Alcohol Packaging Market Outlook:

Alcohol Packaging Market size was valued at USD 73.8 billion in 2025 and is projected to reach USD 133.4 billion by the end of 2035, rising at a CAGR of 6.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of alcohol packaging is assessed at USD 78.3 billion.

The market is structurally supported by the sustained production volumes, regulatory compliance requirements, and the international trade flows documented by the government and intergovernmental agencies. According to the Congress.gov September 2024 report, the U.S. Alcohol and Tobacco Tax and Trade Bureau, federal excise tax collections from distilled spirits, wine, and beer exceeded USD 10 billion annually in recent fiscal years, reflecting stable packaged alcohol output moving through regulated supply chains. Moreover, the Distilled Spirits Council's October 2025 data indicates that the total U.S. spirits exports in 2024 reached USD 2.45 billion, which is a rise of 10% from 2023, indicating large-scale primary and secondary packaging demand across glass, metal, and corrugated formats.

Besides, the global alcoholic beverages market size accounted for USD 1.75 trillion in 2023 as per the NLM study in November 2024, underscoring a consistent packaging volume requirement across domestic and export channels. Further, the production levels directly translate into high volume procurement of bottles, cans, labels, and transport packaging, mainly in markets with established retail and export infrastructure. According to the OEC 2024 report, the global trade of beverages, spirits, and vinegar reached USD 151 billion, highlighting cross-border labeling compliance and durability requirements that shape packaging specifications. Further, the production scale, environmental regulation, and international trade controls form the principal structural drivers of alcohol packaging demand across the mature and emerging markets.

Key Alcohol Packaging Market Insights Summary:

Regional Highlights:

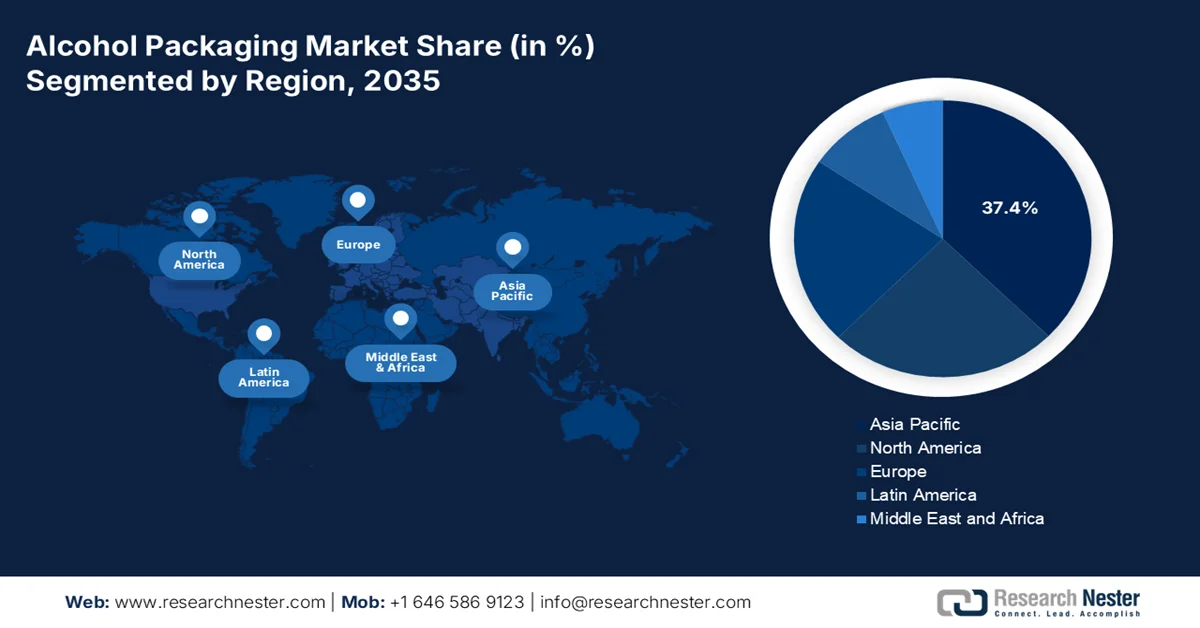

- By 2035, Asia Pacific in the alcohol packaging market is projected to secure a 37.4% share, fueled by expanding middle-class alcohol consumption in China and India alongside stringent regulatory formalization mandating track-and-trace and standardized labeling systems.

- During 2026–2035, North America is anticipated to be the fastest-growing region with a CAGR of 6.3%, stimulated by strong premiumization trends and high per capita expenditure on branded beer, wine, and spirits packaging.

Segment Insights:

- By 2035, beverage manufacturers as the leading end-user sub-segment in the alcohol packaging market are projected to command a 70.3% share, driven by the necessity for bulk primary packaging procurement and centralized purchasing contracts that influence material selection and order volumes across the value chain.

- Over the forecast period 2026–2035, the primary packaging sub-segment is expected to retain the largest share, propelled by its direct product-contact role and increasing premiumization trends demanding high-quality, regulation-compliant packaging materials.

Key Growth Trends:

- Environmental regulations and recycling mandates

- Aluminum can adoption and domestic capacity constraints

Major Challenges:

- Regulatory compliance and label approval delays

- Raw material price volatility and supply insecurity

Key Players: Ball Corporation (U.S.), Crown Holdings, Inc. (U.S.), Owens-Illinois, Inc. (O-I Glass) (U.S.), Ardagh Group S.A. (Luxembourg), Smurfit Kappa Group (Ireland), WestRock Company (U.S.), Berry Global Inc. (U.S.), Stora Enso Oyj (Finland), Verallia (France), Vidrala S.A. (Spain), Vetropack Holding AG (Switzerland), Gerresheimer AG (Germany), Amcor plc (UK), Mondi Group (UK), DS Smith Plc (UK), BA Glass (Portugal), TCPL Packaging Ltd. (India), Samhwa Crown & Closure (South Korea), Bright Packaging Industry Berhad (Malaysia), Meiji Rubber & Chemical Co., Ltd. (Japan)

Global Alcohol Packaging Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 73.8 Billion

- 2026 Market Size: USD 78.3 Billion

- Projected Market Size: USD 133.4 Billion by 2035

- Growth Forecasts: 6.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (37.4% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, United Kingdom, France

- Emerging Countries: India, Brazil, Mexico, South Korea, Australia

Last updated on : 18 February, 2026

Alcohol Packaging Market - Growth Drivers and Challenges

Growth Drivers

- Environmental regulations and recycling mandates: Packaging waste compliance is a structural demand driver in the market. According to the U.S. Environmental Protection Agency's October 2025 report, the containers and packaging accounted for 82.2 million tons of municipal solid waste, nearly 28% of total MSW. Aluminum beverage containers recycling was 670,000 tons, or 50.4% of generation. Further, the alcohol producers are prioritizing lightweight glass, recycled aluminum, and PCR content to meet the regulatory targets. Suppliers with certified input streams gain procurement advantage in Europe and North America. In addition, extended producer responsibility (EPR) frameworks across the EU and several U.S. states are imposing higher recovery and recycled content targets, accelerating investment in closed-loop packaging systems and traceable sustainable material sourcing.

- Aluminum can adoption and domestic capacity constraints: Aluminum cans are mostly used in beer and softdrink sales. According to the Mines 2025 report, per-capita Aluminum consumption in India has reached about 3.5 Kg in FY 2024. However, this remains significantly below, indicating a strong headroom for future demand expansion in beverage and alcohol packaging. Moreover, the growing beer consumption premiumization trends and shift toward ready-to-drink alcoholic beverages are surging the aluminum can penetration across urban markets. At the same time, the domestic rolling and can making capacity constraints, along with dependence on imported scrap and primary aluminum price volatility are tightening supply dynamics and influencing long term procurement contracts.

- Compliance driven packaging standardization: India’s mandatory Bureau of Indian Standards certification for the aluminum cans under the cookware utensils and cans for food and beverages creates the technical specifications governing material composition, seam integrity, pressure resistance, internal coating adherence, and leakage prevention. This eliminates non-certified suppliers regardless of price competitiveness. Unlike voluntary quality programs, QCOs are legally enforceable with market access consequences. Manufacturers possessing pre-certified facilities and documented quality management systems gain an undefeatable advantage over non-certified entrants. The policy driver is technical harmonization; its effect is systematic supplier consolidation toward compliance-capable packaging manufacturers across India's alcohol market.

Challenges

- Regulatory compliance and label approval delays: Manufacturers entering the alcohol packaging market face mandatory pre-approval of the labels and bottles design via the alcohol and Tobacco Tax and the trade bureau COLAs online system. This requirement creates significant time-to-market barriers as each unique bottle shape, size, and label must receive federal certification before commercial distribution. Further, the revised labeling regulations require entrants to continuously monitor regulatory changes across multiple beverage categories simultaneously.

- Raw material price volatility and supply insecurity: Glass price fluctuations create the persistent margin compression for the packaging manufacturers, particularly those dependent on long term price contracts with beverage producers. New entrants in the market are lacking diversified supplier networks and face acute vulnerability as established players secure preferential pricing via long-term vendor contracts that newcomers cannot match.

Alcohol Packaging Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.1% |

|

Base Year Market Size (2025) |

USD 73.8 billion |

|

Forecast Year Market Size (2035) |

USD 133.4 billion |

|

Regional Scope |

|

Alcohol Packaging Market Segmentation:

End user Segment Analysis

Beverage manufacturers represent the leading end-user sub-segment in the alcohol packaging market and are expected to hold the share value of 70.3% by 2035. This dominance is driven by the fundamental requirement for bulk procurement of primary packaging directly from producers before distribution to retail and on-trade channels. According to the APEDA February 2026 data, the third-largest market for alcoholic beverages is India in the world. There are nearly 12 joint venture companies with the licensed capacity of 33,919 kilo-liters p.a. to produce alcoholic beverages which are grain based. Additionally, major multinational producers consolidate purchasing power through centralized packaging contracts, reinforcing beverage manufacturers as the dominant end-user segment driving material selection, order volumes, and technical specifications across the entire packaging value chain.

Component Segment Analysis

The primary packaging is the largest subsegment in the market, as it encompasses all materials in direct contact with alcoholic beverages. This category includes glass bottles, aluminum cans, PET containers, bag-in-box liners, and pouches that serve as the critical interface between the product and consumer. The U.S. Food and Drug Administration (FDA) maintains stringent Food Contact Substance (FCS) notification requirements for the primary packaging materials, specifically addressing alcoholic beverage containers. The sub-segment's value is further amplified by premiumization trends where spirits brands invest a certain percentage of product cost in primary packaging for super premium expressions, utilizing heavy bottom glass ceramic closures and embossed decorations that secondary components cannot replace.

Functionality Segment Analysis

The recyclable packaging has emerged as the dominant sub-segment in the alcohol packaging market. The segment is driven by the regulatory mandates and corporate sustainability commitments. This segment includes glass bottles, aluminum cans, and paperboard cartons designed for material recovery and reprocessing into new packaging substrates. According to the U.S. Environmental Protection Agency's October 2025 report, the container and packaging recycling rate reached 53.9%, with aluminum beer and beverage cans significantly higher than the overall municipal solid waste recycling rate. As governments tighten recycled content mandates and carbon disclosure requirements, alcohol brands are increasingly standardizing mono-material and high-recovery packaging formats to align with circular economy targets.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Material Type |

|

|

Packaging Type |

|

|

Component |

|

|

Application |

|

|

Technology |

|

|

Functionality |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Alcohol Packaging Market - Regional Analysis

APAC Market Insights

The Asia Pacific alcohol packaging market is the dominant one and is poised to hold the regional share value of 37.4% by 2035. The market is propelled by three powerful and concurrent growth drivers that create an unmatched expansion trajectory. China and India are driving the market by the rising middle-class consumers on alcohol, representing an incremental demand for branded packaged alcoholic beverages, directly expanding the total addressable packaging market. On the other hand, the regulatory formalization is aggressively mandating track and trace system anti-counterfeit features and standardized labeling to combat tax evasion, pushing billions in incremental packaging investment. The market ensures a competitive advantage in glass, aluminum, closures, and smart packaging.

The market in India is driven by steady upstream aluminum output and sustained consumption levels. According to PIB August 2024 data, primary aluminum production reached 10.43 lakh tonnes in April to June 2024 to 2025, up 1.2% from 10.28 lakh tonnes in the same period, strengthening the domestic availability of metal for beverage cans and closures. On the demand side, the NLM October 2024 study indicates that 19% of men aged 15 and above consume alcohol, including 20% in rural and 17% in urban areas, sustaining packaged alcohol circulation across states. Additionally, India’s metal recycling rate of approximately 25% highlights both supply-side recovery potential and ongoing reliance on primary metal inputs. Together, these data deliver a positive impact on the market growth.

The alcohol packaging market in China is fueled by large-scale beverage production, steady consumption volumes, and expanding recycling infrastructure. According to the USDA May 2025 data, the country produced over 37.9 million kilolitres of beer in 2023, indicating substantial primary packaging throughput across glass bottles and aluminum cans. Moreover The Transition Asia April 2025 data has also reported that the aluminum output has exceeded 40 million tonnes annually in recent years, ensuring strong upstream material availability for beverage can manufacturing. Together, high beverage production volumes, stable aluminum supply capacity, and government-led recycling initiatives are reinforcing demand for compliant, lightweight, and recyclable alcohol packaging formats across China’s domestic and export-oriented beverage supply chains.

North America Market Insights

The North America alcohol packaging market is the fastest growing and grows at the CAGR of 6.3% during the forecast period 2026 to 2035. The market is driven by deeply entrenched beer culture the world’s largest premium wine consumption base and the highest per capita spirits branding expenditure wine consumption base and the highest per capita spirits branding expenditure globally. The market is characterized by format standardization around the aluminum can, which functions as the de facto unit of measurement for both domestic consumption and cross-border trade with Canada. Demand is increasingly decoupled from volume and driven by premiumization, with brands investing more in heavier glass tactile finishes and dynamic printing to command shelf distinction.

The sustained regulated production volumes and federal revenue flows are driving the alcohol packaging market in the U.S. According to the Congress.gov December 2024 report, the alcohol excise tax collection totaled USD 11.1 billion in 2023, and distilled spirits comprising 61% of that amount. Besides the alcoholic beverage manufacturing shipments are reflecting the significant primary and secondary packaging throughput across glass bottles, aluminum cans, closures, and corrugated formats. On the other hand, the metalized flexible packaging provides barrier protection against light and oxygen, which is relevant for product stability in wine bladders and certain RTD alcohol products. Further, the Federal Register January 2025 report shows that the TTB added multiple new container sizes for wine and distilled spirits. These data show a strong market growth in the U.S.

The stable, regulated production volumes and federal excise revenue flows are supporting the alcohol packaging market in Canada. According to the Government of Canada's March 2025 report, the government has earned nearly USD 15.7 billion from the sale of alcohol. Besides, the Beer Canada March 2024 data depicts that the government of Canada capped the scheduled 4.7% inflation based excise increase at 2% and expanded progressive duty relief, granting 80% to 90% excise rate reductions on the first 15,000 hectoliters (hl) of annual production per brewer. These measures particularly support 1,240 small Canadian brewers producing under 15,000 hl annually, improving production predictability and working capital allocation. Overall, excise predictability and targeted relief reduce volatility across the beer’s value chain from grain suppliers to hospitality, supporting steady packaging throughput in Canada’s regulated alcohol sector.

Canada Beer Excise Relief Measures

|

Policy Measure |

Previous Structure |

Revised Structure |

Market Impact on Packaging |

|

Inflation-Based Excise Adjustment |

4.7% scheduled increase (April 1, 2024) |

Capped at 2% for two years |

Improves production stability and packaging order visibility |

|

Progressive Beer Banding Relief |

Lower relief threshold |

80%–90% rate reduction on first 15,000 hl |

Supports small-batch output and diversified SKU packaging |

|

Eligible Brewers |

Standard banding system |

1,240 brewers under 15,000 hl benefit most |

Sustains demand for bottles, cans, labels, and corrugated formats |

|

Duration |

Annual indexation |

Two-year relief window |

Short- to mid-term packaging procurement stability |

Source: Beer Canada

Europe Market Insights

The alcohol packaging market in Europe is a mature, regulated, intensive ecosystem defined by heritage circular economy mandates and profound regional fragmentation. Europe operates as a mosaic of national packaging preferences, German consumers demand deposit return glass stein bottles, French winemakers require region-specific Burgundy or Bordeaux shapes, and Scotch Whisky distillers specify hand-blown crystal decanters for aged expressions. Moreover, sustainability is not an emerging trend but an operational baseline enforced via legally binding recycling targets and extended producer responsibility taxes that make lightweighting and recycled content economic necessities rather than marketing choices. The market is further distinguished by the coexistence of ultra-premium handcrafted packaging for aged spirits and industrialized returnable systems for mainstream beer, creating parallel value tiers.

The high per capita consumption and strong domestic production are supporting the market in Germany. According to the NLM study in September 2025, Germany records 12.8 litres of pure alcohol consumption per person aged 15 and above, substantially above the global average of 5.8 litres, indicating sustained volume circulation across beer, wine, and spirits packaging formats. At the same time, cost pressures have reshaped procurement dynamics. The Destatis January 2023 data reported that producer prices for glass and glass products increased by 26.9% YoY in January 2023, with particularly sharp increases for glass bottles. Given Germany’s heavy reliance on glass packaging for beer and spirits, this inflation directly affected filling operations, contract bottlers, and brand owners. Moreover, the glass input costs have accelerated efficiency measures, lightweighting initiatives, and stronger adoption of reusable bottle systems, which are already embedded in Germany’s beverage deposit framework. Overall, high consumption intensity sustains packaging demand while producer price volatility is driving cost optimization and material strategy adjustments across the German alcohol packaging supply chain.

Producer Prices of Glass and Glass Product

|

Year |

Glass and Glass Products |

Bottles of Non Colored Glass |

Bottles of Colored Glass |

|

January 2020 |

107.2 |

105.7 |

103.2 |

|

January 2021 |

109.0 |

111.0 |

103.7 |

|

January 2022 |

122.2 |

118.4 |

114.7 |

|

January 2023 |

153.4 |

166.0 |

157.1 |

Source: Destatis January 2023

The alcohol packaging market in UK is influenced by sustained consumption levels and regulatory reforms affecting excise structure and packaging compliance. According to the Office for Budget Responsibility in November 2025, alcohol duty receipts totaled £12.0 billion, reflecting continued packaged alcohol removals into the domestic market. Besides, the UK implemented a reformed alcohol duty system based on strength by alcohol by volume, replacing the previous banding structure, which directly affects labeling, SKU configuration, and pack-size strategy across beer, wine, and spirits. Additionally, the WSTA July 2025 data reports that the UK production of wine and spirits generated over £9.2 billion in annual turnover in recent years, underscoring steady primary and secondary packaging throughput. The combination of excise reform, stable duty revenues, and consistent domestic production supports the continued demand for glass bottles and aluminum cans, driving the market in the UK.

Key Alcohol Packaging Market Players:

- Ball Corporation (U.S.)

- Crown Holdings, Inc. (U.S.)

- Owens-Illinois, Inc. (O-I Glass) (U.S.)

- Ardagh Group S.A. (Luxembourg)

- Smurfit Kappa Group (Ireland)

- WestRock Company (U.S.)

- Berry Global Inc. (U.S.)

- Stora Enso Oyj (Finland)

- Verallia (France)

- Vidrala S.A. (Spain)

- Vetropack Holding AG (Switzerland)

- Gerresheimer AG (Germany)

- Amcor plc (UK)

- Mondi Group (UK)

- DS Smith Plc (UK)

- BA Glass (Portugal)

- TCPL Packaging Ltd. (India)

- Samhwa Crown & Closure (South Korea)

- Bright Packaging Industry Berhad (Malaysia)

- Meiji Rubber & Chemical Co., Ltd. (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Ball Corporation has solidified its leadership in the market by anchoring its strategy in sustainability and technology innovation. Ball showcased its commitment to co-creating the future with brands through interactive digital experiences and dynamic printing capabilities that enable personalized, purpose-driven packaging. According to the 2024 annual report, the company has used 74% of averaged recycled content for beverage packing.

- Crown Holdings Inc. continues to assert its dominance in the market via strategic capacity alignment and geographic expansion. The company has reported the performance with the U.S. beverage volumes surging, and EU shipments are growing, driven especially by accelerated growth in the alcohol segment, which rebounded strongly after several quarters of mass beer declines.

- Owens-Illinois Inc. remains the undisputed global leader in glass packaging for the alcohol packaging market, executing aggressive capacity expansion to capture the surging demand for premium beer and wine bottles. The company is actively tackling glass recycling challenges, advocating for collection infrastructure improvements to approach aluminum’s reuse rates.

- Ardagh Group S.A. strengthens its competitive positioning in the alcohol packaging market by leveraging its status as the largest domestic manufacturer of glass bottles for the U.S. spirits market. The company’s sustainability leadership is evidenced by pilot programs achieving carbon footprint reduction for craft beer clients through increased recycled content. In Q3 2025, the company has earned a revenue of USD 2,504 millions.

- Smurfit Kappa Group is transforming the market via pioneering e-commerce solutions for the rapidly expanding online beverage sector. With the European online alcohol sales growing, the company has launched its innovative eBottle packaging portfolio featuring Rollor Bottle Pack, BiPack, and Pop-up Insert solutions that address the critical challenges of product damage, sustainability, and consumer experience.

Here is a list of key players operating in the global market:

The global market is very competitive and is dominated by the established multinational giants and specialized regional players. Leaders leverage massive scale in metal packaging command the glass segment. The competitive landscape is defined by a decisive shift toward sustainability and circular economy models. Key strategic initiatives include heavy investment in lightweighting technology to reduce the material use and carbon footprint demonstrated by the top players and the expansion of production capacity for recycled aluminum and glass. Further, the players are pursuing geographic expansion via mergers and acquisitions to serve the fast-growing Asia Pacific market, along with innovations in smart packaging and premiumization to enhance brand value and consumer engagement. For example, in November 2024, ITC collaborates with Frugalpac to bring sustainable paper bottles to India & South Asia.

Corporate Landscape of the Market:

Recent Developments

- In June 2025, Berlin Packaging, the world's largest hybrid packaging supplier, announced that it has completed its acquisition of Sarom Packaging and Romgallia. Sarom Packaging supplies glass packaging for the food and beverage industries, specializing in wine bottles and closures.

- In December 2024, the Coca‑Cola Company announced that it has agreed to acquire Billson’s, an Australia-based brand of alcohol ready-to-drink products that include local market leaders Vodka with Tangle, Vodka with Grape Burst, and Vodka with Portello.

- In July 2024, ProMach announced that it has acquired MBF, a leading global producer of bottle-filling and closing machines. MBF is a well-known and respected partner for wine and distilled spirits producers around the world.

- Report ID: 4475

- Published Date: Feb 18, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Alcohol Packaging Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.