Veterinary Hematology Analyzers Market Outlook:

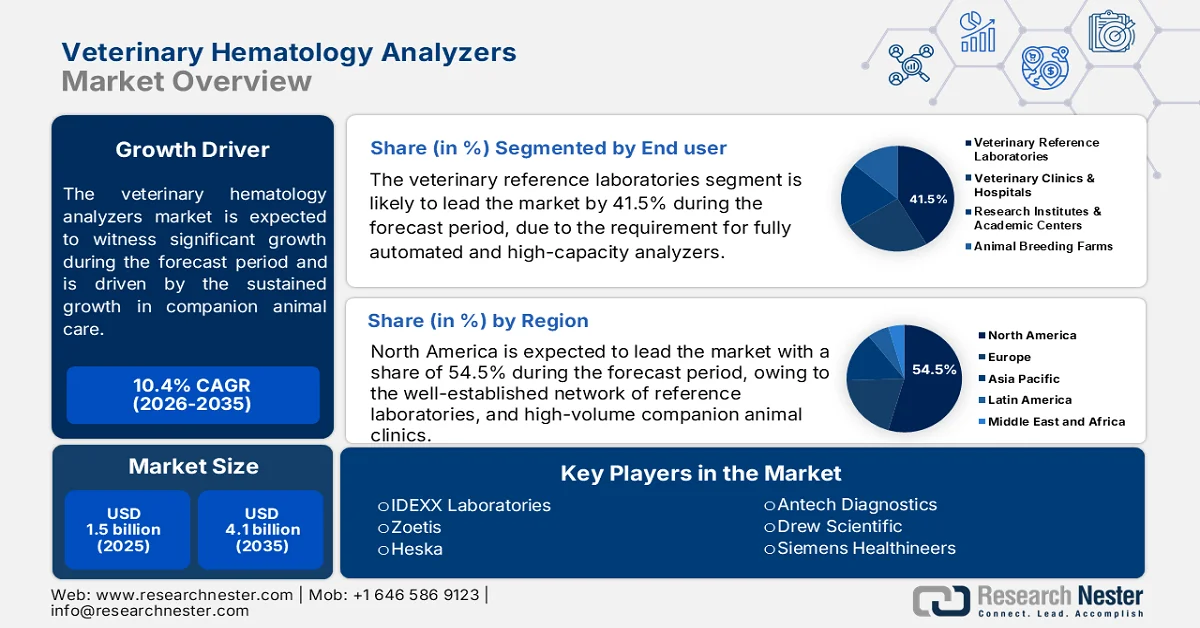

Veterinary Hematology Analyzers Market size was over USD 1.5 billion in 2025 and is projected to cross USD 4.1 billion by the end of 2035, growing at more than 10.4% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of veterinary hematology analyzers is estimated at USD 1.7 billion.

The veterinary hematology analyzers market is supported by sustained growth in companion animal care, higher utilization of diagnostic testing in veterinary practice, and expanding preventive health programs. The AVMA November 2024 data also reported that 59.8 million U.S. households owned dogs and 42.1 million owned cats in 2024, creating a substantial base of animals requiring routine wellness assessments, pre-surgical evaluations, and chronic disease monitoring. Hematology testing remains a standard component of these workflows because blood-based assessment supports evaluation of infection, inflammation, anemia, immune status, and treatment response. Demand is also reinforced by the aging pet population, as older animals require more frequent monitoring and repeat laboratory testing. These factors collectively support recurring instrument utilization and consumable demand across small-animal clinics, specialty hospitals, emergency centers, and veterinary laboratory networks.

The livestock sector also contributes significantly to analyzer demand through disease surveillance, herd health management, and food-animal productivity programs. The U.S. Department of Agriculture January 2024 data reported approximately 87.2 million head of cattle and calves, 74.5 million hogs and pigs, and more than 518 million chickens in national inventories during recent reporting periods, highlighting the scale of animal populations requiring health monitoring. Federal and international animal health programs continue to emphasize early disease detection, biosecurity, and monitoring of production animals, increasing the need for laboratory-supported diagnostics. Procurement activity is particularly supported by the need for reliable testing capacity, workflow standardization, and timely diagnostic information across both private veterinary practices and institutional animal health networks.

Key Veterinary Hematology Analyzers Market Insights Summary:

Regional Insights:

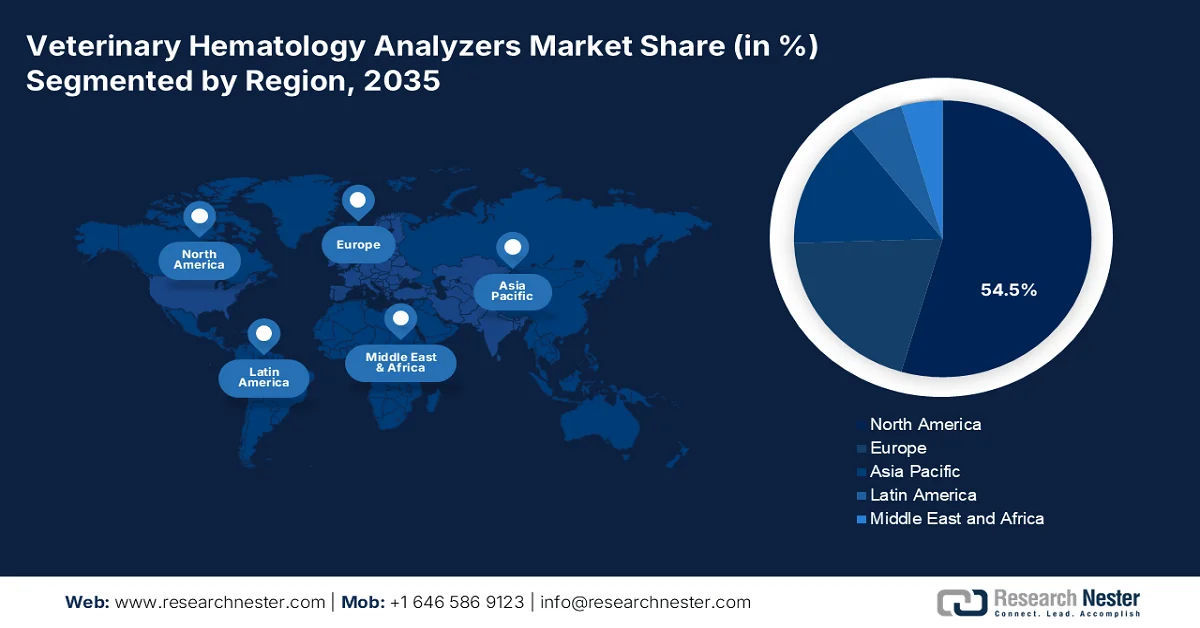

- North America is anticipated to command 54.5% of the veterinary hematology analyzers market revenue by 2035, underpinned by the extensive presence of reference laboratories, academic veterinary institutions, and high-volume companion animal clinics

- Asia Pacific is set to witness rapid expansion throughout 2026-2035 in the market, stimulated by the growing veterinary infrastructure supported by rising companion animal ownership and intensification of livestock farming

Segment Insights:

- Veterinary reference laboratories are projected to account for 41.5% of the veterinary hematology analyzers market by 2035, reinforced by the expansion of centralized high-throughput diagnostic facilities investing in fully automated hematology analyzers for large-volume testing and biosafety-compliant pathogen surveillance

- Companion animals are expected to remain the dominant animal type segment in the market through 2035, fueled by rising pet ownership and increasing expenditure on preventive healthcare for dogs and cats

Key Growth Trends:

- Increased funding for animal disease surveillance

- Rising government investment in animal disease surveillance

Major Challenges:

- Stringent regulatory approvals

- Distribution and After-Sales Service Network Gaps

Key Players: IDEXX Laboratories (U.S.),Zoetis (U.S.),Heska (U.S.),Antech Diagnostics (U.S.),Drew Scientific (U.S.),Siemens Healthineers (Germany),Nihon Kohden (Japan),Sysmex (Japan),Hitachi High-Tech (Japan),Fujifilm (Japan),Scil Animal Care (Germany),Woodley Equipment Company (UK),Boule Medical (Sweden),Horiba (France),EKF Diagnostics (UK),bioMérieux (France),BPC BioSed (Italy),Samsung Medison (South Korea),Transasia Bio-Medicals (India),Skanex (Malaysia).

Global Veterinary Hematology Analyzers Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.5 billion

- 2026 Market Size: USD 1.7 billion

- Projected Market Size: USD 4.1 billion by 2035

- Growth Forecasts: 10.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (54.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, South Korea, Australia, Brazil, Singapore

Last updated on : 8 June, 2026

Veterinary Hematology Analyzers Market - Growth Drivers and Challenges

Growth Drivers

- Increased funding for animal disease surveillance: The U.S. Department of Agriculture has significantly increased appropriations for the National Animal Health Laboratory Network. According to the Congress.gov April 2026 data, Congress allocated USD 65 million specifically for NAHLN infrastructure upgrades, including hematology analyzers for biosafety Level 2 and 3 laboratories. This funding enables reference labs to purchase high-throughput, fully automated analyzers for rapid outbreak response. Manufacturers should target NAHLN Level 1 and 2 laboratories with ruggedized, high-capacity analyzers capable of processing many samples per hour. The rising market growth is driven by increased government spending in Asia and Europe.

- Rising government investment in animal disease surveillance: Government-funded animal health surveillance programs are increasing demand for veterinary hematology analyzers because routine blood testing is a key component of disease detection and herd health monitoring. The USA Facts October 2025 data allocated approximately USD 754.2 million for Animal and Plant Health Inspection Service programs, supporting animal disease prevention, surveillance, and emergency preparedness activities. Hematology testing is frequently used in investigations of infectious diseases, livestock health assessments, and outbreak response. As governments strengthen preparedness against zoonotic and livestock diseases, procurement of laboratory instruments is expected to increase, particularly among public veterinary laboratories and reference centers responsible for large-scale surveillance programs.

Challenges

- Stringent regulatory approvals: Manufacturers must navigate complex regulatory pathways, including FDA Class II medical device clearance and CE-IVDR certification in Europe. The approval process takes months on average. Though the global veterinary hematology analyzers market is expected to grow, despite regulatory delays increasing time-to-market.

- Distribution and After-Sales Service Network Gaps: Veterinary clinics demand rapid technical support and reagent replenishment. Building a nationwide service network requires significant capital. Leading companies overcame this by acquiring regional distributors across Europe, adding several service technicians. This reduced the average response time.

Veterinary Hematology Analyzers Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

10.4% |

|

Base Year Market Size (2025) |

USD 1.5 billion |

|

Forecast Year Market Size (2035) |

USD 4.1 billion |

|

Regional Scope |

|

Veterinary Hematology Analyzers Market Segmentation:

End user Segment Analysis

Veterinary reference laboratories represent the leading end user sub-segment in the veterinary hematology analyzers market and is poised to hold the share value of 41.5% by the end of 2035. The segment is driven by facilities like the Virginia-Maryland College of Veterinary Medicine's VMDL. As one of only 35 Level 1 labs in the National Animal Health Laboratory Network and one of 48 in the FDA Veterinary Investigation and Response Network, the VMDL performs routine animal disease diagnosis, outbreak response, and food safety testing, as per the Mizzou April 2025 data. Phase I infrastructure improvements, including biosafety Level 2 and 3 laboratories, a dedicated classroom, and advanced HVAC systems, enable faster, safer, and more accurate diagnostic surveillance. Such centralized, high-throughput facilities invest heavily in fully automated hematology analyzers, driving market demand for precision instruments capable of handling large sample volumes while maintaining strict biosafety protocols for emerging pathogens.

Animal Type Segment Analysis

The companion animals’ sub-segment, particularly dogs and cats, dominates the veterinary hematology analyzers market due to rising pet ownership and increased spending on preventive care. Routine complete blood counts are essential for diagnosing anemia, infections, and leukemia in aging pet populations. Data from the American Pet Products March 2023 data indicates that over 66% of U.S. households owned a pet, with dogs and cats driving increase in veterinary hematology testing volumes. As pets live longer due to better nutrition and medicine, chronic disease monitoring becomes routine. This demographic shift compels veterinary practices to adopt benchtop and portable hematology analyzers for real-time, in-clinic results, particularly for geriatric wellness panels.

Technology Segment Analysis

Laser flow cytometry stands as the leading technology sub-segment within the veterinary hematology analyzers market due to its superior accuracy and multiplexing capabilities. This technology utilizes focused laser beams to illuminate individual cells as they pass through a fluid stream, measuring light scatter and fluorescence emission. These optical signatures allow precise differentiation of white blood cells, red blood cells, and platelets based on size, granularity, and DNA content. Unlike conventional impedance methods, laser flow cytometry excels at identifying immature or atypical cells, including blasts and reactive lymphocytes. This high sensitivity makes it invaluable for diagnosing complex hematological disorders such as leukemia, autoimmune anemia, and thrombocytopenia in companion animals, thereby driving its widespread adoption in reference laboratories and advanced veterinary clinics.

Our in-depth analysis of the veterinary hematology analyzers market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Modality |

|

|

Animal Type |

|

|

End user |

|

|

Technology |

|

|

Sales Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Veterinary Hematology Analyzers Market - Regional Analysis

North America Market Insights

North America is dominating the veterinary hematology analyzers market and is expected to hold the regional revenue share of 54.5% by the end of 2035. The market is characterized by a well-established network of reference laboratories, academic veterinary institutions, and high-volume companion animal clinics. Demand is driven by routine wellness screening, chronic disease management in aging pet populations, and regulatory requirements for livestock health certification. Key trends include the adoption of differential analyzers, increasing preference for point-of-care devices in rural practices, and emphasis on multi-species validation for food animal testing. Regulatory oversight from the FDA and Health Canada ensures that all commercial analyzers meet stringent performance and safety standards before market entry.

The expanding animal health surveillance programs, veterinary laboratory modernization, and demand for faster diagnostic testing is shaping the veterinary hematology analyzers market in the U.S. According to the USDA March 2025 data, the country had approximately 1.88 million farms and ranches, creating a substantial requirement for livestock health monitoring and diagnostic services. In addition, the U.S. FDA June 2022 data indicates National Animal Health Laboratory Network (NAHLN) comprises more than 60 participating laboratories that support animal disease surveillance and testing nationwide. As veterinary clinics, academic centers, and diagnostic laboratories increase testing capacity to improve disease detection and herd management, demand for hematology analyzers is expected to remain strong across both companion animal and livestock healthcare segments.

The increasing investment in animal health management, livestock monitoring, and veterinary diagnostic services is driving the veterinary hematology analyzers market in Canada. According to Manitoba Cooperator February 2026 data, the country's cattle inventory reached approximately 11.1 million, highlighting the continued need for veterinary testing and herd health surveillance across the livestock sector. Additionally, the Canadian Food Inspection Agency (CFIA) reported that its planned spending allocates significant portion directed toward safeguarding animal health, disease prevention, and inspection activities. These initiatives are encouraging veterinary laboratories, research institutions, and animal health providers to strengthen diagnostic capabilities, supporting demand for hematology analyzers used in routine blood analysis, disease detection, and animal health monitoring.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035 in the veterinary hematology analyzers market. The market is characterized by rapid expansion of veterinary infrastructure, driven by rising companion animal ownership and intensification of livestock farming. The region benefits from government-led animal disease surveillance programs and growing foreign direct investment in veterinary diagnostics. Emerging trends include adoption of laser flow cytometry in metropolitan clinics and increased distribution partnerships between global brands and regional suppliers to navigate local procurement channels and after-sales service requirements.

The rising animal healthcare infrastructure and livestock disease management programs is driving the veterinary hematology analyzers market in India. According to the PIB September 2025 data, India produced a record 239.3 million tonnes of milk in FY 2023–24, reflecting the scale of dairy operations that require routine veterinary monitoring and diagnostic support. In addition, the Government of Odisha February 2022 data the nation has allocated approximately ₹4,352 crore to the Livestock Health and Disease Control Programme (LHDCP) for 2024–25, supporting disease surveillance, vaccination, and animal health services nationwide. These investments are increasing the demand for laboratory-based diagnostics and point-of-care testing across veterinary hospitals, livestock farms, and research institutions, thereby driving adoption of hematology analyzers for efficient animal health assessment and disease detection.

The animal disease control systems and support large-scale livestock production is shaping the veterinary hematology analyzers market in China. According to the AHDB April 2025 data, the country produced approximately 70.26 million tons of pork in 2024, underscoring the need for extensive veterinary health monitoring across commercial swine operations. In addition, the Ministry of Agriculture and Rural Affairs reported that China maintained an inventory of pigs, one of the largest livestock populations globally. The scale of animal production, combined with ongoing government efforts to improve disease surveillance, biosecurity, and food safety, is driving demand for veterinary diagnostic infrastructure, including hematology analyzers used for routine blood testing and disease management.

Europe Market Insights

The stringent regulatory standards under the In Vitro Diagnostic Regulation and a strong emphasis on zoonotic disease surveillance across member states is driving the veterinary hematology analyzers market in Europe. Key markets include Germany, France, the United Kingdom, Italy, and Spain, supported by well-funded reference laboratories and academic veterinary institutions. Demand is driven by routine health screening for companion animals, livestock trade compliance, and participation in EU-wide One Health monitoring programs. Manufacturers prioritize CE-IVDR certification, multi-species validation, and integration with national laboratory information systems. Regional trends include consolidation of public veterinary labs, increasing adoption of fully automated 5-part differential analyzers, and growing preference for compact benchtop units suitable for both small animal clinics and food safety testing facilities.

Advanced diagnostic practices and strong animal health infrastructure is shaping the veterinary hematology analyzers market in Germany. Veterinary laboratories continue to use standardized reference methods, such as manual chamber counting with a 1:200 blood dilution and duplicate RBC/non-RBC counts, to validate automated hematology systems and ensure analytical accuracy, as per NLM April 2025 study. The presence of German suppliers such as Bioanalytic GmbH in specialized veterinary hematology consumables highlights the country’s established diagnostic ecosystem. Combined with Germany’s large livestock sector and increasing adoption of automated veterinary laboratory technologies, demand for hematology analyzers is expected to grow as clinics and laboratories seek faster, standardized, and quality-assured blood analysis for companion and production animals.

The veterinary practices increasingly adopt advanced in-clinic diagnostics to improve workflow efficiency and accelerate clinical decision-making. These are driving the veterinary hematology analyzers market in UK. A notable example is Zoetis’ in September 2024 data unveiling of the AI-powered Vetscan OptiCell™ hematology analyzer at the London Vet Show 2024, demonstrating the UK's role as a key market for innovative veterinary diagnostic technologies. The analyzer combines cartridge-based testing, AI-driven blood cell classification, and point-of-care complete blood count (CBC) analysis, reflecting broader industry demand for faster and more accurate hematology testing. Growth is further supported by the UK's well-established companion animal healthcare sector, expanding veterinary laboratory capabilities, and increasing investment in digital and AI-enabled diagnostic platforms that enhance patient care and operational efficiency across veterinary clinics and hospitals.

Key Veterinary Hematology Analyzers Market Players:

- IDEXX Laboratories (U.S.)

- Zoetis (U.S.)

- Heska (U.S.)

- Antech Diagnostics (U.S.)

- Drew Scientific (U.S.)

- Siemens Healthineers (Germany)

- Nihon Kohden (Japan)

- Sysmex (Japan)

- Hitachi High-Tech (Japan)

- Fujifilm (Japan)

- Scil Animal Care (Germany)

- Woodley Equipment Company (UK)

- Boule Medical (Sweden)

- Horiba (France)

- EKF Diagnostics (UK)

- bioMérieux (France)

- BPC BioSed (Italy)

- Samsung Medison (South Korea)

- Transasia Bio-Medicals (India)

- Skanex (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- IDEXX Laboratories holds a dominant position in the veterinary hematology analyzers market, leveraging its robust installed base of ProCyte DX analyzers that deliver advanced hematology parameters. The company has strategically integrated its analyzers with cloud-based practice management software, enabling seamless data sharing and remote diagnostics for veterinary clinics. In 2024, the company has made a revenue of USD 3,897,504.

- Zoetis has significantly expanded its footprint in the market following its acquisition of Abaxis, which brought the well-known Vetscan and i-STAT product lines. The company focuses on point-of-care solutions that combine hematology, clinical chemistry, and electrolyte analysis in compact, easy-to-use devices. In 2024, the company has witnessed a 11% of revenue growth.

- Heska Corporation has strengthened its presence in the market through its Element i+ and ProCyte (partnered) analyzers, focusing on high-performance, compact systems for in-clinic use. The company’s strategic initiatives include developing cloud-based laboratory information systems and AI-driven decision support tools to enhance diagnostic accuracy.

- Antech Diagnostics, a subsidiary of Mars Incorporated, is a major force in the veterinary hematology analyzers market, offering a comprehensive portfolio of in-house analyzers such as the Catalyst and ProCyte series. The company has strategically integrated its diagnostic instruments with Sound technologies and telemedicine platforms to provide holistic diagnostic solutions.

- Drew Scientific has carved a niche in the veterinary hematology analyzers market with its specialized line of HemaTRUE and EXPRESS series analyzers, which are particularly valued for research institutions and exotic animal practices. The company’s strategic initiatives include developing multi-species databases and customizing analysis algorithms for non-traditional pets like birds, reptiles, and laboratory animals.

Here is a list of key players operating in the global veterinary hematology analyzers market:

The veterinary hematology analyzers market is moderately consolidated, with leading players focusing on precision, automation, and point-of-care solutions. Key strategic initiatives include launching portable analyzers, integrating AI-driven software for rapid cell differentiation, and expanding distribution networks in emerging economies. Companies are also forming partnerships with veterinary clinics and research institutes to enhance product credibility. For instance, IDEXX and Heska (now part of Mars) emphasize cloud-based data management, while Abaxis (now Zoetis) focuses on compact, easy-to-use devices. Mergers and acquisitions are common, allowing players to broaden their portfolios and geographic reach, intensifying competition.

Corporate Landscape of the Market:

Recent Developments

- In May 2026, HORIBA announced the launch of Yumivet, its new veterinary diagnostics brand, alongside the introduction of a dedicated solution, the Yumivet VH2500 hematology analyzer. Yumivet is designed to support the evolving needs of veterinary professionals, combining fast, reliable diagnostics with intuitive workflows to enhance clinical decision-making across many animal species.

- In April 2026, Zoetis Inc., announced it is expanding the capabilities of Vetscan OptiCell, its cartridge-based, artificial intelligence-powered hematology analyzer, marking the next step in the platform’s evolution.

- In January 2026, Norma Instruments is proud to announce the launch of the iVet-5R veterinary hematology analyzer, the latest innovation in our veterinary hematology portfolio. Designed for in-clinic complete blood count (CBC) testing, the iVet-5R brings lab-level precision directly to veterinary practices.

- Report ID: 8156

- Published Date: Jun 08, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.