AI Sensor Market Outlook:

AI Sensor Market size was valued at USD 6.5 billion in 2025 and is projected to reach USD 190.6 billion by the end of 2035, rising at a CAGR of 40.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of AI sensor is assessed at USD 9.1 billion.

The adoption of artificial intelligence sensors is expanding as governments and public institutions increase their investments in intelligent infrastructure, automation and connected systems. Public sector initiatives supporting smart transportation, industrial automation, and environmental monitoring are significantly increasing the demand for AI-enabled sensing technologies that can process the data at the edge. According to AASHTO data for December 2024, the U.S. Department of Transportation has awarded USD 130 million to 42 technology demonstration projects through its SMART Grants program. Moreover, the SMART program created under the Infrastructure Investment and Jobs Act allocates USD 500 million to support technology deployment in transportation systems. Many of the technologies funded through SMART projects, such as connected infrastructure, intelligent traffic management, autonomous mobility systems, and smart intersections, require sensor networks integrated with AI-based analytics to collect and process real-time transportation data, therefore driving the artificial intelligence sensor market.

Besides, the environmental monitoring defense surveillance, and public safety systems are also contributing to expanding demand for the AI sensor platforms. According to the UNEP November 2022 data, IQAir aggregates data from more than 25,000 air quality monitoring stations across over 140 countries using AI-based analytics to interpret real-time environmental sensor data and assess population exposure to pollution. Such large-scale environmental monitoring networks demonstrate the growing role of sensor-driven data ecosystems combined with AI analytics to support public health protection and regulatory monitoring, reinforcing demand for advanced sensing technologies used in air quality surveillance and environmental intelligence systems. On the other hand, the defense and security agencies are also accelerating AI sensor deployment, providing an optimistic outlook for the AI sensor market growth.

Key AI Sensor Market Insights Summary:

Regional Highlights:

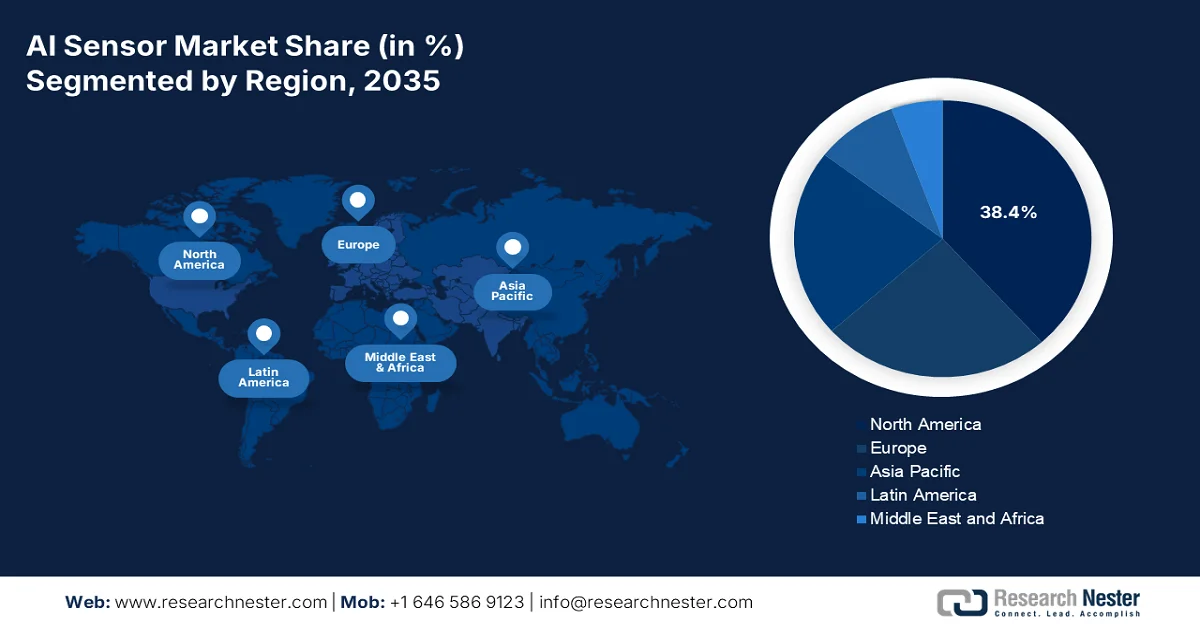

- North America AI sensor market is anticipated to capture a 38.4% share by 2035, supported by strong adoption across industrial, automotive, and medical applications attributable to substantial government funding for defense modernization, smart grid infrastructure, and semiconductor manufacturing

- Asia Pacific is projected to witness the fastest expansion in the market with a CAGR of 28.5% during 2026–2035, stimulated by semiconductor manufacturing leadership, government-backed smart city initiatives, and accelerating automotive electrification

Segment Insights:

- In the AI sensor market, the Hardware segment is projected to account for a 52.4% share by 2035, propelled by the expanding requirement for high-fidelity physical infrastructure capable of capturing and converting real-world data for AI processing

- Deep Learning technology is anticipated to maintain its leading position throughout 2026–2035 in the segment, stimulated by its advanced capability to process unstructured sensor data and enable edge-level computer vision tasks

Key Growth Trends:

- Rising government funding for R&D in AI

- Growth of smart manufacturing programs

Major Challenges:

- Supply chain volatility and tariff exposure

- Price competition and margin erosion

Key Players: Intel Corporation (U.S.), NVIDIA Corporation (U.S.), Qualcomm Technologies, Inc. (U.S.), Texas Instruments Incorporated (U.S.), Analog Devices, Inc. (U.S.), Infineon Technologies AG (Germany), Robert Bosch GmbH (Germany), STMicroelectronics N.V. (Switzerland), Sony Group Corporation (Japan), TDK Corporation (Japan), Omron Corporation (Japan), Samsung Electronics Co., Ltd. (South Korea), SK Hynix Inc. (South Korea), Honeywell International Inc. (U.S.), TE Connectivity Ltd. (Switzerland), Teledyne Technologies Incorporated (U.S.), COMPREDICT GmbH (Germany), Ambarella, Inc. (U.S.), Elliptic Labs (Norway), Butlr (U.S).

Global AI Sensor Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.5 billion

- 2026 Market Size: USD 9.1 billion

- Projected Market Size: USD 190.6 billion by 2035

- Growth Forecasts: 40.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.4% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Singapore, United Arab Emirates, Brazil, Vietnam

Last updated on : 12 March, 2026

AI Sensor Market - Growth Drivers and Challenges

Growth Drivers

- Rising government funding for R&D in AI: The public sector investment in AI research is accelerating the development and commercialization of sensor technologies capable of performing on-device analytics. According to the NITRD May 2025 data, the U.S. is set to invest USD 2.2 trillion in the next five years in AI infrastructure supporting the research programs focused on energy infrastructure, manufacturing facilities, cybersecurity upgrades, and integrating AI in government. Government-backed research programs also stimulate the collaboration between universities, semiconductor developers, and industrial manufacturers to advance intelligent sensing technologies for manufacturing automation, agriculture, and infrastructure monitoring. Additionally, standards for trustworthy AI and sensor-enabled cyber-physical systems, supporting interoperability and large-scale deployment therefore driving the growth for the artificial intelligence sensor market.

U.S. Investment Areas Supporting AI Infrastructure

|

Investment Area |

Funding |

|

Manufacturing Facilities |

USD 600 Billion |

|

Energy Infrastructure |

USD 1.1 Trillion |

|

Cybersecurity Upgrades |

USD 250 Billion |

|

Safe and Ethical AI |

USD 50 Billion |

|

AI Integration in Government |

USD 200 Billion |

Source: NITRD May 2025

- Growth of smart manufacturing programs: Government-supported industrial modernization programs are increasing the adoption of intelligent sensors across the manufacturing facilities, hence driving the AI sensor market growth. AI-enabled sensors are widely used in predictive maintenance, robotic automation, and process monitoring within advanced manufacturing environments. The U.S. National Institute of Standards and Technology operates the Manufacturing USA network, a public private imitative supporting innovation in smart manufacturing technologies, including the AI-integrated sensors and industrial automation systems. As per the Advanced Manufacturing data in December 2024, the manufacturing USA network involves 17 manufacturing innovation institutes working to advance digital manufacturing and intelligent production systems. Further, the global manufacturing modernization policies promote the factories to integrate advanced sensor networks capable of real-time process monitoring and machine learning-based quality control.

- Precision agriculture and environmental monitoring programs: The Department of Agriculture funding programs are surging the adoption of the AI sensor for crop monitoring, irrigation optimization, and livestock management. According to the EWG January 2025 data, the natural resource conservation service provides financial assistance via the environmental quality incentives program, obligated USD 1.84 billion for conservation practices, including cost-sharing for precision agriculture technologies. Moreover, the farmers utilize precision agriculture practices with sensor-based irrigation and nutrient management, showing the fastest adoption rates. For equipment manufacturers, these programs reduce adoption barriers for farmers while creating demand for AI sensor market products that operate reliably in dust, moisture, and temperature-extreme environments.

Challenges

- Supply chain volatility and tariff exposure: Global supply chain dependencies create existential risks for AI sensor manufacturers, mainly new entrants without diversified sourcing networks. The artificial intelligence sensor market relies on the specialized components, silicon wafers, rare earth elements, and advanced substrates that are concentrated in specific geographic regions. Disruptions from the trade policies, natural disasters, or geopolitical tensions can halt production lines overnight. Further, the implementation of the tariffs targeting the critical sensor components and the related technologies triggers ripple effects across global supply chains and elevates costs for the imported image processing chips and specialized LiDAR modules.

- Price competition and margin erosion: The artificial intelligence sensor market is intensely competitive, with the established players offering similar sensor solutions at aggressive price points, creating significant margin erosion risks for the new entrants. The player benefits from the economies of scale, established customer relationship and a vertically integrated supply chain that enable predatory pricing strategies. According to the artificial intelligence (AI) sensor market analysis, the new players must differentiate via advanced features, superior accuracy, and integrated AI capabilities rather than competing on price, focusing on premium segments where the price sensitivity is lower. However, this strategy requires substantial R&D investment and longer sales cycles.

AI Sensor Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

40.2% |

|

Base Year Market Size (2025) |

USD 6.5 billion |

|

Forecast Year Market Size (2035) |

USD 190.6 billion |

|

Regional Scope |

|

AI Sensor Market Segmentation:

Component Segment Analysis

The hardware sub-segment is leading and is poised to hold the share value of 52.4% by the end of 2035 in the artificial intelligence (AI) sensor market. This dominance is due to the physical infrastructure required to support AI algorithms. Before the data can be processed by the software, it must be captured and converted by the high-fidelity hardware components. According to the BIS July 2025 data, Cadence has exported EDA hardware and software, and semiconductor design technology worth USD 45,305,317.41 to CSCC. Moreover, the automotive company is actively investing in computer and electronic semiconductor fabrication equipment and sensor production lines. This capital reflects the industry's focus on scaling the hardware capacity to meet the demand for the AI-enabled sensing components across the automotive and consumer electronics supply chains.

Technology Segment Analysis

Within the technology sub segment, deep learning is dominating in the AI sensor market. The segment is driven by the unparalleled ability to process the unstructured data, such as raw pixel arrays from the image sensor or point clouds from LiDAR, and recognize complex patterns without explicit programming. In the AI sensors, deep learning, mainly convolutional neural networks are essential for enabling computer vision tasks such as object detection and facial recognition directly at the edge. Moreover, the funding for AI core techniques, including deep learning, is rising. This sustained investment in foundational AI research accelerates the deployment of more advanced algorithms onto power-constrained sensor hardware, ensuring deep learning remains the primary technological driver for intelligent sensor capabilities.

Processing Type Segment Analysis

Edge based AI sensors are projected to hold the largest share of the processing mode by 2035 fundamentally altering how data is handled in the internet of things. Unlike cloud-dependent systems, edge-based sensors perform data processing and inference locally, which drastically reduces the latency and bandwidth consumption. This architectural shift is critical for time-sensitive applications such as autonomous vehicle navigation and industrial robotics, where milliseconds can determine the safety outcomes. According to the HAI August 2022 data, the CHIPS and Science Act of 2022 allocates USD 52 billion to strengthen the domestic semiconductor fabrication and innovation, enhancing production pipelines for AI-driven sensors, including those used in edge-based AI applications.

Our in-depth analysis of the AI sensor market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Sensor Type |

|

|

Technology |

|

|

Processing Mode |

|

|

End use Vertical |

|

|

Application |

|

|

Connectivity |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

AI Sensor Market - Regional Analysis

North America Market Insights

The North America dominates the global artificial intelligence (AI) sensor market and is expected to hold the regional revenue share of 38.4% by the end of 2035. The market is driven by the substantial government funding for defense, modernization, smart grid infrastructure, and semiconductor manufacturing. The region benefits from early adoption of the autonomous vehicle regulations and the established healthcare reimbursement frameworks for remote monitoring technologies. According to the U.S. Department of Energy, in December 2024, the grid modernization investments exceeding USD 10.5 billion are creating a sustained demand for the edge-based sensing units capable of real-time load balancing and anomaly detection. The convergence of defense procurement, infrastructure spending, and healthcare digitization positions North America as the primary market for high-reliability AI sensors across industrial, automotive, and medical applications.

The federal investment in artificial intelligence, advanced manufacturing, and intelligent infrastructure is expanding the growth of the artificial intelligence sensor market in the U.S. According to the CSIS October 2025 data, the federal government invested USD 3.3 billion in AI research and development, supporting technologies such as intelligent sensing systems, robotics, and autonomous platforms. Additionally, the Gitnux February 2026 data has depicted that the U.S. Department of Defense has allocated USD 1.8 billion for artificial intelligence and data acceleration initiatives, which include sensing and surveillance technologies supporting the defense operations. These federal investments are strengthening the deployment of AI-enabled sensing technologies, reinforcing the U.S. role as a major innovation hub for intelligent sensing technologies.

The rising federal investments and R&D in artificial intelligence are driving the growth of the artificial intelligence (AI) sensor market in Canada. According to the Prime Minister of Canada, April 2024 data, the Government of Canada continues to support AI development through the Pan-Canadian Artificial Intelligence Strategy, which received USD 443 million to strengthen AI research, commercialization, and industry adoption across sectors such as robotics, environmental monitoring, and intelligent infrastructure. Additionally, Government of Canada's June 2025 data reported that about 6.1% of businesses in Canada were using AI technologies, reflecting the growing integration of AI-driven systems that depend on sensor-based data collection. These programs are stimulating the deployment of intelligent sensing technologies across various sectors and supporting the adoption of AI-enabled sensing technologies.

Use of AI Among Businesses

|

|

Second Quarter 2025 |

Second Quarter 2024 |

|

AI used in producing goods or delivering services |

12.2 |

6.1 |

|

Text analytics using AI |

35.7 |

27.0 |

|

Data analytics using AI |

26.4 |

25.0 |

|

Virtual agents or chat bots |

24.8 |

26.5 |

|

Natural language processing |

23.1 |

28.9 |

|

Marketing automation using AI |

23.1 |

15.2 |

|

Speech or voice recognition using AI |

20.0 |

18.1 |

|

Large language models |

19.1 |

21.9 |

|

Machine learning |

18.6 |

20.1 |

|

Recommendation systems using AI |

14.0 |

12.3 |

|

Image or pattern recognition |

11.4 |

21.8 |

|

Deep learning |

6.6 |

1.9 |

|

Decision making systems based on AI |

5.7 |

6.1 |

|

Robotics process automation |

3.8 |

2.6 |

|

Augmented reality |

3.2 |

2.6 |

|

Biometrics |

3.2 |

1.0 |

|

Machine or computer vision |

3.1 |

4.7 |

|

Neural networks |

2.5 |

4.4 |

|

Other type |

6.1 |

6.7 |

Source: Government of Canada, June 2025

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region in the artificial intelligence sensor market and is poised to register a CAGR of 28.5% during the forecast period 2026 to 2035. The market is driven by the semiconductor manufacturing dominance, government-led smart city programs, and rapid automotive electrification. The demand is primarily from the end users. APAC growth is defined by top-down national strategies such as China's 14th Five-Year Plan, Japan's Society 5.0, and South Korea's Digital New Deal that allocate billions in directed funding toward sensor infrastructure and domestic fabrication capacity. Moreover, the region benefits from vertical integration, with leading semiconductor foundries, MEMS fabrication facilities, and consumer electronics assembly often located within the same geographic clusters. On the other hand, the region's rapidly aging societies create a sustained healthcare monitoring demand, while urbanization across Southeast Asia drives smart city sensor deployment via manufacturing scale and domestic consumption.

The digital public infrastructure expansion and manufacturing localization incentives are driving the AI Sensor market in India. According to the PIB February 2026 data, the Production Linked Incentive scheme for electronics manufacturing allocated USD 1.4 billion, mainly for sensor and component production, with 836 approved applications. Moreover, the PIB December 2024 data depicts that India's Smart Cities Mission has deployed the sensor systems across 100 cities, with the Ministry of Housing and Urban Affairs reporting AI-enabled environmental and traffic sensors installed across the cities. According to the PIB August 2022 data, the manufacturing sector investment reached USD 27.6 billion in advanced automotive technology products, with predictive maintenance sensors representing the fastest-growing category. These data indicate an optimistic growth in the India market.

The strong capabilities in electronics manufacturing, satellite remote sensing technologies, and automation systems are fueling the demand for the artificial intelligence (AI) sensor market in China. According to the OEC 2024 data, China is a major exporter of components used in control and sensing systems, and the country exported approximately USD 765 million worth of parts and accessories for automatic control instruments (HS 9032.90), highlighting its strong manufacturing base for sensor-related components. On the other hand, in the space and remote sensing sector, China is also advancing satellite imaging technologies that rely on high-resolution optical and radar sensors capable of capturing imagery with resolutions as fine as 50 centimeters or less, enabling detailed monitoring for environmental, agricultural, and infrastructure applications, based on the USCC December 2024 data. These developments, combined with large-scale industrial production and growing investments in satellite observation systems, are strengthening the growth in China.

Europe Market Insights

The AI sensor market in Europe is defined by the stringent regulatory frameworks driving the adoption in automotive safety, healthcare digitization, and industrial automation. The European Commission’s investment has stimulated the remote patient monitoring and diagnostic image sensor deployment across the member states. The general safety regulation mandates advanced driver assistance systems in all new vehicles, requiring AI-enabled sensors for pedestrian detection, lane keeping, and emergency braking. Moreover, Germany’s Industry 4.0 platform and France's Defi robotique program create a demand for predictive maintenance sensors. The European Green Deal Industrial Plan directs funding toward energy-efficient manufacturing, with sensor-based monitoring systems qualifying for carbon reduction incentives. The convergence of safety mandates, healthcare modernization, industrial policy, and sustainability targets positions Europe as the second-largest regional market with distinct requirements for compliance, interoperability, and data protection under GDPR and emerging AI legislation.

The AI sensor market is expanding rapidly in Germany as the country boosts its AI ecosystem and industrial automation capabilities. Germany’s strong manufacturing base and robotics adoption are creating favorable aspects for the AI-enabled sensing technologies used in various sectors. According to the International Trade Administration data published in June 2025, Germany ranked 3rd globally in robot density in manufacturing in 2022, highlighting the extensive use of sensor-integrated robotic systems in the industrial facilities. Moreover, the German federal government announced USD 1.9 billion in funding to support technology startups, strengthening the national AI innovation ecosystem. These developments are increasing the integration of intelligent sensing technologies and enabling a positive impact on market growth.

The expanding artificial intelligence adoption across public services, healthcare monitoring, and digital infrastructure is shaping the AI sensor market in the UK. According to the Government of the UK, January 2025 data, the government’s Plan for Change targets up to USD 57 billion in public sector efficiency savings via the use of AI and digital technologies across institutions. Local authorities are increasingly deploying AI-enabled sensor technologies, including connected home sensors and monitoring devices that detect behavioral changes among elderly residents to prevent accidents and support independent living. Moreover, the UK’s AI ecosystem continues to expand rapidly, with more than 5,800 AI companies operating across the country, generating USD 30.5 billion in revenue based on the UK Government's September 2025 report. These data show that the UK is a growing hub for AI-enabled digital technologies.

Key AI Sensor Market Players:

- Intel Corporation (U.S.)

- NVIDIA Corporation (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

- Analog Devices, Inc. (U.S.)

- Infineon Technologies AG (Germany)

- Robert Bosch GmbH (Germany)

- STMicroelectronics N.V. (Switzerland)

- Sony Group Corporation (Japan)

- TDK Corporation (Japan)

- Omron Corporation (Japan)

- Samsung Electronics Co., Ltd. (South Korea)

- SK Hynix Inc. (South Korea)

- Honeywell International Inc. (U.S.)

- TE Connectivity Ltd. (Switzerland)

- Teledyne Technologies Incorporated (U.S.)

- COMPREDICT GmbH (Germany)

- Ambarella, Inc. (U.S.)

- Elliptic Labs (Norway)

- Butlr (U.S)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Intel Corporation is a foundational player in the AI sensor market, providing the high-performance computing architecture required to process the complex data at the edge. By integrating AI accelerators directly into its sensor processing units and hardware, Intel enables real-time analytics for applications ranging from industrial automation to smart cities.

- NVIDIA Corporation has redefined the market by leveraging its GPU leadership to create specialized AI platforms for sensor data fusion. Through its Jetson platform and powerful computing fabrics, the company enables autonomous machines and robots to interpret inputs from cameras, LiDAR, and radar simultaneously. In 2025, the company made a revenue of USD 1.7 billion in the automotive sector.

- Qualcomm Technologies Inc is a dominant player in the AI sensor market, mainly within the mobile and consumer electronics segments. By embedding dedicated AI engines into its system-on-chip, Qualcomm enables on-device sensor processing for smartphones, IoT devices, and next-gen PCs. In 2024, the company made a revenue of USD 32,791 in the equipment and services segment.

- Texas Instruments Incorporated plays a critical role in the market by focusing on low-power embedded processing and analog integration. Their microcontrollers and processors are designed to bring machine learning capabilities to industrial and automotive sensors, enabling predictive maintenance and smarter factory floors.

- Analog Devices, Inc excels in the AI sensor market by bridging the physical and digital worlds with precision sensing technology combined with embedded AI. By converting real-world phenomena such as motion, temperature, and sound into actionable data, ADI enables the intelligent industrial instruments and the healthcare monitors to detect anomalies instantly.

Here is a list of key players operating in the global artificial intelligence (AI) sensor market:

The global artificial intelligence sensor market is intensely competitive and is defined by a mix of established semiconductor giants and innovative niche players. The landscape is defined by the rapid technological convergence, where companies integrate edge AI capabilities directly into sensors for faster data processing. The key strategic initiatives include heavy investment in R&D for low-power high-efficiency chips, strategic acquisitions to boost the AI software capabilities, and forming partnerships with the automotive and consumer electronics manufacturers to secure design wins. For example, in September 2025, COMPREDICT partners with Sonatus to accelerate AI-powered virtual sensor deployment in next-gen vehicles. The market is geographically diverse, and automotive MEMS and Asia dominate in manufacturing and consumer electronics integration.

Corporate Landscape of the AI Sensor Market:

Recent Developments

- In January 2026, Ambarella, Inc., an edge AI semiconductor company has announced the launch of a powerful edge AI 8K vision SoC with industry-leading AI and multi-sensor perception performance.

- In September 2025, Elliptic Labs has announced the launch of its AI Virtual Proximity Sensor INNER BEAUTY on vivo’s V60 and IQOO Z10 Turbo+ smartphones. Both the vivo V60 and iQOO Z10 Turbo+ smartphones are targeted for the global market.

- In July 2025, Butlr, a leader in physical AI (PAI) technology, announced the Heatic Wired sensor to complement its wireless portfolio of AI and body heat sensing technology products that provide anonymous insight into the built environment.

- Report ID: 8435

- Published Date: Mar 12, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.