across different regions, an increase in drug approvals, reimbursement policies, and national formularies, the prevalence of immunocompromising conditions and diabetes, and expansion in the patient pool. Based on government estimates published by the U.S. Food and Drug Administration (FDA) in 2025, 26 of 50, which is 52% of novel drug approvals, were readily approved in 2024 for diseases, including Neimann-Pick disease Type C, Duchenne muscular dystrophy, primary biliary cholangitis, familial chylomicronemia syndrome, and classical congenital adrenal hyperplasia. Moreover, of the 50 drugs, the FDA’s Center for Drug Evaluation and Research (CDER) surpassed its Prescription Drug User Fee Act (PDUFA) objectives for 47, which is 94% drugs, thus making it suitable for boosting the market globally.

FDA’s CDER Yearly Novel Drug Approval Analysis (2015-2024)

Source: U.S. FDA

Furthermore, the decentralized clinical trial models for drug development, the AI integration in antimicrobial discovery pipelines, subscription-based payment models for critical antibiotics, the point-of-care rapid diagnostic adoption, regionalization of active pharmaceutical ingredient supply chain, and the bacteriophage therapy re-emergence for refractory infections are trends that are positively impacting the anti-infective drugs market globally. According to official statistics published by the World Health Organization (WHO) in November 2025, the number of clinical trials in Africa accounted for 990 in 2023 and 1,049 in 2024. Meanwhile, trials further catered to 13,284 in 2023 and 14,521 in 2024, 18,048 as of 2023 and 19,758 in 2024 for Europe, which is further followed by 14,213 and 20,247 in South-East Asia. Besides, the clinical trial conduction across different countries is also bolstering the market growth worldwide.

Country-Wise Clinical Trial Analysis for Drug Development (2025)

|

Countries |

Number of Clinical Trials |

|

U.S. |

197,090 |

|

China |

162,704 |

|

India |

94,141 |

|

Japan |

67,462 |

|

Germany |

59,320 |

|

UK |

52,227 |

|

France |

50,768 |

|

Netherlands |

45,471 |

|

Canada |

38,166 |

|

Spain |

37,438 |

Source: WHO

Key Anti-infective Drugs Market Insights Summary:

Regional Highlights:

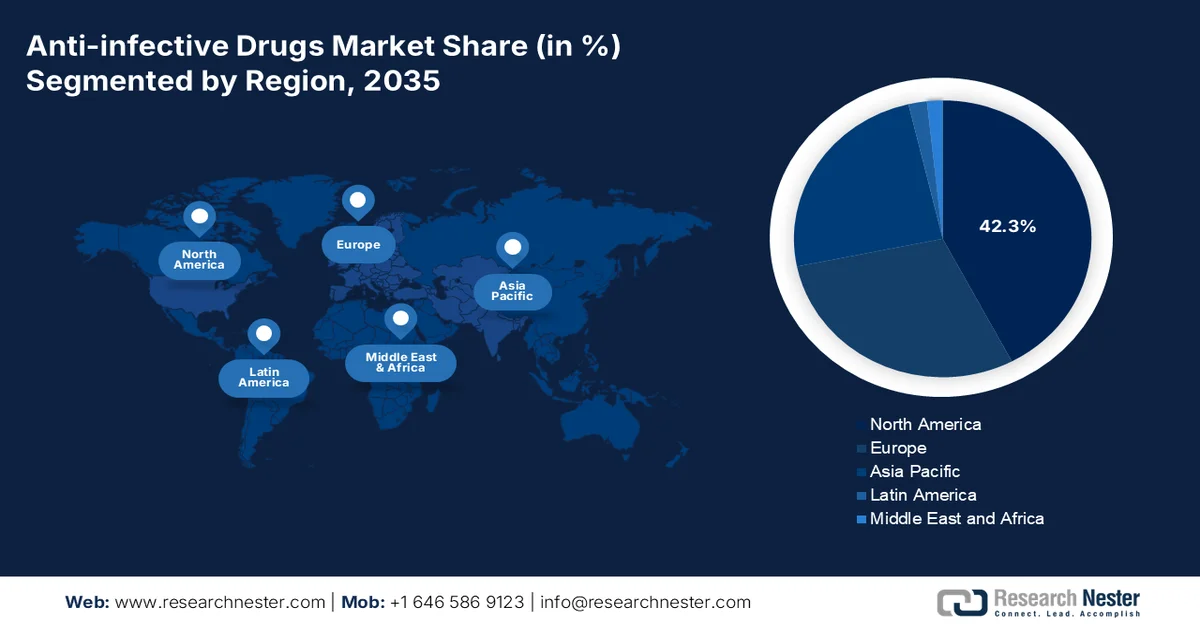

- By 2035, North America in the anti-infective drugs market is projected to command a 42.3% share, underpinned by strong antimicrobial stewardship programs, rising antibiotic consumption, and advanced healthcare infrastructure.

- Asia Pacific is poised to be the fastest-growing region over 2026-2035, accelerated by expanding patient pool, increasing healthcare expenditure, and growing prevalence of infectious diseases.

Segment Insights:

- In the anti-infective drugs market, the natural/semi-synthetic sub-segment is expected to account for a dominant 72.5% share by 2035, propelled by rising demand for natural drugs supported by increasing herbal supplement consumption.

- The generic drugs segment is anticipated to secure the second-largest share during 2026–2035, fueled by improving healthcare affordability and accessibility alongside rising burden of antimicrobial resistance.

Key Growth Trends:

- Increase in the aging population

- Expansion in universal health coverage

Major Challenges:

- Geopolitical fragility of the generic API supply chain

- Accelerating antimicrobial resistance (AMR) outpacing diagnostics

Key Players: Pfizer Inc. (U.S.), Merck & Co., Inc. (U.S.), Johnson & Johnson (U.S.), AbbVie Inc. (U.S.), Eli Lilly and Company (U.S.), Viatris Inc. (U.S.), Abbott Laboratories (U.S.), Bristol-Myers Squibb (U.S.), Gilead Sciences Inc. (U.S.), Novartis AG (Switzerland), Roche Holding AG (Switzerland), GlaxoSmithKline plc (GSK) (UK), AstraZeneca plc (UK), Sanofi SA (France), Bayer AG (Germany), Teva Pharmaceutical Industries Ltd. (Israel), Sun Pharmaceutical Industries Ltd. (India), Cipla Ltd. (India), Daiichi Sankyo Company, Limited (Japan), CSL Limited (Australia), Yuhan Corporation (South Korea), Pharmaniaga Berhad (Malaysia), Zai Lab (China), OmnixMedical (Israel), Shionogi & Co., Ltd. (Japan).

Global Anti-infective Drugs Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 138 billion

- 2026 Market Size: USD 143.1 billion

- Projected Market Size: USD 191.3 billion by 2035

- Growth Forecasts: 3.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 1 April, 2026

Anti-infective Drugs Market - Growth Drivers and Challenges

Growth Drivers

- Increase in the aging population: This particular population category is effectively creating demographic pressure on the anti-infective drugs market globally. According to official statistics published by the United Nations Population Fund in June 2024, the worldwide share of people aged 65 years nearly doubled and increased from 5.5% to 10.3%. In addition, this number is further projected to double again by 20.7% by the end of 2074, and at the same time, people aged more than 80 years are also expected to be thrice the present number. Besides, at present, over 60% of the world population resides in countries that comprise an overall fertility rate below the replacement level. Additionally, the average rate required to replace a population of 2.1 live births per woman is also uplifting the anti-infective drugs market demand.

- Expansion in universal health coverage: The aspect of government initiatives for expanding universal health coverage, especially across low- and middle-income nations, is systematically enhancing the accessibility to crucial anti-infective drugs for untreated populations. As stated in an article published by NLM in March 2025, an estimated 2 billion people are presently witnessing financial challenges, with 1 billion witnessing catastrophic out-of-pocket health expenditure, while 344 million people are falling into poverty. Besides, fewer than 30% countries, which is 42 of 138 nations, are making efforts to optimize service coverage and diminish out-of-pocket expenses. Therefore, with these limitations, there is a huge scope for increasing universal health coverage services, which in turn is positively impacting the anti-infective drugs market globally.

- Rise in vector-borne infections: The increase in modified precipitation patterns and worldwide temperatures is deliberately extending the geographic range of vector-borne infectious disorders, which is enhancing the anti-infective drugs market demand globally. As stated in an article published by the WHO in September 2024, these diseases account for over 17% of overall infectious disorders and eventually cause more than 700,000 deaths every year due to viruses, bacteria, and parasites. Besides, malaria leads to approximately 249 million cases across different locations, and further results in over 608,000 deaths annually. Simultaneously, dengue is also another viral infection that affects over 3.9 billion people across 132 countries, with roughly 40,000 deaths per year, thereby making it suitable for boosting the market development.

Challenges

- Geopolitical fragility of the generic API supply chain: Active pharmaceutical ingredients (APIs) for essential antibiotics, including penicillins, cephalosporins, and macrolides, are manufactured in two industrial clusters. These clusters comprise China’s Zhejiang province and India’s Hyderabad region and this particular hyper-concentration creates a single point of failure in the anti-infective drugs market. Besides, a regional lockdown, environmental shutdown, or export ban instantly triggers global shortages of critical drugs, such as meropenem and piperacillin-tazobactam. Moreover, the increase in regulatory scrutiny, including the USFDA, EMA, CDSCO, on data integrity and pollution control has forced marginal suppliers offline.

- Accelerating antimicrobial resistance (AMR) outpacing diagnostics: The aspect of resistance is evolving faster than clinical decision-making. Additionally, by the end of 2030, the WHO has estimated that annual deaths could be attributable to AMR, yet the diagnostic tools to combat this are critically lagging. At present, physicians prescribe broad-spectrum antibiotics empirically, often without identifying the pathogen. This overuse accelerates resistance, while waiting 3 days for culture results is clinically unacceptable for septic patients. Besides, the missing link is rapid, point-of-care phenotypic susceptibility testing within 1 to 2 hours. Although CRISPR-based and AI-predictive diagnostics exist in labs, they remain too expensive and unapproved for frontline use in ICUs, thus negatively impacting the anti-infective drugs market growth.

Anti-infective Drugs Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

3.7% |

|

Base Year Market Size (2025) |

USD 138 billion |

|

Forecast Year Market Size (2035) |

USD 191.3 billion |

|

Regional Scope |

|

Anti-infective Drugs Market Segmentation:

Drug Origin Segment Analysis

The natural/semi-synthetic sub-segment, part of the drug origin segment, is anticipated to garner the largest share of 72.5% in the anti-infective drugs market by the end of 2035. The sub-segment’s upliftment is primarily attributed to its importance in modernized society, especially in medicine, wherein there lies the provision of targeted treatments for different conditions. According to official statistics published by the America Botanical Council in September 2025, the retail sales of herbal dietary supplements, particularly in the U.S., has reached a noteworthy USD 13.2 billion as of 2024. Additionally, customers in the country significantly spent USD 680 million on herbal supplements in the same year, in comparison to 2023, demonstrating a 5.4% surge. Therefore, with this continuous increase in herbal supplements, there is a huge demand for natural drugs, which is positively impacting the market growth.

Drug Type Segment Analysis

The generic drugs segment in the anti-infective drugs market is projected to account for the second-largest share during the forecast period. The segment’s growth is highly fueled by the aspect of enhancing healthcare affordability and accessibility, which is suitable for providing therapeutic quality, safety, and efficacy at a significantly reduced expense. As stated in an article published by the WHO in November 2023, the aspect of bacterial antimicrobial resistance (AMR) is effectively responsible for 1.2 million deaths globally and also readily contributes to 4.9 million deaths. Besides, this is projected to lead to USD 1 trillion additional healthcare expenses by the end of 2050, along with USD 3.4 trillion in gross domestic product (GDP) losses every year by the same year. Therefore, there is a huge demand for generic drugs, owing to their comprehensive availability, lower expenses, and increased consumption rates.

Distribution Channel Segment Analysis

By the end of the stipulated timeline, the hospitals segment, which is part of the distribution channel, is expected to hold the third-largest share in the anti-infective drugs market. The segment’s development is highly propelled by its role as the primary treatment hub for severe, complex, and resistant infections—including surgical site infections, ventilator-associated pneumonia, and bloodstream infections—which require immediate intravenous therapy and continuous clinical monitoring. Hospitals maintain comprehensive inventories of antibiotics, antivirals, and antifungals across all WHO AWaRe categories, supported by on-site diagnostic infrastructure for antimicrobial susceptibility testing. This particular channel benefits from substantial patient volumes, with the majority of antibacterial prescriptions originating in hospital settings.

Our in-depth analysis of the anti-infective drugs market includes the following segments:

|

Segment |

Subsegments |

|

|

|

Drug Type |

|

|

Distribution Channel |

|

|

Infection Type |

|

|

Route of Administration |

|

|

Drug Class |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Anti-infective Drugs Market - Regional Analysis

North America Market Insights

North America in the anti-infective drugs market is anticipated to garner the largest share of 42.3% by the end of 2035. The market’s upliftment in the region is highly attributed to the presence of strong antimicrobial stewardship programs, an increase in antibiotic consumption rates, and innovative healthcare infrastructure, along with a rise in surgical volumes, concentration of notable drug development, and hospital-based intravenous antibiotic administration. According to official statistics published by NLM in April 2024, the projected surgical rate in the U.S. typically ranges from 12.0 to 21.4 operations per 100,000 people. Besides, according to an ISAPS article published in June 2024, the country also performed more than 6.1 million procedures, followed by Brazil with 3.3 million surgeries. Moreover, the prevalence of surgery among different genders, ages, and ethnicities in the region is positively impacting the anti-infective drugs market growth.

Surgery Prevalence Among Gender, Age, and Ethnicity in the U.S. (2024)

|

Gender |

Age |

Ethnicity |

|||

|

Male |

10.1% |

0 to 17 years |

4.9% |

Hispanic |

7.1% |

|

Female |

12.3% |

18 to 34 years |

8.8% |

Non-Hispanic White |

13.3% |

|

- |

- |

35 to 49 years |

9.9% |

Non-Hispanic Black |

8.6% |

|

- |

- |

50 to 64 years |

14.5% |

Non-Hispanic Asia |

6.8% |

|

- |

- |

Over 65 years |

19.4% |

Non-Hispanic Other |

10.6% |

Source: NLM

The anti-infective drugs market in the U.S. is growing significantly, owing to the increased focus on antimicrobial resistance, escalating the need for last-line therapies, hospital stewardship programs for shaping utilization patterns, and generous federal funding for novel antimicrobial development. As per an article published by NLM in October 2024, the country significantly spent USD 99 billion, especially on orally- and clinician-administered anticancer therapies, as of 2023. In addition, this particular expenditure is predicted to increase to USD 180 billion by the end of 2028, owing to the price introduction of suitable therapeutics and a surge in existing products. Besides, as per the February 2026 HHS Government article, the Health and Human Services (HHS) Secretary declared the plan for strengthening prevention and ensuring treatment expansion by investing USD 100 million. This is suitable for overcoming homelessness issues, combating opioid addiction, and optimizing public safety, thus driving the market growth in the country.

The federal-provincial coordination on antimicrobial resistance surveillance, the presence of provincial formularies in limiting broad-spectrum antibiotic accessibility, an increase in governmental investment for diagnostic implementation, and the demand for target therapies are factors fueling the anti-infective drugs market in Canada. As per an article published by the Canada Organization for Rare Disorders in July 2025, there has been the allocation of USD 1.4 billion for the upcoming 3 years across territories and provinces in the country under Canada’s Rare Disease Drug Strategy. The purpose is to optimize equitable accessibility to rare disease treatments, along with diagnostic and screening services. Moreover, based on the February 2026 Government of Canada estimates, nearly USD 500 million every year has also been allocated for futuristic phases to assist people with chronic disorders, thereby denoting a huge demand for anti infective drugs in the country.

APAC Market Insights

The Asia Pacific in the anti-infective drugs market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by an increase in the patient pool, a surge in healthcare spending, a rise in the incidence of infectious disorders, expansion in government-based strategies, and regional pharmaceutical manufacturing capabilities. According to official statistics published by NLM in February 2023, a suitable proportion, roughly ranging from 4% to 7% of the overall GDP, has been invested in the health industry in the majority of regional countries. Moreover, the region is also subject to significant private and public healthcare divisions, especially in Malaysia. Besides, the health status across high, upper-middle, and lower-middle income nations is also positively influencing the market development in the overall region.

Health Status Analysis in the Asia Pacific (2024)

|

Countries |

Health at Birth (Females) |

Health at Birth (Males) |

Survival to Age 65 (Females) |

Survival to Age 65 (Males) |

Under Age 5 Mortality Rate (1,000 per live births) |

|

Australia |

70.7 years |

69.9 years |

94.1% |

89.2% |

3.8 |

|

Japan |

74.8 years |

71.9 years |

94.7% |

90.0% |

2.3 |

|

Korea |

74.1 years |

70.7 years |

96.4% |

92.0% |

2.8 |

|

Singapore |

75.0 years |

72.4 years |

93.8% |

87.9% |

3.8 |

|

China |

70.1 years |

67.2 years |

90.4% |

82.0% |

6.6 |

|

Malaysia |

65.1 years |

63.0 years |

86.6% |

77.5% |

7.8 |

|

India |

58.3 years |

58.0 years |

78.6% |

71.7% |

29.1 |

|

Vietnam |

68.0 years |

62.8 years |

87.6% |

72.7% |

20.3 |

Source: OECD

The anti-infective drugs market in China is gaining increased traction, owing to the presence of a massive population, increased burden of bacterial infections, continuous healthcare system reforms, the aging population, surge in hospitalization rates, and ongoing governmental investment for novel therapeutics. As per an article published by Infectious Medicine in December 2025, the country has witnessed 75.1 million incidences, along with 5,590 deaths from enteric infection caused by parasites, bacteria, and viruses. In addition, both mortality and age-standardized incidence rates in the country accounted for 0.44 per 100,000 population and 59.04 per 100,000, respectively. Therefore, with an increase in such incidents, there is a huge demand for generic drugs, which in turn, caters to fueling the market expansion and development in the country.

The aspects of an increase in the burden of infectious disorders, focus on national health priorities, the availability of anti-TB-fixed-dose and first-line combination drugs, improvement in treatment outcomes, continuous government investment on anti-infectives, and growth in pharmaceutical manufacturing facilities are trends that are developing the anti-infective drugs market in India. Based on government estimates published by the Ministry of Health and Family Welfare in July 2025, there has been a 17.7% reduction in tuberculosis incidence from 23.7 million to 19.5 million, along with 21.4% decline in mortality from 2.8 million to 2.2 million, both of which have been successfully achieved in 2023. Likewise, there has also been a 78.1% drop in malaria cases and 77.6% decline in deaths, which was recorded in 2024, along with a yearly parasite incidence reducing from 0.92 to 0.18, thus proliferating the market development in the country.

Europe Market Insights

Europe in the anti-infective drugs market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly fueled by the existence of strong public healthcare systems, strict regulatory oversight through the Europe Medicines Agency (EMA), tactical investments under pharmaceutical strategy, and robust generic substitution. According to official statistics published by OECD in November 2024, there has been an increase in the inflow of internationally-trained doctors in regional nations by 17% as of 2022, along with a surge in trained nurses by 72%. Simultaneously, as of 2023, more than 40% of doctors in Norway, Switzerland, and Ireland, and over 50% nurses in Ireland have received foreign training services. Therefore, with this increase in healthcare professionals, there is a huge growth opportunity for the anti-infective drugs market in the overall region.

The anti-infective drugs market in Germany is gaining increased exposure, owing to an increase in clinical demand, the presence of a suitable reimbursement landscape for advanced drugs, the utilization of antibiotics for aiding infections, and the presence of statutory health insurance. As stated in an article published by Deutschland in May 2025, nearly 3 quarters of 30 drugs with the latest active ingredients were placed on the domestic economy as of 2023. These particular drugs are targeted to aid cancer, immunological, and infectious disorders. Likewise, more than 350 active ingredients and almost 400 biotechnology-driven drugs have also been accepted in the country. Based on the approval, there is the availability of standard gene and cell therapies to alleviate and cure complicated diseases, thereby making it suitable for uplifting the market in the overall country.

The increased volume of specific and consumption public health reforms, continuous budget allocation by the government for novel anti-infectives, a surge in the utilization of broad-spectrum antibiotics, such as third-generation cephalosporins, and an upsurge in suitable funding for infectiologie in hospitals are driving the anti-infective drugs market in France. Based on government estimates published by the Ministry for Europe and Foreign Affairs in November 2024, the Europe Union and the Global Fund have successfully saved over 65 million lives and also diminished the number of deaths caused by infectious diseases every year by 61%. In addition, these administrative organizations have invested over USD 65 billion in supporting national programs. Moreover, the Global Fund, in particular, remains the ultimate fundraising technique in the country by offering 28% of overall funding for AIDS, 62% for malaria, and 76% for tuberculosis, thus driving the market exposure.

Key Anti-infective Drugs Market Players:

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Johnson & Johnson (U.S.)

- AbbVie Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Viatris Inc. (U.S.)

- Abbott Laboratories (U.S.)

- Bristol-Myers Squibb (U.S.)

- Gilead Sciences Inc. (U.S.)

- Novartis AG (Switzerland)

- Roche Holding AG (Switzerland)

- GlaxoSmithKline plc (GSK) (UK)

- AstraZeneca plc (UK)

- Sanofi SA (France)

- Bayer AG (Germany)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Cipla Ltd. (India)

- Daiichi Sankyo Company, Limited (Japan)

- CSL Limited (Australia)

- Yuhan Corporation (South Korea)

- Pharmaniaga Berhad (Malaysia)

- Zai Lab (China)

- OmnixMedical (Israel)

- Shionogi & Co., Ltd. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Pfizer Inc. maintains a broad anti-infective drugs market portfolio that spans both established hospital injectables and novel therapeutics targeting resistant pathogens. The company has strategically leveraged its manufacturing scale to ensure supply continuity for essential antibiotics during global health emergencies.

- Merck & Co., Inc. is recognized for its leadership in developing novel antibiotic combination therapies specifically designed to overcome carbapenem resistance in Gram-negative infections. The company actively engages in antimicrobial stewardship initiatives and public-private partnerships to preserve the efficacy of its anti-infective products.

- Johnson & Johnson has historically contributed to the anti-infective market through its infectious disease division, focusing on treatments for resistant tuberculosis and viral infections. The company continues to evaluate its anti-infective pipeline, prioritizing assets that address critical global health security threats.

- AbbVie Inc. strengthened its anti-infective presence through strategic acquisitions, integrating established antiviral therapies and hospital-based antibiotic products into its specialty portfolio. The company focuses on lifecycle management of key anti-infective assets while deprioritizing early-stage antibiotic discovery in favor of more predictable therapeutic areas.

- Eli Lilly and Company has a heritage in anti-infective drug development, though the company has significantly reduced its antibiotic research footprint in recent years. Today, Lilly focuses primarily on niche anti-infective agents for severe or resistant infections, often in collaboration with government agencies and non-profit organizations.

Here is a list of key players operating in the global anti-infective drugs market:

The anti-infective drugs market is highly competitive, dominated by large multinational pharmaceutical companies alongside significant generic manufacturers from India. Key players are pursuing strategic initiatives such as portfolio refinement, public-private partnerships, and geographic expansion. For instance, Pfizer ensures supply chain resilience through the AMR Action Fund, while Merck focuses on novel combination therapies for resistant Gram-negative infections. Moreover, India-based manufacturers, such as Sun Pharma and Cipla leverage cost-efficient production and vast distribution networks. Besides, in November 2024, Zai Lab and Pfizer strategically collaborated for the notable antibacterial drug, XACDURO in mainland China. Based on this collaboration, Pfizer undertook and performed commercialization activities for the drug and Zai Lab leveraged the industry-based commercialization facility of Pfizer, thus driving the anti-infective drugs industry globally.

Corporate Landscape of the Anti-infective Drugs Market:

Recent Developments

- In December 2025, OmnixMedical successfully raised USD 25 million in a Series C funding round-up, which was co-led by the EIC Fund and Harel Insurance & Finance, along with existing shareholders, including Oriella Limited, Xenia Ventures, Tal Ventures, and Entree Capital.

- In February 2025, AbbVie declared that the FDA has effectively approved EMBLAVEO, which is the first-ever and only fixed-dose, monobactam/β-lactamase, and intravenous inhibitor combination antibiotic, suitable for patients aged more than 18 years.

- In June 2024, Shionogi & Co., Ltd. expanded worldwide infectious disease and antimicrobial research operations, particularly to the U.S., for addressing emerging and present heath challenges by deliberately establishing its first-ever research infrastructure in California.

- Report ID: 8492

- Published Date: Apr 01, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Anti-infective Drugs Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.