Agricultural Fumigants Market Outlook:

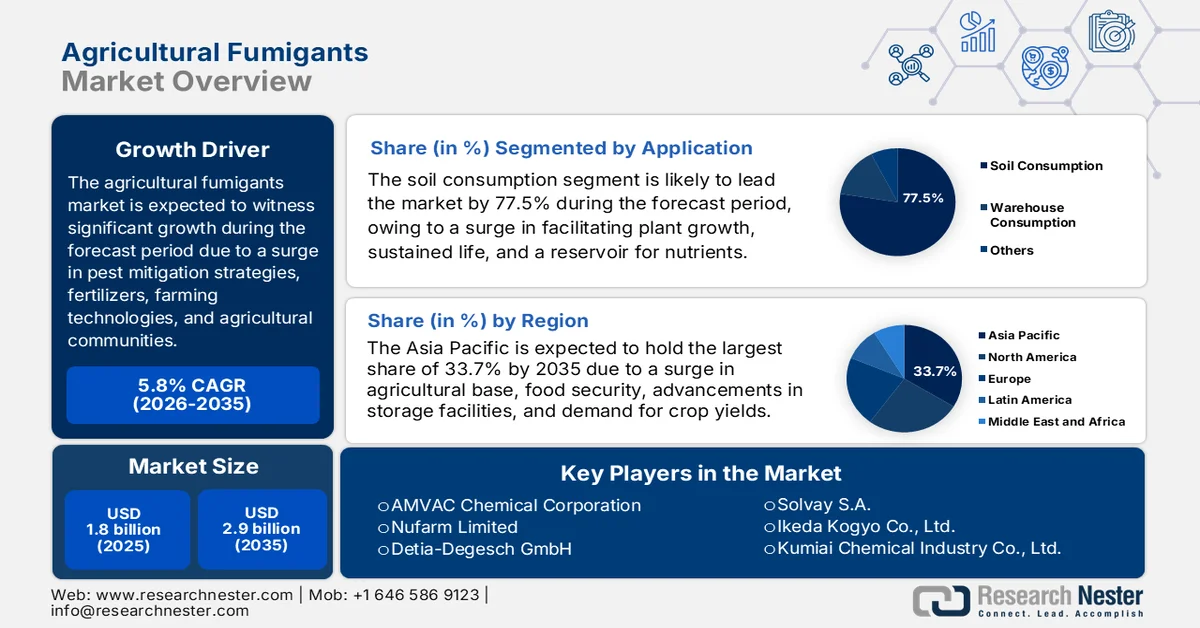

Agricultural Fumigants Market size was valued at over USD 1.8 billion in 2025 and is expected to reach USD 2.9 billion by the end of 2035, growing at a CAGR of 5.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of agricultural fumigants is evaluated at USD 1.9 billion.

The global agricultural fumigants market is being significantly reshaped by emerging factors, including volatility in fertilizers and input expenses, climate change-specific pest migration patterns, the presence of rural agricultural communities, and the presence of suitable liability and insurance premiums. According to official statistics published by America Farm Bureau Federation in September 2025, there has been an increase in the payer’s pricing of fertilizers, including gulf diammonium phosphate, from almost USD 5 per ton in January 2025 to USD 800 in August, thus constituting a 36% surge within less than 8 months. Likewise, the pricing of Tampa ammonia settlements effectively reached USD 487 per metric ton in August 2025. Meanwhile, the import of 25% of U.S.-based fertilizer utilization is also denoting a huge growth opportunity for the market worldwide.

U.S.-based Import Analysis of Fertilizer Utilization in Different Countries (2024)

|

Fertilizer Type |

Countries |

Import |

|

Potassium |

Canada |

85% |

|

Russia |

10% |

|

|

ROW |

3% |

|

|

Israel |

2% |

|

|

Nitrogen |

Canada |

26% |

|

Russia |

18% |

|

|

Trinidad & Tobago |

18% |

|

|

ROW |

17% |

|

|

Qatar |

9% |

|

|

Saudi Arabia |

7% |

|

|

Algeria |

6% |

|

|

Phosphate |

Saudi Arabia |

39% |

|

ROW |

25% |

|

|

Israel |

12% |

|

|

Mexico |

12% |

|

|

Egypt |

8% |

|

|

Jordan |

5% |

Source: America Farm Bureau Federation

Furthermore, the integration of IoT-based real-time gas monitoring, the shift towards subscription-specific fumigation-as-a-service, the development of multi-component formulations with synergistic adjuvants, and the resurgence of heat-driven integrated fumigation protocols are a few trends that are driving the agricultural fumigants market globally. As stated in an article published by Heliyon in February 2025, the global population is continuously increasing and accounts for 7.9 billion, which has resulted in the adoption of IoT-driven technologies to reshape the agricultural industry. This particular technological integration is projected to increase the overall agricultural production by 70% by the end of 2050. In this regard, the total arable land for food production has been estimated to be nearly 20 million square miles, which is 40% of the global land, thereby denoting a positive impact on the agricultural fumigants market expansion.

Key Agricultural Fumigants Market Insights Summary:

Regional Highlights:

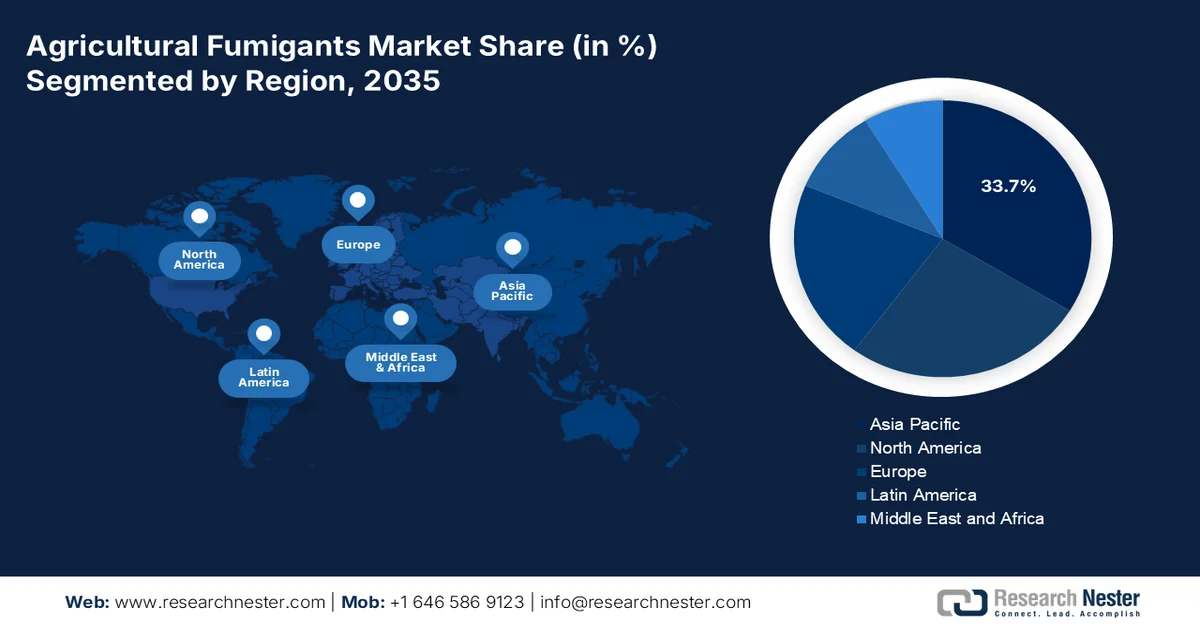

- Asia Pacific agricultural fumigants market is projected to dominate with a 33.7% share by 2035, supported by expanding agricultural base, rising food security concerns, and increased adoption of modern storage infrastructure

- Europe is set to register the fastest growth in the market over the forecast period 2026-2035, stimulated by stringent regulatory frameworks, rising adoption of sustainable farming practices, and increasing incidence of soil-borne pathogens

Segment Insights:

- In the agricultural fumigants market, the soil consumption sub-segment is expected to capture a dominant 77.5% share by 2035, reinforced by its essential role in supporting plant growth and maintaining soil nutrient balance

- The commercial storage/warehousing segment is anticipated to secure the second-largest share during 2026–2035, influenced by the growing need for large-scale grain storage and efficient pest control in high-capacity facilities

Key Growth Trends:

- Expansion of high-density protected cultivation

- Focus on strategic grain reserves

Major Challenges:

- Health, safety, and application risks

- Logistical and infrastructure barriers in emerging economies

Key Players: BASF SE, Corteva Agriscience, FMC Corporation, UPL Limited, ADAMA Ltd., Syngenta AG, AMVAC Chemical Corporation, Nufarm Limited, Detia-Degesch GmbH, Arkema S.A., Eastman Chemical Company, LANXESS AG, Solvay S.A., Ikeda Kogyo Co., Ltd., Kumiai Chemical Industry Co., Ltd., Sumitomo Chemical Co., Ltd., Mitsui Chemicals, Inc., Nippon Soda Co., Ltd., Balchem Corporation, Landmark Fumigants, Kemin Industries, FumiHogar.

Global Agricultural Fumigants Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size:USD 1.8 billion

- 2026 Market Size: USD 1.9 billion

- Projected Market Size: USD 2.9 billion by 2035

- Growth Forecasts: 5.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (33.7% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, India, Germany, Brazil

- Emerging Countries: Indonesia, Vietnam, Thailand, Mexico, Turkey

Last updated on : 7 April, 2026

Agricultural Fumigants Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of high-density protected cultivation: The transition towards protected cultivation, including vertical farming, polytunnels, and greenhouses, has created suitable conditions for soil-borne pathogen buildup, owing to ongoing cropping cycles without natural fallow periods. According to official statistics published by NLM in July 2025, LEDs are increasingly utilized for vertical farming, with 660 nm red and 450 nm blue LEDs accounting for efficiencies of 81% and 93%, respectively, for Watts of light that is emitted per unit of supplied electricity. Besides, the incorporation of leaf photosynthesis utilizes light in the wavelength range from 400 nm to almost 730 nm, and further accounts for almost 95% in the red and blue spectral regions, thereby making it suitable for bolstering the agricultural fumigants market globally.

- Focus on strategic grain reserves: The presence of different governments across regions has escalated the filling and construction of tactical grain reserves to buffer against future shocks, which is deliberately expanding storage facilities. As per an article published by NLM in October 2023, the global grain production has successfully reached 2.8 billion tons as of 2023, denoting an increase by 0.9% in comparison to 2022. Moreover, the overall number of individuals has reached 2.4 billion, indicating an increase of 391 million, leading to increased focus on food security and reserve facilities for grain. Therefore, there is a huge demand for low-temperature grain storage technology, constituting a 15-degree Celsius. This is extremely suitable for maintaining the quality and germination of rice, thus positively impacting the agricultural fumigants market globally.

- Rise in contract farming: The suitable consolidation of small-scale farms into contract farming with large-scale agribusinesses has resulted in establishing processing facilities and centralized collection, which is uplifting the agricultural fumigants market expansion. Based on an article published by the Frontiers Organization in May 2024, contract farming has resulted in boosting the probability of manual weeding by 28.2%, along with the utilization of organic fertilizers by 31.1%, particularly for rice farmers in China. Additionally, there has been an increase in the probability of applying organic fertilizer by 50.7%of vegetable farmers in the country. Therefore, contract farming focuses on fostering sustainable agricultural development, which is denoting an optimistic outlook for the agricultural fumigants market across different regions.

Challenges

- Health, safety, and application risks: The inherent toxicity of the agricultural fumigants market presents an unyielding operational challenge regarding human safety during transport, storage, and application. Unlike surface sprays, fumigants are true gases or volatile liquids that require sealed environments, specialized personal protective equipment, and rigorous re-entry intervals. Accidental exposures, though decreasing, still occur due to improper aeration, equipment failure, or simple human error, often with fatal consequences for applicators or bystanders. This risk profile has led to a shortage of certified applicators in many agricultural regions, as younger workers increasingly avoid hazardous roles.

- Logistical and infrastructure barriers in emerging economies: The lack of proper storage, handling, and application infrastructure across rapidly developing agricultural economies severely limits the agricultural fumigants market penetration. Besides, fumigation requires gas-tight storage structures, calibrated dosing equipment, and reliable aeration systems, all of which are often absent in fragmented smallholder farming systems. Instead, farmers resort to open, unsafe application methods that yield poor pest control while exposing rural communities to toxic fumes. Moreover, the cold chain for temperature-sensitive fumigants is frequently broken, leading to product degradation before use. Additionally, distribution channels in remote areas lack basic safety training, resulting in leaking cylinders or improperly stored tablets that degrade into hazardous byproducts.

Agricultural Fumigants Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.8% |

|

Base Year Market Size (2025) |

USD 1.8 billion |

|

Forecast Year Market Size (2035) |

USD 2.9 billion |

|

Regional Scope |

|

Agricultural Fumigants Market Segmentation:

Application Segment Analysis

The soil consumption sub-segment, which is part of the application segment, is anticipated to garner the largest share of 77.5% in the agricultural fumigants market by the end of 2035. The sub-segment’s upliftment is highly driven by its role as the crucial foundation of agriculture in facilitating plant growth, sustaining life, and acting as a reservoir of air, water, and nutrients. According to official statistics published by NLM in May 2025, 57% of worldwide croplands witnessed reductions in soil exposure, and 86% are subjected to an extreme climate scenario. Besides, to keep a control on this, the Standing Senate Committee on Agriculture and Forestry in Canada introduced a study report on identifying barriers in soil management and ensuring a wide-ranging federal strategy for soil health, which is responsible for positively impacting the sub-segment’s growth.

End use Facility Segment Analysis

Based on the end use facility, the commercial storage/warehousing segment in the agricultural fumigants market is projected to account for the second-largest share during the forecast period. The segment’s growth is primarily fueled by the aspect of comprising massive export grain silos at port terminals and centralized warehouse complexes that aggregate the production process from large-scale smallholder farms before processing or distribution. However, the fundamental challenge here is scale and containment that constitutes a single commercial silo can hold tens of thousands of metric tons of grain, creating a vast, three-dimensional space where pests can rapidly multiply if any fumigant concentration drops below lethal levels. Unlike on-farm storage, commercial warehousing operates under strict contractual timelines for quarantine clearance, forcing operators to execute fumigations with precision and speed.

Form Segment Analysis

By the end of the stipulated timeline, the gas sub-segment, which is part of the form segment, is expected to grab the third-largest share in the agricultural fumigants market. The sub-segment’s development is highly propelled by an increase in the demand for natural gas for producing nitrogen, which is considered one of the main fertilizer components, thereby enabling a surge in crop yields. As stated in an article published by NLM in September 2025, it has been estimated that soybean cultivation has the ability to fix roughly 16 million tons of nitrogen per year. This further accounts for approximately 77% of nitrogen, which is expected to be readily fixed by cultivated legumes. Besides, in the case of legumes, including mucuna, cowpea, crotalaria, and clover, which are suitable for incorporating in the soil, the nitrogen amount can fix almost 100 kg/ha, thereby positively impacting the expansion of gas implementation in agriculture.

Our in-depth analysis of the agricultural fumigants market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

End use Facility |

|

|

Form |

|

|

Pest Control Method |

|

|

Crop Type |

|

|

Product Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Agricultural Fumigants Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the agricultural fumigants market is anticipated to grab the highest share of 33.7% by the end of 2035. The market’s upliftment in the region is primarily attributed to the existence of the massive agricultural base, an increase in food security concerns, a surge in implementing modernized storage facilities, a rise in the demand for higher crop yields, and governmental approaches to diminish harvest losses and food security. According to official statistics published by Plant Communications in July 2025, the United Nations projected that the population in the region is poised to surpass 5 billion by the end of 2050, which caters to more than half of the worldwide population. This has led to readily prioritizing food yield, quality, and dietary diversity, along with bolstering the agricultural output. Besides, the region significantly holds 24.9% of the global arable land that is responsible for enhancing agricultural production and nourishment of the population, thus uplifting the agricultural fumigants market growth.

The agricultural fumigants market in China is growing significantly, owing to the expanded demand for pre-plant soil fumigation and post-harvest grain storage protection, an increase in investments for smart fumigation technologies by utilizing data analytics and sensors for controlling and monitoring the fumigation process, and developing controlled-release formulations. As per an article published by the State Council Information Office in March 2026, the planting area in the country effectively utilizes BeiDou technology and has eventually exceeded by 3.7 million mu, which is nearly 246,667 hectares as of 2025. Besides, more than 16,000 units of smart agricultural machinery are operating across different farmlands, particularly in East China's Shandong Province, thereby making it suitable for bolstering the market expansion.

The aspects of generous budget allocation, sustainable agricultural inputs, expansion of the Nano Di Ammonium Phosphate (DAP) application, the continuous incorporation of fumigation processes, and administrative regulations for manufacturing are certain factors that are responsible for uplifting the agricultural fumigants market in India. Based on government estimates published by the PIB Government in March 2026, the country successfully achieved an outstanding food grain production of 357.3 million metric tons between 2024 and 2025, along with the horticulture output of 362.0 million metric tons that reflects a robust transition towards high-value crops. Besides, agriculture and its allied activities account for almost 1/5th of the nation’s gross value added (GVA) and employ an estimated 46.1% of the overall workforce, and also readily supports 55% of the population. Moreover, the agricultural footprint is continuously expanding, thus denoting an optimistic outlook for the agricultural fumigants market demand in the overall country.

Agricultural Footprint Growth Analysis in India (2026)

|

Food Commodity |

Production |

|

Millets |

18.5 million tons |

|

Pulses |

25.6 million tons |

|

Spices |

12 million metric tons |

|

Coconut |

21.3 billion (yearly) |

|

Rice |

150.1 million tons |

|

Wheat |

117.9 million tons |

|

Fruits |

114.5 million tons |

|

Vegetables |

219.6 million tons |

|

Sugarcane |

454.6 million tons |

|

Cotton |

5.0 million tons |

|

Tea |

1.2 million tons |

Source: PIB Government

Europe Market Insights

Europe in the agricultural fumigants market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the strict regulatory oversight, a robust transition towards sustainable farming solutions, an escalation in the prevalence of soil-borne pathogens in intensified cropping systems, the monoculture of high-value crops, and growth in the chloropicrin industry. According to official statistics published by NLM in October 2025, farmers in the region have the liberty to voluntarily participate in eco-schemes under the Europe Agricultural Guarantee Fund, which is considered the first payment pillar, accounting for 25% of the regional funding. Meanwhile, the Europe Agricultural Fund for Rural Development, the second regional pillar, focuses on 35% fund allocation for voluntary Climate and Environmental Measures to support organic farming, thus proliferating the market development.

The agricultural fumigants market in Germany is gaining increased traction, owing to the presence of the most innovative chemical manufacturing facility, with organizational contributions to ensure crop protection, as well as the expanded cereal cultivation and high-value horticulture requirement, and focus on sustainable fumigation technologies. As per an article published by the Sino-German Agricultural Center in April 2025, a coalition was developed between the center-left SPD and the conservative CDU/CSU that has abandoned the utilization of chemical pesticides by 50%. In replacement, the country focuses on promoting precision farming and the adoption of pest management. Moreover, the coalition agreement has initiated an increased emphasis on fruit and vegetable production, based on which the country comprises a self-sufficiency rate of just 30%, which also caters to identifying both organic and traditional farming.

An increase in the demand for suitable crop protection chemicals, the presence of polytunnel and greenhouse agriculture, generous governmental support, focus on sustainable agricultural and chemical advancements, and suitable circular economy strategies are responsible for fueling the agricultural fumigants market in France. As per an article published by the Europe Environment Agency in September 2025, the country’s net greenhouse gas emissions have effectively decreased by 35% and by 8% between 2022 and 2023. Therefore, based on this successful reduction, the country is significantly respecting aims of the Paris Agreement, despite the domestic energy consumption being highly reliant on fossil fuels. Furthermore, the country’s climate and energy strategy has aimed to cater to decarbonization risks and adapt to climate change, thus making it suitable for fueling the market demand.

North America Market Insights

North America in the agricultural fumigants market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by the presence of strict regulatory policies, large-scale farming operations, an increase in the adoption of precision application technologies, and the robust preference for compliant and registered fumigant products. According to official statistics published by NLM in January 2026, precision farming has the capability to diminish water utilization by 20% to more than 50%, depending on specific implementation and environment. Additionally, this farming form grew at an average yearly rate of 15.1%, with the U.S. leading a huge surge in recent years. Besides, IoT-based irrigation systems are deliberately associated with more than 30% reinforcement automation and water saving approaches for optimizing disease and pest management efficiency, thus driving the market expansion in the overall region.

The agricultural fumigants market in the U.S. is gaining increased exposure, owing to the intensified cultivation of specialty and high-value crops, especially across the Pacific Northwest, Florida, and California, along with a strong regulatory framework for fueling innovation, and a continuous increase in exporting grains. Based on government estimates published by the ERS USDA Government in July 2025, there has been a steady growth in domestic agricultural exports that reached USD 176 billion as of 2024, denoting a rise from USD 52.9 billion in past years. Additionally, the share of high-value products (HVP), such as vegetables, fruits, meats, and dairy products account for 69% of the overall valuation in the country. Moreover, in terms of modified trade policies and a rise in household incomes, agricultural exports in the country grew by almost 6% to 17% in 2024, thereby positively fueling the market growth.

10-Year Export Analysis of Bulk and High-Value Products in the U.S. (2014-2024)

|

Year |

Bulk Products (USD Billion) |

High-Value Products (USD Billion) |

|

2014 |

52 |

103 |

|

2015 |

43 |

95 |

|

2016 |

47 |

92 |

|

2017 |

47 |

96 |

|

2018 |

46 |

99 |

|

2019 |

42 |

99 |

|

2020 |

52 |

98 |

|

2021 |

64 |

112 |

|

2022 |

75 |

120 |

|

2023 |

58 |

116 |

|

2024 |

55 |

121 |

Source: ERS USDA Government

The mandatory quarantine and pre-shipment fumigation demand, the presence of cold-climate grain storage conditions, generous funding opportunities by the government, and the increased focus on authorizing methyl bromide are factors that are driving the agricultural fumigants market in Canada. Based on government estimates published by the Canada Grain Commission in November 2025, between 2024 and 2025, the Canada Grain Commission’s overall expenditure amounted to USD 16,884,985, along with a total full-time equivalent staff of 477. Besides, in terms of investments, the Government of Canada significantly made enhancements to the AgriStability program by increasing the compensation rate from 80% to 90% and further doubling the payment to USD 6 million. Simultaneously, the Commission focused on fair compensation for farmers by initiating USD 19.5 million as a security payment for suitable producer claims, thereby making it suitable for boosting the market growth.

Key Agricultural Fumigants Market Players:

- BASF SE (Germany)

- Corteva Agriscience (U.S.)

- FMC Corporation (U.S.)

- UPL Limited (India)

- ADAMA Ltd. (Israel)

- Syngenta AG (Switzerland)

- AMVAC Chemical Corporation (U.S.)

- Nufarm Limited (Australia)

- Detia-Degesch GmbH (Germany)

- Arkema S.A. (France)

- Eastman Chemical Company (U.S.)

- LANXESS AG (Germany)

- Solvay S.A. (Belgium)

- Ikeda Kogyo Co., Ltd. (Japan)

- Kumiai Chemical Industry Co., Ltd. (Japan)

- Sumitomo Chemical Co., Ltd. (Japan)

- Mitsui Chemicals, Inc. (Japan)

- Nippon Soda Co., Ltd. (Japan)

- Balchem Corporation (U.S.)

- Landmark Fumigants (Australia)

- Kemin Industries (U.S.)

- FumiHogar (Spain)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- BASF SE leverages its deep expertise in crop protection chemistry to offer a portfolio of soil fumigants designed for high-value horticulture and specialty crops. The company focuses on developing formulations that balance efficacy against soil-borne pathogens with reduced environmental persistence.

- Corteva Agriscience maintains a strong presence in the agricultural fumigants sector through its legacy of innovative soil treatment solutions inherited from the Dow and DuPont merger. The company prioritizes research into next-generation fumigant alternatives that comply with evolving regulatory standards while protecting grower productivity.

- FMC Corporation is recognized as a leading innovator in soil fumigation technologies, particularly for high-demand crops like strawberries, potatoes, and tree nuts. The company actively pursues strategic partnerships and precision application methods to enhance worker safety and application efficiency.

- UPL Limited has emerged as a significant global player in agricultural fumigants by aggressively expanding its post-harvest protection portfolio across Asia, Africa, and Latin America. The company emphasizes accessible, cost-effective fumigation solutions tailored to smallholder farmers and large-scale storage operators alike.

- ADAMA Ltd. differentiates itself through a broad portfolio of off-patent fumigant active ingredients, offering affordable alternatives to proprietary chemistries without compromising on quality. The company focuses on simplifying application protocols and improving safety profiles for farmers in emerging agricultural markets.

Here is a list of key players operating in the global agricultural fumigants market:

The global agricultural fumigants market is highly consolidated, with the top multinational corporations commanding significant shares through expansive product portfolios and global distribution networks. The competitive landscape is defined by a shift towards sustainable and low-toxicity solutions in response to stringent environmental regulations, such as the Montreal Protocol. Notable players are actively pursuing strategic initiatives to maintain leadership, including acquisitions to expand geographic footprint and product offerings. For instance, in December 2025, BASF Agricultural Solutions and ADAMA Ltd. effectively signed a commercialization and co-development deal that centered on ADAMA’s proprietary fungicide active ingredient known as Gilboa. This particular deal escalated the delivery process of pioneering and newest disease management solutions for assisting farmers in Europe to overcome resistance and effectively maintain healthy yields, which has positively impacted the agricultural fumigants industry worldwide.

Corporate Landscape of the Agricultural Fumigants Market:

Recent Developments

- In July 2025, Kemin Industries introduced RevoCURB, which is the latest FIFRA25(b)-exempt soil treatment, for addressing the restrictions of conventional fumigants and offering a sustainable and safer alternative for both traditional and organic growers.

- In June 2025, FMC Corporation strategically formed an agreement with Corteva Agriscience for expanding its fluindapyr fungicide technology, especially in the U.S.-based soybean and corn industries.

- In February 2025, FumiHogar’s project, the Europe LIFE NextFUMIGREEN project, unveiled suitable advances in natural biopesticides through standard research and innovation on pesticides that permit a homogeneous distribution in environments without enhancing humidity and significantly enabling safety and efficacy for farmers.

- Report ID: 8503

- Published Date: Apr 07, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.