Advanced Ophthalmology Technology Market Outlook:

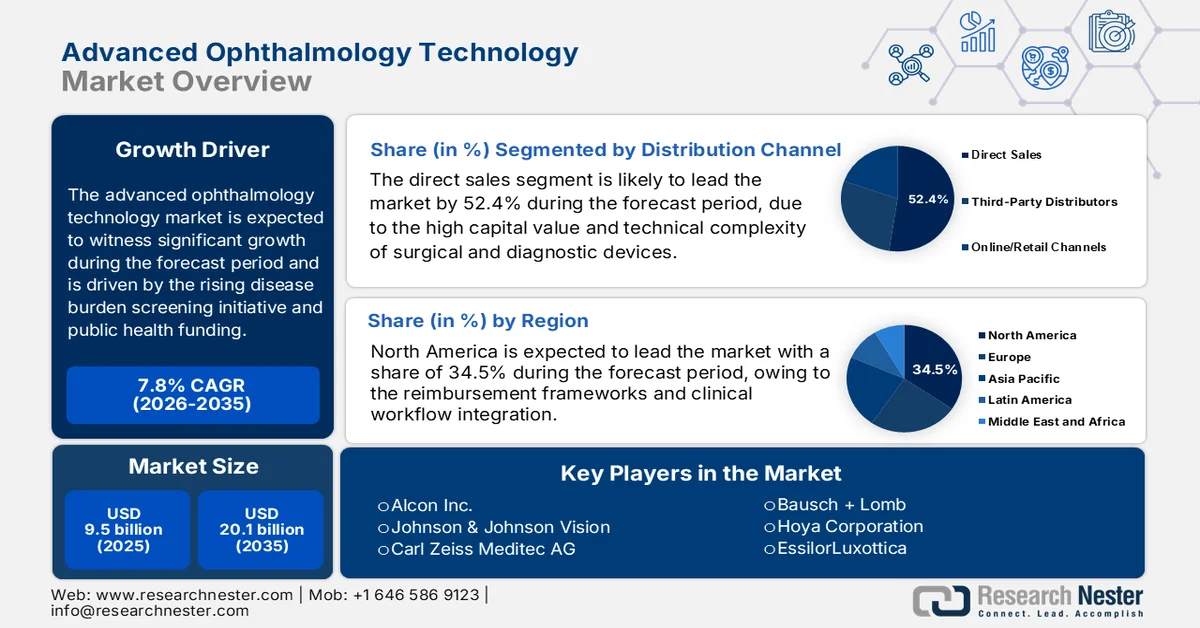

Advanced Ophthalmology Technology Market size was valued at USD 9.5 billion in 2025 and is projected to reach USD 20.1 billion by the end of 2035, rising at a CAGR of 7.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of advanced ophthalmology technology is assessed at USD 10.2 billion.

The advanced ophthalmology technology market is supported by the rising disease burden screening initiative and public health funding. According to the WHO March 2023 report, nearly 2.2 billion people globally have vision impairment of blindness, with over 1 billion cases preventable and yet to be addressed, creating a sustained demand for diagnostic imaging, surgical systems, and digital ophthalmic solutions across care settings. Moreover, the rising cataract surgeries are reflecting the sustained procedural volumes. As per the NLM study in January 2025 study the cataract surgical rate has been reported 36 to 12,800 per million population across different countries. The rising surgical rates across different regions show the uneven distribution of advanced ophthalmic infrastructure and present an active opportunity for suppliers seeking to expand into underpenetrated regions.

Besides, the public health initiatives aimed at addressing the preventable burden of vision impairment continue to drive the procurement of diagnostic imaging platforms and surgical systems, mainly in low and middle-income countries, where screening programs are scaling with the governmental and multilateral funding support. Moreover, the institutional programs and regulatory support are surging the technology deployment across regions. The NLM study published in April 2025 indicates that the National Eye Institute continues to fund translational research in retinal imaging gene therapies and tele ophthalmology with its annual budget of USD 835 million, reflecting a sustained federal commitment to innovation in ophthalmic care delivery. These factors enable the manufacturers to align product development pipelines with the key areas, such as portable diagnostic devices, facilitating advanced ophthalmology technology market entry via government-backed research initiatives and public health programs.

Key Advanced Ophthalmology Technology Market Insights Summary:

Regional Highlights:

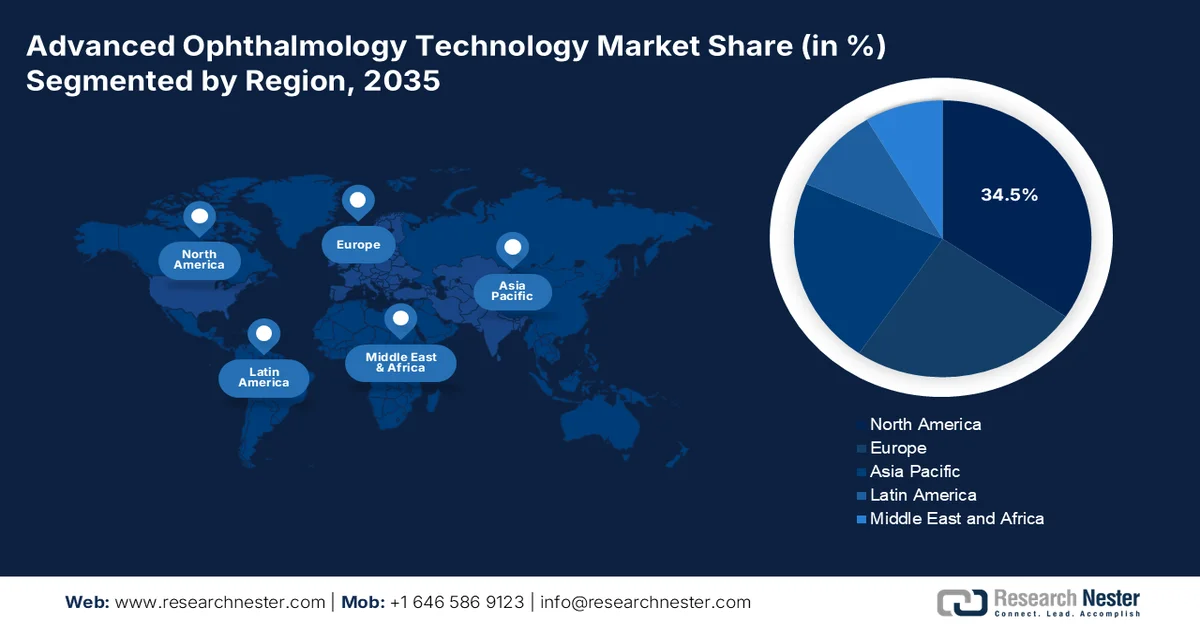

- In the advanced ophthalmology technology market, North America is projected to dominate with a 34.5% revenue share by 2035, owing to mature healthcare infrastructure and strong integration of reimbursement frameworks with clinical workflows

- Asia Pacific is anticipated to be the fastest-growing region with a CAGR of 11.5% during 2026–2035, fueled by rapid healthcare infrastructure expansion and rising burden of age-related eye diseases

Segment Insights:

- In the advanced ophthalmology technology market, the direct sales sub-segment under distribution channel is projected to account for a 52.4% share by 2035, propelled by the high capital value and technical complexity of surgical and diagnostic devices

- The cataract surgery sub-segment within the application segment is anticipated to dominate by 2035, capturing the largest share impelled by the aging demographic and increasing adoption of premium intraocular lenses and femtosecond laser-assisted platforms

Key Growth Trends:

- Rising public expenditure on vision care programs

- Expansion of national screening programs

Major Challenges:

- High capital costs and accessibility challenge

- Shortage of skilled professionals

Key Players: Alcon Inc., Johnson & Johnson Vision, Carl Zeiss Meditec AG, Bausch + Lomb, Hoya Corporation, EssilorLuxottica, NIDEK Co. Ltd., Topcon Corporation, STAAR Surgical Company, Haag-Streit Group, Ziemer Ophthalmic Systems AG, Lumenis Be Ltd., Rayner Intraocular Lenses Limited, Aurolab, Appasamy Associates, Ellex Medical Lasers, Merck, EyeBio, NTC, Eyexora.

Global Advanced Ophthalmology Technology Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 9.5 billion

- 2026 Market Size: USD 10.2 billion

- Projected Market Size: USD 20.1 billion by 2035

- Growth Forecasts: 7.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (34.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, India

- Emerging Countries: South Korea, Brazil, Mexico, Indonesia, Malaysia

Last updated on : 27 March, 2026

Advanced Ophthalmology Technology Market - Growth Drivers and Challenges

Growth Drivers

- Rising public expenditure on vision care programs: The government healthcare budgets are actively allocating funds toward ophthalmic care, which is directly supporting the procurement of advanced technologies. According to the CMS January 2026 data, the healthcare expenditure in the U.S. reached USD 5.3 trillion in 2024, covering high volumes of ophthalmic procedures such as cataract surgeries. This sustained reimbursement environment enables hospitals and ambulatory surgical centers to invest in advanced surgical platforms and imaging systems. Similarly, the NHS continues to expand the ophthalmology capacity via long-term workforce and infrastructure funding plans reflecting the growing patient backlogs. These funding patterns are promoting the vendors to align offering with reimbursement-supported procedures and cost efficiency benchmarks.

- Expansion of national screening programs: The large-scale screening initiatives are a significant factor fueling the demand for imaging and diagnostic technologies in the advanced ophthalmology technology market. As per the data published by the NHS in the November 2024 report, the Diabetic Eye Screening Programme has screened over 3.3 million people annually in England. This necessitates the widespread deployment of retinal imaging systems and digital data platforms. Moreover, these programs are increasing the integration of AI-assisted diagnostics to manage patient volumes efficiently. The scale of these initiatives creates a recurring demand for upgrades, maintenance, and interoperability solutions. Vendors that offer scalable and cloud-integrated imaging technologies are better positioned to capture long term contacts.

- Digital health and teleophthalmology investments: Governments are now actively investing in the digital health infrastructure and boosting the demand for the advanced ophthalmology technology market. The U.S. Department of Health and Human Services promotes the expansion of telehealth via reimbursement policies and infrastructure funding, enabling remote eye care services. Teleophthalmology programs supported by the federal initiatives are improving access in rural and underserved areas, driving the adoption of portable imaging devices and cloud-based diagnostic platforms. Moreover, the EU’s digital health strategies emphasize interoperability and electronic health records integration, supporting the ophthalmic data exchange. These initiatives are pushing the providers toward scalable software-driven solutions that integrate with national health systems.

Challenges

- High capital costs and accessibility challenge: The advanced nature of the ophthalmic devices, such as femtosecond lasers and robotic surgical systems, results in prohibitively high acquisition costs. This creates a significant barrier to entry for new manufacturers in the advanced ophthalmology technology market who invest heavily in R&D, and for suppliers trying to sell into price-sensitive markets. Though the advanced ophthalmology technology market is set to grow, the government pricing constraints and the high costs are limiting the broader accessibility. These costs often restrict the adoption to well-funded hospitals in the developed regions, making it difficult for the new entrants to achieve a rapid market penetration.

- Shortage of skilled professionals: The adoption of advanced ophthalmology technology is heavily dependent on the availability of trained clinicians. A lack of skilled professionals to operate complex diagnostic and surgical equipment creates a significant bottleneck for market penetration, mainly in emerging economies. The new manufacturers face this problem, and clinicians avoid adopting new complex devices without proper training, and investing in large-scale training programs is also costly. Top player uses their existing consumer base to integrate the new surgical platforms into clinical practices.

Advanced Ophthalmology Technology Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.8% |

|

Base Year Market Size (2025) |

USD 9.5 billion |

|

Forecast Year Market Size (2035) |

USD 20.1 billion |

|

Regional Scope |

|

Advanced Ophthalmology Technology Market Segmentation:

Distribution Channel Segment Analysis

Under the distribution channel segment, the direct sales sub-segment is leading and is poised to hold the largest share value of 52.4% by the end of 2035. The segment is driven by the high capital value and technical complexity of surgical and diagnostic devices. The manufacturers use direct sales forces to maintain strong relationships with the hospitals and the ambulatory surgical centers, ensuring proper installation, training, and long-term service contracts. This model allows companies to control pricing, manage supply chain integrity, and introduce premium innovations such as AI-integrated platforms directly to key opinion leaders. According to the Medpac March 2025 data, nearly 40% of the domestic production of medical devices, which includes the ophthalmology technologies are exported. This shows the sustained preference for direct engagement in capital equipment transactions.

Application Segment Analysis

Within the application segment, the cataract surgery sub-segment remains the largest in the advanced ophthalmology technology market by the end of 2035. The segment is driven by the aging demographic and the increasing adoption of the premium intraocular lenses and femtosecond laser-assisted platforms. The demand for advanced surgical technologies is further fueled by patients' expectations for better visual outcomes and reduced recovery times. Strategic investments in portable phacoemulsification systems have expanded access to ambulatory surgical centers. According to the NLM March 2025 study, nearly 3.7 million cataract surgeries were performed in the U.S. annually. This demand reflects the sustained clinical and economic demand for advanced cataract intervention as the primary application driving the market demand.

End user Segment Analysis

The ambulatory surgical centers (ASCs) are the leading sub-segment in the end-user segment in the advanced ophthalmology technology market, fueled by the industry-wide shift toward cost-efficient outpatient surgical care. The ASC offers enhanced patient convenience, reduced hospital-acquired infection risks, and favorable reimbursement structures, making it the preferred setting for cataract, glaucoma, and refractive procedures. The integration of compact advanced surgical platforms has further enabled ASCs to perform increasingly complex ophthalmic surgeries. Moreover, the number of certified ASCs performing ophthalmic surgeries has increased nationwide, accelerating the role of ASCs as the dominant end user segment driving market adoption.

Our in-depth analysis of the advanced ophthalmology technology market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Technology |

|

|

Application |

|

|

End user |

|

|

Modality |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Advanced Ophthalmology Technology Market - Regional Analysis

North America Market Insights

North America is dominating the advanced ophthalmology technology market and is projected to hold the regional revenue share of 34.5% by the end of 2035. The market is defined by the mature healthcare infrastructure, where purchasing decisions are heavily influenced by the reimbursement frameworks, clinical workflow integration, and the concentration of surgical procedures in ambulatory care settings. Manufacturers and suppliers operating in this region navigate a landscape defined by the group of purchasing organizations, integrated delivery networks, and large-scale public health systems such as the Department of Veterans Affairs, which consolidate procurement volumes and exert significant price pressure. The competitive success in North America is based on the ability to offer integrated hardware-software solutions that align with hospital and ASC workflow needs, supported by direct sales forces capable of managing complex, multi-stakeholder purchasing processes involving surgeons, administrators, and supply chain executives.

The advanced ophthalmology technology market in the U.S. is supported by sustained federal healthcare spending, a high procedure volume, and increasing disease burden. The CMS data depicts that the U.S. national health expenditure is reflecting continued allocation toward high-volume specialties such as ophthalmology, mainly cataract and retinal procedures. Moreover, the NLM study in July 2023 depicted that nearly 22 million people had cataracts in the U.S., reinforcing consistent demand for surgical platforms and intraoperative technologies. On the other hand, the Centers for Disease Control and Prevention's May 2024 data reported that nearly 7 million people are living with vision impairment, highlighting a large and growing patient pool requiring ongoing diagnostic and treatment interventions. These factors show an optimistic growth in the U.S. market.

U.S. Vision Impairment and Eye Health Statistics Overview (2024)

|

Category |

Key Statistics |

|

Overall Vision Impairment |

~7 million people in the U.S. have vision impairment, including ~1 million who are blind |

|

Adult Vision Impairment (Age 40+) |

4.2 million Americans (as of 2012); projected to more than double by 2050 |

|

Pediatric Vision Conditions |

6.8% of children (<18) have a diagnosed eye/vision condition; ~3% have blindness or vision impairment |

|

At-Risk Adult Population |

~93 million U.S. adults at high risk for serious vision loss; only ~50% had an eye exam in the past year |

|

Preventable Blindness (Diabetes-related) |

~90% of blindness due to diabetes in U.S. adults is preventable with early detection and treatment |

Source: CDC May 2024

The universal healthcare funding, aging demographics, and the increasing prevalence of vision disorders are fueling the advanced ophthalmology technology market in Canada. According to the Canadian Medical Association 2026 data, the total health expenditure reached USD 344 billion in 2023, reflecting a sustained public investment in the hospital infrastructure and specialized care, including ophthalmology services. The Canadian Ophthalmological Society's May 2023 data estimates that over 8 million people in the nation live with eye conditions that could lead to vision loss, including age-related macular degeneration, glaucoma, and diabetic retinopathy, creating a steady demand for diagnostic imaging and surgical technologies. Moreover, the aging population is increasing the burden of age-related eye diseases and driving procedural volumes across cataract and retinal care, thus boosting the advanced ophthalmology technology market expansion and growth.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region and is expected to expand at a CAGR of11.5% during the assessed period, 2026 to 2035. The region is driven by the rapid healthcare infrastructure expansion, large-scale national screening programs, and a significant burden of age-related eye disease driven by demographic aging across Japan, China, South Korea, and emerging economies. China’s National Health Commission has integrated ophthalmic services into its Healthy China 2030 framework, and India’s National Programme for Control of Blindness and Visual Impairment continues to expand surgical capacity. On the other hand the Japan and South Korea maintain mature markets with high adoption rates of premium intraocular lenses and femtosecond laser technologies. The region benefits from increasing medical tourism, particularly in Malaysia and South Korea, where private healthcare providers offer advanced refractive and cataract surgeries to international patients.

The rapidly increasing burden of cataract-related vision impairment and risk factors is driving the advanced ophthalmology technology market in China. According to the NLM September 2023 data, the cataract cases in China rose from 5.6 million to 18.1 million in the past decade, while disability adjusted life years (DALYs) increased from 449,000 to 1.08 million during the same period, reflecting a significant rise in disease burden. Further, the cataract prevalence reached 43.7 million cases, with DALYs increasing to over 2.3 million, indicating sustained long-term demand for surgical interventions and diagnostic technologies. On the other hand, the NLM October 2023 data depicted that cataract blindness is expected to rise sharply, and reach 40 million in 2025, driven by aging demographics and risk factors. These trends are accelerating demand for the positive impact on market growth.

Reported Cataract Surgery Cases by Age (2023)

|

Age |

Registered Cases |

|

≤40 |

216 439 |

|

41–50 |

534 453 |

|

51–60 |

1 656 195 |

|

61–70 |

4 438 982 |

|

71–80 |

5 386 356 |

|

≥81 |

1 925 038 |

|

≤40 |

216 439 |

Source: NLM April 2023

The large scale government initiatives under the National Programme for Control of Blindness and Visual Impairment is shaping the advanced ophthalmology technology market in India. According to the Digital Sansad February 2024 data, nearly 7.5 million cataract surgeries were performed from 2022 to 2023, which increased to 9 million for 2023 to 2024 and 10.5 million for 2024 to 2025, indicating a strong upward trajectory in procedural demand. Moreover, performance has exceeded expectations with 8.34 million surgeries completed in 2023 and 5.64 million surgeries already performed by December 2024, reflecting accelerated execution capacity. Additionally, integrated initiatives such as corneal collection for keratoplasty and spectacle distribution are expanding the scope of ophthalmic care, further supporting demand for diagnostic and treatment technologies across both urban and rural healthcare infrastructure.

Europe Market Insights

The advanced ophthalmology technology market in Europe is expanding rapidly and is shaped by an aging demographic, public healthcare system procurement cycles, and regulatory harmonization under the EMA and European Commission. The region benefits from established ophthalmic surgery networks and a strong emphasis on early disease detection via national screening programs. The implementation of the medical device regulation has raised the clinical evidence requirements, influencing the product approval timelines and market entry strategies. Public health iniatives including the EU4Health Programme, allocate funding for digital health infrastructure and telemedicine, supporting the deployment of diagnostic imaging platforms across underserved regions. The manufacturers prioritizing regulatory compliance and health economy data are positioned to capture the public procurement contracts.

A high cataract prevalence and cost-sensitive adoption of premium surgical technologies are driving the advanced ophthalmology technology market in Germany. According to the NLM study in June 2025, data from nearly 4.8 million people in Germany were affected by cataracts, with the prevalence rising sharply with age, impacting over 90% of individuals aged 65 to 75, which sustains strong procedural demand for cataract surgeries. On the other hand, the standard outpatient cataract surgery costs are estimated at USD 980 to USD 1090, whereas femtosecond laser-assisted procedures range from USD 760 to USD 2290, creating variability in provider adoption depending on economic feasibility, based on NLM June 2025 study. These data favor technologies that demonstrate clear clinical and economic value within statutory health insurance frameworks, thus driving the market growth.

The rising outpatient volumes and increasing surgical activity are driving the advanced ophthalmology technology market in the UK. According to the Government of the UK, July 2025 data, nearly 9.8 million hospital outpatient appointments for vision in England represent a 27% increase in the appointments since the past decade, highlighting a sustained demand for diagnostic imaging and monitoring technologies. Moreover, the procedural volumes are also expanding, with 581,369 cataract surgery admissions recorded in 2024, indicating a demand for surgical systems such as phacoemulsification and laser-assisted platforms. Additionally, advanced treatment procedures are scaling with 830,687 intravitreal injection therapies performed, reflecting a 233% rise driven by the growing prevalence of retinal diseases and the expanded treatment access. These trends are showing an active upliftment in the market expansion.

Key Advanced Ophthalmology Technology Market Players:

- Alcon Inc. (Switzerland)

- Johnson & Johnson Vision (U.S.)

- Carl Zeiss Meditec AG (Germany)

- Bausch + Lomb (U.S.)

- Hoya Corporation (Japan)

- EssilorLuxottica (France)

- NIDEK Co., Ltd. (Japan)

- Topcon Corporation (Japan)

- STAAR Surgical Company (U.S.)

- Haag-Streit Group (Switzerland)

- Ziemer Ophthalmic Systems AG (Switzerland)

- Lumenis Be Ltd. (Israel)

- Rayner Intraocular Lenses Limited (UK)

- Aurolab (India)

- Appasamy Associates (India)

- Ellex Medical Lasers (Australia)

- Merck (Germany)

- EyeBio (UK)

- NTC (South Korea)

- Eyexora (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Alcon Inc. is a dominant player in the advanced ophthalmology technology market, recognized for its comprehensive portfolio spanning surgical equipment, intraocular lenses, and dry eye diagnostics. The company has advanced its position via digital connectivity, exemplified by its smart cataract surgery ecosystem and the acquisition of the lvantis which has enhanced the minimally invasive glaucoma surgery offerings.

- Johnson & Johnson Vision maintains a formidable presence in the advanced ophthalmology technology market by using its expertise in both surgical and vision care segments. The company’s strategic initiatives center on expanding its premium IOL portfolio mainly via its Tecnis family and advancing femtosecond laser-assisted cataract surgery platforms. The company has invested USD 50 billion in R&D in 2024.

- Carl Zeiss Meditec AG stands as a leader in the advanced ophthalmology technology market, renowned for its high-precision diagnostic imaging, surgical microscopes, and digital workflow platforms. The company has adopted a strategy centered on the integrated digital ecosystems, such as its FORUM platform, which enables seamless data management across the surgical devices.

- Bausch + Lomb maintains a significant position in the advanced ophthalmology technology market via its diversified portfolio that includes surgical instruments, intraocular lenses, and pharmaceutical eye care. The company’s strategic initiatives emphasize innovation in premium cataract surgery with its advanced IOL technologies and the expansion of its MIGS product line. In 2024, the company has reported a revenue of USD 1.280 billion in Q4.

- Hoya Corporation is a key player in the advanced ophthalmology technology market, primarily recognized for its high-quality intraocular lenses and advanced surgical equipment. The company’s strategic focus revolves around material science innovation, mainly in hydrophobic IOLs that offer enhanced visual outcomes and reduced postoperative complications.

Here is a list of key players operating in the global advanced ophthalmology technology market:

The advanced ophthalmology technology market is highly consolidated, defined by the intense R&D rivalry and a trend toward vertical integration. The key players are actively pursuing strategic initiatives such as mergers and acquisitions to expand the surgical and diagnostic portfolios, mainly in premium intraocular lenses and digital connectivity. For example, in May 2024, Merck acquired EyeBio. There is a significant shift toward minimally invasive glaucoma surgery and AI-driven diagnostic platforms. To maintain the market share, leaders are focusing on geographic expansion in emerging markets while investing heavily in next-gen technologies such as refractive laser combinations and home-based monitoring devices.

Corporate Landscape of the Advanced Ophthalmology Technology Market:

Recent Developments

- In December 2025, NTC announced the completion of the acquisition of Pharmathen’s ophthalmology business. The acquisition adds to NTC a consolidated global portfolio of glaucoma treatments, manufactured at various third-party facilities in Europe and the U.S.

- In November 2025, the ZEISS brand, eye care professionals, and providers established a ZEISS VISION CLINIC, the first eye care solution model in Mexico City, a concept that brings together an end-to-end interconnected technology ecosystem.

- In October 2025, Singapore Eye Research Institute (SERI) and Eyexora inked a deal to create Y.ora and advance a minimally invasive surgical device for the treatment of mild-to-severe open-angle glaucoma (OAG).

- Report ID: 8477

- Published Date: Mar 27, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.