Ultra-Fast EV Charging System Market Outlook:

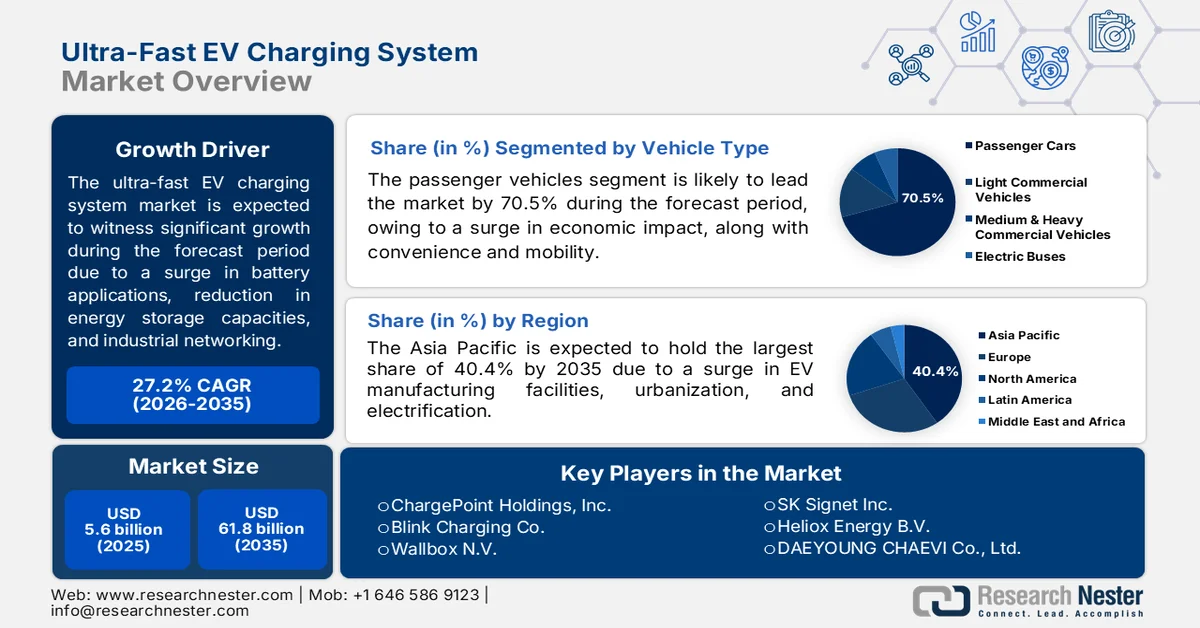

Ultra-Fast EV Charging System Market size was over USD 5.6 billion in 2025 and is expected to reach USD 61.8 billion by the end of 2035, growing at a 27.2% CAGR during the forecast period i.e., 2026-2035. In 2026, the industry size of ultra-fast EV charging system is assessed at USD 7.1 billion.

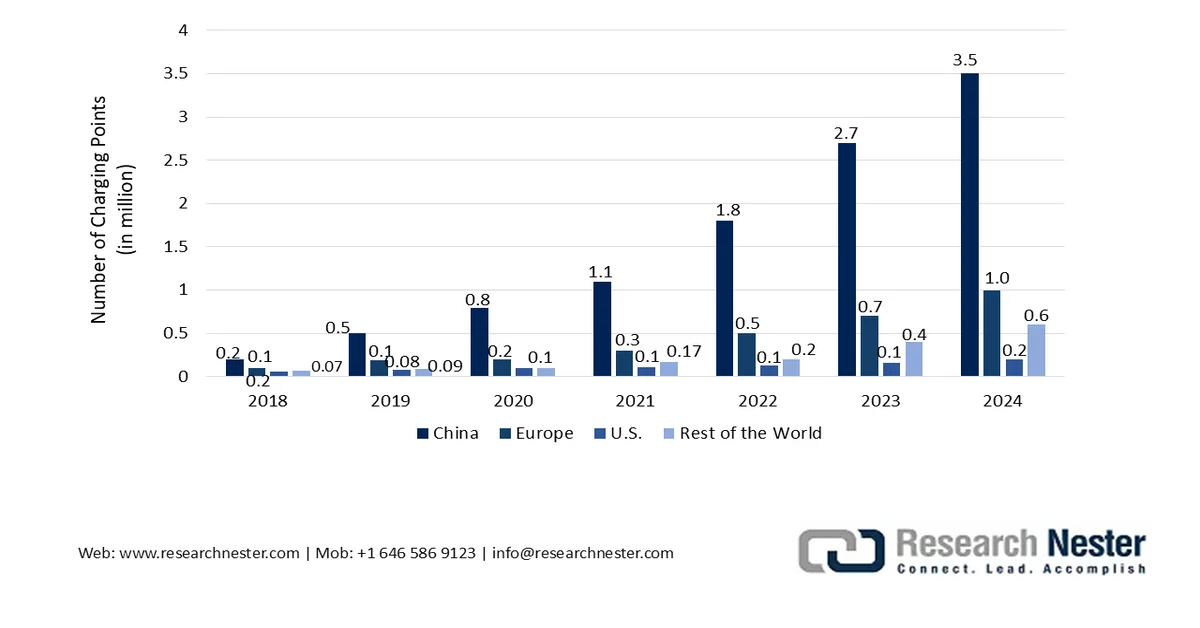

The global ultra-fast EV charging system market is being reshaped, owing to the eventual convergence of refueling and retail, the presence of liability and insurance frameworks, an increase in charging installations, suitable battery applications, a reduction in energy storage expenses, and industrial ethernet networking. According to official statistics published by the IEA Organization in 2025, public chargers readily doubled since 2022 and reached over 5 million. In addition, more than 1.3 million public charging points have been added to the worldwide stock as of 2024, demonstrating a surge by 30% in comparison to 2023. Besides, almost 2/3rd of public charging installations took place in China, presently accounting for nearly 65% of the charging, along with 60% of the electric light-duty vehicle stock. Likewise, there was an increase in charging points in Europe by 35% in 2024, which reached more than 1 million, thus driving the ultra-fast EV charging system market growth.

Region-Wise Public Charging Stock, 2018-2024

Source: IEA Organization

Furthermore, the presence of pop-up and mobile ultra-fast charging stations, gamification and charger-as-identity of charging sessions, as well as the existence of bidirectional ultra-fast charging are a few trends that are responsible for fueling the ultra-fast EV charging system market globally. As stated in an article published by the IEA Organization in 2026, more than 2,500 GW of renewable, along with storage and large-load projects, are presently stalled in grid queues globally. Therefore, meeting the suitable electricity demand by the end of 2030 is poised to require yearly grid investment to increase by an estimated 50% from the current USD 400 billion. This further caters to upscale grid supply chains and ensures suitable management of workforce risks, which further escalates the seasonal requirement of chargers across different construction locations and other events.

Key Ultra-Fast EV Charging System Market Insights Summary:

Regional Highlights:

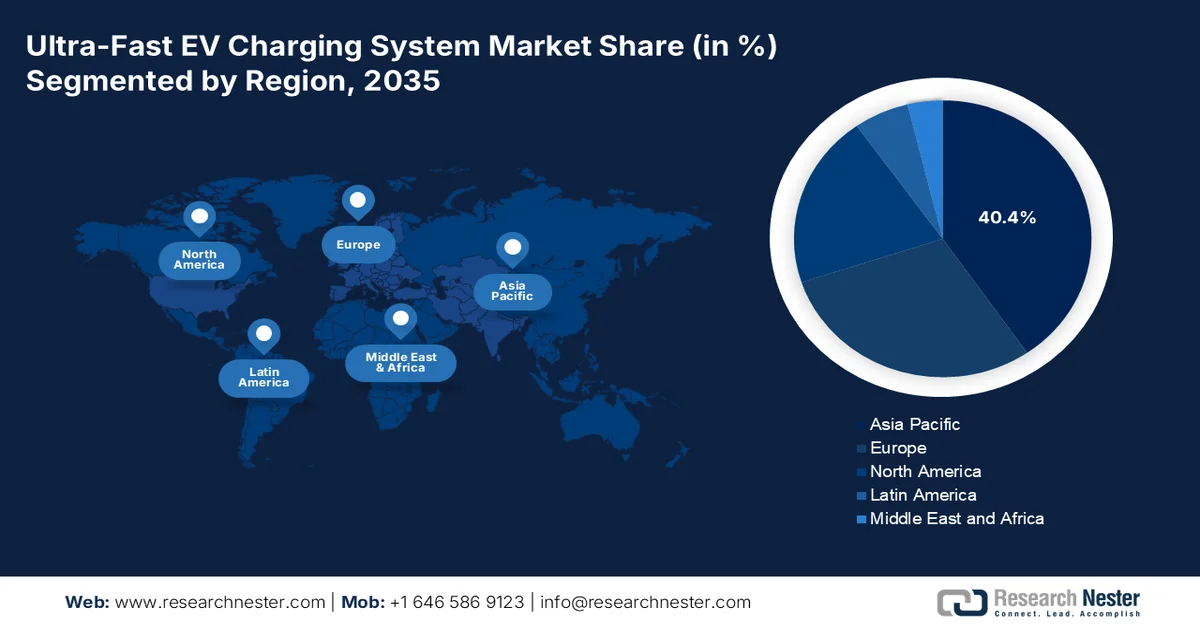

- Asia Pacific ultra-fast EV charging system market is projected to command a 40.4% revenue share by 2035, fueled by quantitative public charging deployment targets, expanding EV manufacturing capacity, rapid urbanization, and supportive electrification policies across major Asian economies

- North America is poised to witness the fastest growth in the market throughout 2026–2035, stimulated by strong federal investments, state-level EV mandates, growing adoption of NACS connector standards, and vertically integrated automakers

Segment Insights:

- The passenger vehicles sub-segment is anticipated to capture 70.5% of the ultra-fast EV charging system market by 2035, propelled by rising passenger car production, enhanced mobility convenience, and the expanding presence of global automotive manufacturers

- The standalone chargers segment is forecast to secure the second-largest share in the market by 2035, supported by the increasing requirement for efficient multi-device charging infrastructure and the rapid expansion of public charging installations worldwide

Key Growth Trends:

- Increase in fleet electrification

- Differentiated electricity tariffs

Major Challenges:

- Grid infrastructure and peak load strain

- Interoperability and connector standard wars

Key Players: ABB E-mobility (Switzerland), Siemens AG (Germany), Tesla Inc. (U.S.), Tritium DCFC Limited (Australia), Alpitronic S.p.A. (Italy), Delta Electronics, Inc. (Taiwan), Schneider Electric SE (France), EVBox (Netherlands), ChargePoint Holdings, Inc. (U.S.), Blink Charging Co. (U.S.), Wallbox N.V. (Spain), BTC Power (U.S.), SK Signet Inc. (South Korea), Heliox Energy B.V. (Netherlands), DAEYOUNG CHAEVI Co., Ltd. (South Korea), EVSIS Co., Ltd. (South Korea), Infy Power Co., Ltd. (China), ADY Power (China), eTreego (Taiwan), Huawei Digital Power (China), bp pulse (UK), Electreon (Israel), BYD (China), ChargePoints (U.S.), General Motors (U.S.).

Global Ultra-Fast EV Charging System Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.6 billion

- 2026 Market Size: USD 7.1 billion

- Projected Market Size: USD 61.8 billion by 2035

- Growth Forecasts: 27.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (40.4% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Japan, South Korea, Germany

- Emerging Countries: India, Canada, United Kingdom, France, Australia

Last updated on : 15 May, 2026

Ultra-Fast EV Charging System Market - Growth Drivers and Challenges

Growth Drivers

- Mandated minimum charger uptime and reliability regulations: Regulators and governments are readily imposing enforceable uptime requirements for mandating the operation of public ultra-fast chargers through operational licenses and public funding. Therefore, based on this and government estimates published by the Department of Energy in May 2026, the U.S. is expected to achieve 28 million EV charging ports by the end of 2030 for significantly supporting 33 million electric vehicles. In addition, of these total charging ports, 92.5% or 25.7 million are predicted to be private level 1 and level 2 chargers across single-family residential. Moreover, approximately 7.6% of 2.1 million private and public level 2 chargers are poised to be available at multifamily homes, restaurants, stores, hotels, and workplaces, thus enhancing the ultra-fast EV charging system market’s exposure.

2030 National EV Charging Network Size Analysis in the U.S.

|

Level Type |

EV Charging Ports |

Locations |

|

Private Level 1 and Level 2 |

25,700,000 |

Access at single-family home |

|

Private Level 2 |

570,000 |

Access at multifamily home |

|

Private Level 2 |

490,000 |

Access at workplace |

|

Public Level 2 |

1,070,000 |

Access at multiple locations |

|

Public DC Fast |

182,000 |

Access at different locations |

Source: Department of Energy

- Increase in fleet electrification: Regional and city authorities are increasingly incorporating low-emission zones, permitting electric delivery taxis, ride-hailing vehicles, and vans during business hours, which is propelling the ultra-fast EV charging system market globally. In this regard, as stated by Transportation Research Interdisciplinary Perspectives in July 2025, Ireland comprises a population of more than 5 million citizens, with 3 million registered vehicles as of 2024, of which an estimated 2.3 million are passenger vehicles. Besides, the fleet electrification in the country is projected to be worth USD 7.5 billion as net consumer benefit, along with USD 8.9 billion as net exchequer expense by the end of 2030. Moreover, the revised EV grants tend to save almost USD 2.3 billion as well as USD 646.1 million for the newest tax systems within the same period, thus boosting the ultra-fast EV charging system market growth.

- Differentiated electricity tariffs: Utility regulators are unveiling specialized electricity rate classes for the ultra-fast EV charging system market, with the intention of separating energy charges from demand charges and permitting the injection of on-site storage during the peak requirement. As per an article published by the IEA Organization in 2025, Europe, India, the U.S., and the UK posted nearly 20% lower wholesale electricity prices on average as of 2024, in comparison to 2023. However, few regions presently permit ultra-fast facilities to be effectively treated as micro-grids with their respective substation meters. Additionally, this bypasses commercial electricity rates, which are designed for factories and office buildings.

Challenges

- Grid infrastructure and peak load strain: The ultra-fast EV charging system market usually exerts immense instantaneous demand on local and regional power grids. Unlike standard AC chargers, a single ultra-fast charger can draw power equivalent to dozens of households simultaneously. When deployed in clusters at highway corridors or urban hubs, these chargers create sharp demand spikes that aging grid infrastructure is ill-equipped to handle. Besides, utilities face the dual burden of reinforcing substations, upgrading transformers, and replacing feeders without disrupting existing consumers. Furthermore, the unpredictable nature of fast-charging events, such as arriving at random intervals and durations, makes load forecasting exceptionally difficult.

- Interoperability and connector standard wars: Unlike the universal fuel nozzle at gasoline stations, ultra-fast EV charging suffers from fragmented connector ecosystems. CCS1 dominates North America for non-Tesla vehicles, while NACS is rapidly displacing it after automaker adoptions. Besides, Europe and South Korea utilize CCS2, while Japan retains CHAdeMO, and China mandates GB/T. This patchwork forces charging networks to install multiple cable types on each pedestal, increasing hardware cost, complexity, and unutilized space. Additionally, even within a single connector standard, communication protocols vary. Besides, Open Charge Point Protocol (OCPP) implementations differ by vendor, leading to authentication failures, session termination, and billing errors when a driver uses a third-party app, thus limiting the ultra-fast EV charging system market growth.

Ultra-Fast EV Charging System Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

27.2% |

|

Base Year Market Size (2025) |

USD 5.6 billion |

|

Forecast Year Market Size (2035) |

USD 61.8 billion |

|

Regional Scope |

|

Ultra-Fast EV Charging System Market Segmentation:

Vehicle Type Segment Analysis

During the forecast period, the passenger vehicles sub-segment, part of the vehicle type segment, is projected to grab the highest share of 70.5% in the ultra-fast charging system market. The sub-segment’s growth is effectively driven by providing unparalleled economic impact, convenience, and mobility. For instance, as stated in an article published by the IBEF Organization in September 2025, the automotive industry in India readily contributes to an estimated 7.1% of the gross domestic product (GDP) and significantly employs approximately 37 million people, both directly and indirectly. Based on this development, the passenger vehicle category has witnessed immense growth over the past 2 decades, with the availability of sedans, hatchbacks, MPVs, and SUVs. Moreover, at present, the country is home to roughly 15 global automotive manufacturers. Successfully set up production facilities, which are increasing the availability of passenger cars.

Automobile Production in India, 2020-2025

Source: IBEF Organization

Installation Type Segment Analysis

Based on the installation type, the standalone chargers segment is anticipated to garner the second-highest share in the ultra-fast EV charging system market by the end of 2035. The segment’s upliftment is primarily attributed to the necessity for efficient, safe, and rapid charging across numerous devices simultaneously. According to official statistics published by the IEA Organization in 2023, there were 2.7 million public charging points globally by the end of 2022. This is more than 900,000 installations at the beginning of 2022, demonstrating a 55% increase in stock. Besides, over 600,000 public slow charging points were also installed in the same year, of which 360,000 were located in China, totaling the slow chargers stock in the country to over 1 million. Simultaneously, Europe comprised 460,000 slow chargers within the same duration, indicating a 50% increase from 2021, thereby bolstering the segment’s growth.

End user Segment Analysis

The automotive OEMs sub-segment, which is part of the end user segment, is expected to account for the third-highest share in the ultra-fast EV charging system market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by its transformation from passive vehicle manufacturers to active infrastructure stakeholders. Unlike independent charging networks that prioritize commercial returns, OEMs deploy ultra-fast charging systems primarily to enhance vehicle value proposition, reduce range anxiety, and secure brand loyalty. Besides, a domestic automaker launching a flagship electric model cannot rely solely on third-party chargers, while customers expect a seamless, brand-integrated fast-charging experience akin to a captive refueling network. Moreover, the 2025 International Council on Clean Transportation demonstrated a list of OEMs, regarding their class coverage for zero-emission vehicles (ZEVs) across different regions, which is proliferating its expansion and exposure globally.

ZEV Model Class Coverage for Different Manufacturers, 2023-2024

|

Components |

SAIC |

Geely |

Chery |

Chang’am |

BYD |

|

Region-wise Class Coverage |

|

|

|

|

|

|

China |

88.0% |

88.0% |

75.0% |

62.0% |

62.0% |

|

U.S. |

- |

25.0% |

- |

- |

- |

|

Europe |

50.0% |

38.0% |

12.0% |

- |

38.0% |

|

India |

25.0% |

- |

- |

- |

12.0% |

|

Japan |

- |

- |

- |

- |

12.0% |

|

2024 Sales-Weighted Average |

81.0% |

76.0% |

74.0% |

62.0% |

62.0% |

|

2024 Analysis |

100 |

94 |

92 |

77 |

76 |

|

2023 Analysis |

100 |

78 |

78 |

93 |

77 |

Source: International Council on Clean Transportation

Our in-depth analysis of the ultra-fast EV charging system market includes the following segments:

|

Segment |

Subsegments |

|

Vehicle Type |

|

|

Installation Type |

|

|

End user |

|

|

Component |

|

|

Power Output |

|

|

Connector Standard |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Ultra-Fast EV Charging System Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the ultra-fast EV charging system market is anticipated to account for the largest share of 40.4% by the end of 2035. The market’s upliftment in the region is primarily driven by quantitative targets for public charging station deployment, the presence of the largest EV manufacturing base, rapid urbanization, strong electrification policies across India, South Korea, Japan, and China, and battery swapping technology for electric trucks. According to official statistics published by the ESCAP Organization in December 2024, the EV adoption and manufacturing target in Indonesia is projected to account for a 15 million EV fleet, including 13 million 2W and 2 million 4W battery electric vehicles by the end of 2030. Likewise, 100% electric motorcycles are to be adopted by 2040, while the nation is also focused on the 4-wheelers' ICE phase-out target by 2050, thus positively contributing towards the ultra-fast EV charging system market upliftment.

Battery Electric Vehicle Adoption Analysis in Asia Pacific, 2023

|

Countries |

Adoption % |

|

Philippines |

0.1% |

|

Malaysia |

1.9% |

|

Indonesia |

2.4% |

|

Vietnam |

4.0% |

|

Thailand |

10.8% |

Source: ESCAP Organization

The ultra-fast EV charging system market in China is growing significantly, owing to the correlation between EV population and charging infrastructure demand, provincial government strategies for developing high-quality charging infrastructure systems, vertical integration benefits, contributions by domestic manufacturers, and an escalation in deployment timelines. As stated in an article published by the State Council Information Office in February 2026, there has been an expansion in the charging network for electric vehicles, totaling 20.7 million in January. This readily marked a sharp surge of 49.6%, which is suitable for the market expansion in the country. Moreover, almost 4.8 million of these networks were public charging infrastructures, while 15.9 million were private facilities, demonstrating an increase by 31.2% and 56.1% year-on-year (YoY), respectively, thereby positively impacting the ultra-fast EV charging system market growth.

The aspects of targeting electrified new vehicle sales, achieving a doubled charger installation target, transition in pay-per-use fee system, grid congestion mitigation, and standard competition among organizations for enabling technological leapfrogging are certain factors that are fueling the ultra-fast EV charging system market in Japan. Besides, the industry's growth in the country was worth USD 252.9 million as of 2025, which is projected to be worth USD 319.2 million by 2026, and finally reach USD 2,052.7 million by the end of 2035. Moreover, as per the 2025 IEA Organization article, the country has readily targeted a stock of 300,000 public charging points, which is to be achieved by the end of 2030, marking almost 9 times the overall stock as of 2024. Therefore, based on the continuous industry growth and the objective of installing generous charging points, the ultra-fast EV charging system market is steadily expanding in the overall country.

North America Market Insights

North America in the ultra-fast EV charging system market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by strong federal funding, state-level electrification mandates, an increase in the transition to NACS as a suitable connector standard, the presence of vertically integrated automakers, and repurposing EV batteries. According to official statistics published by the IEA Organization in 2026, the largest sources of electricity generation in the region are 40% of natural gas and 17% of nuclear, both accounting for the overall generation. Meanwhile, the total electricity production in the region caters to 5,465,900 GW, along with more than 12% of the trend, and 18% of the global share as of 2023, thereby denoting a huge growth opportunity for the ultra-fast EV charging system market.

Electricity Generation Sources in North America, 2023

|

Source Type |

Generation (GWh) |

|

Coal |

798,486.0 |

|

Oil |

65,609.0 |

|

Natural Gas |

2,193,111.0 |

|

Nuclear |

909,508.0 |

|

Hydropower |

650,495.0 |

|

Biofuels |

57,290.0 |

|

Waste |

16,194.0 |

|

Wind |

487,354.0 |

|

Solar PV |

245,067 |

|

Geothermal |

23,820.0 |

|

Other Sources |

15,866.0 |

Source: IEA Organization

The ultra-fast EV charging system market in the U.S. is gaining increased traction, owing to the presence of the NEVI formula program corridor completion mandates, the adoption of the federal highway administration minimum standards rule, and the electrification of non-tactical vehicle fleets. As stated in an article published by Atmospheric Pollution Research in May 2026, 36% of light-duty vehicle fleet transitions in New York comprised Tier 3 vehicles, and an estimated 6% were plug-in electric or hybrid vehicles by the end of 2025. Meanwhile, there has been a rapid increase in the gasoline direct injection (GDI) adoption from 5% to 36% within the same timeline. Therefore, this fleet turnover highlighted a suitable lag between fleet composition modifications and regulatory implementation, which is boosting the market development in the country.

The existence of a zero-emission vehicle infrastructure program, the cold climate performance mandate by Natural Resources Canada, and the provincial zero-emission vehicle mandate alignment are a few trends that are propelling the ultra-fast EV charging system market in Canada. As per an article published by the Government of Canada in February 2026, both provincial and federal purchase incentives, amounting to almost USD 12,000, are significantly combined with the diminished expenses of vehicle maintenance and charging. Besides, based on a study by Clean Energy Canada, the overall cost of ownership of a small electric hatchback vehicle was worth USD 39,000, along with a comparable gasoline model worth USD 30,000. Simultaneously, the ownership expense for the gasoline vehicle was roughly more than USD 80,000, which is less than USD 49,000 for electric vehicles, thus denoting an optimistic outlook for the market development.

Europe Market Insights

Europe in the ultra-fast EV charging system market is projected to witness suitable growth and expansion by the end of the stipulated timeline. The market’s growth in the region is effectively attributed to binding regulatory policies, cross-border corridor demands, robust private and public funding mechanisms, greenhouse gas emission reduction, and an escalation in internal combustion engine vehicles. According to official statistics published by NLM in December 2022, the region has effectively set a 37.5% greenhouse gas reduction rate, which is poised to be achieved by the end of 2030 for the mobility industry. Besides, the objectives of the regional Member States for EV promotion, the EV stock is predicted to be almost 73 times more than in previous years by the end of 2040, readily contributing to cumulative in-use emission reduction of 2 gigatons of carbon dioxide equivalent, thus proliferating the ultra-fast EV charging system market growth.

The ultra-fast EV charging system market in Germany is gaining increased exposure, owing to the largest vehicle industry, the presence of ambitious electric vehicle adoption targets, and the correlation of charging infrastructure demand, along with expansion in engineering and manufacturing industries. As stated in an article published by the Europe Commission in November 2025, the country has already surpassed AFRI public charging point requirements by almost 200%. This particular approach foresees tax incentives for supporting EV uptake and strengthened support for multi-apartment charging. Additionally, the expanded funding for depot charging for high-density vehicles and buses, along with the development of a domestic e-truck high-power motorway network are also part of the plan, thereby making it suitable for bolstering the market exposure.

The ultra-fast charger density per capita, secured and substantial recovery funds, the electrification of tourist-heavy coastal highways, energy abundance, and the increased demand for advanced cooling fluids and thermal interface materials are certain trends that are driving the ultra-fast EV charging system market in Spain. Based on government estimates published by the ITA in July 2024, the country’s overall installed energy capacity surged by 4.9% as of 2022 and successfully reached 119 GW. This particular increase was highly fueled by renewable energy, which experienced a 9.1% increase in installed capacity across Portugal. Moreover, within the domestic renewable capacity, photovoltaic energy witnessed the greatest surge in the same year, growing more than 22% or 4.4 GW. This has readily made PV the third leading generation capacity after combined and wind cycle, thus enhancing the market demand in the country.

Key Ultra-Fast EV Charging System Market Players:

- ABB E-mobility (Switzerland)

- Siemens AG (Germany)

- Tesla Inc. (U.S.)

- Tritium DCFC Limited (Australia)

- Alpitronic S.p.A. (Italy)

- Delta Electronics, Inc. (Taiwan)

- Schneider Electric SE (France)

- EVBox (Netherlands)

- ChargePoint Holdings, Inc. (U.S.)

- Blink Charging Co. (U.S.)

- Wallbox N.V. (Spain)

- BTC Power (U.S.)

- SK Signet Inc. (South Korea)

- Heliox Energy B.V. (Netherlands)

- DAEYOUNG CHAEVI Co., Ltd. (South Korea)

- EVSIS Co., Ltd. (South Korea)

- Infy Power Co., Ltd. (China)

- ADY Power (China)

- eTreego (Taiwan)

- Huawei Digital Power (China)

- bp pulse (UK)

- Electreon (Israel)

- BYD (China)

- ChargePoints (U.S.)

- General Motors (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- ABB E-mobility is a dominant force in the ultra-fast EV charging space, leveraging its deep heritage in industrial power electronics and grid infrastructure to deliver highly reliable, liquid-cooled direct current fast chargers. The company focuses heavily on interoperability and fleet electrification, ensuring its charging platforms seamlessly integrate with multiple vehicle architectures and utility back-end systems.

- Siemens AG applies its century-old expertise in substation automation, medium-voltage switchgear, and energy management to deploy ultra-fast charging solutions that are deeply integrated with smart grid capabilities. The German giant prioritizes holistic e-mobility ecosystems, pairing its chargers with on-site battery storage, load balancing software, and renewable energy umbilicals to reduce grid upgrade costs.

- Tesla Inc. tightly couples its ultra-fast Supercharger hardware with its proprietary vehicle battery management software, enabling charging curves that optimize both speed and cell longevity across its fleet. While historically a closed network, Tesla has begun opening its connector standard and select stations to non-Tesla EVs, fundamentally reshaping competitive dynamics in North America.

- Tritium DCFC Limited pioneered compact, fanless liquid-cooled ultra-fast chargers built for harsh outdoor environments, focusing on ease of installation and minimal maintenance requirements. The Australian manufacturer utilizes a modular power cartridge architecture, which allows operators to scale charging capacity incrementally and replace individual power modules without taking entire pedestals offline.

- Alpitronic S.p.A. has gained significant traction in Europe with its Hypercharger product line, known for exceptionally high efficiency ratings and redundant power supply designs. The Italian company emphasizes modular silicon carbide power stages and remote over-the-air firmware updates, ensuring that deployed ultra-fast chargers remain adaptable to evolving vehicle battery technologies.

Here is a list of key players operating in the global ultra-fast EV charging system market:

The ultra-fast EV charging system market is characterized by intense competition between established power electronics leaders and specialized charging infrastructure providers. Key players are pursuing distinct strategic initiatives to secure market position. Major Europe-based and U.S. manufacturers differentiate through high-power platform reliability, grid integration expertise, and strategic utility partnerships. Besides, in October 2025, bp pulse declared the opening of its newest electric vehicle charging facility in Houston, which demonstrated the organization’s continuous efforts to offer reliable and convenient EV charging options across the U.S. In addition, this facility features 40 ultra-fast EV charging bays that are equipped with 150 kW direct current (DC) fast chargers, thereby denoting an optimistic outlook for the ultra-fast EV charging system industry ultra-fast EV charging system market growth.

Corporate Landscape of the Ultra-Fast EV Charging System Market:

Recent Developments

- In November 2025, Electreon signed a memorandum of understanding (MoU) and acquired Induct EV’s assets and deliberately set the stage for a worldwide powerhouse in wireless EV charging as well as stationary high-power technology.

- In March 2025, BYD unveiled the Super e-Platform that features flash-charging batteries, new silicon carbide power chips, and a 30,000 RPM motor for upgrading the core electric components and achieving a charging power of 1 megawatt, along with a 2-peak charging speed of 2 kilometers per second.

- In December 2024, ChargePoint and General Motors accelerated EV infrastructure growth, especially in the U.S., by joining efforts for installing different ultra-fast charging ports at suitable locations across the country and ensuring the newest advancements in EV charging for optimizing access to chargers.

- Report ID: 8570

- Published Date: May 15, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.