Intelligent Transportation System Market Outlook:

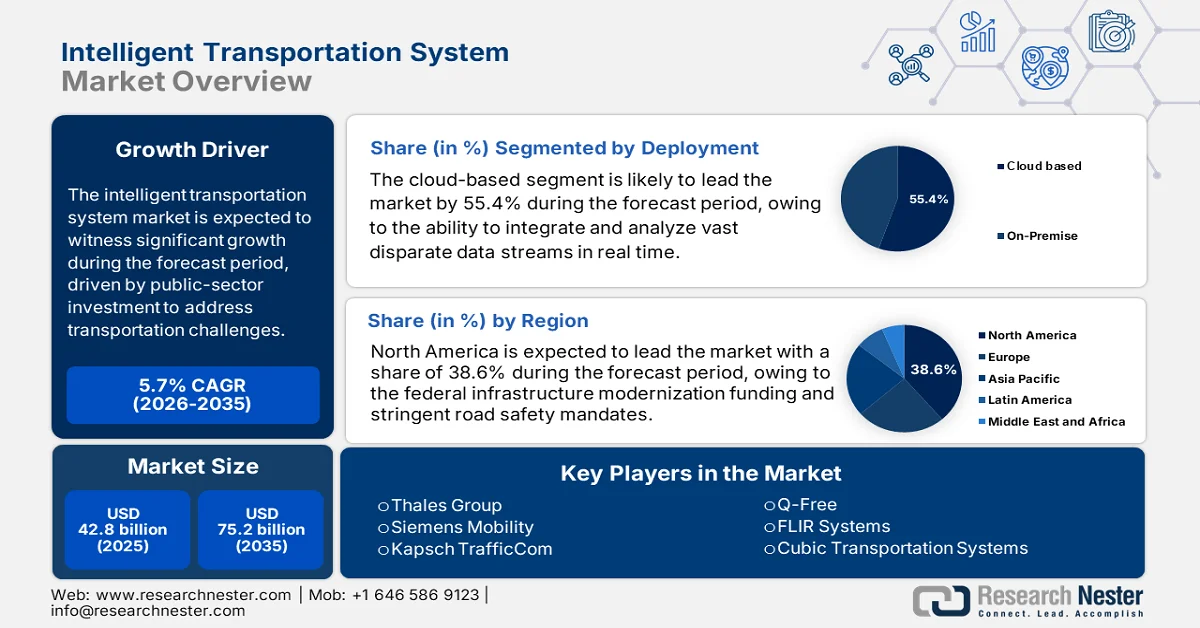

Intelligent Transportation System Market size was valued at USD 42.8 billion in 2025 and is projected to reach USD 75.2 billion by the end of 2035, rising at a CAGR of 5.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of intelligent transportation system is estimated at USD 45.2 billion.

The market is driven by public-sector investment aimed at addressing core operational challenges in transportation networks. According to the CNU Journal April 2022 data, the Federal Highway Administration reports that in the U.S., congestion and unreliable travel impose over USD 190 billion annually in economic costs, prompting federal and state agencies to prioritize traffic management corridor optimization and safety monitoring programs under the intelligent transportation system-related funding streams. Moreover, the Federal Highway Administration's February 2026 report shows that the U.S. Infrastructure Investment and Jobs Act allocates more than USD 350 billion for the highways and safety programs with dedicated funding mechanisms, such as the advanced transportation technology and innovation program supporting state and municipal ITS upgrades.

Besides, the World Health Organization data in December 2023 shows that nearly 1.19 million people die each year as a result of road traffic crashes. This data reinforces the sustained procurement of real-time monitoring, enforcement automation, and incident response systems by transport authorities. Moreover, the urbanization and freight movement pressures further sustain the institutional spending on the market. the Geography of Transportation 2024 report indicates that the transportation GDP ranges from 6% to 12%, and the inefficiencies can reduce this by certain percentage mainly in the emerging countries Further the government-backed safety, efficiency, and fiscal performance imperatives anchor long-term market demand, with procurement largely driven by public agencies, concession operators, and infrastructure authorities rather than discretionary commercial adoption.

Key Intelligent Transportation System Market Insights Summary:

Regional Highlights:

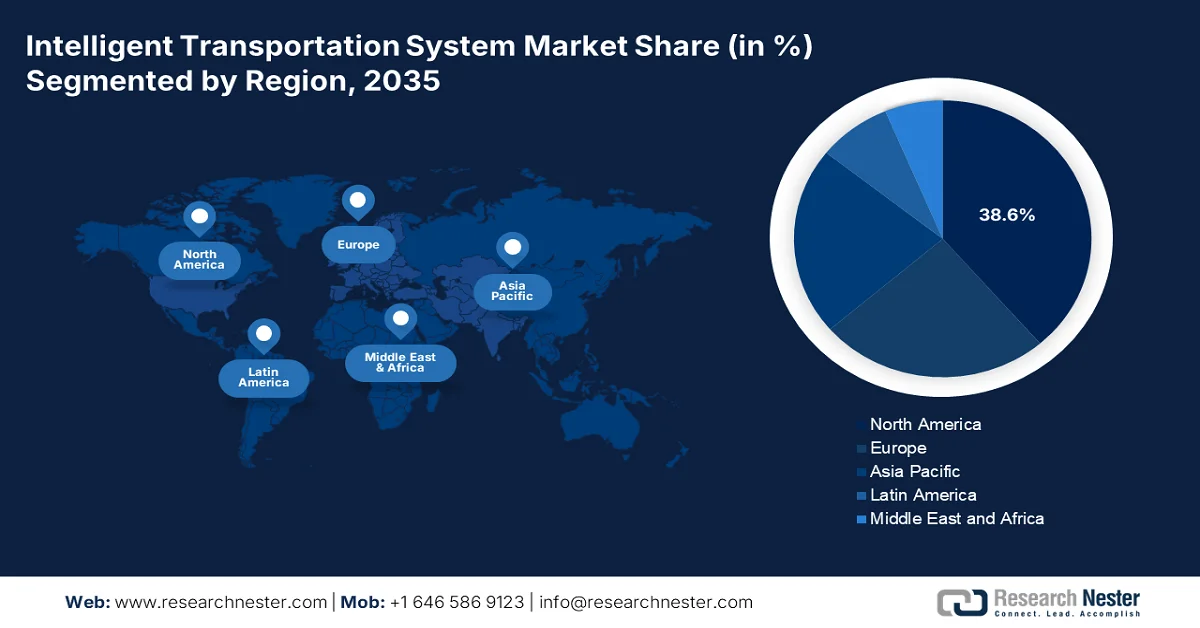

- North America intelligent transportation system market is projected to secure a 38.6% revenue share by 2035, impelled by federal infrastructure modernization funding and stringent roadway safety mandates

- Asia Pacific is anticipated to record the fastest CAGR of 9.5% during 2026–2035, stimulated by large-scale government-led urbanization and smart transportation investments

Segment Insights:

- Intelligent Transportation System Market’s cloud-based solutions segment is projected to account for 55.4% share by 2035, propelled by increasing government adoption of cloud-first strategies and rising public cloud spending

- The software segment is expected to retain the highest share by 2035, driven by the growing demand for AI-powered analytics and data-driven traffic intelligence solutions

Key Growth Trends:

- Escalating public expenditure on road safety and fatality reduction

- Federal infrastructure investment and policy mandates

Major Challenges:

- High initial capital and R&D investment

- Intensive system integration and interoperability demands

Key Players: Thales Group (France), Siemens Mobility (Germany), Kapsch TrafficCom (Austria), Q-Free (Norway), FLIR Systems (U.S.), Cubic Transportation Systems (U.S.), Iteris, Inc. (U.S.), Motorola Solutions (U.S.), IBM Corporation (U.S.), Cisco Systems, Inc. (U.S.), TomTom (Netherlands), Garmin Ltd. (U.S.), Hitachi Rail (Japan), Mitsubishi Electric Corporation (Japan), NEC Corporation (Japan), Samsung SDS (South Korea), Hyundai Mobis (South Korea), Kapsch TrafficCom India (India), Adatek (Australia), SMH Rail & Transit Sdn. Bhd. (Malaysia).

Global Intelligent Transportation System Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 42.8 billion

- 2026 Market Size: USD 45.2 billion

- Projected Market Size: USD 75.2 billion by 2035

- Growth Forecasts: 5.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, Brazil, South Korea, United Arab Emirates, Singapore

Last updated on : 17 February, 2026

Intelligent Transportation System Market - Growth Drivers and Challenges

Growth Drivers

- Escalating public expenditure on road safety and fatality reduction: Road safety has become a fiscal and policy priority, directly stimulating the market by transport authorities. Moreover, road traffic injuries cause a million deaths annually, imposing economic losses in many countries. Moreover, the governments are allocating sustained budgets for automated enforcement, traffic monitoring, and incident response systems. According to the U.S. Department of Transportation, in November 2024, nearly 42,514 roadway fatalities were recorded in 2022, prompting federal grants under the Safe Streets and Roads for All program, which committed USD 5 billion for safety-focused infrastructure, including the ITS-enabled traffic management. Further, the vendors aligned with safety compliance and reporting standards gain priority access to long-term public contracts.

Number of Roadway Fatalities

![]()

Source: U.S. Department of Transportation, November 2024

- Federal infrastructure investment and policy mandates: The direct government spending via legislation, such as the U.S. Bipartisan Infrastructure Law, is the most significant demand driver of the intelligent transportation system market. According to the U.S. Department of Transportation, in December 2025, nearly USD 54 million was granted for the 34 projects across 21 states in the third and final round of the SMART Stage 1 Grants. This creates a guaranteed multi-year funding stream for state and local agencies, directly translating into procurement for traffic management, connected vehicle infrastructure, and smart grid projects. The funding is tied to achieving safety, efficiency, and sustainability goals, mandating the adoption of ITS solutions and setting a global benchmark for public investment in modernized transportation networks.

- Road safety imperatives and fatality reduction goals: High roadway fatality rates are compelling governments to mandate technology-based solutions. The U.S. national roadway safety strategy explicitly promotes the market, such as automated speed enforcement, intersection safety cameras, and vehicle-to-everything communication. This shifts demand from discretionary upgrades to essential safety infrastructure. For instance, the Federal Highway Administration’s Safe Streets and Roads for All grant program allocated over USD 800 million in its first year for projects, as per the U.S. DOT February 2023 that include ITS deployments demonstrating how safety objectives are directly funding the market growth for specific sensor software and data analytics platforms.

Challenges

- High initial capital and R&D investment: Entering the intelligent transportation system market requires immense upfront investment in R&D for hardware resilience and software analytics, plus the cost of pilot deployments. The long sales cycles with the public agencies delay ROI. Startups rely heavily on venture capital to fund the development before securing city contracts. Though the market is expected to grow, this growth is capital-intensive, favoring established players with deeper pockets who can absorb these costs during the lengthy validation and procurement phases.

- Intensive system integration and interoperability demands: New systems must integrate with a city’s legacy infrastructure and disparate new technologies. A lack of universal standards creates vendor lock-in. Companies succeed by acting as the master system integrators, but this requires vast experience. New suppliers often struggle as their products must prove compatibility with existing ecosystems from giants, which can necessitate costly custom development work for each deployment.

Intelligent Transportation System Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.7% |

|

Base Year Market Size (2025) |

USD 42.8 billion |

|

Forecast Year Market Size (2035) |

USD 75.2 billion |

|

Regional Scope |

|

Intelligent Transportation System Market Segmentation:

Deployment Segment Analysis

The cloud-based solutions are leading and are poised to hold the share value of 55.4% by 2035 in the intelligent transportation system market. This model is favored for its scalability, lower upfront capital expenditure, and ability to integrate and analyze vast disparate data streams in real time from across a city’s mobility network. Cloud platforms enable seamless updates, advanced AI analytics, and easier interoperability between different ITS components, which is vital for the evolving smart city ecosystems. Government transport agencies are increasingly adopting cloud-first strategies for new projects. Further, the government transport agencies are increasingly adopting cloud-first strategies for new projects. Additionally, the government spending on public cloud services has surged by the 17.1% as per the data reported by the World Bank in 2022, highlighting the accelerated transition from legacy on-premise systems.

Component Segment Analysis

The software dominates and holds the highest share value in the market. The segment reflects the core value shift from hardware to data intelligence and the ongoing management. This includes analytics platforms, AI-driven management software, cybersecurity solutions, and system integration services. The growth is further driven by the need to process data from sensors and cameras into actionable insights for traffic prediction, autonomous vehicle support, and dynamic pricing. The hardware becomes a data-gathering commodity while the software creates the actionable intelligence. Additionally, recurring software revenues from updates, cloud-based platforms, and data-driven services are strengthening long-term vendor profitability and market stickiness.

End user Segment Analysis

The government transportation agencies are leading the end-user segment in the intelligent transportation system market. As the primary owners and operators of public road infrastructure, they are the principal investors in large-scale ITS deployments for traffic management, public safety, and congestion reduction. Their procurement drives the market, focusing on solutions that improve operational efficiency, enhance commuter safety, and meet sustainability goals. The scale of their investment is substantial. Moreover, government mandates on smart mobility emission reduction and urban digitization are accelerating nationwide ITS rollouts across highways and smart cities. Long-term public funding programs and public–private partnerships further ensure stable demand and continuous system upgrades.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Component |

|

|

Application |

|

|

Deployment |

|

|

End user |

|

|

System |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Intelligent Transportation System Market - Regional Analysis

North America Market Insights

The North America intelligent transportation system market is the largest and dominating one and is projected to hold the regional revenue share of 38.6% by 2035. The demand is driven by the federal infrastructure modernization funding and stringent road safety mandates. The U.S. Bipartisan Infrastructure Law provides multi-year non-discretionary funding streams for ITS deployment via programs such as SMART Grants and PROTECT. Moreover, the national roadway safety strategy compels technology adoption to reduce fatalities. Further, the dominant trend is the shift from hardware-centric projects to integrated, cloud-based software platforms for traffic management and data exchange, with a parallel emphasis on resilient and secure infrastructure to withstand cyber threats and climate events.

The federal safety led funding programs most notably the Safe Streets and Roads for All (SS4A) initiative administered by the U.S. Department of Transportation is driving the market in U.S. SS4A awards fund safety planning activities covering over half of the U.S. population creating a nationwide pipeline of data driven roadway assessments and implementation projects that directly depend on traffic analytics monitoring and safety management systems. According to the U.S. Department of Transport in February 2023, traffic crashes generated an economic burden of USD 340 billion, strengthening the fiscal justification for ITS-enabled prevention and post-crash response investments. Moreover, in the first SS4A funding round, U.S. DOT awarded 474 action plan grants and 37 implementation grants, signaling near-term demand for deployable safety systems at the municipal and county level. These data signal a positive impact on the market growth in the U.S.

Sustained federal infrastructure funding, urban safety priorities, and congestion mitigation mandates, with the procurement largely led by public agencies and municipal transit authorities is propelling the intelligent transportation market in Canada. According to the Government of Canada's November 2024 report, the federal government committed USD 30 billion for public transit projects, including traffic management and smart mobility systems. Further, the report from the Government of Canada in May 2024, Transport Canada reports that road safety remains a material public concern, with 1,931 road traffic fatalities recorded in 2022, reinforcing demand for data-driven traffic monitoring, collision analytics, and enforcement support systems across provinces. These federally funded safety and efficiency imperatives, along with the municipal climate and mobility reporting requirements, position the Canada market for a steady and government-led growth.

Number of Fatalities (2003-2022)

|

Year |

Fatalities |

|

2003 |

2,777 |

|

2004 |

2,735 |

|

2005 |

2,898 |

|

2006 |

2,871 |

|

2007 |

2,753 |

|

2008 |

2,431 |

|

2009 |

2,216 |

|

2010 |

2,238 |

|

2011 |

2,023 |

|

2012 |

2,075 |

|

2013 |

1,951 |

|

2014 |

1,841 |

|

2015 |

1,887 |

|

2016 |

1,900 |

|

2017 |

1,861 |

|

2018 |

1,930 |

|

2019 |

1,761 |

|

2020 |

1,711 |

|

2021 |

1,821 |

|

2022 |

1,931 |

Source: Government of Canada May 2024

APAC Market Insights

The Asia Pacific intelligent transportation system market is anticipated to register the fastest CAGR of 9.5% during the forecast period of 2026 to 2035. The market is propelled by the massive government-led urbanization, infrastructure modernization, and strategic industrial policy. The core drivers are smart transportation and 5 G-enabled connectivity. A dominant trend is the adoption of cloud native AI powered traffic management platforms and extensive deployments of electronic toll collection and traffic surveillance to combat congestion in cities. The APAC region deploys large-scale, greenfield ITS projects, creating demand for complete turnkey systems. Additionally, countries like Japan and South Korea are driving innovation in autonomous vehicle testing ecosystems and V2X communication standards supported by strong public-private partnerships.

market in India is accelerated by large-scale highway expansion and expressway investments that require continuous traffic monitoring, enforcement, and corridor-level management. As per IBEF November 2025 data, India’s National Highway network reached 146,204 km, significantly expanding the operational base for ITS deployment across federal and state-managed corridors. Further, the Government of India announced a ₹11 lakh crore program to develop 17,000 km of high-speed access-controlled expressways by 2033, with around 40% already under construction and most sections targeted for completion by 2030, creating near- and mid-term visibility for ITS procurement. These government-funded programs position ITS as a foundational operational layer for India’s expanding road network, supporting sustained market growth driven by MoRTH, NHAI, and state public works authorities.

The intelligent transportation system market in China is being accelerated by large-scale government-led transport modernization under the 14th Five-Year Plan, which emphasizes integration, safety, smart upgrades, and green transformation across national networks. According to the People’s Republic of China, in July 2025, China invested ¥15.2 trillion in transport fixed assets, representing a 23.3% increase over the previous planning cycle, providing a substantial funding base for digital traffic management and network coordination systems. Further, by 2024, more than 90% of the national comprehensive transport network framework was already in place, shifting policy focus from physical expansion toward operational efficiency and intelligent control. The scale of the network, 191,000 km of expressways, 5.49 million km of highways, 162,000 km of railways, and urban systems supporting 300 million daily public transport trips, creates sustained demand for traffic monitoring sensor integration and centralized management platforms. Overall, these policy-backed investments position China as a continued growth market.

Europe Market Insights

The intelligent transportation system market in Europe is growing significantly and is driven by the regulatory framework from the EU, prioritizing safety, sustainability, and digital integration. The core driver is the EU’s sustainable and smart mobility strategy, which mandates significant reductions in transport emissions and road fatalities, directly pushing the member states to invest in traffic management, connected vehicle infrastructure, and multimodal ticketing systems. A key trend is the push for a cooperative intelligent transport system, creating a harmonized cross-border digital ecosystem for vehicle-to-everything communication. Moreover, the market is shifting from the standalone national systems toward interoperable cloud-based platforms that support real-time data sharing across borders.

A strong federal investment in digital infrastructure, with the requirements for data security protocols and resilient sensor network design, is accelerating the market in Germany. According to the EIA June 2024 data, EUR 12.8 billion is allocated for digital transport infrastructure and mobility modernization, including funding streams supporting connected traffic management and roadside sensing systems operated by federal and state authorities. Further, the UDV December 2021 data shows that nearly 45% of accidents are due to a collision with a vehicle driven by someone. Further reinforcing ITS adoption, Germany’s Federal Office for Information Security (BSI) reported that transport and traffic control systems are among the critical infrastructures subject to mandatory IT security audits under the KRITIS framework, pushing federal and state authorities to upgrade secure data transmission, encryption, and sensor network resilience as part of new ITS procurements.

Safety performance targets sustained government investment in digital road infrastructure and data governance requirements led by national and local transport authorities, which is driving the market in UK. The UK government report in May 2023 has reported that it has invested £23 billion in the Strategic Road Network, supporting smart motorway operations, traffic monitoring, and incident management systems operated by National Highways. Moreover, the UK Research and Innovation in December 2025, safety outcomes remain a core policy driver, as 1,695 road fatalities were recorded in 2022, reinforcing the continued deployment of data-driven safety and traffic control systems. Further, Innovate UK manages an average annual budget of £300 to £400 million, working with government partners to fund transport innovation, including connected and intelligent road systems. Overall, the UK market is expected to rise steadily.

Key Intelligent Transportation System Market Players:

- Thales Group (France)

- Siemens Mobility (Germany)

- Kapsch TrafficCom (Austria)

- Q-Free (Norway)

- FLIR Systems (U.S.)

- Cubic Transportation Systems (U.S.)

- Iteris, Inc. (U.S.)

- Motorola Solutions (U.S.)

- IBM Corporation (U.S.)

- Cisco Systems, Inc. (U.S.)

- TomTom (Netherlands)

- Garmin Ltd. (U.S.)

- Hitachi Rail (Japan)

- Mitsubishi Electric Corporation (Japan)

- NEC Corporation (Japan)

- Samsung SDS (South Korea)

- Hyundai Mobis (South Korea)

- Kapsch TrafficCom India (India)

- Adatek (Australia)

- SMH Rail & Transit Sdn. Bhd. (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Thales Group leverages its defense and aerospace expertise to create secure integrated ITS solutions. Their strategy focuses on developing AI-powered traffic management platforms that unify urban mobility data from road sensors to public transit, enhancing the city-wide efficiency and safety within the intelligent transportation system market. In 2024, the company made annual sales of €20 billion.

- Siemens Mobility is a leader in rail and road convergence, investing heavily in digital twins and cloud-based IoT platforms such as Siemens Xcelerator. Their initiative centers on creating a seamless, sustainable mobility network using data analytics to optimize traffic flow and rail operations across the market. In 2024, the company made an income of 9,620 million euros.

- Kapsch TrafficCom strategically focuses on congestion pricing and tolling technologies as a core growth vector. They are pioneering solutions for connected vehicles and enforcement systems, helping cities implement effective urban traffic management strategies within the competitive intelligent transportation system market.

- Q-Free champions open standards and interoperable ITS architecture. Their key initiatives involve expanding their portfolio of radar-based detection and smart city intersection technologies, aiming to provide scalable vendor-agnostic solutions that improve traffic safety and data collection in the intelligent transportation system market.

- Teledyne FLIR dominates in thermal imaging and video analytics. Their strategy integrates advanced sensors and AI-driven perception software for traffic monitoring, incident detection, and vulnerable road user protection, providing critical data inputs for the market.

Here is a list of key players operating in the global market:

The market is highly competitive and fragmented, with dominance by established infrastructure and technology giants from North America, Europe, and East Asia. The key players are aggressively pursuing growth via strategic mergers and acquisitions to expand their geographical reach and technological portfolio. For example, in August 2024, Iteris was acquired by Almaviva for USD 335 million. Moreover, the major focus is on the heavy R&D investment in cloud-based solutions, AI, machine learning, and vehicle-to-everything communication to develop integrated smart city ecosystems. Partnerships with governments and local entities are also crucial for deploying large-scale contract-based projects as the market shifts from traditional hardware towards data-centric software-defined platforms.

Corporate Landscape of the Intelligent Transportation System Market:

Recent Developments

- In July 2025, Modaxo Inc., a global technology organization focused on moving the world’s people, announced the launch of Intelliscape, a new brand and organization comprising intelligent transport systems for road and rail assets acquired from SEA, a division of Cohort PLC.

- In March 2025, Huawei unveiled seven innovative ICT products and solutions across four major transportation sectors. The company's digital and intelligent foundation contributes to empowering the transportation industry and accelerating industry intelligence.

- In August 2024, RGBSI announced the launch of its state-of-the-art smart transportation products, developed to redefine safety, efficiency, and innovation in the mobility sector. These products, created with cutting-edge technology and engineering, align with RGBSI’s commitment to advancing global transportation.

- Report ID: 3261

- Published Date: Feb 17, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.