Anesthesia Monitoring Devices Market Outlook:

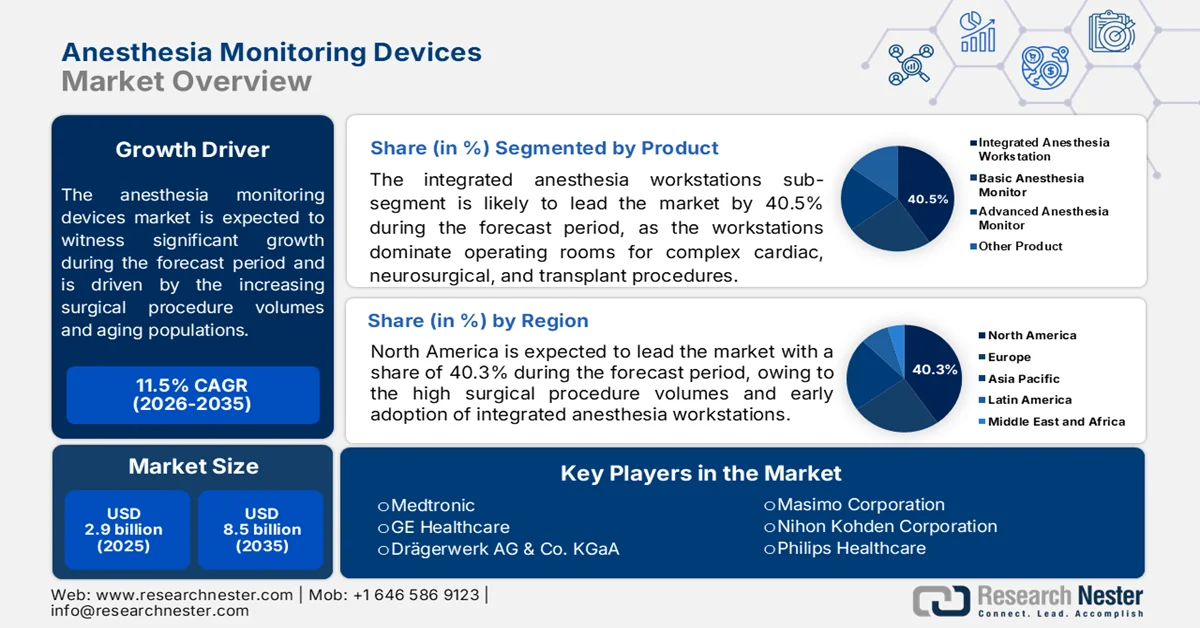

Anesthesia Monitoring Devices Market size was valued at USD 2.9 billion in 2025 and is projected to cross USD 8.5 billion by the end of 2035, growing at more than 11.5% CAGR during the forecast period i.e., 2026-2035. In 2026, the industry size of anesthesia monitoring devices is assessed at USD 3.2 billion.

The anesthesia monitoring devices market is expanding in response to the increasing surgical procedure volumes, aging populations, and the stronger regulatory emphasis on perioperative patient safety. The World Health Organization (WHO) in September 2023 estimates that more than 300 million surgical procedures are performed each year globally, creating sustained demand for continuous monitoring systems across operating rooms, ambulatory surgical centers, and intensive care units. Government-backed healthcare infrastructure investments are also supporting the procurement of advanced physiological monitoring technologies. In the U.S., the Centers for Medicare & Medicaid Services (CMS) January 2026 data reported national health expenditure growth of 7.2% in 2024, with hospital care remaining the largest spending category. Higher procedural spending has accelerated the adoption of the integrated anesthesia workstations equipped with capnography, pulse oximetry, electrocardiography, and gas monitoring capabilities.

The anesthesia monitoring devices market is witnessing increasing demand for advanced perioperative monitoring systems as healthcare providers focus on reducing anesthesia-related complications and improving surgical outcomes. According to the NLM February 2026 study, nearly 37.1% of anesthesiologists frequently use anesthesia depth monitoring, and neuromuscular blockade monitoring adoption remains low at 9.7%, highlighting a substantial untapped demand for objective monitoring technologies in operating rooms. The study also found that 72.1% of clinicians frequently use nociception monitoring, reflecting growing interest in individualized analgesia management. However, high equipment costs limited device availability, and continued reliance on the conventional clinical assessment methods remains a major barrier to wider adoption. These gaps are expected to support procurement opportunities for the hospitals seeking standardized perioperative monitoring systems and compliance with patient safety protocols.

Key Anesthesia Monitoring Devices Market Insights Summary:

Regional Highlights:

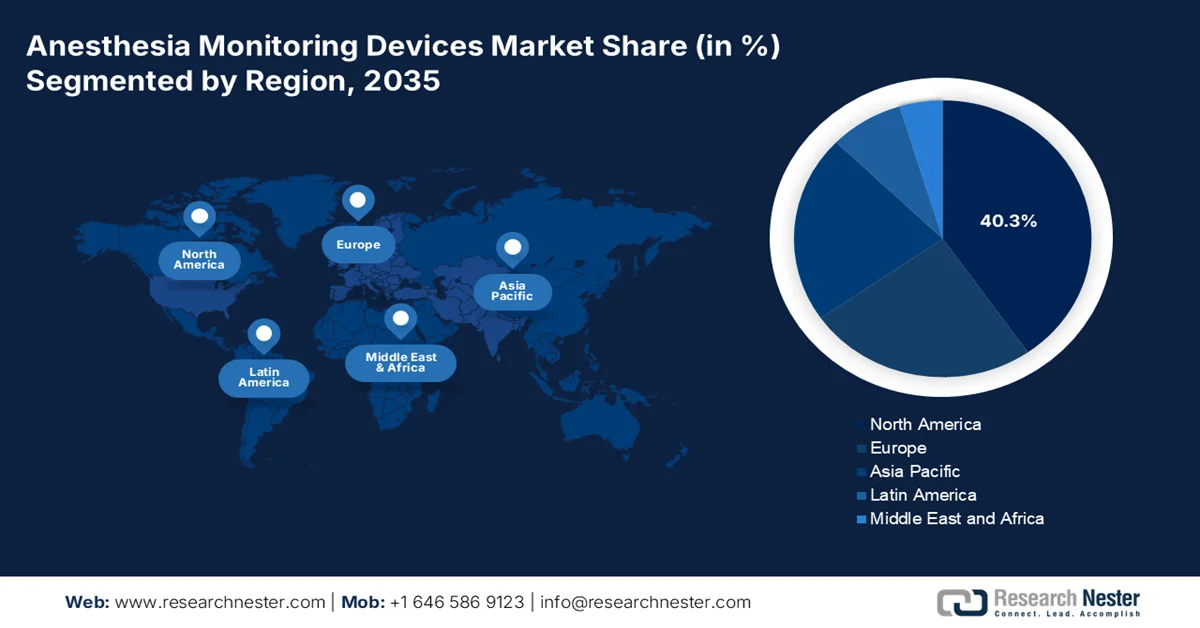

- The anesthesia monitoring devices market in North America is projected to command a 40.3% share by 2035, supported by rising surgical procedure volumes, stringent patient safety standards, and growing adoption of integrated anesthesia monitoring technologies

- Asia Pacific is anticipated to witness the fastest CAGR in the market during 2026-2035, stimulated by rapid hospital infrastructure modernization, increasing surgical volumes, and expanding medical tourism investments

Segment Insights:

- The integrated anesthesia workstation sub-segment is expected to account for a 40.5% share of the anesthesia monitoring devices market by 2035, propelled by increasing demand for automated safety checks, AI-driven decision support, and real-time anesthesia monitoring in complex surgical procedures

- Hospitals are projected to remain the dominant end user segment in the market by 2035, reinforced by rising investments in advanced monitoring systems for robotic and minimally invasive surgeries alongside the need for centralized surveillance and electronic medical record connectivity

Key Growth Trends:

- Increasing global surgical volumes

- Expansion of aging population

Major Challenges:

- Escalating tariffs and trade barriers

- Stringent clinical validation and evidence requirements

Key Players: Medtronic, GE Healthcare, Drägerwerk AG & Co. KGaA, Masimo Corporation, Nihon Kohden Corporation, Philips Healthcare, Mindray Medical International, Schiller AG, Smiths Medical, Edwards Lifesciences, Nonin Medical, Infinium Medical, Fukuda Denshi, Spacelabs Healthcare, Contec Medical Systems, BPL Medical Technologies, Shenzhen Comen Medical Instruments, Mediana, Heyer Medical AG, Boston Scientific Corporation.

Global Anesthesia Monitoring Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.9 billion

- 2026 Market Size: USD 3.2 billion

- Projected Market Size: USD 8.5 billion by 2035

- Growth Forecasts: 11.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, United Kingdom

- Emerging Countries: India, Indonesia, Malaysia, South Korea, Australia

Last updated on : 15 May, 2026

Anesthesia Monitoring Devices Market - Growth Drivers and Challenges

Growth Drivers

- Increasing global surgical volumes: The growing number of surgical procedures continues to expand the installed base requirement for anesthesia monitoring devices. According to the Open Anesthesia January 2025 data, nearly 143 million surgical procedures are needed each year to meet the unmet clinical demand. Rising procedure volumes in orthopedics, cardiovascular surgery, oncology, and emergency care are increasing the need for the continuous monitoring of oxygenation, ventilation, anesthetic depth, and neuromuscular blockade. Governments are investing in surgical system expansion to reduce waiting times and improve perioperative outcomes. Higher procedural throughput is encouraging hospitals to deploy a scalable monitoring platform capable of supporting high-acuity operating room environments and ambulatory surgery centers.

Global Surgical Volume and Access Burden

|

Indicator |

Statistics / Findings |

|

Population lacking access to safe surgical and anesthesia care |

Over 5 billion people globally lack access to safe surgical and anesthesia services |

|

Annual unmet surgical procedure demand |

Approximately 143 million additional surgeries are required annually worldwide |

|

Global surgeries performed in low-income countries |

Low-income countries account for only 6% of global surgeries despite representing over one-third of the world’s population |

|

Deaths from untreated surgical conditions |

16.9 million deaths were linked to untreated surgical conditions in 2010 |

|

Annual deaths linked to lack of surgical access |

Around 4.7 million deaths annually occur due to untreated surgical conditions in LMICs |

|

Share of global disease burden related to surgical conditions |

Surgical diseases account for approximately 30% of the global disease burden |

|

Potential preventable deaths through expanded surgical access |

Expanding essential surgical services could prevent approximately 1.5 million deaths annually in LMICs |

|

Workforce shortages affecting surgical capacity |

Global shortage of 550,000 anesthesiologists and 1.1 million surgeons |

|

Anesthesia-related mortality in LMICs |

Anesthesia-related death rates may be up to 100 times higher in LMICs compared with high-income countries |

Source: Open Anesthesia January 2025

- Expansion of aging population: Population aging and increasing chronic disease prevalence are significantly increasing the demand for perioperative monitoring technologies. The United Nations January 2025 data estimates that the global population aged 65 years and above will exceed 1.5 billion by 2050, increasing surgical intervention rates. Older patients frequently require advanced physiological monitoring during anesthesia because of higher cardiovascular and respiratory risk profiles. Moreover, many adults live with at least one chronic disease. Chronic diseases such as cancer, diabetes, obesity, and cardiovascular disorders are associated with higher surgical utilization and longer perioperative monitoring requirements. Hospitals are prioritizing advanced anesthesia monitoring systems capable of supporting high-risk patient management, predictive alarm systems, and integrated hemodynamic analysis to reduce perioperative complications and improve recovery outcomes.

- Increasing investments in ambulatory surgical centers: Governments and healthcare systems are increasingly shifting surgical procedures toward the ambulatory surgical centers (ASCs) and the outpatient facilities to reduce inpatient costs and improve procedural efficiency. This transition is expanding the demand for compact, portable, and integrated anesthesia monitoring systems. Outpatient hospital spending and ASC utilization have steadily increased due to the reimbursement reforms pushing for same-day surgeries. Minimally invasive procedures, including laparoscopic and robotic surgeries, require continuous anesthesia monitoring despite shorter recovery durations. Portable capnography, pulse oximetry, and multi-parameter monitoring systems are therefore becoming standard procurement priorities in outpatient environments. Vendors are responding by introducing lightweight wireless monitoring systems with centralized data integration capabilities suitable for high-turnover outpatient surgical environments and decentralized care facilities.

Challenges

- Escalating tariffs and trade barriers: Manufacturers face significant cost disadvantages when entering foreign markets due to the protectionist trade policies. For example, the U.S. tariffs on Chinese medical devices directly increase the landed cost of anesthesia monitors, eroding price competitiveness for new players who rely on cross-border supply chains. This challenge forces companies to either absorb costs or raise prices, both of which are detrimental during initial anesthesia monitoring devices market penetration.

- Stringent clinical validation and evidence requirements: Payers and clinicians demand robust evidence that a new monitoring parameter improves patient outcomes, such as reducing intraoperative awareness. Generating this data is expensive and time-consuming. New players in the anesthesia monitoring devices market often face problems such as needing sales to fund studies, but hospitals require studies before purchasing. Many innovative startups seek strategic partnerships with academic medical centers or secure venture capital funding specifically earmarked for phase III/IV clinical trials, allowing them to generate the necessary evidence without relying on initial product sales revenue.

Anesthesia Monitoring Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.5% |

|

Base Year Market Size (2025) |

USD 2.9 billion |

|

Forecast Year Market Size (2035) |

USD 8.5 billion |

|

Regional Scope |

|

Anesthesia Monitoring Devices Market Segmentation:

Product Segment Analysis

The integrated anesthesia workstation is the leading sub-segment within the product segment and is expected to hold the share value of 40.5% by the end of 2035. These workstations dominate operating rooms for complex cardiac, neurosurgical, and transplant procedures. According to the Health Management March 2025 adverse event reports, related to anesthesia delivery decreased by approximately 18% following the adoption of fully integrated systems with automated safety checks. Moreover, U.S. hospitals performing annual surgeries had replaced modular setups with integrated workstations. Key drivers include reduced user error, real-time alarm integration, and electronic anesthesia record-keeping. Manufacturers focus on closed-loop target-controlled infusion and artificial intelligence-driven decision support, making integrated workstations the standard of care in high-volume surgical centers.

End user Segment Analysis

Hospitals are the leading sub-segment under the end user segment in the anesthesia monitoring devices market in 2035. Tertiary hospitals in the U.S. increased their anesthesia monitoring device budgets to support complex multidisciplinary surgeries. Data from the OIG July 2025 report indicates that anesthesia was administered to 18% of 3.9 million sessions in SPM procedures. The hospitals prioritize advanced monitors with connectivity to electronic medical records and centralized surveillance systems. The growing volume of robotic and minimally invasive surgeries requires real-time depth-of-anesthesia and hemodynamic monitoring, which only tertiary centers can fully fund. Consequently, hospitals continue to dominate procurement, especially for integrated workstations and multi-parameter monitors.

Portability Segment Analysis

In the anesthesia monitoring devices market, the portability segment is led by standalone monitors, which dominate the fixed operating room environments due to their reliability, uninterrupted power supply, and seamless integration with anesthesia workstations. These monitors support continuous multi-parameter tracking, including depth of anesthesia, gas exchange, hemodynamics, and neuromuscular function, without the risk of signal interference or battery depletion associated with the wireless devices. Anesthesiologists prefer wired systems for prolonged and high acuity surgeries where data latency is unacceptable. While handheld and wearable wireless monitors are gaining traction in ambulatory surgery centers and field hospitals, standalone wired monitors remain the gold standard for major procedures such as cardiac, neurosurgical, and transplant operations. Their robust connectivity to central nursing stations and electronic medical records ensures real-time decision support, positioning them as the backbone of perioperative monitoring in tertiary care hospitals.

Our in-depth analysis of the anesthesia monitoring devices market includes the following segments:

|

Segment |

Subsegments |

|

Product |

|

|

Patient Age Group |

|

|

End user |

|

|

Portability |

|

|

Parameter Monitored |

|

|

Component |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Anesthesia Monitoring Devices Market - Regional Analysis

North America Market Insights

North America is dominating the anesthesia monitoring devices market and is poised to hold a regional share of 40.3% by the end of 2035. The market is driven by high surgical procedure volumes, early adoption of integrated anesthesia workstations, and a strong emphasis on patient safety standards. hospitals and ambulatory surgery centers across the region prioritize depth of anesthesia monitoring, capnography, and hemodynamic tracking as standard of care. Regulatory bodies have progressively expanded monitoring requirements beyond operating rooms into procedural sedation areas such as endoscopy suites and dental clinics. Moreover, the shift toward value-based care promotes the investment in monitors that reduce complications, shorten recovery times, and improve perioperative workflow efficiency, solidifying North America’s leadership position.

Increasing surgical volumes, rising geriatric populations, and continued hospital investment in perioperative safety technologies are shaping the anesthesia monitoring devices market in the U.S. According to the NLM November 2023 study, more than 40 to 50 million surgical procedures are performed annually in U.S. hospitals, creating sustained demand for anesthesia depth, neuromuscular, and physiological monitoring systems. Moreover, the U.S. Census Bureau's June 2025 data indicates that the population aged 65 years and older is projected to increase by 3.1%, driving higher rates of complex surgeries requiring advanced monitoring. Industry adoption is also accelerating via large-scale hospital installations and product innovation. In December 2025, Blink Anesthesia installed 119 TwitchView® Train-of-Four monitoring systems at a leading U.S. academic medical center. In addition, GE HealthCare in October 2025 introduced the FDA 510(k)-pending Carestation™ 850 anesthesia delivery platform in 2025, reflecting ongoing technological upgrades across the U.S. operating rooms. These data show an active anesthesia monitoring devices market growth in the U.S.

The rising surgical volumes, demographic aging, and growing clinical focus on perioperative efficiency and anesthesia research are driving the anesthesia monitoring devices market in Canada. According to the NLM April 2024 study Canada anesthesiology departments have published 3,490 research articles within 2023, reflecting sustained institutional emphasis on improving anesthesia practices, monitoring standards, and patient safety protocols. Surgical demand remains strong, with the NLM June 2022 study depicting that Canadian surgeons performed more than 2.3 million procedures annually, increasing the utilization of anesthesia monitoring systems across hospitals and outpatient facilities. Demographic trends are also supporting long-term market growth, as the 2026 Canadian Medical Association reported approximately 7.6 million people aged 65 years and older in 2023, representing 18.9% of the national population, with seniors projected to account for up to 23.4% by 2030. The growing elderly population is increasing demand for advanced perioperative monitoring technologies during high-risk and complex surgeries.

APAC Market Insights

The Asia Pacific is projected to expand at the fastest CAGR during the assessed period, 2026 to 2035, in the anesthesia monitoring devices market. The region is defined by the rapid modernization of public hospital infrastructure, increasing surgical volumes, and a growing focus on patient safety standards across both mature and emerging economies. Countries such as Japan, South Korea, and Australia lead in adopting integrated anesthesia workstations and depth of monitoring technologies, while China, India, Indonesia, and Malaysia are witnessing stimulating procurement of basic and mid-tier monitors for expanding secondary and tertiary care facilities. Additionally, the rise of medical tourism in Southeast Asia is driving private hospital chains to upgrade anesthesia monitoring systems to international accreditation standards, fostering competition among global and regional manufacturers.

The rising healthcare expenditure and increasing demand for surgical and critical care services are driving the anesthesia monitoring devices market in India. According to the ASSOCHAM October 2024 data, India’s total healthcare expenditure increased from USD 9.4 billion in 2023 to 2024 to USD 10.7 billion in 2024 to 2025, strengthening investments in hospital infrastructure and perioperative care capacity. Budget allocation under the Pradhan Mantri Ayushman Bharat Health Infrastructure Mission (PMABHIM) also nearly doubled from USD 250.6 million to USD 490.2 million in 2024 to 2025, supporting the modernization of healthcare facilities and monitoring capabilities. Disease burden trends are also contributing to market expansion, as non-communicable diseases accounted for nearly 5.87 million deaths and approximately 226.8 million DALYs in India, as per the NLM March 2024 study, increasing the need for advanced anesthesia and patient monitoring systems during complex surgical procedures.

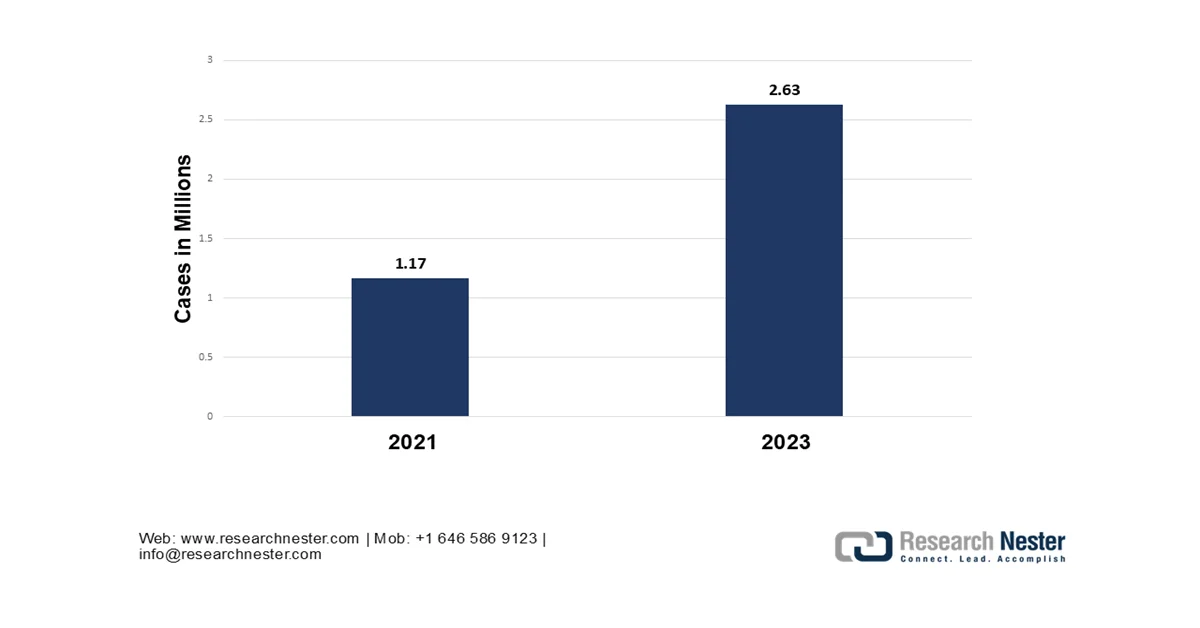

Japan anesthesia monitoring devices market reached USD 552.5 million in 2025 and is poised to reach USD 1,180.5 million by the end of 2035 at a CAGR of 7.9% during the forecast period 2026 to 2035. The market is projected to exceed USD 596.1 million in 2026. The nation is driven by the increasing surgical demand and rapid population aging. The national medical expenditure reflects continued investment in hospital and perioperative care infrastructure. According to the NLM January 2025 study, the total surgeries performed in the nation were 2.63 million, increasing demand for advanced monitoring during high-risk surgeries. Additionally, the Pharmaceuticals and Medical Devices Agency (PMDA) reported continued approvals of advanced patient monitoring technologies supporting the modernization of operating room systems across Japanese healthcare facilities.

Number of Surgical Procedures in Japan, 2023

Source: NLM January 2025

Europe Market Insights

The anesthesia monitoring devices market in Europe is shaped by the stringent regulatory frameworks, harmonized medical device standards under the EU MDR, and a strong emphasis on perioperative patient safety across both the Western and Eastern regions. Germany, France, Italy, Spain, and the UK lead in the deployment of integrated anesthesia workstations with advanced gas analysis and depth of monitoring capabilities. The Nordics prioritize interoperable systems connected to national electronic health records. Public procurement via national health systems drives demand for cost-effective, reliable monitors with standardized connectivity protocols. Emerging trends include the adoption of portable monitors for ambulatory surgery centers and the regional anesthesia procedures, as well as increased focus on capnography for sedation outside operating rooms. Russia and Eastern European markets are gradually modernizing legacy Soviet era equipment, creating opportunities for value-engineered monitoring solutions without compromising clinical safety standards.

The increasing hospital digitization, high surgical procedure volumes, and rising healthcare expenditure are driving the anesthesia monitoring devices market in Germany. According to the Federal Statistical Office of Germany (Destatis), 2026 data, healthcare expenditure was 474 billion euros, reflecting continued investment in hospital infrastructure and advanced clinical technologies. Destatis 2026 data also reported that people aged 67 years and older represented more than 20% of Germany’s population in 2024, increasing demand for perioperative monitoring during age-related surgical procedures. Moreover, Germany’s Federal Ministry of Health expanded funding under the Hospital Future Act to accelerate digital modernization of hospitals, including connected patient monitoring and operating room technologies. These initiatives are supporting the adoption of integrated anesthesia monitoring systems across German healthcare facilities.

The increasing elective procedures, aging demographics, and ongoing hospital modernization initiatives are driving the anesthesia monitoring devices market in the UK. According to the Government of the UK, January 2025 data, the elective care waiting list exceeded 7.5 million cases in 2024, increasing pressure on hospitals to expand the surgical capacity and perioperative monitoring capabilities. The Office for National Statistics reported in June 2022 that 18.9% of the UK population was aged 65 years and older, contributing to the higher volumes of complex surgeries requiring advanced anesthesia monitoring. Additionally, the UK government committed a billion for NHS technology and infrastructure upgrades, including digital operating rooms and patient monitoring improvements. These investments are supporting greater adoption of integrated anesthesia monitoring systems across hospitals and ambulatory surgical centers.

Key Anesthesia Monitoring Devices Market Players:

- Medtronic (U.S.)

- GE Healthcare (U.S.)

- Drägerwerk AG & Co. KGaA (Germany)

- Masimo Corporation (USA)

- Nihon Kohden Corporation (Japan)

- Philips Healthcare (Netherlands)

- Mindray Medical International (China)

- Schiller AG (Switzerland)

- Smiths Medical (UK)

- Edwards Lifesciences (U.S.)

- Nonin Medical (U.S.)

- Infinium Medical (U.S.)

- Fukuda Denshi (Japan)

- Spacelabs Healthcare (U.S.)

- Contec Medical Systems (China)

- BPL Medical Technologies (India)

- Shenzhen Comen Medical Instruments (China)

- Mediana (South Korea)

- Heyer Medical AG (Germany)

- Boston Scientific Corporation (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Medtronic is a dominant player in the anesthesia monitoring devices market, using its acquisition of Covidien to integrate the advanced capnography and cerebral oximetry into anesthesia workstations. The company focuses on developing comprehensive patient monitoring platforms that combine hemodynamic gas exchange and depth of anesthesia parameters. In 2024, the company generated a revenue of USD 8.6 billion in Q4.

- GE Healthcare maintains a stronghold in the anesthesia monitoring devices market via its modular monitoring platform and B850 anesthesia monitor. The company prioritizes interoperability, enabling seamless data flow between anesthesia devices and electronic medical records. The company continues to drive innovation in the anesthesia monitoring devices market, supporting both pediatric and adult anesthesia care. In 2025, the company made a revenue growth of 2%.

- Dragerwerk AG & Co. KGaA is a longstanding leader in the anesthesia monitoring devices market, renowned for its integrated anesthesia workstations and patient monitors. The company’s strategic initiatives focus on closed-loop anesthesia delivery and smart alarm management to reduce cognitive load on clinicians. The company strengthens its position in the anesthesia monitoring devices market, particularly across Europe and emerging economies.

- Masimo Corporation has transformed the anesthesia monitoring devices market by introducing non-invasive continuous hemoglobin and oxygen content monitoring alongside its core SET pulse oximetry. The company platform allows seamless integration of anesthesia gas monitoring, sedation tracking, and brain function indices. By focusing on signal extraction technology and reducing false alarms, Masimo drives safety and portability in the anesthesia monitoring devices market.

- Nihon Kohden Corporation is a key player in the anesthesia monitoring devices market, known for its Life Scope and CNS series. The company emphasizes integrated OR solutions combining anesthesia gas analysis, entropy modules, and standard vital signs. The strategic initiatives include developing AI-based predictive algorithms for hypotension and awareness during surgery, battery-operated monitors for field hospitals.

Here is a list of key players operating in the global anesthesia monitoring devices market:

The anesthesia monitoring devices market is highly consolidated and is led by the established multinationals with broad product portfolios and integrated anesthesia delivery solutions. The key players focus on strategic initiatives such as mergers and acquisitions, technological advancements in AI-driven depth of anesthesia monitors, and portable devices for low-resource settings. For example, in October 2025, Boston Scientific Corporation announced it had entered into a definitive agreement to acquire Nalu Medical, Inc. Companies are also emphasizing connectivity with electronic medical records and telemedicine capabilities. Emerging manufacturers from Asia, mainly China and India, are gaining share via cost-effective, reliable devices. Intense R&D investments aim to improve patient safety, reduce alarm fatigue, and enhance non-invasive hemodynamic monitoring, driving a shift toward value-based integrated operating room ecosystems.

Corporate Landscape of the Anesthesia Monitoring Devices Market:

Recent Developments

- In October 2025, Philips and Getinge formed a new commercial partnership in Europe to offer customers easier access to a complete anesthesia and monitoring solution. By combining Philips’ monitoring solutions with Getinge’s leading anesthesia care products, the partnership provides a single point of contact for purchasing and support, helping clinicians deliver high-quality care in the operating room.

- In March 2024, Medtronic plc, a global leader in healthcare technology, announced U.S. Food and Drug Administration (FDA) 510(k) clearance for the BIS™ Advance monitor. The new BIS™ Advance monitor delivers the clinically validated BIS™ algorithm with a completely redesigned interface that is easy to configure and use.

- In November 2024, Mindray unveiled exciting upgrades to its A7 and A5 anesthesia systems under the A Series Anesthesia. The brand-new enhancements incorporate innovative technologies that empower anesthesiologists to deliver precise anesthesia, leading to greater patient safety and efficiency throughout the perioperative period.

- Report ID: 8033

- Published Date: May 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.