Thermal Management Materials Market Outlook:

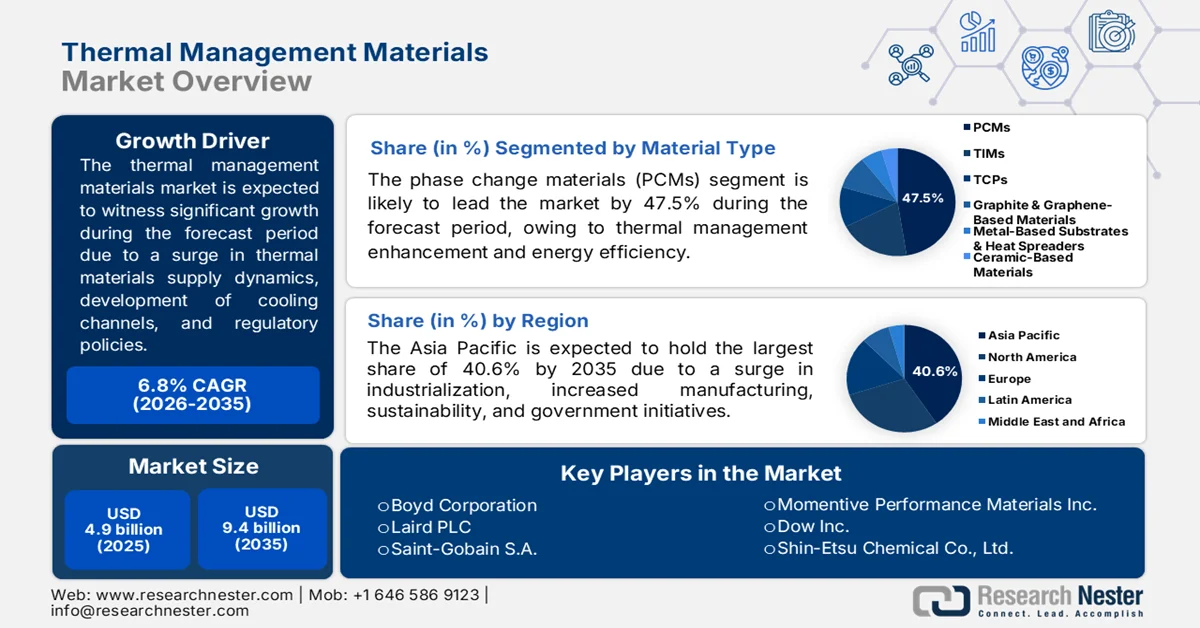

Thermal Management Materials Market size was valued at USD 4.9 billion in 2025 and is expected to reach USD 9.4 billion by the end of 2035, gradually mounting at a 6.8% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of thermal management materials is estimated at USD 5.2 billion.

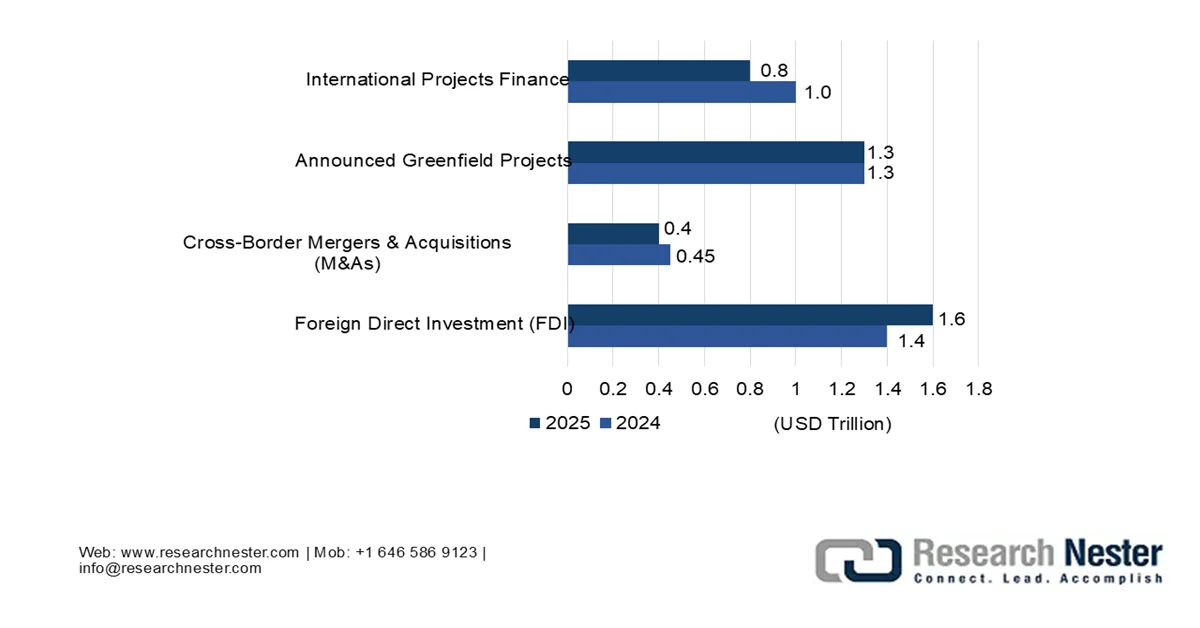

The global thermal management materials market is significantly gaining exposure, owing to the increased emphasis on thermal materials supply chain dynamics, expansion in data centers, additive manufacturing of conformal cooling channels, and regulatory pressure on per-and polyfluoroalkyl substances phase-outs. According to an official data report published by the UN Trade and Development Organization in January 2026, data centers are readily shaping global investments, with an increase in foreign direct investment (FDI) of USD 270 billion, highly fueled by a surge in the demand for artificial intelligence (AI) facilities and digitalized networks. In addition, data centers account for over 1/5th of the worldwide greenfield project valuations, which makes them the largest recipients of global investments, thus denoting a huge growth opportunity for the thermal management materials market.

Rise in Global FDI for Data Centers, 2024-2025

Source: UN Trade and Development Organization

Furthermore, the recycling infrastructure and thermal material circular economy, thermal acoustics integration, and the presence of self-healing thermal interfaces are a few trends that are readily responsible for driving the thermal management materials market globally. As stated in an article published by the IEA Organization in 2022, the worldwide sales of heat pumps upsurged by 11% as of 2022, marking a second year of double-digit growth for the centralized technology for securing sustainable heat. Based on this growth, there was an increase in heat pump sales in Europe by 40%. Additionally, the sales of air-to-water models, which are suitable for underfloor heating systems and typical radiators, increased by nearly 50%. Moreover, in the U.S., there has also been an expansion in the purchase of gas furnaces, while China continues to remain the largest heat pump economy, thus enhancing the market demand.

Yearly Global Sales Growth of Heat Pumps, 2021-2022

|

Components/Countries |

Sales % |

|

Global Heat Pumps |

11.0% |

|

Global Air-to-Water Heat Pumps |

24.0% |

|

Europe |

49.0% |

|

Japan |

13.0% |

|

China |

2.0% |

|

Global Air-to-Air Heat Pumps |

5.0% |

|

Europe |

19.0% |

|

U.S. |

11.0% |

|

China |

6.0% |

Source: IEA Organization

Key Thermal Management Materials Market Insights Summary:

Regional Highlights:

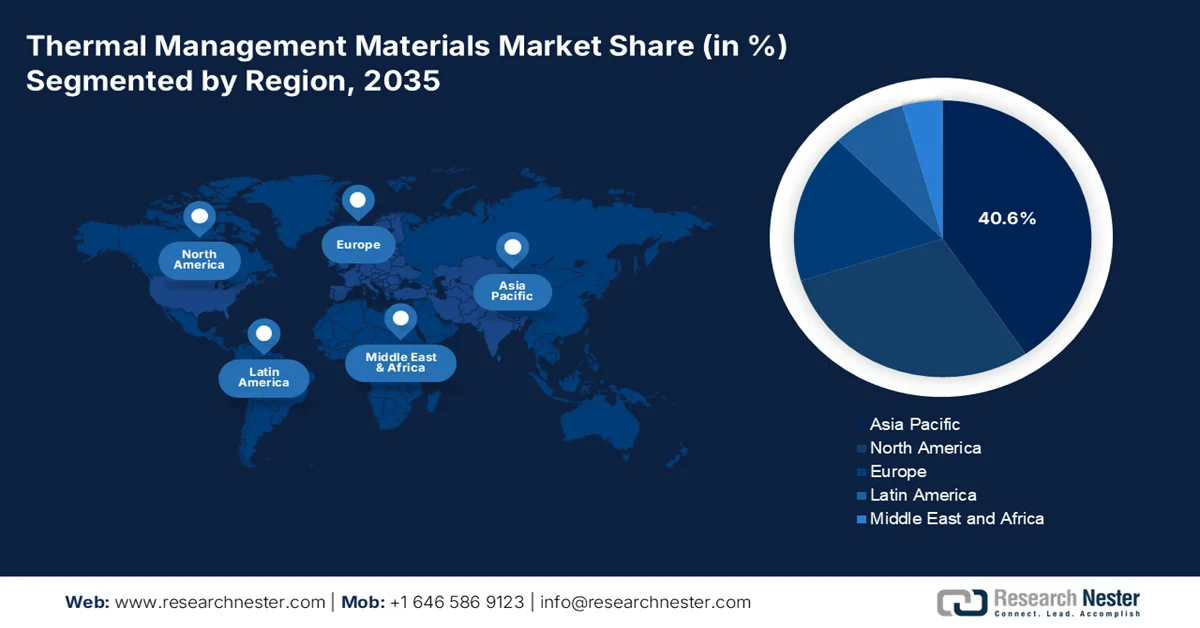

- The thermal management materials market in Asia Pacific is projected to account for a 40.6% share by 2035, driven by accelerating EV production, expanding 5G infrastructure deployment, and strong manufacturing concentration across China, Japan, and South Korea

- Europe is anticipated to witness the fastest expansion in the market throughout 2026–2035, fueled by automotive electrification, stringent sustainability regulations, and rising investments in next-generation 5G network infrastructure

Segment Insights:

- The phase change materials (PCMs) segment is forecast to capture a 47.5% share of the thermal management materials market by 2035, owing to increasing demand for advanced thermal energy storage solutions in concentrated solar power applications

- The consumer electronics sub-segment is projected to secure the second-largest share in the market during the forecast period, stimulated by growing digital connectivity, rising data center electricity consumption, and expanding low-carbon technology deployment

Key Growth Trends:

- Miniaturization-induced thermal density

- Increase in quantum computing cryogenics

Major Challenges:

- Raw material volatility and geopolitical concentration

- Technical complexity of multi-material integration

Key Players: Henkel AG & Co. KGaA, 3M Company, Honeywell International Inc., DuPont de Nemours, Inc., Parker Hannifin Corporation, Wacker Chemie AG, Boyd Corporation, Laird PLC, Saint-Gobain S.A., Momentive Performance Materials Inc., Dow Inc., Shin-Etsu Chemical Co., Ltd., Panasonic Corporation, Kaneka Corporation, Fujipoly Sarcon Corporation, Dexerials Corporation, European Thermodynamics Ltd, tesa SE, LISAT Corporation.

Global Thermal Management Materials Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4.9 billion

- 2026 Market Size: USD 5.2 billion

- Projected Market Size: USD 9.4 billion by 2035

- Growth Forecasts: 6.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (40.6% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: China, United States, Japan, Germany, South Korea

- Emerging Countries: India, Vietnam, Brazil, Saudi Arabia, Indonesia

Last updated on : 13 May, 2026

Thermal Management Materials Market - Growth Drivers and Challenges

Growth Drivers

- Miniaturization-induced thermal density: The effective proliferation of proactive implantable medical devices, such as cochlear implants, neurostimulators, and leadless pacemakers, is driving the thermal management materials market growth globally. According to official statistics published by the World Health Organization (WHO) in April 2026, heat-based mortality for people aged more than 65 years gradually increased by an estimated 85%. Besides, roughly 489,000 heat-related deaths occur every year, with 45% cases in Asia and 36% in Europe. Regarding this, approximately 61,672 heat-driven excessive deaths have occurred in Europe, based on which there is an increase in the utilization of medical devices, which is highly responsible for fueling the market’s growth across different nations.

- Increase in quantum computing cryogenics: Quantum processors effectively operate at certain temperatures, which has created an increased demand for cryogenic thermal interface materials. As stated in an article published by NLM in August 2025, magnesia, as a thermal material, is significantly recognized as a suitable replacement for alumina, owing to its thermal conductivity that ranges between 40 and 60 W m−1 K−1. In addition, this particular range for the material has been widely accepted and effectively aligns with the theoretically calculated thermal conductivity of magnesia-based single crystals, ranging from 50 to 60 W m−1 K−1. Besides, quantum computing organizations are increasingly specifying diamond-filled composites, along with rare-earth-specific alloys that continue to remain compliant, thereby proliferating the thermal management materials market globally.

- Hydrogen fuel cell thermal gradients: The aspect of proton-exchange membrane fuel cells demands simultaneous heating during cold start, which is positively driving the thermal management materials market worldwide. This bidirectional requirement requires thermal management materials with rapid response times and uniform heat distribution across the cell stack. Besides, an expansion in the hydrogen economy, especially in stationary and heavy-duty trucking power, demonstrates a distinct factor that separates from battery thermal management due to the availability of unique bi-directional thermal gradients. Moreover, the continuous supply facility for insulating materials is also responsible for enhancing the market’s demand globally.

2024 Global Insulating Materials Export and Import Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

Germany |

314 million |

121 million |

|

U.S. |

280 million |

270 million |

|

China |

225 million |

- |

|

Canada |

- |

110 million |

|

Global Trade Valuation |

1.9 billion |

|

|

Global Trade Share |

0.008% |

|

|

Product Complexity |

1.2 |

|

Source: OEC

Challenges

- Raw material volatility and geopolitical concentration: The single greatest structural risk to the thermal management materials market is the geographic concentration of critical raw materials, specifically gallium, indium, and synthetic graphite. China controls the majority of global refined gallium and indium production, both essential for liquid metal thermal interface materials and high-performance conductive polymers. Recent export controls imposed by Beijing on these metals have demonstrated how quickly supply chains can seize, forcing downstream manufacturers into bidding wars for restricted inventory. This volatility is not merely a pricing issue; it becomes a qualification nightmare. Besides, automotive and data center OEMs require multi-year supply stability to justify the expensive reliability testing and certification processes for new thermal materials.

- Technical complexity of multi-material integration: Modern thermal management solutions are rarely a single material; they are multi-layered systems that must interface seamlessly with substrates, adhesives, heatsinks, and active cooling hardware. The roadblock lies in the fact that a high-performance thermal grease may excel in lab conditions but fail catastrophically in the field due to pump-out, dry-out, or interfacial delamination caused by coefficient of thermal expansion mismatches. Engineers face a frustrating trade-off: select a material with exceptional thermal conductivity but poor mechanical reliability, or choose a durable material that underperforms under peak load. This complexity is magnified in applications, such as AI server racks, where repeated thermal cycling from idle to full operational load can exceed, thus causing a hindrance in the thermal management materials market.

Thermal Management Materials Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.8% |

|

Base Year Market Size (2025) |

USD 4.9 billion |

|

Forecast Year Market Size (2035) |

USD 9.4 billion |

|

Regional Scope |

|

Thermal Management Materials Market Segmentation:

Material Type Segment Analysis

Based on the material type, the phase change materials (PCMs) segment is anticipated to garner the highest share of 47.5% in the thermal management materials market by the end of 2035. The segment’s upliftment is primarily attributed to its importance for enhancing thermal management and energy efficiency by effectively storing and releasing huge amounts of latent heat at particular temperatures. For instance, as stated in an article published by Applied Thermal Engineering in January 2025, the worldwide concentrating solar power fleet is projected to grow to 73 GW, 281 GW, and 426 GW by the end of 2030, 2040, and 2050, respectively. Therefore, there is continuous research and development for phase change materials, particularly for thermal energy storage in concentrated solar power, which is positively impacting the segment’s growth and development globally.

End use Application Segment Analysis

During the forecast period, the consumer electronics sub-segment, which is part of the end use applications segment, is projected to grab the second-highest share in the thermal management materials market. The sub-segment’s growth is highly driven by its importance for a modernized lifestyle that is fueling digitalized connectivity, technological advancement, and economic growth. According to official statistics published by the UN Trade and Development (UNCTAD) Organization in 2024, the mineral production for digital transition, including cobalt, lithium, and graphite, is expected to increase by 500% by the end of 2050 to meet the increasing need for low-carbon and digital technologies. Besides, data centers, which are the backbone of the digital world, significantly consumed approximately 460 TWh of electricity as of 2022, which is further predicted to double by the end of 2026, thereby denoting a huge growth opportunity for consumer electronics.

Form Factor Segment Analysis

The greases and pastes sub-segment, part of the form factor segment, is expected to account for the third-highest share in the thermal management materials market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by reducing friction, preventing wear, and protecting machinery from contamination and corrosion across hard-to-reach and heavy-duty areas. These dispensable materials are engineered as viscous, fluid compounds that fill microscopic air gaps between a heat-generating component, such as a central processing unit or power module, and a heat sink or cooling plate. Their primary advantage is ultra-low bond line thickness, which minimizes thermal resistance and enables superior heat transfer compared to solid pads.

Our in-depth analysis of the thermal management materials market includes the following segments:

|

Segment |

Subsegments |

|

Material Type |

|

|

|

|

Form Factor |

|

|

Technology/Thermal Conductivity |

|

|

Encapsulation Technology |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Thermal Management Materials Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the thermal management materials market is anticipated to garner the highest share of 40.6% by the end of 2035. The market’s upliftment is primarily attributed to increased industrialization, concentrated manufacturing across South Korea, Japan, and China, the exponential growth in the electric vehicle production, government strategies, sustainable transportation, and 5G infrastructure deployment. According to official statistics published by the IEA Organization in 2025, there has been an increase in the electric car production in China, which has reached 12.4 million as of 2023. In addition, the country remains one of the world’s largest electric car manufacturing facilities, catering to over 70% of the global production as of 2024. Besides, domestic OEMs effectively accounted for over 80% of production, thereby making it suitable for uplifting the thermal management materials market growth in the region.

Electric Cars and Car Manufacturing Production in China and China Joint Venture, 2021-2024

|

Year |

China (Million) |

China Joint Venture (Million) |

|

2021 |

2.3 |

0.8 |

|

2022 |

4.8 |

1.0 |

|

2023 |

6.9 |

1.1 |

|

2024 |

10.2 |

1.3 |

Source: IEA Organization

The thermal management materials market in China is growing significantly, owing to the massive electronics manufacturers, strong electric vehicle production targets, which is readily supported by the National Development and Reform Commission (NDRC), as well as the Made in China 2025 approach, and expansion in 5G facilities. As stated in an article published by the State Council in December 2025, the value-added industrial output of the majority of manufacturing organizations increased by 10.6% year-on-year (YoY). Additionally, there was also an increase in their combined operating revenues by 8.4% to almost USD 1.9 trillion, and meanwhile, overall profits surged by 12.8% to USD 83.4 billion. Besides, the country produced 1 billion smartphones, indicating a 0.7% rise, thereby denoting an optimistic outlook of the market’s growth and expansion.

The aspects of strict energy conservation policies, reliance on imports for upstream electronic materials and a strong electronics export supply chain, as well as an increase in the utilization of renewable energy in mainstream energy consumption, are certain factors that are positively driving the thermal management materials market in Japan. Besides, the domestic thermal management materials industry size was worth USD 214.9 million as of 2025, which is projected to grow at USD 230.8 million by 2026, and further upsurge to USD 438.5 million, along with a 7.4% growth rate by the end of 2035. Moreover, as per the 2025 Japan Electronics and Information Technology Industries Association (JEITA) data report, the country’s exports of electronic components and devices approximately reached USD 7.5 million, thus demonstrating a surge by 100.9%, which is suitable for the thermal management materials market upliftment.

Electronics Export Analysis in Japan, 2025

|

Components |

March 2025 |

2025 Total To Date |

||

|

Amount (USD Million) |

% |

Amount (USD Million) |

% |

|

|

Consumer Electronic Equipment |

226.1 |

99.7 |

638.9 |

106.3 |

|

Video |

208.9 |

99.6 |

590.7 |

10.6.2 |

|

Audio |

17.2 |

100.8 |

48.1 |

107.4 |

|

Industrial Electronic Equipment |

1,401.5 |

99.3 |

3,673.8 |

101.6 |

|

Telecommunication |

1.9 |

129.8 |

4.8 |

99.8 |

|

Radio Communication |

144.9 |

100.1 |

394.4 |

104.2 |

|

Computers and Information Terminals |

283.9 |

100.2 |

765.5 |

107.1 |

|

Electronic Application Equipment |

414.0 |

91.0 |

1,094.4 |

93.2 |

|

Electric Measuring Instrumentation |

553.2 |

105.8 |

1,406.9 |

105.2 |

|

Electronic Business Machines |

3.3 |

85.8 |

7.6 |

120.4 |

|

Electronic Components and Devices |

6,123.4 |

101.4 |

16,854.7 |

104.5 |

|

Electronic Components |

1,433.6 |

103.3 |

3,969.7 |

107.1 |

|

Electronic Devices |

3,222.2 |

103.8 |

8,775.2 |

105.4 |

Source: JEITA

Europe Market Insights

Europe in the thermal management materials market is expected to emerge as the fastest-growing region during the forecast period. The market’s development is highly propelled by the rapid electrification of the automotive industry, strict environmental regulations under REACH and the Europe Green Deal directives, and the expansion of 5G telecommunications infrastructure. According to official statistics published by Europe Digital Strategy in August 2025, the Europe Commission and the Smart Networks and Services Joint Undertaking (SNS JU) significantly allocated more than USD 352 million in funding for supporting innovative research, advancement in next-generation networks, and facility deployment. Based on this, there has been an expansion of basic 5G networks across the region, thereby making it suitable for enhancing the thermal management materials market exposure.

5G Households Coverage Analysis in Europe, 2024

|

Countries |

Coverage % |

|

Netherlands |

1.0% |

|

Denmark |

1.0% |

|

Austria |

1.0% |

|

Greece |

1.0% |

|

Italy |

0.9% |

|

Germany |

0.9% |

|

Norway |

0.9% |

|

Sweden |

0.9% |

Source: Europe Digital Strategy

The thermal management materials market in Germany is gaining increased traction, owing to the largest automotive manufacturing facility, the presence of the massive chemical industry, the acceleration in the deployment of renewable energy systems, and government support through partnerships and grants. As stated in an article published by the ITA in August 2025, the country comprises a target of 80% of its overall electricity supply from renewables by the end of 2030, of which 59% was achieved as of 2024. Besides, the nation has planned to diminish its greenhouse gas emissions by 65% by the end of the same year, which is part of its objective to gain carbon neutrality by the end of 2045. Moreover, carbon dioxide emissions decreased in 2024, with the country remaining the 6th most carbon-intensive electricity in the overall region at 381 gCO₂/kWh, which is fueling the market development.

The existence of industrial decarbonization mandates, expansion in data center and immersion cooling adoption, the development of energy efficiency regulations, offshore and nuclear wind thermal management requirements, and hydrogen economy infrastructure are a few trends that are responsible for expanding the thermal management materials in the UK. As per an article published by the Climate Change Committee in June 2025, the country has an ambitious target to reduce emissions by 68% by the end of 2030 and achieve Net Zero by 2050. This target is highly driven by the decarbonization of the electricity system by replacing both gas and coal. In addition, future progress is expected to utilize low-carbon electricity and adopt suitable solutions, including engineered removals and tree planting, thus expanding the market’s reach in the overall country.

North America Market Insights

North America in the thermal management materials market is projected to experience considerable growth by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by the exponential growth of data center facilities, an increase in the rapid adoption of electric vehicles, necessitating sophisticated battery thermal management, along with the reshoring of pharmaceutical manufacturing and semiconductor. According to official statistics published by the Congress Government in January 2026, the data center yearly energy utilization as of 2023 accounted for an estimated 176 TWh, which is roughly 4.4% if annual electricity consumption, especially in the U.S. In addition, data center energy consumption is expected to double or triple by the end of 2028, accounting for almost 12% of domestic electricity consumption, thereby driving thermal management materials market growth in the country.

The thermal management materials market in the U.S. is gaining exposure, owing to the concentration of major technology organizations, the unprecedented demand for liquid cooling solutions, the reshoring of semiconductor manufacturing, growth in the aerospace and defense industry, and the expansion of the electric vehicle sector. As stated in an article published by the Semiconductor Industry Association in 2026, based on semiconductors, the chips powering modern smartphones comprise over 15 billion transistors, with the capability of switching on and off numerous times every second. Additionally, semiconductors are a huge part of AI-based data centers that contain various transistors, and the country commands more than 50% of worldwide chip revenues. Besides, through research investments and government incentives, over 100 projects have been announced across 28 states, thus positively fueling the thermal management materials market growth in the nation.

The presence of natural resource industries and clean technology, along with supply chain dynamics for the electric vehicle battery supply chain, generous government investments in battery gigafactories, an increase in the demand for thermal interface materials, and the telecommunications infrastructure rollout are certain factors for driving the thermal management materials market in Canada. As per an article published by the Government of Canada in October 2025, the Minister of Energy and Natural Resources declared an investment of more than USD 22 million in supporting 8 projects to escalate battery advancement and production capacity across the country. This was suitable for powering electric vehicles and achieving net-zero emissions by the end of 2050, as well as ensuring the worldwide battery demand, which is projected to surge by almost 150-fold, thus proliferating the thermal management materials market growth.

Key Thermal Management Materials Market Players:

- Henkel AG & Co. KGaA (Germany)

- 3M Company (U.S.)

- Honeywell International Inc. (U.S.)

- DuPont de Nemours, Inc. (U.S.)

- Parker Hannifin Corporation (Chomerics division) (U.S.)

- Wacker Chemie AG (Germany)

- Boyd Corporation (U.S.)

- Laird PLC (UK)

- Saint-Gobain S.A. (France)

- Momentive Performance Materials Inc. (U.S.)

- Dow Inc. (U.S.)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Panasonic Corporation (Japan)

- Kaneka Corporation (Japan)

- Fujipoly Sarcon Corporation (Japan)

- Dexerials Corporation (Japan)

- European Thermodynamics Ltd (UK)

- tesa SE (Germany)

- Parker Hannifin Corporation (Chomerics division) (U.S.)

- LISAT Corporation (U.S.)

- HP Additive Manufacturing Solutions (U.S.)

- Boyd Corporation (U.S.)

- Mitsubishi Chemical Group (Japan)

- ZF (Germany)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Henkel AG & Co. KGaA maintains a commanding presence in the thermal interface materials segment through its extensive portfolio of dispensing solutions, including thermally conductive adhesives and gap fillers tailored for automotive power electronics. The company focuses on formulating high-reliability greases that address pump-out and dry-out failures in high-temperature EV battery modules.

- 3M Company leverages its expertise in microreplication and material science to produce advanced thermal management films, pads, and tapes for consumer electronics and data center infrastructure. The company actively develops compressible, high-performance interface materials that accommodate uneven surface topography while maintaining consistent thermal conductivity under compression.

- Honeywell International Inc. has established itself as a supplier of premium thermal interface materials for mission-critical aerospace and high-performance computing applications, where reliability under extreme conditions is non-negotiable. The company offers phase change materials and thermal greases specifically engineered to withstand repeated thermal cycling without degradation or migration.

- DuPont de Nemours, Inc. utilizes its deep heritage in polymer science to deliver thermally conductive silicones, encapsulants, and adhesives that serve electric vehicle battery packs and 5G telecommunications hardware. The company emphasizes halogen-free and low-volatility formulations to meet evolving regulatory standards for indoor and automotive applications.

- Parker Hannifin Corporation (Chomerics division) specializes in hybrid solutions that combine thermal management with electromagnetic interference shielding, addressing a critical need in dense electronic enclosures. Chomerics has developed a reputation for gap-filling pads and conductive putties that maintain performance across wide temperature ranges encountered in industrial and defense environments.

Here is a list of key players operating in the global thermal management materials market:

The global thermal management materials market is characterized by the dominance of diversified U.S. chemical conglomerates and specialized German and Japan-based material science firms. A critical strategic shift is underway from passive product supply to integrated thermal solution design. Key players are aggressively pursuing vertical integration, typified by Alexium International's acquisition of Microtek Laboratories to secure Phase Change Material (PCM) supply chains. Besides, in November 2025, HP Additive Manufacturing Solutions announced a series of latest collaborations and innovations for its objective to escalate the implementation of additive manufacturing across different industries. In addition, the company’s goal is to simplify complexity and ensure creativity by empowering engineers, creators, and designers with the correct tools for designing and producing, thus bolstering the thermal management materials industry worldwide.

Corporate Landscape of the Thermal Management Materials Market:

Recent Developments

- In March 2026, Boyd Corporation successfully completed the sale of its thermal business to Eaton for USD 9.5 billion, leading to its engineered materials business operating as an independent organization, which is further backed by Goldman Sachs Alternatives.

- In December 2025, Mitsubishi Chemical Group and Boston Materials, Inc. collaborated with each other, driven by investments from MCG’s U.S.-specific corporate venture capital group, known as Diamond Edge Venture, for making advancements in thermal management solutions for high-performance computing and AI data centers.

- In June 2025, ZF introduced TherMas for reducing the energy requirement of batteries through improved heat utilization and efficiency during winter conditions, along with significantly delivering heating and cooling capacities at almost 10 kW at temperatures of -25 degrees Celsius and 35 degrees Celsius.

- Report ID: 8563

- Published Date: May 13, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Thermal Management Materials Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.