Dairy Packaging Market Outlook:

Dairy Packaging Market size was over USD 24 billion in 2025 and is predicted to reach USD 38.2 billion by the end of 2035, mounting at a CAGR of 5.3% during the forecast timeline, i.e., 2026-2035. In 2026, the industry size of dairy packaging is assessed at USD 25.2 billion.

The worldwide dairy packaging market is significantly being reshaped by the confluence of fundamental modifications, technological breakthroughs, and macroeconomic transitions. The market’s upliftment also reflects a suitable interplay between industrial packaging, cultural anthropology, and biological science. Besides, according to official statistics published by NLM in October 2022, just 2% of plastic packaging materials are readily recycled as packaging materials globally. Besides, 30% of plastic-based packaging products are either too small or extremely complex to recycle, thus denoting the huge importance of sustainability. Moreover, plastic materials are commonly utilized as packaging materials, and almost 26% of the overall utilization of polymers in packaging makes it the largest application of plastic materials, thus driving the market growth.

Furthermore, the aspect of gut health facility uplifting functional packaging requirements, layers of multisensory and delightful packaging experiences, an increase in beverages with the purpose of fueling functional format advancement, along with crafting heritage and conventional packaging aesthetics, are certain trends that are bolstering the market globally. As per an article published by NLM in July 2025, a surge in sugar-sweetened beverages constitutes an intake of more than 50 kcal per 226.8 gram in serving, further excluding vegetables and fruit juices. In addition, the worldwide prevalence of this particular beverage among young adults increased from 6.5% to 11.3%, with females continuously exhibiting a higher prevalence in comparison to males. Therefore, with this boost in beverage intake, there is a huge growth opportunity for the market across different nations.

Key Dairy Packaging Market Insights Summary:

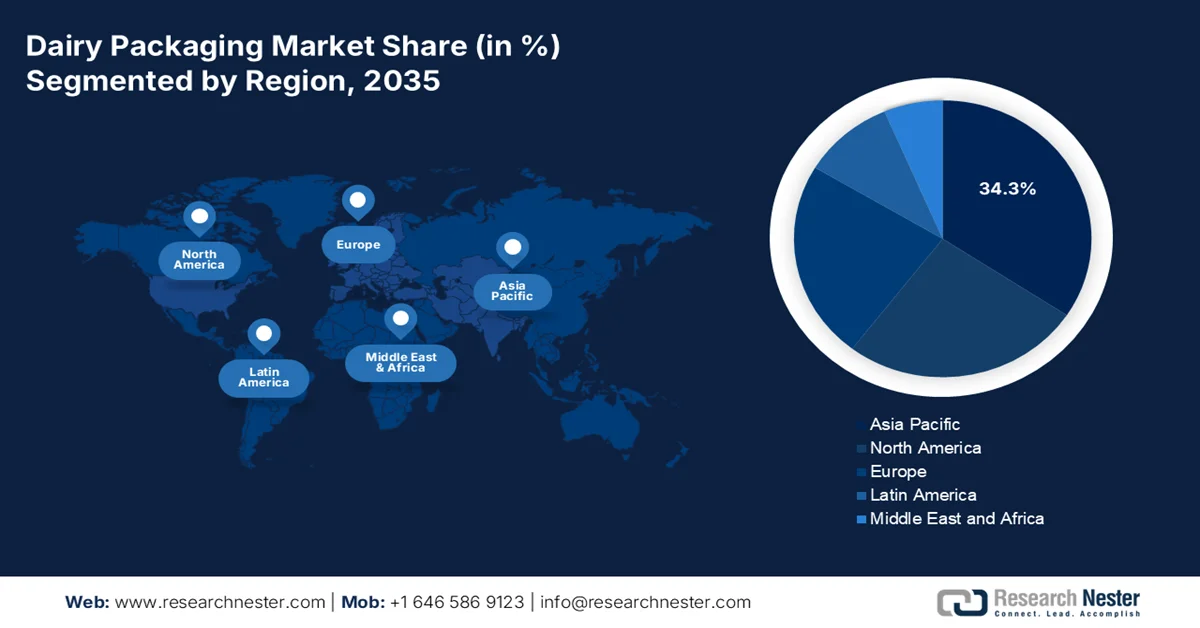

Regional Highlights:

- Asia Pacific is projected to command a leading 34.3% share of the dairy Packaging market by 2035, driven by expanding middle-class populations, rapid urbanization, and accelerated retail and cold chain infrastructure development.

- Europe is anticipated to register the fastest growth during the forecast period 2026–2035, fueled by stringent sustainability regulations and rising demand for advanced barrier materials and convenient dairy formats.

Segment Insights:

- In the dairy Packaging market, the plastic sub-segment under material is expected to capture a dominant 43.8% share by 2035, propelled by its ability to extend shelf life while offering lightweight, cost-efficient, and durable product protection.

- By 2035, the rigid packaging segment is projected to hold the third-largest share, attributed to its structural strength and superior protection for liquid and processed dairy products across complex supply chains.

Key Growth Trends:

- Increase in protein powerhouse demand

- Integration of new packaging strategies

Major Challenges:

- Intense market competition and margin pressure

- Technology integration and digital transformation hurdles

Key Players: Tetra Pak International SA, Amcor plc, SIG Combibloc Group AG, Elopak AS, Sonoco Products Company, Berry Global Inc., Mondi Group, Pactiv Evergreen Inc., Sealed Air Corporation, Huhtamaki Oyj, Greatview Aseptic Packaging Co., Ltd., Stora Enso Oyj, Nippon Paper Group, International Paper Company, DS Smith plc, Smurfit Westrock, Constantia Flexibles Group GmbH, ProAmpac, Serac Group, Pact Group Holdings Ltd.

Global Dairy Packaging Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 24 billion

- 2026 Market Size: USD 25.2 Billion

- Projected Market Size: USD 38.2 billion by 2035

- Growth Forecasts: 5.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (34.3% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, Germany, France, India

- Emerging Countries: Poland, Netherlands, Italy, Brazil, South Korea

Last updated on : 3 March, 2026

Dairy Packaging Market - Growth Drivers and Challenges

Growth Drivers

- Increase in protein powerhouse demand: The enduring worldwide focus on protein consumption, especially complete proteins from dairy sources, is significantly uplifting the need for specialized packaging formats, which is positively impacting the dairy packaging market. According to official statistics published by the Journal of Dairy Science in November 2025, milk is readily added to gain a protein concentration of 90 mg/mL, and the 2.2-diphenyl-1-picrylhydrazyl free radical scavenging capacity of the coffee-milk system increased from 33.5% to 49.3%. Besides, an upsurge in milk protein concentration has been observed in the enhanced foam extension rate, which is accompanied by a slight reduction in foam stability, thereby making it suitable for bolstering the market exposure.

- Integration of new packaging strategies: The growing prioritization of mental wellness is fueling the adoption of aptogens, functional ingredients, and nootropics in dairy products, which is altering packaging demands in the market. As stated in an article published by UA Dairy in 2026, the worldwide dairy industry was valued at USD 550.4 billion by the end of 2025 and is further projected to increase to USD 720.6 billion by the end of 2035. The growth rate over this duration has been predicted to account for 2.7%, denoting an upsurge of over USD 170 billion in the upcoming decade. Therefore, with this ongoing development in the industry, there is a huge demand for different and sustainable packaging methods.

- Focus on plant-based packaging: The maturation of plant-based dairy alternatives from imitation to suitable nutrition is positively uplifting packaging advancement, which is specific to the growing market globally. As per an article published by NLM in January 2026, the growth rate of the plant-based milk industry as of 2022 was 7.9% and is further anticipated to exhibit a 9.9% growth by the end of 2033. Besides, the international industrial size of plant-specific dairy alternatives was worth USD 28.5 billion in 2023, and further reached USD 32.3 billion by the end of 2025. Moreover, the nutritional profile of the finalized dairy alternatives depends on plant-based treatment methods, such as soybeans, which are fermented for a short time, thus denoting a 28.5% increase in the overall phenolics.

Challenges

- Intense market competition and margin pressure: The dairy packaging market is characterized by intense competitive dynamics that compress profit margins and challenge sustainable business models for all but the largest players. The market is highly competitive and moderately fragmented, with established multinational corporations and specialized regional players vying for market share across diverse geographic markets and application segments. Besides, Tetra Pak, Amcor, SIG Combibloc, and other industry leaders have leveraged economies of scale, extensive R&D capabilities, and global customer relationships to maintain dominant positions, creating substantial barriers for smaller competitors in the market.

- Technology integration and digital transformation hurdles: The integration of smart technologies and digital solutions into the market represents a significant opportunity that simultaneously poses formidable implementation challenges for manufacturers. Intelligent packaging systems capable of monitoring freshness, tracking conditions in transit, or providing consumer engagement through QR codes and RFID tags require substantial investment in both hardware capabilities and software infrastructure. For traditional packaging manufacturers whose core competencies lie in material science and converting processes, building digital expertise demands new talent, new partnerships, and new business models that extend far beyond established operations.

Dairy Packaging Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.3% |

|

Base Year Market Size (2025) |

USD 24 billion |

|

Forecast Year Market Size (2035) |

USD 38.2 billion |

|

Regional Scope |

|

Dairy Packaging Market Segmentation:

Material Segment Analysis

The plastic sub-segment, which is part of the material segment, is anticipated to garner the largest share of 43.8% in the dairy packaging market by the end of 2035. The sub-segment’s upliftment is highly propelled by expanding shelf life, providing affordable, lightweight, and durable solutions, as well as ensuring product safety. According to official statistics published by NLM in August 2023, plastic particles that are smaller than 5 mm in diameter are considered microplastics, and those that are less than 1 μm in diameter are nanoparticles. Besides, nanoparticles are frequently referred to as particles of size less than 100 nm, while particles of sizes ranging from 100 nm to almost 1 μm are known as small microplastics. Additionally, nanoparticles constitute a large volume ratio and a specific surface area that are reactive with organic natter and natural solids, thus fueling the sub-segment’s growth.

Packaging Format Segment Analysis

By the end of the stipulated timeline, the rigid packaging segment, part of the packaging format, is projected to hold the third-largest share in the market. The segment’s growth is highly fueled by its structural integrity, superior product protection, and established consumer familiarity. This packaging format encompasses non-flexible containers, including bottles, jars, cups, tubs, and cartons, that maintain their shape when filled and during handling, providing essential crush resistance for dairy products throughout complex supply chains. The segment's leadership position is driven by the material requirements of specific dairy categories, such as liquid milk, which predominantly utilizes rigid HDPE bottles and gable-top cartons, while yogurt, fresh cheese, butter, and ice cream rely on thermoformed plastic cups and tubs that preserve product texture and prevent deformation during refrigerated transport and retail display.

Application Segment Analysis

The milk sub-segment in the market is expected to account for the third-largest share by the end of the stipulated timeline. The sub-segment’s development is highly propelled by offering protection to the highly perishable dairy product from oxygen, contamination, and light, along with extending shelf life and ensuring safety. As stated in an article published by OECD in July 2025, the worldwide milk production is expected to grow at 1.8% per annum in the upcoming decade. This comprises 81% of cow milk, 15% of buffalo milk, and 4% of combined camel, sheep, and goat milk. In addition, this growth is effectively driven by an increase in yields per animal, with a surge in number of cows projected to be moderate. Therefore, with this projected upsurge, there is a huge growth opportunity for the sub-segment globally.

Our in-depth analysis of the market includes the following segments:

|

Segment |

Subsegments |

|

Material |

|

|

Packaging Format |

|

|

Application |

|

|

Sustainability |

|

|

Packaging Type |

|

|

Technology |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Dairy Packaging Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the dairy packaging market is anticipated to garner the highest share of 34.3% by the end of 2035. The market’s upliftment in the region is primarily attributed to expansion in middle-class populations, rapid urbanization, cold chain extension, sustainability transformation, and growing retail infrastructure across emerging economies. For instance, according to an article published by the Journal of Cleaner Production in April 2024, packaging in India is considered the fifth largest economic industry, which has rapidly grown at a 26.7% growth rate by the end of 2025. In addition, the packaging industry’s valuation in the country was worth USD 240.8 billion by the end of the same year. Therefore, with such growth in the packaging sector, the overall market is deliberately growing in the region.

The dairy packaging market in China is growing significantly, owing to the presence of the largest dairy processing industry, strong urbanization, expansion in the middle-class population, and the adoption of sustainable packaging solutions. As stated in an article published by the Journal of Agriculture and Food Research in March 2026, over the past 4 years, the per capita dairy consumption in the country has increased by almost 40 times. In addition, the share of milk produced by industrialized farms has surged from 16% to nearly 75% at present. Besides, the dairy farming trend in the country is emerging to be stronger across the low- and middle-income population, wherein the yearly growth rates of dairy and meat consumption have reached 3.6% and 5.1%, which is about twice the international average, thereby making it suitable for bolstering the market expansion.

The expansion in the dairy industry, packaged penetration, infrastructure modernization, generous fund allocation, and an increase in sustainable materials are certain factors that are responsible for boosting the market in India. According to an article published by the PIB Government in September 2025, dairy is considered the largest agricultural product in the country, significantly contributing 5% to the domestic economy. The industry has not only employed over 80 million farmers but has also touched more than rural households. Besides, there has been a rise in milk production by 63.5% from 146.3 million tons to 239.3 million tons by the end of 2024. This denotes that the country has significantly maintained an outstanding yearly growth rate of 5.7% over the past 10 years, thereby positively impacting the market expansion.

Europe Market Insights

Europe in the dairy packaging market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by strict sustainability regulations, technological advancements in barrier materials, and modified consumer preferences for on-the-go and convenient dairy formats. According to official statistics published by the Foreign Agricultural Services in December 2025, the 2026 cheese production in the region is expected to reach 10.8 million metric tons, denoting a rise by 0.2% from 2025. Besides, as per the June 2025 Europe Commission article, the main milk producers in the region are Poland, the Netherlands, France, Germany, Ireland, and Italy, altogether accounting for over 70% of regional milk production. Additionally, there have been 20 million cows in the region as of 2023, with an average of 7,800 kg of milk produced by each cow, thus bolstering the market expansion in the market.

The dairy packaging market in the UK is gaining increased traction, owing to the post-Brexit regulatory alignment with regional sustainability standards, the provision of a budget for dairy packaging strategies, a flexible packaging fund, and a commitment to reusability and recycling. As per a data report published by the UK Dairy Organization in November 2024, milk and dairy foods in the UK are an essential source of nutrition for young children aged between 1.5 and 3 years. Besides, the latest National Diet and Nutrition Survey has demonstrated that milk and milk-based products contributed 31% of protein, 59% of calcium, 64% of iodine, 54% of vitamin B2, 30% of potassium, 35% of vitamin A, 30% of vitamin D, and 35% of zinc. Moreover, for the 18-year-old population, these milk products contribute 40% of iodine, 29% of vitamin B2, and 34% of calcium, thereby fueling the market demand in the country.

The aspects of strong industrial capabilities, robust sustainability targets, and engineering excellence, along with generous investment through the federal government, are certain factors that are proliferating the market in Germany. As per an article published by NLM in April 2022, the country is regarded as the largest milk producer in the whole of Europe, with an output of an estimated 33 million tons of milk. In addition, almost half of the produced quantity has been exported, demonstrating a production value of over USD 11.8 billion. Besides, as per the January 2025 Europe Investment Bank article, Gropper, which is the country’s dairy company, significantly sources its raw milk from 780 dairy farmers within a radius of nearly 160 kilometers. Moreover, the region’s financing arm generously invested USD 57.9 million in September 2024 in Gropper to ensure modernization, thus driving the market expansion.

North America Market Insights

North America in the dairy packaging market is projected to witness moderate growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by sustainability transformation, convenience and on-the-go consumption, technological advancements, as well as supply chain and retail dynamics. Based on government estimates published by the USDA in May 2025, the administrative organization invested USD 3.1 billion for 141 selected projects under the partnership for climate-smart commodities. Besides, as stated in an article published by NLM in October 2025, the AI industry for personalized nutrition is gradually growing by over 23% every year, with the region emerging as the leader as of 2023. Additionally, 41% of the population currently own smartwatch, and almost 4 in 10 health application users track their diet, thus boosting the market exposure in the region.

The dairy packaging market in the U.S. is growing significantly, owing to generous federal budget allocation for packaging strategies, advanced manufacturing technologies for packaging material production, and an increased focus on recycled infrastructure. According to official statistics published by the USDA in March 2022, the milk production amount in the country surged by 1.5% growth rate, with dairy farms producing 18,197 pounds of milk per cow. This further increased to 23,777 pounds, which is positively impacting the market growth. Meanwhile, there has also been an increase in the national herd size from 9,199,000 to 9,388,000, denoting a yearly 0.10% growth rate. Besides, the productivity among dairy farms has been comprehensive, particularly across California, Arizona, New Mexico, and Idaho, accounting for 4.4% and 3.5% growth rate, thereby making it suitable for bolstering the market in the overall country.

The surge in the demand for health-focused and plant-based dairy alternatives, circular economy imperatives, sustainability transformation, on-the-go consumption patterns, convenience culture, governmental funding opportunities, and technological innovation in packaging are enhancing the market in Canada. As per an article published by the Government of Canada in July 2023, there has been the provision of more than USD 7.5 million to Dairy Farmers of Canada (DFC) to assist in supporting sustainable development in the dairy sector. This particular funding has been provided through the AgriScience Program-Clusters Component, under the Sustainable Canadian Agricultural Partnership. Moreover, the government has also declared compensatory payment for dairy producers under the Dairy Direct Payment Program (DDPP), with a total of USD 1.75 billion in compensation, thus driving the market growth.

Key Dairy Packaging Market Players:

- Tetra Pak International SA (Sweden/Switzerland)

- Amcor plc (UK/Switzerland)

- SIG Combibloc Group AG (Switzerland)

- Elopak AS (Norway)

- Sonoco Products Company (U.S.)

- Berry Global Inc. (U.S.)

- Mondi Group (UK)

- Pactiv Evergreen Inc. (U.S.)

- Sealed Air Corporation (U.S.)

- Huhtamaki Oyj (Finland)

- Greatview Aseptic Packaging Co., Ltd. (China)

- Stora Enso Oyj (Finland)

- Nippon Paper Group (Japan)

- International Paper Company (U.S.)

- DS Smith plc (UK)

- Smurfit Westrock (Ireland/U.S.)

- Constantia Flexibles Group GmbH (Austria)

- ProAmpac (U.S.)

- Serac Group (France)

- Pact Group Holdings Ltd (Australia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Tetra Pak International SA dominates the dairy packaging sector, highly driven by its pioneering aseptic carton technology that extends shelf life for milk and dairy products without preservatives. The company recently strengthened its market position by introducing India's first beverage carton with recycled polymer content and earning the Resource Efficiency award for its paper-based barrier material innovation.

- Amcor plc has solidified its dairy packaging leadership through its largest-ever investment in North American dairy production capacity, enabling the rollout of AmPrima recycle-ready films for cheese and dairy applications. The company's collaboration with Fonterra to replace non-recyclable multi-material laminates with mono-material polyethylene film is expected to remove non-recyclable material annually from the Australia-based dairy market.

- SIG Combibloc Group AG is aggressively expanding in the world's largest dairy market with a €90 million aseptic carton plant in Ahmedabad, India, targeting the vast milk sector where the majority of its global packaging business is derived from dairy applications. The company's aseptic solutions address India's cold chain challenges by enabling milk packaging that requires no refrigeration, with plans for an extrusion line by the end of 2027.

- Elopak AS is rapidly scaling its U.S. presence with a $100 million manufacturing facility in Arkansas, capitalizing on the market penetration of cartons in American dairy versus Europe. The company has already commissioned a second production line for early 2026 and announced a third line for 2027, responding to strong demand as dairies seek supply diversification following competitor closures.

- Sonoco Products Company enhances dairy packaging through its advanced in-mold labelling (IML) technology at expanded German facilities, creating visually appealing, fully recyclable plastic containers specifically designed for yogurt, butter, and other dairy products. The company's investment in Zwenkau includes PermaSafe technology that rivals metal cans in oxygen barrier protection while offering resealable convenience for shelf-stable dairy applications.

Here is a list of key players operating in the global market:

The global dairy packaging market is highly competitive and moderately fragmented, characterized by the presence of established multinational corporations and specialized regional players. Market leadership is primarily determined by a company's ability to innovate in material science, particularly in developing sustainable and recyclable solutions such as bio-based polymers, lightweight materials, and fully recyclable aseptic cartons. Key players such as Tetra Pak, Amcor, and SIG Combibloc dominate through continuous investment in research and development, focusing on extending product shelf life and enhancing barrier properties. Besides, in April 2025, ProAmpac expanded its dairy packaging portfolio with high-performance butter wraps. This readily includes foil-paper-based options and butter fresh parchment, which has been designed to protect margarine, butter, and other oil-specific solid products to provide superior grease resistance and excellent dead-fold properties to minimize air exposure and maintain freshness, thus fueling the dairy packaging industry.

Corporate Landscape of the Dairy Packaging Market:

Recent Developments

- In February 2026, Tetra Pak undertook a suitable step in sustainable packaging by extending its advanced paper-based barrier technology to high-speed Tetra Pak A3/Speed filling lines, with Maeil Dairies emerging as the very first producer worldwide by integrating the solution for its soy milk product.

- In August 2025, INEOS Styrolution has introduced its newest circular packaging breakthrough, which comprises sour cream cups that are made with 30% recycled polystyrene and are available in ALDI SÜD stores across Germany.

- In June 2025, Vinamilk introduced its science-driven innovation strategy that demonstrated its advancement to enhance and preserve the natural value of dairy, while catering to the diversified health and nutrition demands.

- Report ID: 8411

- Published Date: Mar 03, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.