Acute Migraine Drugs Market Outlook:

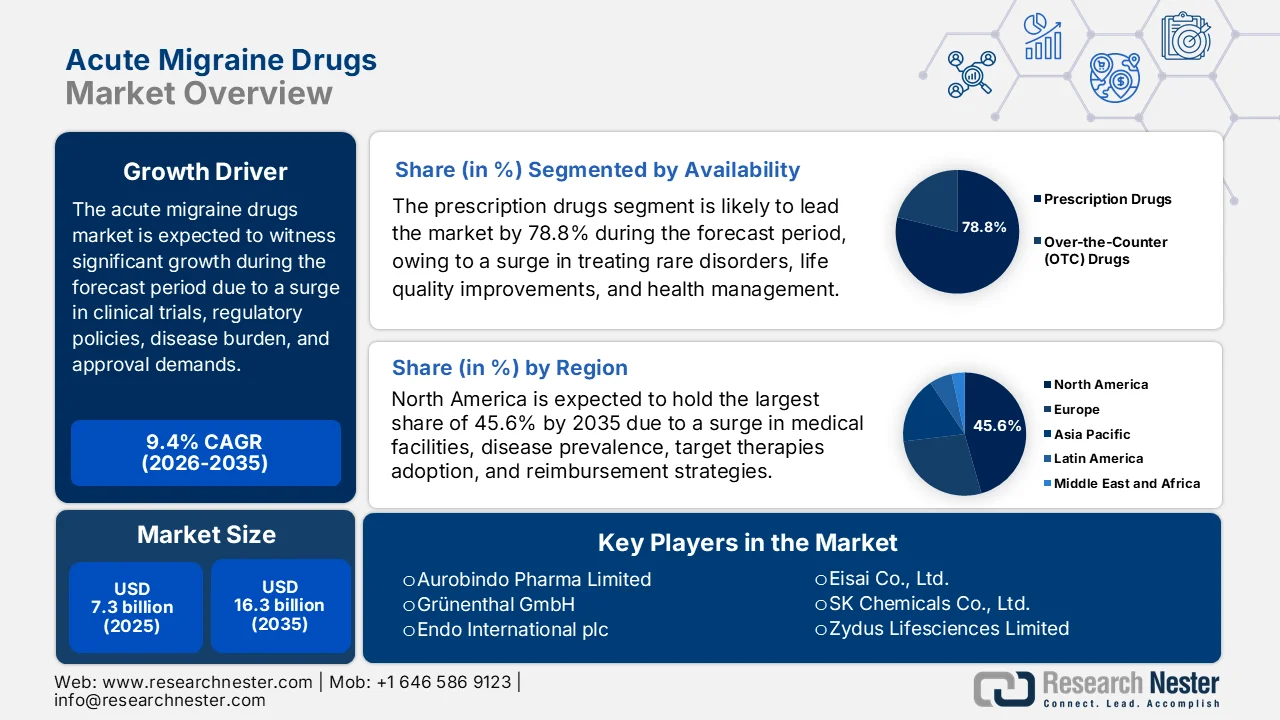

Acute Migraine Drugs Market size was valued at over USD 7.3 billion in 2025 and is projected to reach USD 16.3 billion by the end of 2035, growing at a CAGR of 9.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of acute migraine drugs is estimated at USD 7.9 billion.

The global acute migraine drugs market is being significantly reshaped, owing to factors such as regulatory dynamics, strict approval demands, expanded meticulous data collection and clinical trials, payer management strategies, reimbursement policies, and the increased burden across different economies. According to official statistics published by the World Health Organization (WHO) in October 2025, headache disorders approximately impact 40% of the population, or 3.1 billion people globally. This caters to 3 common neurological conditions for age groups ranging from 5 years to 80 years. Besides, based on the April 2023 Cleveland Clinic Organization article, migraines affect almost 12% to 15% of the population, and chronic migraine is estimated to impact 1% to 2.2% of people. Therefore, based on this prevalence and the impact on the population, there is a huge demand for the market.

Furthermore, the rapid onset of non-oral delivery systems, the presence of fixed-dose combination therapies, and drug-free neuromodulation therapies are a few trends that are responsible for driving the acute migraine drugs market globally. As stated in an article published by The Lancet Neurology in May 2025, 313 trials were identified, including 29 neuromodulation and 284 pharmacological, along with a clinical study on 48,789 adult patient pool, comprising 25,078 male and 20,611 female. Of these, the number needed to treat (NNT) accounted for 4.6%, and the number needed to harm (NNH) was 17.1% based on tricyclic antidepressants. Besides, in the case of serotonin and norepinephrine reuptake inhibitors, the NNT was 7.4% and NNH was 13.95, which was followed by 2.7% NNT and 216.3% NNH for botulinum toxin, thereby expanding the treatment provisions of migraine.

Key Acute Migraine Drugs Market Insights Summary:

Regional Highlights:

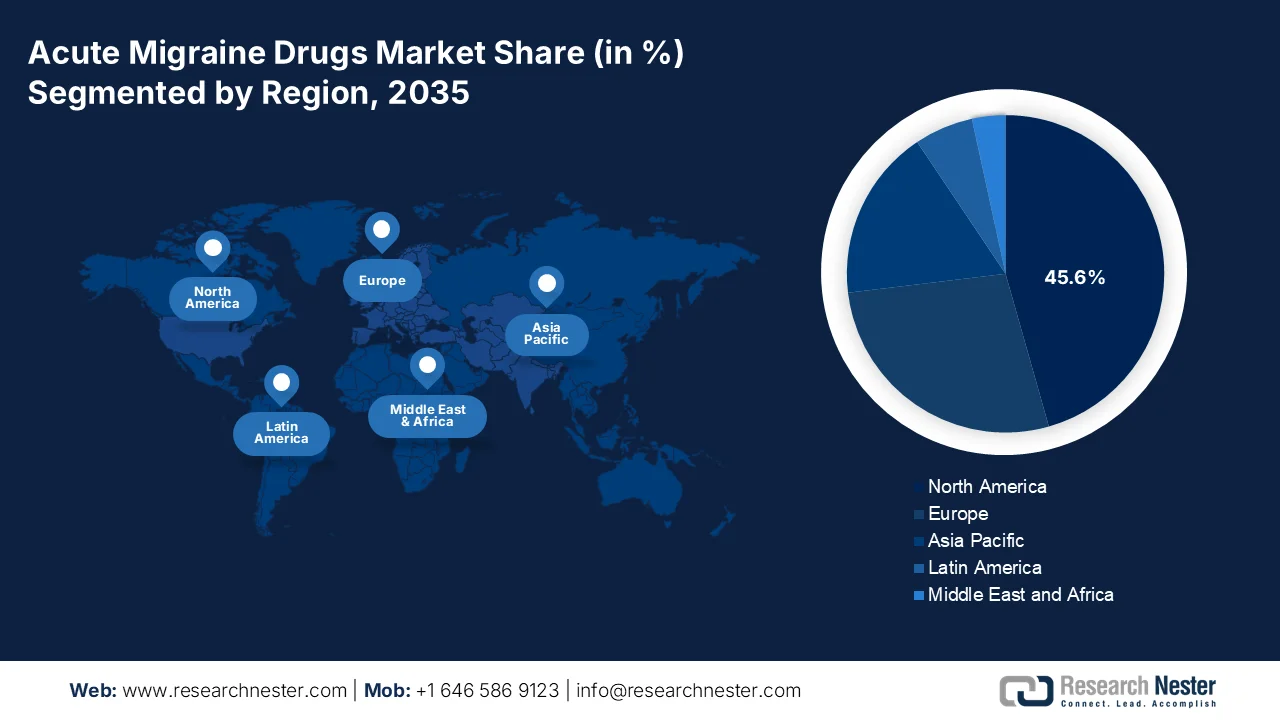

- North America acute migraine drugs market is projected to dominate with a 45.6% share by 2035, attributed to rising disease prevalence, advanced healthcare infrastructure, and expanding reimbursement coverage

- Asia Pacific is anticipated to witness the fastest growth over 2026-2035, propelled by a large undiagnosed population and improving healthcare access

Segment Insights:

- Prescription Drugs sub-segment in the acute migraine drugs market is expected to account for a 78.8% share by 2035, driven by cost-effective preventive treatments and improved quality of life outcomes

- Adults sub-segment is projected to hold the second-largest share during 2026-2035, fueled by higher disease burden and increased frequency of migraine episodes

Key Growth Trends:

- First-line recommendations for target therapies

- Pipeline advancement in notable mechanisms of action

Major Challenges:

- High research and development failure rates

- Suboptimal diagnosis and treatment of migraine in primary care

Key Players: GlaxoSmithKline (UK), Pfizer Inc. (U.S.), Novartis AG (Switzerland), Teva Pharmaceutical Industries Ltd. (Israel), Merck & Co., Inc. (U.S.), Johnson & Johnson (U.S.), Eli Lilly and Company (U.S.), AbbVie Inc. (U.S.), Bayer AG (Germany), AstraZeneca plc (UK), Sun Pharmaceutical Industries Ltd. (India), Dr. Reddy's Laboratories Ltd. (India), Cipla Limited (India), Lupin Limited (India), Aurobindo Pharma Limited (India), Grünenthal GmbH (Germany), Endo International plc (Ireland), Eisai Co., Ltd. (Japan), SK Chemicals Co., Ltd. (South Korea), Zydus Lifesciences Limited (India), Axsome Therapeutics, Inc. (U.S.), Amneal Pharmaceuticals, Inc. (U.S.), Satsuma Pharmaceuticals, Inc. (U.S.).

Global Acute Migraine Drugs Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 7.3 billion

- 2026 Market Size: USD 7.9 billion

- Projected Market Size: USD 16.3 billion by 2035

- Growth Forecasts: 9.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (45.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: India, South Korea, Singapore, Brazil, Indonesia

Last updated on : 28 April, 2026

Acute Migraine Drugs Market - Growth Drivers and Challenges

Growth Drivers

- First-line recommendations for target therapies: The elevation of targeted therapies to first-line treatment solutions by authoritative medical organizations is fundamentally escalating the acute migraine drugs market growth. According to official statistics published by the Frontiers Organization in June 2024, it has been readily estimated that almost 42% of migraines are inherited and are associated with increased pain scores, early onset, and frequent attacks. Therefore, as a part of target therapy, fremanezumab is regarded as an approved monoclonal antibody, which is recommended to be consumed monthly at 225 mg or quarterly at 675 mg. Regarding this antibody medication, Phase II and Phase III HALO studies determined successful results for both chronic and episodic migraine, thus bolstering the market growth.

- Pipeline advancement in notable mechanisms of action: The ongoing development of migraine therapies targeting notable mechanisms of action beyond the established pathway represents a long-lasting driver for the acute migraine drugs market. As stated in an article published by Frontiers Organization in February 2024, migraine patients, especially in the U.S., spent USD 11,010 yearly for direct healthcare expenses, intending to aid diseases. In addition, the yearly indirect expenses of migraine patients, owing to workplace absenteeism and disability, amount to USD 2,350 more in comparison to non-migraine patients. Therefore, based on these expenses, pipeline assets include neuromuscular blocking agents that provide suitable alternatives for patients unable to tolerate conventional options, thereby making it suitable for fueling the market growth.

- Growing demand for oral therapies: This is considered a straightforward driver for the acute migraine drugs market, which caters to the growing and strong patient preference for on-demand and convenient oral therapies. As per an article published by NLM in August 2022, the increased utilization of paracetamol, triptans, and non-steroidal anti-inflammatory drugs is considered the mainstay of oral migraine treatment. Besides, based on a Phase III clinical trial, a pharmaceutical product comprising rizatriptan and meloxicam demonstrated a pain-free and superior symptom response at 2 hours post-dose in comparison to placebo, with a 48-hour sustained pain-free rate. Likewise, the AXS-07 formulation is also superior to placebo for both bothersome and pain-free symptom endpoints, especially in terms of mild pain, thus denoting an optimistic outlook for the market.

Challenges

- High research and development failure rates: The pharmaceutical industry faces an exceptionally challenging roadblock when attempting to develop truly differentiated acute migraine drugs. Besides, preclinical models poorly predict human migraine efficacy, as the pathophysiology involves complex interactions between the trigeminal vascular system, cortical spreading depression, and central sensitization, with processes that rodent models cannot faithfully replicate. Consequently, promising compounds frequently advance to expensive Phase II trials only to fail on primary endpoints of pain freedom at two hours or sustained response. Moreover, several CGRP antagonists and serotonin receptor modulators have been abandoned in late-stage development due to hepatotoxicity signals or lack of superiority over placebo, thus negatively impacting the acute migraine drugs market.

- Suboptimal diagnosis and treatment of migraine in primary care: A foundational roadblock undermining the entire acute migraine drugs market is the persistent underdiagnosis and mismanagement of migraine in general practice settings. The majority of migraine sufferers first present to primary care physicians rather than neurologists, yet these frontline providers receive minimal headache medicine training during medical school or residency. Consequently, migraine is frequently mislabeled as sinus headache, tension-type headache, or stress-related symptoms, leading to inappropriate prescriptions of antibiotics, muscle relaxants, or opioids, with agents that have no evidence base for migraine and may exacerbate the condition.

Acute Migraine Drugs Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.4% |

|

Base Year Market Size (2025) |

USD 7.3 billion |

|

Forecast Year Market Size (2035) |

USD 16.3 billion |

|

Regional Scope |

|

Acute Migraine Drugs Market Segmentation:

Availability Segment Analysis

Based on the availability segment, the prescription drugs sub-segment is anticipated to garner the largest share of 78.8% in the acute migraine drugs market. The sub-segment’s upliftment is primarily attributed to its importance for aiding rare diseases, optimizing quality of life, and managing temporary illnesses. According to official statistics published by the JMCP Organization in August 2024, a clinical study was conducted on 2,307 patient pairs to evaluate the difference between migraine-based and all-cause expenses. The study resulted in the payers’ pricing of galcanezumab, which is a prescription monoclonal antibody injection, amounting to USD 4,321, in comparison to USD 5,033 for standard-of-care (SOC) preventive migraine treatments. Besides, there was an increase in the expense of galcanezumab by USD 24,704 when compared with the pharmacy costs of USD 9,507. Therefore, this demonstrates suitable cost savings that are incurred with preventive migraine treatment, which is fueling the sub-segment’s growth.

Age Group Segment Analysis

During the forecast period, the adults sub-segment, part of the age group segment, is projected to capture the second-largest share in the acute migraine drugs market. The sub-segment’s growth is highly driven by bearing the highest disease burden because migraine onset peaks during the reproductive and peak working years, creating a profound intersection of medical need and economic productivity. Adults experience migraine attacks with greater frequency and severity compared to pediatric or geriatric populations, driven by hormonal fluctuations, occupational stress, irregular sleep patterns, and lifestyle triggers unique to this life stage. For women in this group, the association between menstrual cycles and migraine significantly increases attack frequency, while professional demands often delay treatment seeking until pain becomes debilitating.

Treatment Type Segment Analysis

By the end of the stipulated timeline, the acute (abortive) treatment segment, which is part of the treatment type, is expected to account for the third-largest share in the acute migraine drugs market. The segment’s development is strongly propelled by the advantage of combating headaches since its inception, reducing pain, attack duration, and symptom severity, including light sensitivity and nausea. As per an article published by NLM in January 2023, migraine impacts almost 12% of adults, with an increased prevalence in 18% of the female population and 6% in the male population. In this regard, over 70% of migraine-based visits are made to primary care providers in the U.S., playing a crucial role in managing and diagnosing acute migraine. Therefore, with the increased prevalence and treatment facilities, the segment is eventually gaining exposure.

Our in-depth analysis of the acute migraine drugs market includes the following segments:

|

Segment |

Subsegments |

|

Availability |

|

|

Age Group |

|

|

Treatment Type |

|

|

Route of Administration |

|

|

Distribution Channel |

|

|

Drug Class |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Acute Migraine Drugs Market - Regional Analysis

North America Market Insights

North America in the acute migraine drugs market is anticipated to garner the highest share of 45.6% by the end of 2035. The market’s upliftment is highly driven by an increase in the disease prevalence, strong healthcare infrastructure, the rapid adoption of notable targeted therapies, the presence of suitable reimbursement policies, intensive research and development investments, and strong patient advocacy. According to official statistics published by the IPSOR Organization in August 2025, the U.S. comprises a population of over 330 million people, and is readily supported by complex healthcare systems globally. Additionally, KFF, which is the leading health policy in the country, indicated that 48.7% of the population have private insurance coverage through an employer, 6.3% receive it through health insurance, followed by 21.2% depending on Medicaid, and 14.6% on Medicare, along with 1.3% on other public insurance forms, thus enabling an increased acute migraine drugs market growth in the overall region.

Uninsured, Public, and Private Coverage for Adults in the U.S., 2019-2022

|

Year |

Uninsured |

Public |

Private |

|

2019 |

14.7% |

20.4% |

66.8% |

|

2020 |

13.9% |

20.5% |

67.5% |

|

2021 |

13.5% |

21.7% |

66.6% |

|

2022 |

12.2% |

22.0% |

67.8% |

Source: IPSOR Organization

The acute migraine drugs market in the U.S. is growing significantly, owing to an increase in the presence and availability of receptor antagonists, clinical recognition of migraine-based comorbidities, integrated care models, non-pharmacological approaches, and efficient medications. As stated in an article published by the NIH in December 2025, β2 Adrenergic receptors are significantly encoded on chromosome 5 and primarily predominated on muscle cells of the airways. Likewise, β2 receptors are part of the G-protein–coupled receptor (GPCR), comprising 7 transmembrane helices, along with a short intracellular helix, which is usually known as helix 8 that lies parallel to the membrane. Moreover, the extracellular loops tend to facilitate ligand binding, while intracellular loops interact with the G protein, thus creating a positive impact on the market development.

The public formulary management, regional variation for drug accessibility, the adoption of non-oral delivery systems, clinical guidelines, the adoption of acupuncture and neutral stimulators, and provincial drug plans are certain factors that are uplifting the acute migraine drugs market in Canada. As per an article published by the Innovative Medicines Canada in July 2023, 18% of the newest medicines introduced worldwide are easily available through the domestic public drug plans. Besides, in March 2023, IMC declared a National Strategy for Drugs for Rare Diseases, which comprised USD 1.5 billion for more than 3 years to support the implementation. In addition, this particular funding province assisted in optimizing accessibility to the latest and emerging drugs, along with access enhancement to present drugs, screening processes, and early diagnosis, thus proliferating the market access.

APAC Market Insights

The Asia Pacific in the acute migraine drugs market is expected to emerge as the fastest-growing region during the forecast period. The market’s development is highly propelled by the massive undiagnosed patient population, an improvement in healthcare facilities, an upsurge in migraine awareness, rapid urbanization, and the universal health insurance system. According to official statistics published by NLM in May 2025, China comprised the highest migraine burden, with 13 million cases, along with 184.7 million prevalent cases, followed by South Korea, Japan, and Australia. Based on this, incidence rates peaked among adolescents, ranging between 10 and 14 years, and meanwhile, the disability and prevalence were highest among middle-aged women from 40 to 44 years. Therefore, with this upsurge in the incidence, there is a huge demand for the market in the overall region.

The acute migraine drugs market in China is gaining increased traction, owing to modernization in the healthcare system, an increase in disease awareness, an escalation in approval duration, the sustained demand for both preventive and acute treatments, and optimization in patient accessibility. As stated in an article published by NLM in May 2023, the country has a total of 1,030,935 healthcare centers, with 36,570 hospitals and 977,790 primary-based clinics. In addition, there also exist 3,275 tertiary hospitals, which are frequently affiliated with hospital-based universities and large-scale medical facilities. Apart from these, the country also has 10,848 secondary hospitals, which are medium-sized hospitals across counties and districts. Moreover, there are 9,798 unclassified hospitals and 12,649 primary hospitals, thereby creating suitable growth opportunities for the acute migraine drugs market in the country.

The aspects of government expenditure on drugs, an increase in treatment facilities, generous funding for neurology workforce training, headache management programs, the incorporation of a telemedicine platform, an administrative awareness program, and suitable accessibility to targeted therapies are a few trends that are responsible for expanding the acute migraine drugs market in India. Based on government estimates published by the PIB in March 2026, the Ayushman Bharat scheme offers subsidized care to the total population through insurance, 863 million digitalized health IDs, and more than 184,000 primary healthcare facilities. Besides, the country effectively supplies 20% of worldwide generic medicines, along with 55% to 60% of UNICEF’s vaccines, as well as a bioeconomy growth towards USD 300 billion by the end of 2030. Therefore, with all these developments, the market is gradually expanding in the country.

Europe Market Insights

Europe in the acute migraine drugs market is projected to withstand a considerable share by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by continuously evolving clinical guidelines, expanded accessibility to target therapies, a surge in the disease prevalence, the availability of fixed-dose combination products, and reimbursement approvals. According to official statistics published by NLM in January 2025, a clinical study was conducted on 7,311 respondents with diagnosed migraines, which represented approximately 30.5 million adults, with a weighted prevalence of 11.5% across five countries in the region. Based on this, Spain has the highest prevalence, accounting for 14%, followed by Germany, the UK, France, and Italy. Besides, the study proclaimed that 56% of respondents reported disability due to the disease, with the highest percentage in Germany, with 66%, thereby ensuring the market expansion in the overall region.

The acute migraine drugs market in Germany is gaining increased exposure, owing to the comprehensive and early adoption of target therapies, the presence of a decentralized statutory health insurance system, an increase in reimbursement decisions, the inclusion of monoclonal antibodies, and patient demand for non-injectable administration. As stated in an article published by the NIH in December 2024, nearly 87% of the population, which is over 70 million people, comprises public health insurance. Besides, the Versicherungspflichtgrenze, which is the yearly income level of the country, amounted to USD 86,179.9 as of 2025, is also contributing to the public health insurance aspect. In this regard, the basic health insurance premium accounts for 14.6% of gross income, and the yearly income level in 2025 was USD 77,264.1, thus denoting an optimistic outlook for the market growth.

The evolving clinical pathways, governmental investments, direct medical expenses, priority towards therapies, issuing positive guidance for eligible patients, a shift towards ditans and gepants, and the presence of long-lasting neurological diseases are a few factors that are positively fueling the acute migraine drugs market in the UK. As per an article published by the UK Government in April 2026, Sure Start, which is a government-based initiative in England, indicated that every USD 1.3 of up-front investment in the initiative generated an estimated USD 2.6 in long-lasting direct and indirect benefits. Additionally, this particular government coverage substantially diminished the likelihood of hospitalization during both childhood and adolescence, thereby making a suitable contribution to the increased demand of the market in the overall country.

Key Acute Migraine Drugs Market Players:

- GlaxoSmithKline (UK)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Merck & Co., Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Eli Lilly and Company (U.S.)

- AbbVie Inc. (U.S.)

- Bayer AG (Germany)

- AstraZeneca plc (UK)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy's Laboratories Ltd. (India)

- Cipla Limited (India)

- Lupin Limited (India)

- Aurobindo Pharma Limited (India)

- Grünenthal GmbH (Germany)

- Endo International plc (Ireland)

- Eisai Co., Ltd. (Japan)

- SK Chemicals Co., Ltd. (South Korea)

- Zydus Lifesciences Limited (India)

- Axsome Therapeutics, Inc. (U.S.)

- Amneal Pharmaceuticals, Inc. (U.S.)

- Satsuma Pharmaceuticals, Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- GlaxoSmithKline has historically been a foundational player in the acute migraine space, largely due to its pioneering development and commercialization of triptans. The company continues to leverage its neurology expertise to maintain a presence in the market, though its focus has increasingly shifted toward specialty care and respiratory portfolios.

- Pfizer Inc. has aggressively expanded its migraine portfolio through strategic acquisitions, most notably gaining access to a leading oral CGRP antagonist approved for acute treatment. The company focuses on integrating digital health tools with its migraine therapies to enhance patient engagement and treatment adherence.

- Novartis AG maintains a significant presence in migraine management through collaborative agreements that combine its development capabilities with partners' novel assets. The company emphasizes personalized medicine approaches and has invested in broadening access to innovative acute therapies across global markets.

- Teva Pharmaceutical Industries Ltd. brings a dual strategy to the acute migraine market, offering both branded specialty products and a broad portfolio of generic triptans and ergot derivatives. The company leverages its established global supply chain to deliver cost-effective acute treatment options, particularly in price-sensitive healthcare systems.

- Merck & Co., Inc. has historically contributed to the acute migraine landscape with its ergot alkaloid-based formulations that remain in use for refractory cases. The company continues to evaluate neurology opportunities while balancing investment across its broader pharmaceutical pipeline.

Here is a list of key players operating in the global acute migraine drugs market:

The acute migraine drugs market features a competitive environment where large multinational pharmaceutical companies compete alongside specialty generic drug manufacturers from Asia. The market has experienced significant consolidation, with major players aggressively acquiring smaller biotech firms to gain access to innovative CGRP-targeting therapies and ditans. Strategic initiatives include extensive research and development investments in novel drug delivery mechanisms such as intranasal sprays and orally disintegrating tablets to improve patient compliance. Besides, in January 2025, Axsome Therapeutics, Inc. received the U.S. FDA approval for its SYMBRAVO®, which is ideal for the acute treatment of migraine among adults. This approval has been possible through thorough research, which is positively contributing to the acute migraine drugs industry globally.

Corporate Landscape of the Acute Migraine Drugs Market:

Recent Developments

- In August 2025, Teva Pharmaceuticals gained the U.S. FDA acceptance for AJOVY for the preventive treatment of episodic migraine among children and adolescent patients aged between 6 and 17 years, along with a weight of 45 kilograms.

- In May 2025, Amneal Pharmaceuticals, Inc. declared the approval for Brekiya® injection by the U.S. FDA, which is the first-ever and only dihydroerhotamine autoinjector for the acute treatment of migraine as well as cluster headaches among adults.

- In April 2025, Satsuma Pharmaceuticals, Inc., along with its corporate parent, Shin Nippon Biomedical Laboratories, Ltd., received the acceptance of a 505(b)(2) New Drug Application (NDA) for Atzumi™ nasal powder by the U.S. FDA for aiding migraine among the adult population.

- Report ID: 8535

- Published Date: Apr 28, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.