Textured Soy Protein Market Outlook:

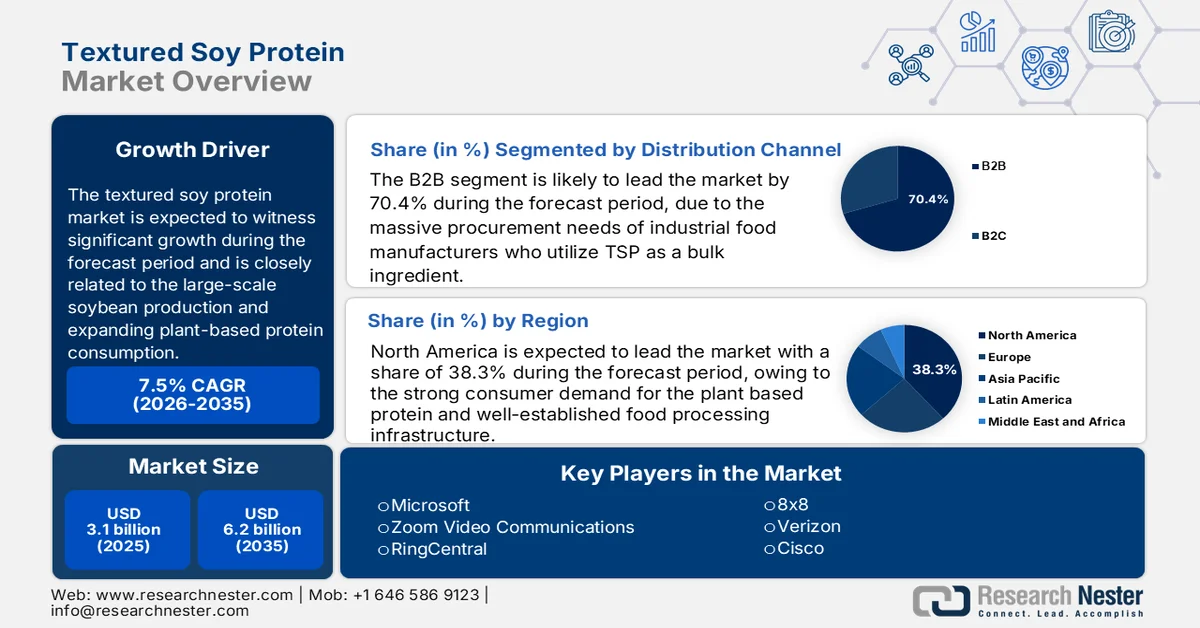

Textured Soy Protein Market size was valued at USD 3.1 billion in 2025 and is projected to reach USD 6.2 billion by the end of 2035, rising at a CAGR of 7.5% during the assessed period, i.e., 2026-2035. In 2026, the industry size of textured soy protein is evaluated at USD 3.2 billion.

The global textured soy protein market is supported by the large-scale soybean production, expanding plant-based protein consumption, and policy alignment toward sustainable protein systems. According to the USDA May 2025 data, the food and beverage sector accounted for 16.8% of sales and 15.4% of all employees from all U.S. manufacturing establishments in 2021. Further, the federal dietary guidance continues to promote the plant-based protein intake. Moreover, the dietary guideline recommends legumes and soy products as a core protein alternative, influencing procurement standards across institutional feeding programs. On the other hand, the USDA in August 2024 states that the U.S. federal spending on food and nutrition assistance exceeded USD 142.2 billion in 2024, demonstrating the scale at which dietary standards can shape the protein sourcing decisions.

Besides, the demand for growth is reinforced by the food security and sustainability properties. Moreover, the global meat consumption continues to rise, increasing the pressure on the alternative protein supply chain to support sustainable dietary diversification. On the other hand, the U.S. EPA's March 2025 data notes that agriculture accounts for 9.4% of total U.S. greenhouse gas emissions, driving the policy attention toward lower-emission protein sources. In Asia, the imports on soybean remain elevated to meet the food and feed demand. This scale of trade underpins global soy processing capacity expansion. Collectively, robust soybean output, institutional dietary alignment, and environmental policy pressures are reinforcing steady growth conditions for textured soy protein across industrial food manufacturing and export markets.

Key Textured Soy Protein Market Insights Summary:

Regional Highlights:

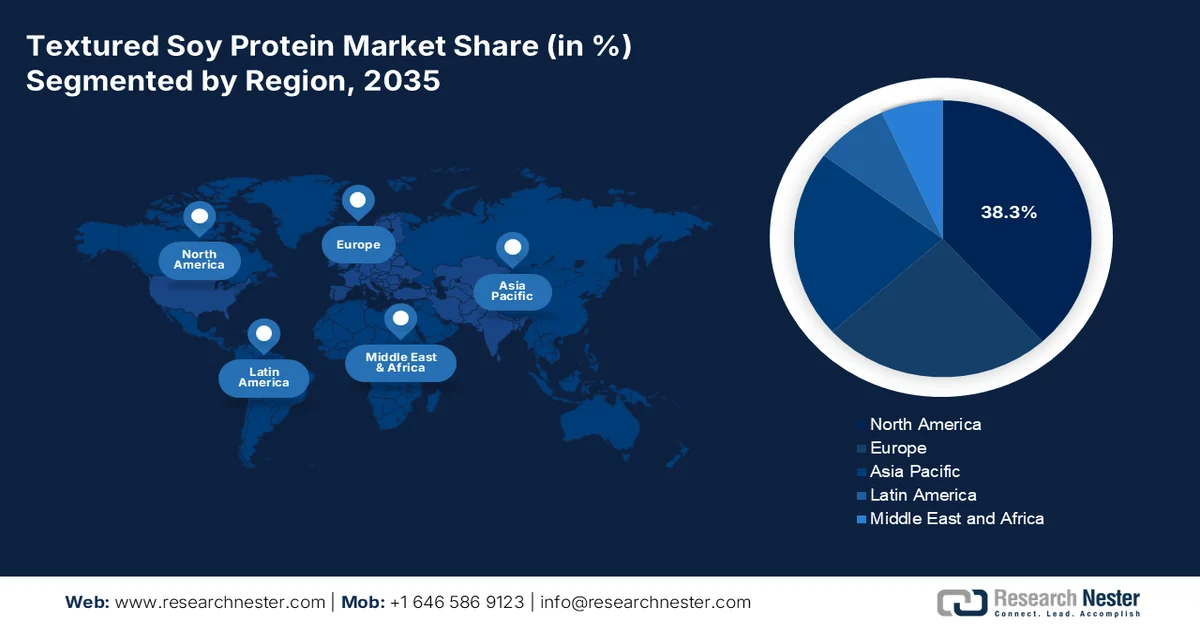

- North America is projected to secure a 38.3% share by 2035 in the textured soy protein market, attributed to robust consumer demand for plant-based proteins and a well-established food processing ecosystem.

- Asia Pacific is anticipated to expand at a CAGR of 8.8% during 2026–2035, fueled by rising population, increasing disposable incomes, and shifting dietary preferences toward plant-based proteins.

Segment Insights:

- The B2B segment in the textured soy protein market is forecast to command a 70.4% share by 2035, propelled by large-scale procurement requirements from industrial food manufacturers utilizing TSP as a bulk ingredient for plant-based and hybrid meat products.

- The Food Processing Industry segment is expected to retain the largest share through 2035, stimulated by its extensive use of textured soy protein in meat analogues, ready-to-eat meals, and protein-rich snack formulations.

Key Growth Trends:

- Expansion of government food and nutrition assistance spending

- Promoting plant based protein intake

Major Challenges:

- High capital investment

- Competition from alternative plant proteins

Key Players: Archer Daniels Midland Company (ADM), Cargill, Incorporated, DuPont (Nutrition & Biosciences), The Scoular Company, Farbest Brands, Gillco Ingredients, White River Soy Processing, LLC, Crown Soya Protein Group, Linyi Shansong Biological Products Co., Ltd., Austrade Inc., Fuji Oil Holdings Inc., Nisshin Oillio Group, Ltd., The Hain Celestial Group, George Weston Foods, CJ CheilJedang Corporation, Daesang Corporation, Ruchi Soya Industries Ltd., Sonic Biochem Extractions Ltd., Vinayak Ingredients (India) Pvt. Ltd., Azelis.

Global Textured Soy Protein Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.1 billion

- 2026 Market Size: USD 3.2 billion

- Projected Market Size: USD 6.2 billion by 2035

- Growth Forecasts: 7.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, Canada

- Emerging Countries: India, Brazil, South Korea, Spain, Italy

Last updated on : 9 March, 2026

Textured Soy Protein Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of government food and nutrition assistance spending: Public food procurement programs influence the plant protein demand. According to the USDA August 2025 data, the U.S. federal spending on food and nutrition assistance exceeded USD 142.2 billion in 2024, covering programs such as SNAP, the national school lunch program, and WIC. Moreover, the national school programs have served several meals to the children. The federal meal standards allow legumes and soy products as protein components, creating a recurring institutional demand. As governments expand food subsidy programs to manage inflation and food insecurity, cost-efficient protein formats gain procurement priority. For the suppliers in the market, alignment with the institutional nutritional specifications and bulk tender participation provides stable volume channels. Similar publicly funded feeding programs across Europe and Asia reinforce the structured demand for plant-based protein ingredients in processed foods supplied to schools, hospitals, and community feeding systems.

- Promoting plant based protein intake: Government dietary policy strongly shapes protein-sourcing patterns. The dietary guidelines for the U.S. recommend beans, peas, lentils, and soy products as part of healthy dietary patterns. These guidelines influence federal procurement of military rations and healthcare meal services. According to CDC data from April 2025, 9 in 10 U.S. adults have at least one chronic disease, underscoring the public health emphasis on preventive dietary strategies. Further, the plant based protein are promoted for cardiovascular and metabolic health outcomes. Moreover, the institutional catering and contract foodservice providers frequently align menus with alternatives. The manufacturers in the market believe that policy-aligned formulation capabilities improve eligibility for large-scale supply agreements and long-term institutional contracts.

- Growth in global soybean production and trade: Raw material availability highlights the market manufacturing expansion. As per the data published in the USDA 2025 data, the global soybean production reached 427.15 million metric tons in 2024 to 2025. This surge in production is supporting large-scale processing infrastructure. Government-supported crop insurance, farm subsidies, and export programs stabilize the soybean supply chain. Consistent production growth reduces the input volatility and supports downstream value-added soy protein processing. For TSP processors, proximity to high-output soybean regions lowers the logistics costs and improves the capacity planning. Export-oriented crushing and protein extraction facilities are expanding in the key producing regions, strengthening global supply reliability.

Top Soybean Producing Countries

|

Market |

% of Global Production |

Total Production (2024/2025, Metric Tons) |

|

Brazil |

40% |

171.5 Million |

|

U.S. |

28% |

119.05 Million |

|

Argentina |

12% |

51.11 Million |

|

China |

5% |

20.65 Million |

|

India |

3% |

12.58 Million |

|

Paraguay |

2% |

10.2 Million |

|

Canada |

2% |

7.57 Million |

|

Ukraine |

2% |

7.2 Million |

|

Russia |

2% |

7.05 Million |

|

Uruguay |

0.98% |

4.2 Million |

Source: USDA 2025

Challenges

- High capital investment: Producing high-quality textured soy protein requires advanced extrusion technology, mainly high moisture extrusion systems that create meat textures. High investment is required leveraging long standing technological capabilities to meet the demand in Europe. The company utilizes advanced systems such as Soprotex N long fiber slices and Tradcon to simulate whole chicken muscle texture. For new entrants, the capital expenditure for such equipment in the market, coupled with the technical expertise required to operate it, presents a formidable barrier to entry.

- Competition from alternative plant proteins: The market faces growing competition from other plant-based proteins, including pea, chickpea, fava bean, quinoa, and emerging fungal proteins. Top companies produce fungal protein, which naturally possess meat like fiber structure. New entrants focused solely on soy may find their addressable market reducing as food manufacturers diversify protein sources to meet the consumer preferences for variety and reduced allergenicity.

Textured Soy Protein Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.5% |

|

Base Year Market Size (2025) |

USD 3.1 billion |

|

Forecast Year Market Size (2035) |

USD 6.2 billion |

|

Regional Scope |

|

Textured Soy Protein Market Segmentation:

Distribution Channel Segment Analysis

The B2B sub-segment is dominating and is poised to hold the share value of 70.4% by the end of 2035 in the textured soy protein market. The dominance is due to the massive procurement needs of industrial food manufacturers who utilize TSP as a bulk ingredient for producing plant-based meat pet food and hybrid meat products. These manufacturers require consistent quality technical specifications and volume pricing that only direct B2B transactions can provide. According to the United Soybean Board data in 2026, the U.S. is the leading exporter of soybeans, contributing USD 29.6 billion, with the vast majority destined for foreign food processing plants rather than retail shelves. This data underscores the global reliance on industrial supply chains, where ingredients such as the textured soy protein move through B2B channels to be transformed into the finished consumer goods before ever reaching a store.

End user Segment Analysis

The food processing industry is the predominant end-user segment in the market, accounting for the largest share. This sector relies on the TSP as a foundational ingredient for creating a diverse array of products, including meat analogues, ready-to-eat meals, and nutritional snacks. The scalability of food processors allows them to absorb massive volumes of the TSP, driving innovation in the product texture and flavor profiles to meet evolving consumer tastes. As per the IBEF November 2025, the food processing industry in India reached USD 354.5 billion, highlighting the growth potential and the demand for texturized proteins in the emerging markets to cater to the rising population seeking convenient protein-rich foods.

Type Segment Analysis

Dry textured soy protein sub segment is leading the type segment in the market due to its logistical advantages and versatility. Dry TSP offers manufacturers extended shelf life, reduced shipping costs, and the flexibility in the rehydration during the final production process. It serves as the workhorse ingredient for a wide range of applications, from meat extenders to baked goods. Further certain percentage of the soy protein isolates and textured concentrates processed in the U.S. were produced in the dry form to facilitate global trade and storage. This shows the preference for the dry formats as they allow for efficient long-distance transportation and inventory management, making them the backbone of the global textured soy protein supply chain.

Our in-depth analysis of the textured soy protein market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Form |

|

|

Nature |

|

|

Application |

|

|

Distribution Channel |

|

|

Source |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Textured Soy Protein Market - Regional Analysis

North America Market Insights

North America holds the largest share of the global textured soy protein market at 38.3% by the end of 2035. The market is driven by the strong consumer demand for the plant based protein and well established food processing infrastructure. The U.S. dominates the region due to its large health-conscious consumer base and active investment in plant-based innovation, while Canada emerges as a key market with the rising plant-based food consumption. The key drivers include growing vegan trends, lactose intolerance awareness, and innovation in plant-based food products. Supportive government policies and investments in alternative proteins further boost the expansion of the market in North America. The region benefits from the advanced processing technologies and clean-label trends that expand application ranges for textured soy protein in meat substitutes, dairy alternatives, and functional foods.

Increase consumer demand on plant-based protein, raw material scale, export strength, and product innovation are scaling the market in the U.S. As per the report by the MedlinePlus April 2025 data, the U.S. FDA states that 25 grams per day of soy protein may reduce the risk of heart disease, reinforcing soy’s role in cholesterol management and preventive nutrition strategies. Moreover, the USDA January 2025 data depict that the U.S. soybean production reached 4,465 million bushels in 2021, with exports totaling 2,158 million bushels, demonstrating strong upstream capacity and global trade integration that underpins domestic soy protein processing. Additionally, the NLM study in October 2023 shows that the advancements in extrusion technology, such as thiamine-enhanced textured soy protein improves the sensory scores and indicate measurable improvements in product performance for meat analog applications. These data boost the growth prospects for the U.S. market across food manufacturing and plant-based meat segments.

The domestic consumption structure of plant-based protein and application-level demand is fueling the market in Canada. According to the Government of Canada, July 2025 data, Canada exported USD 2.4 billion of plant-based and animal protein ingredients, highlighting a strong cross-border trade integration and processing capacity. Besides, the non-animal-derived proteins accounted for 43.6 thousand tonnes in 2023, indicating a structural preference toward plant-based formats. Soy protein concentrate alone represented 51.9% of plant-based protein volume sales, underscoring soy’s dominant role in processed meat substitutes, baked goods, and staple food categories. In retail, plant-based packaged food sales reached USD 1.6 billion in 2022, with strong performance in the plant-based milk and meat substitutes; therefore, there is a stable growth in Canada market.

Canada Plant-Based Protein Ingredient Market Share by Volume (2023)

|

Protein Ingredient |

Market Share (%) |

|

Soy Protein Concentrate |

51.9% |

|

Gluten |

31.1% |

|

Soy Protein Isolate |

10.4% |

|

Pea Protein |

5.6% |

|

Vegetable Proteins |

1.0% |

Source: Government of Canada, July 2025

APAC Market Insights

The Asia Pacific represents the fastest-growing market and is poised to grow at a CAGR of 8.8% during the forecast period 2026 to 2035. The textured soy protein market in Asia Pacific is driven by the increasing population, rising disposable incomes, and shifting dietary patterns toward plant-based proteins. Traditional soy-based diets in countries such as China, Japan, and India provide a strong cultural foundation for market acceptance. Moreover, the rapid urbanization and expanding middle-class populations are surging the demand for convenient protein-rich processed foods. The government initiatives promoting food security and protein self-sufficiency are fueling the investments in domestic processing capabilities. The region benefits from the established soybean processing infrastructure and the growing plant-based meat alternatives sector.

The production strength, nutritional positioning, and downstream processing capacity are shaping the market in India. As per the report from the PJTAU, October 2025 data, India’s soybean production reaching 14.98 million tonnes reflects a strong domestic raw material base supporting soy protein extraction and value-added manufacturing. Moreover, the MOSPI June 2025 report shows that soybeans containing over 40% protein represent one of the richest plant-based protein sources. Additionally, the presence of more than 2,000 soy food industries operating across small, medium, and large scales indicates an established processing ecosystem catering to the local and regional demand. High daily output of soymilk tofu and related soy products demonstrates consistent consumer acceptance and supply chain depth, hence showing a strong and expanding market for soy-derived protein ingredients, including textured soy protein, across retail and institutional channels.

India Soybean Supply and Demand

|

|

2022-23 |

2023-24 |

2024-25 |

2025-26 |

|

Opening Stocks |

0.50 |

0.50 |

0.30 |

0.50 |

|

Production |

15.00 |

13.10 |

15.20 |

14.40 |

|

Imports |

0.80 |

- |

0.10 |

0.20 |

|

Total Availability |

16.30 |

13.50 |

15.60 |

15.00 |

|

Crush |

14.70 |

12.30 |

13.90 |

13.10 |

|

Total Consumption |

15.80 |

13.20 |

15.10 |

14.40 |

|

Exports |

- |

- |

- |

- |

|

Ending Stocks |

0.50 |

0.30 |

0.50 |

0.60 |

Source: PJTAU, October 2025

The market in China is supported by large-scale soybean imports, expanding domestic processing capacity, and strong demand from the plant-based and food manufacturing sectors. As per the OEC 2024 data, China remains the world’s largest soybean importer. The country has imported over USD 47.2 billion in 2024, ensuring consistent raw material availability for crushing and protein extraction industries. Moreover, the country’s established tofu soy beverage and meat alternative segments provide a mature consumption base for soy-derived proteins, while rapid growth in convenience foods and ready meals is increasing industrial demand for functional protein ingredients. With sustained import volumes, strong domestic soy food traditions, and scaling industrial food production, China remains a high-volume and strategically significant market for textured soy protein across both traditional and modern retail channels.

Europe Market Insights

The Europe is experieincing significant growth due to increasing consumer demand for the plant based protein sources, rising awareness of health benefits, and a shift towards sustainable food options. The market is defined by a diverse range of applications, including meat analogs, snacks, and ready-to-eat meals. The key countries, such as Germany UK, and France, contribute significantly to market share, reflecting a robust demand for the soy-based meat alternatives. The market players are focusing on product diversification, sustainable sourcing, and strategic partnerships to enhance their market presence and meet the evolving consumer preferences across Europe. The expansion of the textured soy protein market in Europe is fueled by the increased adoption of plant-based diets, supportive regulatory frameworks, and innovations in product formulations.

The textured soy protein market in Germany is supported by the strong oilseed processing capacity, rising plant-based consumption, and expanding foreign trade. According to the OEC 2024 data, Germany imported over 1.7 billion tonnes of soybeans in 2024, reflecting sustained raw material inflows for the crushing and protein ingredient production. Moreover, Germany’s food and feed soybean imports remain substantial within EU trade flows, reinforcing its position as a central processing and redistribution hub. Public nutrition strategy initiatives under the German federal government further emphasize plant-based dietary patterns, influencing institutional catering and retail product development. Further, the high soybean import volumes, declining meat consumption, and policy-supported dietary transition are strengthening long term demand conditions for soy-based protein ingredients across Germany’s food manufacturing and retail sectors.

The health driven demand and large-scale soybean import dependency that support domestic processing and food manufacturing are fueling the growth of the market in the UK. According to the Heart UK June 2024 clinical guidance, indicating that 15 grams of soy protein per day can contribute to the reduction of cholesterol equivalent to two large glasses of soy drink or 100g of fresh edamame, reinforces soy’s positioning within heart-health and preventive nutrition strategies, influencing retail and foodservice formulation decisions. Moreover, the NLM study March 2024 data depicts that the UK imports 33 million tonnes of soybean products annually for USD 16.54 billion, demonstrating a substantial reliance on international soy supply chains to support the demand for feed and food ingredients. Further, the health-linked consumption drivers and high-volume soybean imports underpin steady growth prospects for the UK.

Key Textured Soy Protein Market Players:

- Archer Daniels Midland Company (ADM) (U.S.)

- Cargill, Incorporated (U.S.)

- DuPont (Nutrition & Biosciences) (U.S.)

- The Scoular Company (U.S.)

- Farbest Brands (U.S.)

- Gillco Ingredients (U.S.)

- White River Soy Processing, LLC (U.S.)

- Crown Soya Protein Group (Denmark)

- Linyi Shansong Biological Products Co., Ltd. (China)

- Austrade Inc. (Germany)

- Fuji Oil Holdings Inc. (Japan)

- Nisshin Oillio Group, Ltd. (Japan)

- The Hain Celestial Group (UK)

- George Weston Foods (Australia)

- CJ CheilJedang Corporation (South Korea)

- Daesang Corporation (South Korea)

- Ruchi Soya Industries Ltd. (India)

- Sonic Biochem Extractions Ltd. (India)

- Vinayak Ingredients (India) Pvt. Ltd. (India)

- Azelis (Luxembourg)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Archer Daniels Midland Company is the top player in the global market, leveraging its agricultural supply chain and processing capabilities. As a key player, the company has focused on expanding its portfolio of non-GMO and organic textured soy proteins to meet the surging demand from the plant-based food sector. The company has made a net earnings of USD 1,800 in 2024.

- Cargill, Incorporated, holds a significant position in the textured soy protein market, utilizing its vast global network to supply high-quality ingredients to the food and beverage industry. Recognizing the shift toward plant-based diets, Cargill has adopted a strategy centered on product innovation and sustainability.

- DuPont, via its nutrition and biosciences division, is a major innovator in the market, known for its advanced ingredient technologies and deep application expertise. The company’s strategic focus is on providing integrated solutions that combine textured soy proteins with hydrocolloids and cultures to optimize the taste, texture, and nutrition of plant-based meats.

- The Scoular Company has carved out a strong niche in the textured soy protein market by focusing on supply chain efficiency and customized ingredient solutions for the mid-market food companies. As a key player, the company’s strategic initiatives center on agility and responsiveness, providing textured soy protein in various forms.

- Farbest Brands is a prominent supplier and distributor in the textured soy protein market, distinguished by its long-standing relationships with the leading global manufacturers. The company’s strategic approach involves bridging the gap between top-tier TSP producers and food companies across North America, offering a reliable supply of high-stability, consistent ingredients.

Here is a list of key players operating in the global market:

The global textured soy protein market is highly competitive, characterized by the presence of large multinational agribusinesses and specialized regional players. The key strategic initiatives among market leaders include a significant investment in research and development to improve the texture and functionality of TSP for use in plant-based meat alternatives. The companies are actively expanding their production capacities and forming strategic partnerships with the food manufacturers to secure supply chains. Further, the major trend is the focus on non-GMO and organic product lines to cater to the health-conscious consumer base in Europe and North America. Mergers and acquisitions are also prevalent as the larger firms seek to enhance their technological capabilities and geographical footprint. In September 2022, ADM opened a new extrusion facility in Serbia, meeting accelerated demand for the textured soy proteins.

Corporate Landscape of the Textured Soy Protein Market:

Recent Developments

- In May 2024, Gillco, a soy protein supplier is proud to offer SUPRO soy protein to those looking to produce plant-based meat alternatives with delicious taste, texture, and nutritional value.

- In March 2024, Azelis, a leading innovation service provider in the specialty chemicals and food ingredients industry, announced a new distribution agreement with Soy Austria, a leading manufacturer of natural, sustainable, soy-based ingredients for the food industry.

- In February 2024, White River Soy Processing, LLC, a developer and operator of oilseed processing plants in the U.S., announced that it purchased Benson Hill Ingredients, LLC, which operates an established food grade soybean processing facility in Creston, Iowa, from Benson Hill, Inc.

- Report ID: 8425

- Published Date: Mar 09, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.