Driver Drowsiness Detection System Market Outlook:

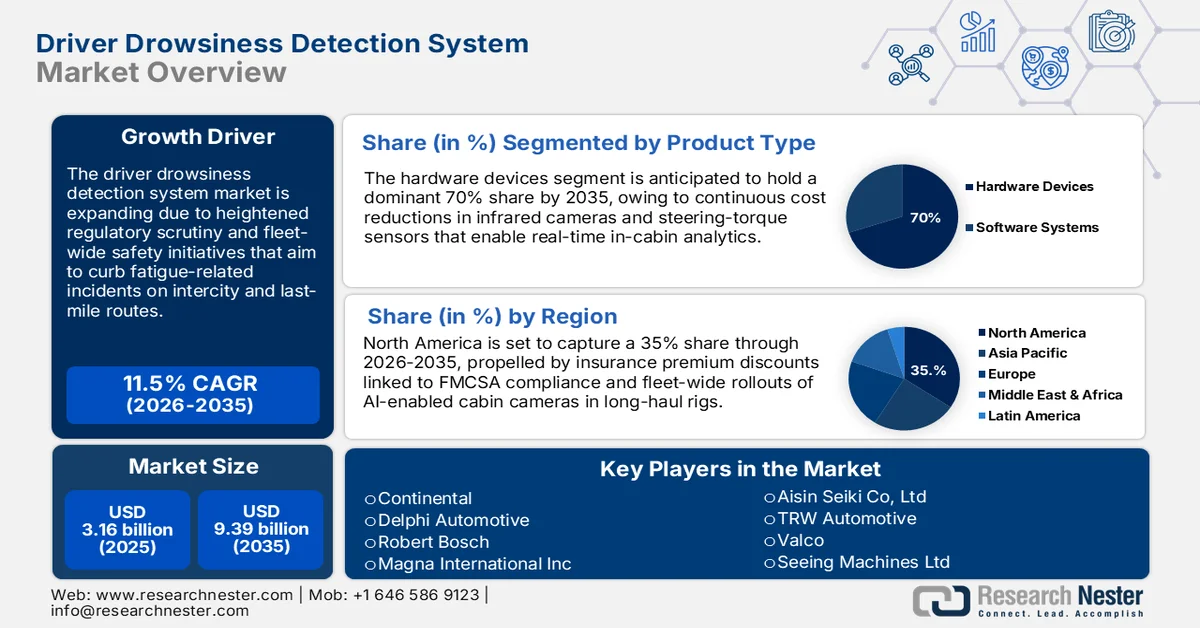

Driver Drowsiness Detection System Market size was over USD 3.16 billion in 2025 and is poised to exceed USD 9.39 billion by 2035, growing at over 11.5% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of driver drowsiness detection system is estimated at USD 3.49 billion.

The driver drowsiness detection system market is seeing strong momentum as safety-focused regulations and fleet safety efforts take root. In October 2024, Netradyne introduced its next-generation DMS sensor, featuring a 98% accuracy rate for detecting fatigue. The system is raising the bar for proactive driver alerting, strengthening accident prevention protocols. Such systems are being integrated by a growing cohort of OEMs to address changing safety mandates. Consumer education on fatigued-driving-related accidents is also on the rise, spurring adoption in passenger and commercial vehicles. Global regulatory trends, particularly in developing markets, are spurring the integration of real-time alert functionality. Industry players are now looking at biometric and AI-based sensor systems.

OEM alliances and government regulations continue to drive a positive market outlook. In April 2025, India's Ministry of Road Transport implemented mandatory drowsiness alert and emergency braking systems on all new cars by April 2026. This aggressive action reflects worldwide trends focusing on driver condition monitoring. Meanwhile, tech startup companies are providing low-cost solutions for fleet and ride-share companies. For example, Samsara AI-based drowsiness alert for fleets was launched globally in October 2024. The collaboration of embedded hardware and software platforms increases system responsiveness. As legal responsibility for fatigue crashes intensifies, DMS technologies become a regulatory and ethical imperative.

Key Driver Drowsiness Detection System Market Insights Summary:

Regional Highlights:

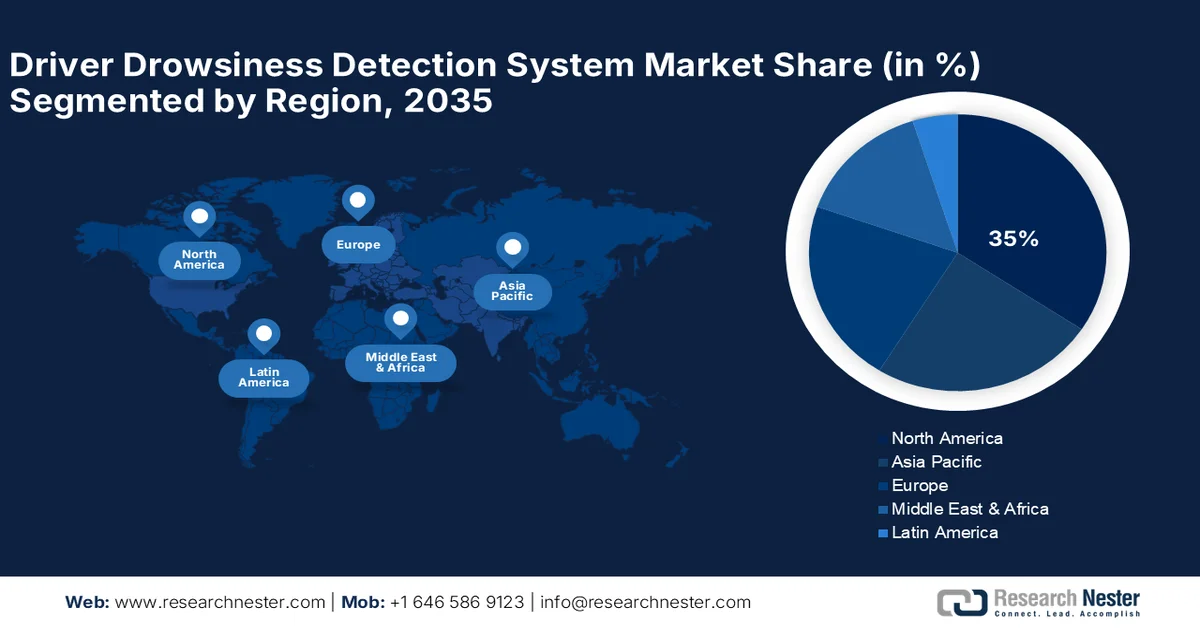

- North America in the driver drowsiness detection system market is anticipated to secure over 35% revenue share by 2035, impelled by favorable regulatory environments and heightened consumer awareness regarding safety

- Asia Pacific is projected to expand at a CAGR of over 11% through 2035, stimulated by vehicle electrification and strengthening safety standards

Segment Insights:

- In the driver drowsiness detection system market, the Hardware devices segment is projected to account for over 70% share by 2035, propelled by their strong integration capabilities and lower latencies

- By 2035, the Passenger car segment is forecast to capture more than 58% share, driven by growing consumer adoption of personal safety features

Key Growth Trends:

- Regulatory mandates to improve road safety

- Advances in artificial intelligence and biometric technologies

Major Challenges:

- False positives and driver mistrust in system accuracy

- Standardization gaps in international markets

Key Players: Stryker Corporation, Johnson & Johnson, OrthoNovis, Inc., Zimmer Biomet, Smith & Nephew, Bombay Ortho Industries, Nuvasive Inc., Aesculap Implant Systems LLC, Orthopaedic Implant Company, CONMED Corporation, DJO Global Inc., Lifesciences, Inc., Henry Schein, Inc., Trimed Inc., Extremity Medical LLC, Alkem Laboratories Limited, Auxein Medical Private Limited.

Global Driver Drowsiness Detection System Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.16 billion

- 2026 Market Size: USD 3.49 billion

- Projected Market Size: USD 9.39 billion by 2035

- Growth Forecasts: 11.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: China, India, Japan, South Korea, Germany

Last updated on : 25 February, 2026

Driver Drowsiness Detection System Market - Growth Drivers and Challenges

Growth Drivers

- Regulatory mandates to improve road safety: Regulations are propelling the mass adoption of driver monitoring systems globally. In October 2024, the India government made it mandatory for fatigue alert systems on all new buses and trucks. Parallel regulations in Europe and North America are compelling original equipment manufacturers (OEMs) to implement embedded digital management systems (DMS). Embedded systems are becoming standard safety features in new vehicles. Governments are making DMS adoption a priority to lower crash fatalities. Nations with expanding transport industries are focusing on commercial fleet compliance. Regulatory clarity is necessary for vehicle makers to standardize fatigue monitors across multiple platforms.

- Advances in artificial intelligence and biometric technologies: Technology advancement is also a growth driver in the driver drowsiness detection system market. Biometric technologies, including heart rate and eye tracking, enhance detection accuracy. Pattern recognition over various driving behaviors is now supported by AI-based analytics. IdriveAI added facial recognition to BlackBerry’s IVY platform in January 2024 to improve fatigue detection accuracy. Such developments provide an earlier warning, enabling more response time for drivers to act safely. OEMs are moving towards multifunctional platforms that integrate safety, comfort, and AI insights.

- Fleet operator demand for predictive safety tools: Commercial vehicle fleets are looking to invest in drowsiness detection systems to lower downtime and liability. In November 2024, Samsara initiated a global rollout of AI-powered fatigue tools that track driver alertness and respond in real time. These solutions lower collisions, claims, and repair bills. Fleets appreciate dashboards that identify at-risk behaviors before incidents occur. Predictive analysis enables fleet managers to tailor reminders and coaching. As driver conduct is directly linked to premiums, the ROI on driver drowsiness detection system investments is increasing. These systems also reinforce driver wellness programs within vehicle fleets.

Challenges

- False positives and driver mistrust in system accuracy: Even with technological advancements, false alarms continue to hamper driver drowsiness detection system adoption. In October 2024, Tesla's cabin-camera-based warning system also misinterpreted fatigue under low-light conditions. Such inaccuracies upset drivers and can cause them to disable the system. Sensor sensitivity fine-tuning and illumination adaptation are constantly evolving. Without accuracy, trust by users in DMS is lost, with its features diminished in use. Developers have to trade off sensitivity against specificity to prevent nuisance warnings. Open calibration and training environments have to be provided to improve system personalization and dependability.

- Standardization gaps in international markets: Market fragmentation results from incomplete harmonized standards for DMS across regions. In February 2024, Rheinmetall acquired orders for its distraction-detection system, but compliance needs were different in every country. Inconsistency overloads manufacturers with regional idiosyncrasies. Europe leads in pushing Level 2 requirements for automation features, while others trail behind with legal certainty. Small and medium-sized OEMs encounter cost barriers in terms of compliance with region-specific requirements. International organizations have not provided harmonized safety standards for fatigue systems. Cross-border vehicles and fleet companies need interoperability platform capabilities, making it an absolute market imperative.

Driver Drowsiness Detection System Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.5% |

|

Base Year Market Size (2025) |

USD 3.16 billion |

|

Forecast Year Market Size (2035) |

USD 9.39 billion |

|

Regional Scope |

|

Driver Drowsiness Detection System Market Segmentation:

Product Type Segment Analysis

Hardware devices segment is set to hold more than 70% driver drowsiness detection system market share by 2035, owing to their strong integration capabilities and lower latencies. Smart Eye's driver fatigue detection system for Solaris buses was certified in October 2024, ensuring real-time fatigue detection through camera-based sensors. Hardware-based DMS solutions have an upper hand in on-the-fly visual and biometric data reading. Embedded nature ensures uninterrupted monitoring even in poor network facilities. High-end infrared and thermal sensors are becoming popular for accuracy at night. Regulatory compliance is desired by OEMs in hardware configurations. Hardware is still essential for mass commercial roles that need rugged and closed modules.

Vehicle Type Segment Analysis

By 2035, passenger car segment is expected to capture over 58% driver drowsiness detection system market share, supported by consumer adoption of personal safety features. In December 2024, IdriveAI introduced the Pro7 dual-lens dashcam, featuring both road and driver-facing cameras. Equipped with AI capabilities, it provides real-time fatigue and distraction detection, enhancing driver coaching and safety measures. Consumers in mid as well as premium segments value smart safety features more than ever before, particularly in urban areas. Automakers use driver drowsiness detection systems for differentiation at mid and premium segment levels. Increased ownership in younger drivers also leads to greater adoption rates. Many major makers package ADAS systems as standard or mid-level trims. Passenger cars are entry points for advanced DMS technologies.

Our in-depth analysis of the global driver drowsiness detection system market includes the following segments:

|

Product Type |

|

|

Vehicle Type |

|

|

System Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Driver Drowsiness Detection System Market - Regional Analysis

North America Market Insights

North America in driver drowsiness detection system market is poised to capture over 35% revenue share by 2035, driven by favorable regulatory environments and increased consumer awareness regarding safety. In January 2024, Tesla introduced its cabin camera-based driver fatigue alert system in refreshed Model 3 units, mainstreaming driver monitoring across its entire vehicle lineup. Regulatory authorities such as NHTSA enable such deployments with AV safety tests. Insurance discounts drive penetration of AI-based DMS in the fleet as well. Increased litigation exposure from fatigue-related crashes is supporting both corporate and consumer demand. With vehicles becoming more autonomous, passive tools become critical. OEMs are now promoting fatigue warnings even in non-premium categories.

The key driver fatigue detection system technologies are based in the U.S., with companies such as Smart Eye and Magna looking to target North America OEMs. In January 2025, Rivian unveiled Level 3 ADAS plans featuring improved driver drowsiness warnings on its EVs. The U.S. market accepts these systems for personal and commercial use. Consumer rating organizations now factor in DMS as a fundamental scoring element. Wellness technologies for drivers are part of an in-cabin personalization trend. The U.S. regulatory environment fosters constant tech advancement. Transport fleets operating across multiple states drive an interest in standardized alert systems.

Canada's prioritization of safety has manifested in growing driver drowsiness detection system adoption in both city and long-distance segments. Canada vehicle sales expanded by 4.4% during Q1 2023, driven in part by requests for tech-enabled models. Cross-province route risk reduction is preferred by fatigue alert tools from fleet operators. Ontario is initiating education campaigns on driver fatigue. Canada research centers for ADAS collaborate with original equipment manufacturers on localizing alert levels. Severe winters amplify vigilance of tech needs. Onboard DMS may become an obligatory feature for heavy trucks and school bus transport systems with changing regulations.

Asia Pacific Market Insights

Asia Pacific driver drowsiness detection system market is expected to register growth of over 11% till 2035, attributed to vehicle electrification and increased standards of safety. In March 2024, the government of India announced DMS mandates for 2026, fast-tracking market readiness. Mid-spec EVs now include fatigue alert systems by local automakers. China, India, and Southeast Asia have high adoption rates in logistics. Regional startup hubs are developing low-cost, vision-based monitoring solutions. Governments also fund local DMS development with subsidies to lower import dependence. The high rate of urbanization in the region necessitates early intervention systems.

The emphasis on autonomous development in China is leading to early adoption of high-end DMS platforms. In November 2024, Tesla introduced refreshed fatigue monitoring for electric vehicles (EVs) manufactured in China. The country's roadmap for AVs through 2025 includes embedding behavior-based safety features. Domestic players such as NIO and Xpeng are at the forefront of in-cabin sensor innovation. Face detection and alertness scores are utilized to coach drivers in real-time. Regulatory push and infrastructure availability aid in local system development. e-Commerce and ride-hailing fleet players drive further adoption of DMS.

India is anticipated to witness stable growth in the drowsiness detection system market, driven by robust regulatory and commercial support. In April 2025, the Ministry of Road Transport announced that compulsory fatigue detection systems would be introduced on new vehicles starting in 2026. Mahindra and Tata Motors are gearing up for integration on all SUV lineups. Tier-2 and Tier-3 cities reflect high volume due to intercity driving stress. Domestic part manufacturers are creating compact sensor kits to reduce price points. Public transport and school buses rank as priority areas for pilots. India's safety-oriented policy environment accelerates OEM and supplier alignment.

Driver Drowsiness Detection System Market Players:

- Continental

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Delphi Automotive

- Robert Bosch

- Magna International Inc

- Aisin Seiki Co, ltd

- TRW Automotive

- Valco

- Seeing machines ltd

- Smart eye AB

- Hella Gmbh and Co

- Autoliv Inc

The driver drowsiness detection system market is characterized by competitive dynamics driven by sensor technology and OEM partnerships. Key companies are Continental, Delphi Automotive, Robert Bosch, Denso Corporation, Magna International Inc, Aisin Seiki Co., Ltd, TRW Automotive, Valeo, Seeing Machines Ltd, Smart Eye AB, Hella GmbH and Co, and Autoliv Inc. These companies specialize in scalable systems with infrared sensors, biometric algorithms, and dashboard integration capabilities. R&D intensity and regulatory attention maintain high barriers to entry. Future leadership is characterized by strategic partnerships and AI capabilities. Businesses compete on accuracy, robustness, and flexibility to train with AI.

Smart Eye unveiled its AIS+ system in January 2025 at CES, with options for video feedback as well as haptic notifications, transforming driver attention management. The platform provides real-time interventions as well as post-event analysis for fleet managers. These moves demonstrate the trend toward modular, smart, and privacy-friendly DMS offerings. Competitive attention is also shifting toward commercial vehicle-specific implementations. As cars become connected to ecosystems, suppliers are marketing end-to-end behavioral monitoring platforms. Innovation continues to provide ongoing differentiation in this changing safety segment.

Here are some leading players in the driver drowsiness detection system market:

Recent Developments

- In April 2025, NueGo equipped its entire electric bus fleet with advanced safety technology, including driver monitoring systems to detect drowsiness. This move enhances passenger safety by ensuring drivers remain alert during operations, potentially preventing accidents and saving lives.

- In February 2025, Netradyne's DMS sensor demonstrated significant improvements in drowsy driving detection, providing fleet operators with reliable tools to monitor driver alertness. The technology aims to reduce accidents caused by fatigue, leading to safer roads for everyone.

- Report ID: 7575

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.