Sustainable Packaging Materials Market Outlook:

Sustainable Packaging Materials Market size was valued at USD 331.9 billion in 2025 and is anticipated to reach USD 709.9 billion by the end of 2035, expanding at around 7.9% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of sustainable packaging materials is evaluated at USD 358.1 billion.

The global sustainable packaging materials market is poised for solid growth in the upcoming years, effectively fueled by shifting consumer values, strict environmental mandates, and corporate sustainability rules. Companies across the globe are proactively transitioning from single-use plastics to address their ecological footprints, thereby fueling intense research into advanced biodegradable polymers, plant-based fibers, and easily recyclable mono-materials. In October 2025, Eurostat reported that the European Union generated a total of 79.7 million tons of packaging waste in 2023, which is equal to almost 177.8 kg per person, showing a slight decrease from 2022 but still higher than 2013 levels by 21.2 kg per capita. In addition, the article also mentioned that packaging waste composition was dominated by paper and cardboard with almost 40.4%, followed by plastic 19.8%, glass 18.8%, wood 15.8%, and metals 4.9%, thus elevating the growth potential of sustainable packaging solutions.

EU Packaging Waste Statistics 2023: Total Generation, Plastic Waste, and Recycling Rates per Capita

|

Indicator |

Value |

|

Waste per capita (all packaging) |

177.8 kg |

|

Plastic packaging waste per capita |

35.3 kg |

|

Plastic waste recycled per capita |

14.8 kg |

|

Plastic recycling rate |

42.1% |

|

Share of plastic in total packaging waste |

19.8% |

|

Change in plastic waste vs 2022 |

-1.0 kg per capita |

|

Change in recycling vs 2022 |

+0.1 kg per capita |

Source: Eurostat

Furthermore, the cross-industry demand is readily accelerating technological advancements that enhance the strength and barrier properties of green alternatives, which is making them viable for sensitive sectors such as food, beverages, and pharmaceuticals. On the other hand, as manufacturing processes mature and supply chains for bio-based raw materials stabilize, these eco-friendly solutions are making a move from smaller premium options to mainstream industry standards, thus reshaping the future of the market. In April 2026, BASF announced the expansion of its ecovio® portfolio with new certified home-compostable grades, which are especially designed for flexible packaging, offering adjustable barrier properties against grease, oxygen, moisture, and liquids for FMCG applications such as food, personal care, and pet food. The company also mentioned that the modular material toolbox enables manufacturers to design suitable packaging structures for either paper or plastic substrates.

Key Sustainable Packaging Materials Market Insights Summary:

Regional Highlights:

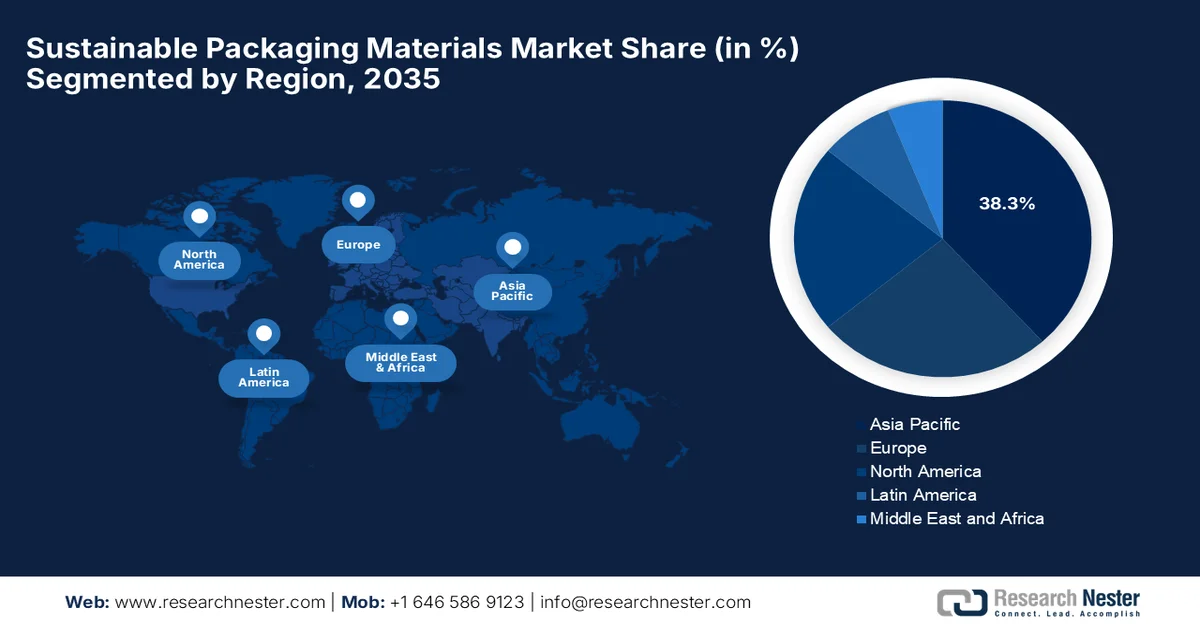

- Asia Pacific is anticipated to capture the largest 38.3% share by 2035 in the sustainable packaging materials market, fueled by strong economic expansion, rapid urbanization, and rising disposable incomes

- North America is expected to witness considerable growth throughout 2026-2035, bolstered by state-level environmental mandates and a highly conscious consumer base

Segment Insights:

- The Paper and Paperboard segment is projected to account for the highest 37.4% share by 2035 in the sustainable packaging materials market, driven by rising demand for paper-based packaging across the food & beverage and e-commerce industries

- The Rigid Packaging segment is poised to secure a considerable revenue share by 2035, supported by its extensive adoption across the food & beverage, personal care, and healthcare sectors

Key Growth Trends:

- Corporate sustainability commitments

- Growth of e-commerce and retail sector

Major Challenges:

- High production costs compared to conventional packaging

- Inadequate recycling and composting infrastructure

Key Players: Amcor (Switzerland),Mondi (UK),Smurfit Westrock (Ireland),Huhtamaki (Finland),Stora Enso (Finland),DS Smith (UK),Sealed Air (U.S.),Sonoco Products Company (U.S.),Walki Group (Finland),envoPAP (India),Paptic (Finland),Kelpi (UK) ,Tata Steel Nederland (Netherlands),EcoEnclose (U.S.),BioPak (Australia).

Global Sustainable Packaging Materials Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 331.9 billion

- 2026 Market Size: USD 358.1 billion

- Projected Market Size: USD 709.9 billion by 2035

- Growth Forecasts: 7.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (38.3% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Germany, Japan, India

- Emerging Countries: Vietnam, Indonesia, Thailand, Brazil, Mexico

Last updated on : 8 July, 2026

Sustainable Packaging Materials Market - Growth Drivers and Challenges

Growth Drivers

- Corporate sustainability commitments: Most of the global companies have been opting for sustainability goals and net-zero targets, which prompts increased adoption of eco-friendly packaging. In this context, brands are redesigning supply chains and packaging strategies in order to align with ESG standards to meet investor expectations, thereby boosting demand in the sustainable packaging materials market. In November 2023, Nokia reported that it had shifted its Fixed Networks Lightspan portfolio packaging to 100% recyclable materials, thereby eliminating plastics, foam, and chemical treatments while replacing them with biodegradable and fully recyclable cardboard-based components. The company also notes that this redesign remarkably reduces packaging size and weight, thereby improving logistics efficiency and cutting transport-related CO₂ emissions by up to 60%.

- Growth of e-commerce and retail sector: The continued expansion of e-commerce and organized retail is fueling demand for sustainable packaging solutions. There have been rising shipment volumes due to which companies are looking for lightweight, durable, and eco-friendly materials to reduce logistics costs and environmental impact. In May 2026, the U.S. Census Bureau reported that in the first quarter of 2026, U.S. retail e-commerce sales reached USD 326.7 billion, seasonally adjusted, rising 2.7% from the previous quarter. The total retail sales increased to almost USD 1,929 billion, which is up 1.5% over the same period. On the other hand, e-commerce has been expanding its role in the retail sector, accounting for 16.9% of total sales, whereas on a year-over-year basis, sales grew 9.8% compared with Q1 2025, while total retail sales increased by 3.9%, indicating a stronger opportunity for the market globally.

Challenges

- High production costs compared to conventional packaging: This is one of the main burdens for the sustainable packaging materials market. The materials such as molded fiber, biodegradable polymers, recycled resins, and specialty paper necessitate advanced manufacturing technologies and additional processing steps, thereby increasing overall production expenses. Apart from this, limited economies of scale for certain bio-based materials also contribute to higher prices, which is making adoption difficult for cost-sensitive industries and small manufacturers. Also, fluctuations in the availability and pricing of renewable feedstocks impact production costs. As a result, most of the businesses depend on traditional packaging materials despite sustainability commitments, slowing the widespread commercialization.

- Inadequate recycling and composting infrastructure: The lack of well-developed recycling and industrial composting infrastructure is a major barrier hindering the growth of the market. Most of the sustainable packaging solutions are especially designed to be recyclable or compostable, and their environmental benefits depend on the availability of efficient collection, sorting, recycling, and composting systems. Most of the developing regions face disparities in terms of waste management facilities, which leads to improper disposal of recyclable and biodegradable packaging materials. Also, differences in recycling standards across countries and contamination of recyclable waste streams reduce material recovery rates. Hence, these infrastructure limitations reduce the effectiveness of circular economy initiatives and hinder the full environmental potential of sustainable packaging solutions.

Sustainable Packaging Materials Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.9% |

|

Base Year Market Size (2025) |

USD 331.9 billion |

|

Forecast Year Market Size (2035) |

USD 709.9 billion |

|

Regional Scope |

|

Sustainable Packaging Materials Market Segmentation:

Material Type Segment Analysis

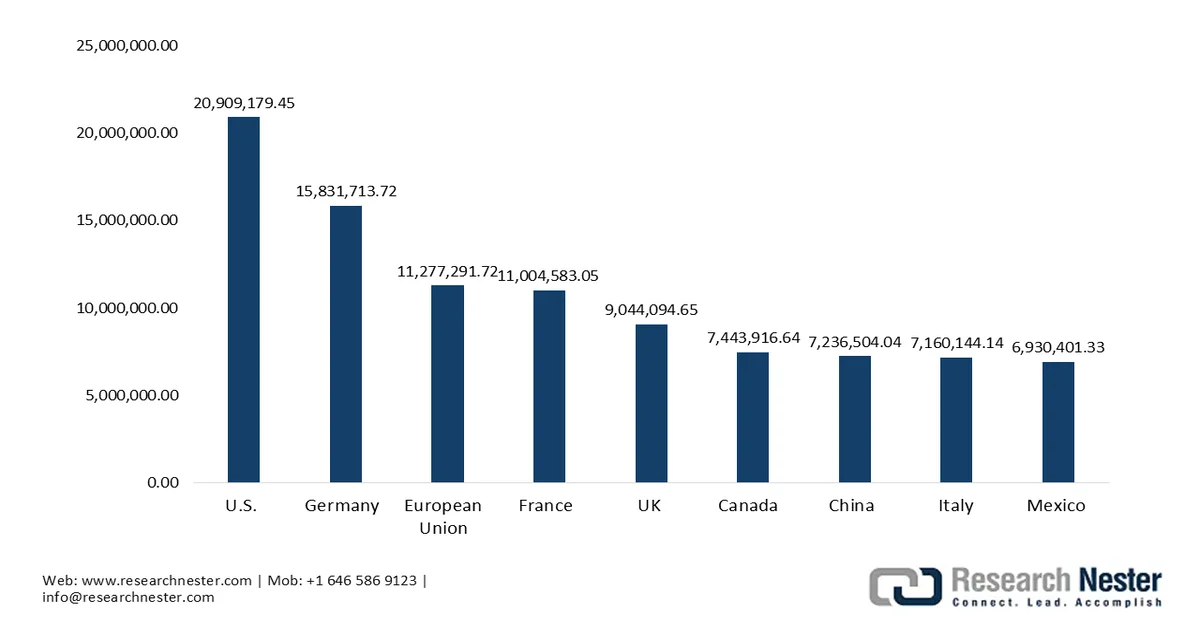

In paper and paperboard in the material type segment is anticipated to hold the highest share of 37.4% in the sustainable packaging materials market during the forecast period. The dominance is propelled by the demand for paper-based packaging, especially strong in the food and beverage and e-commerce industries, in which lightweight, printable, and eco-friendly solutions are preferred. In addition, the advancements in terms of coated and laminated paperboard are also improving resistance to moisture and grease, expanding their range of applications. For instance, in June 2023, Amcor announced the expansion of its AmFiber™ performance paper packaging range in Europe to include heat-seal sachets for culinary and beverage products such as instant coffee, spices, drink powders, and soups. Besides, this recyclable, high-barrier paper-based solution provides strong protection against oxygen and moisture, thus denoting a wider segment scope.

Top Global Importers of Paper and Paperboard in 2023: Country-wise Trade Value Insights

Source: WITS

Packaging Type Segment Analysis

The rigid packaging is projected to attain a considerable revenue share in the market by the conclusion of 2035. The segment’s growth is mainly propelled by its extensive use across food and beverage, personal care, and healthcare sectors. At the same time, it offers key benefits which include strong product protection, tamper resistance, and improved shelf appeal. In February 2023, Gerresheimer and Medicos Beauty Group together reported the development of a sustainable clickable refill jar system combining a reusable glass container with a plastic inner and closure designed for easy refill use. This system uses materials such as 40% post-consumer recycled glass, bio-based polypropylene, and recyclable plastics, aiming to reduce resource use while maintaining durability and user convenience.

Global Imports of Glass Packaging Containers in 2023: Country-wise Shipment Value and Volume Analysis

|

Reporter |

Trade Value (1000 USD) |

Quantity |

|

France |

2,213,257.53 |

- |

|

U.S. |

1,848,906.83 |

1,609,990,000 |

|

European Union |

1,447,405.83 |

1,334,120,000 |

|

Italy |

1,112,217.22 |

1,049,130,000 |

|

Spain |

1,093,564.78 |

- |

|

Belgium |

720,838.66 |

- |

|

Germany |

693,321.00 |

478,641,000 |

|

UK |

630,761.44 |

- |

|

Canada |

425,810.32 |

- |

|

Poland |

314,508.93 |

322,325,000 |

|

Netherlands |

307,621.78 |

246,806,000 |

Source: WITS

End use Industry Segment Analysis

On the basis of end use industry, retail is projected to grow with a notable share in the market over the forecasted years. The rapid expansion of supermarkets, hypermarkets, convenience stores, and e-commerce platforms is propelling the segment’s leadership. Retailers are integrating sustainable packaging solutions to align with consumer expectations, meet regulatory requirements, and enhance differentiation in private label products. Apart from this, major retail players are also establishing ambitious sustainability targets for packaging and working closely with suppliers to develop recyclable, compostable, and reusable alternatives across their product ranges. Furthermore, initiatives such as green retailing and eco-labeling are effectively driving adoption, making sustainability a core business strategy.

Our in-depth analysis of the sustainable packaging materials includes the following segments:

|

Segment |

Subsegments |

|

Material Type |

|

|

Packaging Type |

|

|

End use Industry |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Sustainable Packaging Materials Market - Regional Analysis

APAC Market Insights

Asia Pacific sustainable packaging materials market is anticipated to garner the highest share of 38.3% during the forecast period. The region’s leadership is mainly propelled by strong economic expansion, rapid urbanization, and increasing disposable incomes across countries such as China, India, Japan, South Korea, and those in Southeast Asia. The growing middle-class population, along with heightened environmental awareness, is simultaneously boosting demand for packaged goods and sustainable packaging solutions. In August 2025, the International Trade Administration reported that in 2023, Japan generated almost 7.69 million tons of plastic waste, of which only 460,000 tons, i.e., about 6%, were recycled domestically, whereas significant volumes were either processed through material recycling 1.7 million tons or exported 1.25 million tons. It reported that to improve this, Japan’s Ministry of Environment (MOE) and Ministry of Economy, Trade and Industry (METI) aim to raise recycled plastic use to 1 million tons by 2030, with additional sector-specific targets such as automotive applications reaching 25,000 tons by 2031 and 200,000 tons by 2041.

The nation’s ban on single-use plastics and carbon neutrality targets are responsibly boosting growth in the China sustainable packaging materials market. Meanwhile, local material science innovation has been accelerating, wherein manufacturers are scaling up the production of agricultural waste composites and bio-based polymers to meet this surging demand. The government data published in December 2023 revealed that China introduced a green packaging standards system for the express delivery sector, with a collective aim to reduce excessive packaging and improve recycling practices across e-commerce logistics. One of the primary goals of the plan is that 10% of recycled express packaging should be used for intracity, along with broader efforts to expand cardboard reuse and reduce non-recyclable materials, thus making it suitable for standard market growth.

The sustainable packaging materials market in India is projected to experience explosive growth in the upcoming years owing to a growing emphasis on a circular economy. This rapid expansion of e-commerce, quick-commerce, and food delivery networks in the urban hubs is serving as a massive catalyst, which is forcing brands to pivot toward eco-friendly alternatives. Invest India in November 2023 reported that the country’s food and beverage packaging sector is experiencing strong growth, wherein the industry is projected to reach USD 86 billion by 2029, supported by an annual growth rate of 14.8%. This expansion is driven by rising demand for efficient packaging solutions to reduce food loss caused by spoilage factors. In addition, consumer trends are also supporting this shift, with almost 66% of consumers in India preferring brands with sustainable practices, thus readily accelerating innovation in sustainable food packaging.

North America Market Insights

The North America market is expected to witness considerable growth from 2026 to 2035. The region’s prominence in this field is mainly propelled by state-level environmental mandates and a highly conscious consumer base. The region benefits from advancements in materials science and significant investments in sorting technologies designed to improve domestic recycling loops. In June 2024, the U.S. General Services Administration finalized a rule that encourages contractors to identify products with single-use plastic-free (SUP-free) packaging. This initiative applies across a large federal procurement network involving over 14,500 contractors and a total of USD 45 billion in annual sales, marking the first broad U.S. federal acquisition rule directly targeting plastic packaging waste, thus supporting the growth of the market.

Advanced biochemical engineering capabilities and innovations in terms of closed-loop circular designs are driving growth in the U.S. sustainable packaging materials market. Brands in the country are opting for agricultural waste byproducts such as mushroom mycelium, hemp hurds, and sugarcane bagasse to create molded structural cushioning. For instance, in September 2024, RENW launched in the U.S. with an innovative joint venture that produces plastic-free packaging made from industrial hemp, which offers brands a sustainable, cost-effective alternative to plastic and tree-based materials. It combines advanced technologies backed by more than 75 patents and helps companies reduce fossil fuel use, deforestation, and carbon emissions while meeting evolving regulatory and consumer demands, thus denoting a positive market outlook.

A primary focus on consumer health and agricultural residue usage in packing solutions is a visible trend boosting adoption in the Canada sustainable packaging materials market. Meanwhile, the agricultural sector is driving the adoption of flax and oat hull residues in order to engineer molded fiber containers that are capable of surviving harsh freezing temperatures during winter transport. Domestic operators are pioneering advanced solutions for the food sector that has been influenced by regulatory frameworks. In this context, Health Canada in February 2023 announced its updated guidance on food packaging materials, reaffirming that all packaging needs to comply with the Food and Drugs Act and Regulations for consumer safety. The agency also highlighted its voluntary premarket assessment program and Letters of No Objection for food packaging materials, and manufacturers will be responsible for ensuring the safety and regulatory compliance of packaging that is being used in food contact applications.

Europe Market Insights

The Europe market is expected to witness solid expansion in the upcoming years, propelled mainly by strict eco-design mandates and the commercialization of bio-benign substrates. The industry is pioneering in terms of smart, traceable packaging embedded with molecular markers to optimize high-purity sortation during mechanical and chemical recycling. In April 2026, UPM Specialty Materials and Royal Vaassen introduced Barryrwrap, which is a PFAS-free, recyclable paper packaging solution for pet treats and snacks. The packaging has been built on UPM Solide™ Lucent packaging paper, and it delivers protection against grease, moisture, oxygen, light, and aroma while supporting compliance with the EU Packaging and Packaging Waste Regulation (PPWR). Hence, such instances denote a huge opportunity for the market to grow by the end of 2035.

The high-precision engineering of bio-synthetic substrates and advanced circular economy system integration are reshaping the growth dynamics of Germany sustainable packaging materials market. Innovation in the country is structured around replacing flexible plastics with highly functional, home-compostable barrier papers treated with fluidic plant-based coatings. As of March 2023, government data in Germany, the German Packaging Act deliberately regulates packaging waste, and it introduced a compulsory deposit system for most single-use beverage packaging, charging a standard deposit of typically 25 cents to encourage recycling and reuse. This law has been strengthened over time through regional waste directives, and it promotes reduced packaging use, producer responsibility, and higher recycling rates by linking packaging fees and obligations to material consumption and environmental impact.

The UK sustainable packaging materials market is gaining enhanced traction as businesses shift toward environmentally friendly alternatives. Innovation in terms of fiber-based materials, plant-based polymers, and improved recycling systems is supporting this transition. In addition, the increasing collaboration between material suppliers, brands, and waste management systems is creating more sustainable packaging ecosystems. In September 2023, Mondi and Veetee announced the launch of the UK’s first paper-based packaging for dry rice using Mondi’s recyclable FunctionalBarrier Paper. This innovation replaces plastic packaging while still protecting the rice from moisture and maintaining shelf life, and the packs are designed to be widely recyclable through kerbside systems in the UK.

Key Sustainable Packaging Materials Market Players:

- Amcor (Switzerland)

- Mondi (UK)

- Smurfit Westrock (Ireland)

- Huhtamaki (Finland)

- Stora Enso (Finland)

- DS Smith (UK)

- Sealed Air (U.S.)

- Sonoco Products Company (U.S.)

- Walki Group (Finland)

- envoPAP (India)

- Paptic (Finland)

- Kelpi (UK)

- Tata Steel Nederland (Netherlands)

- EcoEnclose (U.S.)

- BioPak (Australia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Amcor has registered as one of the world's largest sustainable packaging manufacturers, which is serving the food, beverage, healthcare, personal care, and home care industries. The company is highly focused on developing recyclable and high-performance packaging solutions that support circular economy goals.

- Mondi is a leading integrated packaging and paper manufacturer that has a strong emphasis on sustainable packaging materials and circular design principles. The company offers a broad portfolio of paper-based, flexible plastic, and corrugated packaging solutions, which are designed to minimize environmental impact.

- Smurfit Westrock has registered itself as a global leader in paper-based sustainable packaging, which was formed through the merger of Smurfit Kappa and WestRock. In addition, the company manufactures corrugated, consumer, and specialty packaging solutions for a wide range of end use industries.

- Huhtamaki is a prominent manufacturer of sustainable foodservice and consumer packaging solutions that offers products made from renewable, recyclable, and compostable materials. The firm's competitive advantage resides in continuous product innovation, sustainable material development, and expanding manufacturing capabilities.

- Stora Enso has registered itself as a leading renewable materials company that manufactures fiber-based sustainable packaging solutions especially designed to replace fossil-based materials. The company’s packaging portfolio includes renewable paperboard, corrugated packaging, paper bags, and bio-based packaging materials serving consumer goods, food, and industrial markets.

Here is a list of key players operating in the global market:

The sustainable packaging materials market is intensely competitive, which is being led by multinational packaging manufacturers that offer paper-based, recyclable, compostable, fiber-based, and circular packaging solutions. Market leaders have been differentiating themselves through extensive manufacturing footprints, material innovation, sustainability certifications, and investments in terms of recyclable and renewable packaging technologies. Apart from this, regional manufacturers are competing by serving niche applications or local markets with customized sustainable packaging formats. In June 2025, Mondi entered into a partnership with Saga Nutrition to develop recyclable mono-material packaging for Saga’s dry pet food range, thereby replacing non-recyclable multi-material plastic. It is a part of Mondi’s recycle FlexiBag portfolio, and the packaging offers high barrier protection against moisture, fat, and odours.

Corporate Landscape of the Market:

Recent Developments

- In June 2026, Amcor entered into a partnership with Kelpi to evaluate a bio-based, seaweed-derived coating technology that improves barrier performance and recyclability for fiber-based packaging under its AmFiber™ platform. The collaboration aims to develop scalable, lower-carbon packaging solutions that reduce dependency on fossil-based materials.

- In January 2026, Tata Steel Nederland announced the launch of a new packaging steel production line using its patented TCCT (Trivalent Chromium Coating Technology), which enables more sustainable manufacturing, compliance with future regulations, and enhanced food safety.

- Report ID: 8664

- Published Date: Jul 08, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.