Dairy Packaging Solutions Market Outlook:

Dairy Packaging Solutions Market size was valued at USD 37.2 billion in 2025 and is projected to reach USD 63.6 billion by the end of 2035, rising at a CAGR of 5.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of dairy packaging solutions is estimated at USD 39.2 billion.

The global dairy packaging solutions market is structurally linked to the sustained global milk production, rising processed dairy output, and tightening food safety and waste regulations. According to the FAO June 2023 data, the global milk production reached 944 million tons in 2023, reflecting continued expansion across Asia and steady output in Europe and North America. India remains the largest milk producer and is supported by the cooperative procurement systems and cold chain expansion. The U.S. dairy processing industry reinforces the ongoing demand for rigid plastic bottles, laminated cartons, flexible pouches, and bulk transport formats. Moreover, the Eurostat November 2024 data depict that the EU collected over 160 million tons of raw milk in 2023, with Germany, France, and the Netherlands as the leading contributors. These production volumes directly translate into recurring procurement cycles for food-grade plastics, paperboard cartons, aluminum foils, and multilayer barrier materials.

World Dairy Market Trade, 2023

|

|

2021 |

2022 |

2023 |

Change: 2023 over 2022 |

|

Total milk production |

931.1 |

935.9 |

944.0 |

0.9 |

|

Total trade |

88.6 |

84.6 |

85.0 |

0.5 |

Source: FAO June

Moreover, the regulatory compliance and the sustainability mandates are materially influencing the procurement strategies across the dairy processors. The U.S. EPA October 2025 data depicts that the containers and packaging accounted for 82.2 million tons of municipal solid waste generation, representing 28.1% of total waste, driving recycling and material recovery targets across food sectors. On the other the U.S. Food and Drug Administration enforce food-contact material compliance affecting resin selection and multilayer structures used in dairy applications. These regulatory pressures, combined with cold-chain expansion in emerging markets supported by multilateral institutions, are sustaining institutional demand for compliant, lightweight, and recyclable dairy packaging formats across fluid and value-added dairy segments.

Key Dairy Packaging Solutions Market Insights Summary:

Regional Highlights:

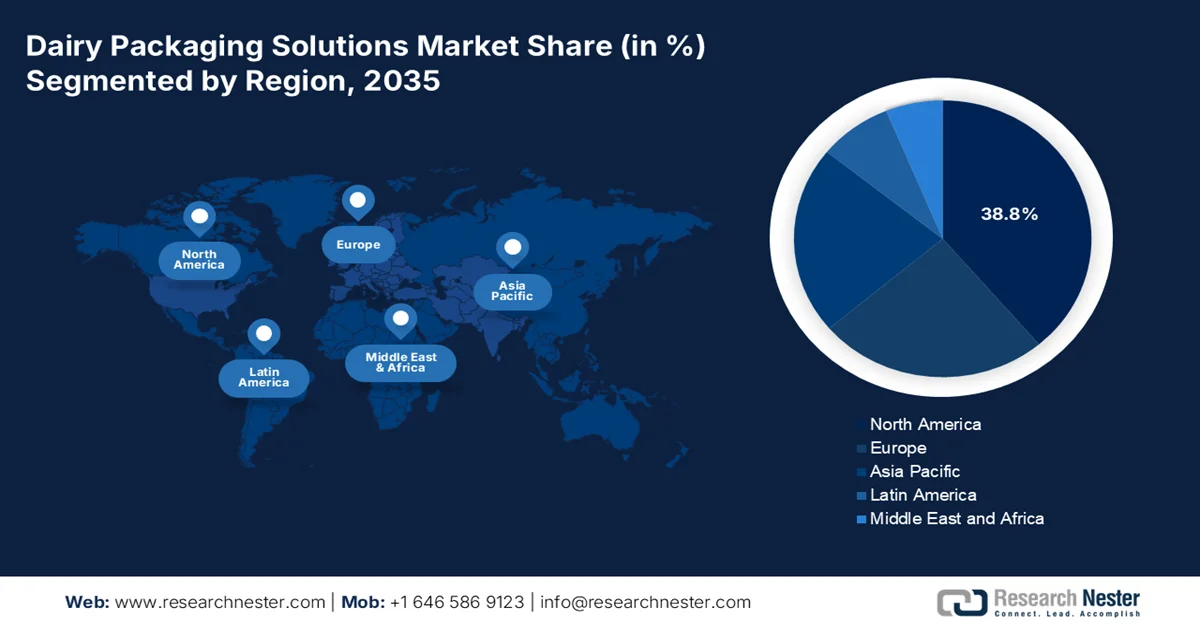

- North America dairy packaging solutions market is anticipated to capture a 38.8% share by 2035, impelled by stringent food safety regulations and rising adoption of recyclable packaging solutions

- Asia Pacific is projected to expand at a CAGR of 4.1% during 2026-2035, stimulated by rapid urbanization and shifting consumer preference toward packaged dairy products

Segment Insights:

- Primary Packaging segment in the dairy packaging solutions market is forecasted to hold a 70.4% share by 2035, driven by its essential role as the fundamental packaging layer for every dairy product unit

- Aseptic Packaging segment is expected to secure a 65.4% share by 2035, propelled by extended shelf life benefits and enhanced supply chain efficiency without refrigeration

Key Growth Trends:

- Cold chain investment

- Food safety and compliance spending

Major Challenges:

- High capital investment for aseptic technology

- Complex regulatory compliance

Key Players: Tetra Pak, Amcor plc, SIG Combibloc Group AG, Greatview Aseptic Packaging Co. Ltd., Elopak AS, Sealed Air Corporation, Berry Global Group Inc., Sonoco Products Company, WestRock Company, International Paper Company, Mondi plc, Huhtamäki Oyj, Constantia Flexibles Group GmbH, Winpak Ltd., Nippon Paper Industries Co., Ltd., DS Smith Plc, Uflex Ltd., KP Tissue Inc. / Kruger Products Inc., ProAmpac, Huhtamak.

Global Dairy Packaging Solutions Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 37.2 billion

- 2026 Market Size: USD 39.2 billion

- Projected Market Size: USD 63.6 billion by 2035

- Growth Forecasts: 5.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, France

- Emerging Countries: India, Brazil, Indonesia, Mexico, Vietnam

Last updated on : 6 April, 2026

Dairy Packaging Solutions Market - Growth Drivers and Challenges

Growth Drivers

- Cold chain investment: Public investment in cold chain logistics directly increases the demand for the dairy packaging solutions market. According to the PIB August 2025 data, India’s Ministry of Food Processing Industries approved 52 cold chain projects under PMKSY, strengthening the refrigerated storage and transport capacity. Moreover, the investment in the agricultural value chain financing across South Asia and Africa, including cold chain modernization. Further, the expanded refrigeration networks extend dairy distribution radii, requiring high-performance multilayer films, aseptic cartons, and tamper-evident closures. Packaging manufacturers positioned in regions receiving infrastructure capital can align supply contracts with new processing clusters and integrated dairy parks.

- Food safety and compliance spending: Heightened enforcement of food contact standards is increasing the demand for certified packaging materials. According to the FDA April 2021 data, food contact substances are regulated under 21 CFR 175-178, affecting polymer selection and additive use. Moreover, the FDA 2026 data shows that the budget reached USD 6.8 billion, with food safety modernization as a core spending area. Further, the compliance pressures are accelerating transitions toward traceable, migration-tested, and recyclable dairy packaging solutions market. Suppliers that invest in regulatory documentation, recycled-content validation, and audit readiness gain preferred-vendor status in large dairy cooperatives and multinational processors. Additionally, the implementation of the FDA Food Safety Modernization Act's preventive controls requirements is compelling dairy processors to strengthen supplier verification programs.

- Public health campaigns promoting dairy consumption: Government-sponsored public health initiatives are promoting dairy consumption, directly expanding the addressable dairy packaging solutions market. The U.S. recommends three daily servings of dairy for individuals. Moreover, the funds for research on dairy’s role in bone health and chronic disease prevention reinforce the dairy in nutrition education materials distributed via the supplemental nutrition program for women, infants, and children. These sustained public health campaigns maintain consumer awareness and consumption levels, supporting the packaging demand. Additionally, federally funded school milk programs and community nutrition outreach initiatives ensure recurring institutional dairy purchases, thereby sustaining steady volume requirements for portion-controlled and bulk dairy packaging formats.

Challenges

- High capital investment for aseptic technology: Entering the premium segment of the dairy packaging solutions market requires massive capital expenditure, mainly for the aseptic filling lines. Moreover, the single filling machine costs in millions. This financial barrier prevents smaller players from competing in the high-margin market, and new entrants face daunting startup costs that favor competitors who have decades of depreciation on their equipment. The break-even period often exceeds years, deterring venture capital.

- Complex regulatory compliance: Navigating global food contact regulations presents a challenge for the new market entrants. The dairy packaging solutions market requires materials that maintain sterility while preventing chemical migration into fatty dairy products. In Europe, new manufacturers must comply with the EU’s packaging and packaging waste regulation that most plastic packaging be designed for recyclability. Top companies address this by producing high-purity recycled plastic that meets the food contact standards.

Dairy Packaging Solutions Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.5% |

|

Base Year Market Size (2025) |

USD 37.2 billion |

|

Forecast Year Market Size (2035) |

USD 63.6 billion |

|

Regional Scope |

|

Dairy Packaging Solutions Market Segmentation:

Packaging Format Segment Analysis

Within the packaging format segment, the primary packaging sub-segment is dominating and is projected to hold the largest share value of 70.4% by the end of 2035 in the dairy packaging solutions market. The segment is dominating as it is the most essential and irreplaceable layer in the packaging hierarchy. Unlike the other sub-segments, such as the secondary and tertiary formats used for transport and display, the primary packaging is required for every single unit of dairy product sold, creating an immense volume-driven market. According to the IDFA September 2022 data, the per capita consumption of dairy products by the U.S. people grew by 12.4 pounds per person, all of which required the primary cup or tub packaging. This data indicates the massive, consistent demand driving the primary packaging segment.

Technology Segment Analysis

Under the technology segment, the aseptic packaging is leading and is poised to hold the share value of 65.4% by the end of 2035 in the dairy packaging solutions market. This technology involves filling sterilized dairy products into pre-sterilized containers within a sterile environment, effectively locking in freshness and nutritional value for months without refrigeration. The dominance of aseptic packaging is driven by the global supply chain efficiencies and the reduction of food waste, mainly in warm climates where cold chain logistics are challenging or expensive. Modern aseptic systems now utilize multi-layer barrier structures that protect light-sensitive dairy nutrients such as riboflavin while eliminating the need for preservatives. Moreover, the ambient stability is the single most important factor driving its adoption among multinational dairy corporations seeking to expand into emerging markets.

Material Type Segment Analysis

The paper and paperboard are projected to hold the largest share value in the material segment. This surge is a direct response to the global regulatory crackdown on single-use plastics and the dairy industry’s commitment to the circular economy principles. The modern paperboard packaging for dairy is no longer a simple carton. It involves advanced high-barrier coating derived from biopolymers that replace the traditional aluminum and polyethylene layers while maintaining the structural integrity required for aseptic storage. Liquid carton board is designed for milk and juice offers superior printability for brand differentiation and is manufactured from renewable wood fibers sourced from sustainably managed forests. As per the EPA October 2025, the overall generation of paper and paperboard in MSW was 67.4 million tons. Recycling rates further strengthen paperboard's sustainable market dominance.

Our in-depth analysis of the dairy packaging solutions market includes the following segments:

|

Segment |

Subsegments |

|

Material Type |

|

|

Packaging Type |

|

|

Application |

|

|

Packaging Format |

|

|

Technology |

|

|

Fill Capacity |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Dairy Packaging Solutions Market - Regional Analysis

North America Market Insights

North America is dominating and is projected to hold the largest regional revenue share of 38.8% by the end of 2035 in the dairy packaging solutions market. The dairy packaging solutions market in North America is driven by the stringent food safety regulations mandating tamper-evident and traceable packaging solutions for fluid milk and cheese products. The government investment in recycling infrastructure, mainly via the U.S. EPA National Recycling Strategy are surging the transition toward recyclable mono material structures. The Canada government's enforcement of the single-use plastics prohibition regulations drives the demand for paper-based alternatives. Further, the established cold chain networks support aseptic and extended shelf life packaging adoption. Consolidation among dairy processors creates demand for standardized, high-volume packaging formats compatible with automated filling lines.

The regulatory compliance-driven innovation and material substitution toward recyclable formats are fueling the dairy packaging solutions market in the U.S. According to the EPA, October 2025 data, the containers and packaging achieved a 53.9% recycling rate, while 30.5 million tons were landfilled and 7.4 million tons were combusted with energy recovery, underscoring regulatory and sustainability pressure on packaging-intensive sectors such as dairy. Further, the Glass container generation reached 9.8 million tons, representing 3.3% of total MSW, while paper and paperboard packaging, including milk cartons and aseptic beverage cartons, accounted for 41.9 million tons (14.3% of total MSW generation). These recovery gaps are accelerating investments in recyclable mono-material HDPE milk bottles, improved carton recovery infrastructure, and recycled-content integration. As sustainability targets tighten under federal and state waste reduction frameworks, U.S. dairy processors are increasingly transitioning toward packaging formats aligned with higher recovery rates, supporting material innovation and replacement-driven market growth.

A stable and high-volume base for packaging demand is driving the dairy packaging solutions market in Canada. According to the Government of Canada's January 2026 report, 96.61 million hectoliters of milk were produced in 2023/24, including 26.9 million hl of fluid milk and 69.6 million hl of industrial milk. With 549 dairy processing plants generating USD 19.3 billion in manufacturing shipments, packaging requirements span HDPE milk bottles, laminated paperboard cartons, flexible milk bags, cheese films, yogurt cups, butter wraps, and bulk powder sacks. Product output, including 500.1 thousand tons of cheese, 387.3 thousand tons of yogurt, 112.8 thousand tons of butter, and 85.1 thousand tons of skim milk powder, creates sustained primary and secondary packaging volumes. Canada’s regulated supply management system provides predictable production flows, reinforcing the long-term packaging procurement stability.

Canada’s Dairy Farm and Processing Sector (2023-2024)

|

Category |

Indicator |

Value |

|

Farm Sector |

Total Net Farm Cash Receipts (Dairying) |

USD 8.88 billion |

|

Dairy Cattle Population (Cows & Heifers) |

1.375 million head (July 1, 2024) |

|

|

Number of Dairy Farms |

9,256 (August 1, 2024) |

|

|

Total Milk Production |

96.61 million hectolitres |

|

|

Organic Milk Production |

1.54 million hectolitres (2023/24) |

|

|

Processing Sector |

Dairy Manufacturing Shipments |

USD 19.3 billion |

|

Number of Dairy Processing Plants |

549 plants |

Source: Government of Canada, 2026

APAC Market Insights

The Asia Pacific is the fastest growing and is expected to register a CAGR of 4.1% during the forecast period 2026 to 2035. The dairy packaging solutions market is driven by the rapid transformation by urbanization changing dietary patterns and expanding modern retail infrastructure across the region. Traditional loose milk purchases are progressively being replaced by packaged formats as consumers prioritize food safety and brand reliability. The region encompasses vastly diverse markets at different developmental stages from nature technologically advanced packaging sectors in Japan and South Korea to rapidly modernizing markets in China and Southeast Asia where cold chain infrastructure is expanding to support fresh dairy distribution. Regulatory harmonization efforts and other regional bodies facilitate cross border dairy trade creating a demand for dairy packaging solutions market in Asia Pacific compliant with multiple national standards simultaneously.

The sustained structural expansion in milk production and the organized procurement are driving the dairy packaging solutions market in India. As per the PIB August 2025 data, under the National Programme for Dairy Development, 31,908 dairy cooperative societies have been organized or revived, adding 17.63 lakh milk producers and increasing milk procurement by 120.68 lakh kg per day. Moreover, the government has approved USD 4.47 million to organize 21,902 new dairy cooperative societies, further strengthening formal supply chains. National milk production increased by 63.56% to 239.30 million tons, reflecting a 5.7% annual growth rate, reinforcing India’s position as the world’s largest milk producer. Overall, the market is accelerating toward recyclable mono-material dairy packaging and compliance-driven material optimization across processors.

The steady raw milk expansion, processing scale-up, and tightening environmental compliance are scaling the demand for the dairy packaging solutions market in China. According to the USDA April 2024 data, the national raw milk production reached 41.97 million tons, reflecting continued capacity growth in large-scale dairy farming. The Ministry of Agriculture and Rural Affairs reported that dairy farming modernization and standardized scale operations continued to expand, strengthening organized milk collection and cold-chain integration. On the other hand, environmental compliance is influencing material selection. China’s Ministry of Ecology and Environment reported ongoing implementation of plastic pollution control measures under the 14th Five-Year Plan, accelerating recyclable and reduced-plastic packaging adoption (mee.gov.cn). According to the Earth.Org data in June 2023, 60 million tons of plastic waste were generated, and China’s dairy processors are increasingly investing in aseptic cartons, recyclable HDPE bottles, and high-barrier flexible packaging to align with food safety and sustainability mandates.

Europe Market Insights

The dairy packaging solutions market in Europe is expanding significantly and is driven by the stringent regulatory frameworks mandating recyclability and recycled content across member states. Rigorous food contact material standards require migration testing for the dairy applications, favoring top suppliers with the regulatory expertise. According to the Eurostat October 2023 data, nearly 84 million tons of packaging waste are generated. Moreover, the European medicines agency oversight extends to pharmaceutical-grade dairy ingredients requiring specialized sterile packaging. Further, the funds for the circular economy projects, including the dairy packaging recycling infrastructure, are driving the growth of the market. Cross-border sustainability targets reinforce long-term packaging compliance investments.

The UK dairy sector provides a substantial foundation for demand for the dairy packaging solutions market in the UK. According to the Dairy UK 2025 data, 10,400 active dairy farmers produce nearly 15 billion litres of milk annually and dairy products valued at £5.7 billion at the wholesale level. High fluid milk volumes sustain demand for HDPE bottles and paperboard cartons while value-added segments support flexible films, tubs, and foil laminates. On the other hand, the Government of UK July 2025 report depicts that the UK packaging waste accounts for 2,265 thousand tons of plastic packaging waste arising, with 1,154 thousand tons recycled, achieving a 51% recycling rate. This regulatory and recovery performance environment is driving dairy processors toward higher recycled content integration and improved material traceability. As Extended Producer Responsibility obligations tighten, the UK dairy packaging suppliers are increasingly prioritizing recyclable mono material plastics and compliant labeling to maintain long term supply contracts.

The dairy packaging solutions market in Germany operates within the strict legal framework under the Packaging Act. According to the bundesumweltministeriumdrinks data from March 2023, the packaging for the liquid foodstuffs is regulated in alignment with Regulation 178/2002 on food safety. Moreover, Germany has maintained high recycling performance for decades, recycling 56% of its waste as early as 2002, and strengthening targets under the Circular Economy Act to reach a 65% recycling rate, exceeding the EU’s 50% minimum target for certain materials according to Earth.Org, in April 2022. Further, the dairy companies procuring milk from 780 farmers within a 160 km radius under multi-year contracts ensure predictable production flows. This supply stability supports long-term packaging procurement planning, particularly for regionally distributed fluid milk packaged under Germany’s deposit-return and recycling compliance systems.

Key Dairy Packaging Solutions Market Players:

- Tetra Pak (Sweden)

- Amcor plc (Switzerland)

- SIG Combibloc Group AG (Switzerland)

- Greatview Aseptic Packaging Co. Ltd. (China)

- Elopak AS (Norway)

- Sealed Air Corporation (U.S.)

- Berry Global Group Inc. (U.S.)

- Sonoco Products Company (U.S.)

- WestRock Company (U.S.)

- International Paper Company (U.S.)

- Mondi plc (UK)

- Huhtamäki Oyj (Finland)

- Constantia Flexibles Group GmbH (Austria)

- Winpak Ltd. (Canada)

- Nippon Paper Industries Co., Ltd. (Japan)

- DS Smith Plc (UK)

- Uflex Ltd. (India)

- KP Tissue Inc. / Kruger Products Inc. (Canada)

- ProAmpac (U.S.)

- Huhtamak (Finland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Tetra Pak leverages its integrated approach to provide complete processing and packaging solutions. The company is actively advancing its sustainability agenda, launching aseptic cartons with the paper based barriers and plant-based polymers to reduce the carbon footprint. Strategic initiatives focus on enhancing the recycling infrastructure globally and developing digital solutions for supply chain traceability. In 2024 the company has a made an investment of USD 45.8 million to support collection sorting and recycling packages.

- Greatview Aseptic Packaging Co., Ltd has captured a significant share in the dairy packaging solutions market by offering cost effective high quality alternatives to the European giants. Their primary strategic initiative involves aggressive geographic expansion into emerging markets across Asia, Africa, and the Middle East, where dairy consumption is high.

- Berry Global Group Inc. is a dominant player in the dairy packaging solutions market, using its extensive expertise in rigid plastics and flexible films to serve the dairy industry. The company’s leadership is most evident in the plastic segment, where it provides a vast array of bottles, tubs, and closures for milk, yogurt, and ice cream. Further, the company has advanced by integrating sustainable practices into its dairy offerings.

- Sonoco Products Company has carved out a significant niche in the dairy packaging solutions market mainly via its expertise in spiral wound composite containers and rigid paperboard cartons. The company’s strongest foothold lies within the paper & paperboard segment serving applications such as powdered infant formula milk powder and certain types of grated cheese. According to the 2024 annual report the company has 69% of the total sales in North America.

- WestRock Company is a cornerstone of the dairy packaging solutions market, renowned for its comprehensive portfolio of coated paperboard and folding cartons used extensively in the dairy aisle. The company excels in the cartons sub-segment, supplying gable top cartons for fluid milk and aseptic cartons for shelf-stable creamers, as well as innovative paperboard sleeves and carriers for multipack yogurt cups.

Here is a list of key players operating in the global dairy packaging solutions market:

The competitive landscape of the global dairy packaging solutions market is defined by the dominance of the multinational corporations with extensive R&D capabilities and a trend toward sustainable and aseptic packaging solutions. The key strategic initiatives include mergers and acquisitions to expand geographic footprint, as well as significant investments in lightweight materials and recyclable mono materials to meet the robust environmental regulations and consumer demand for eco-friendly products. For example, in December 2025, ProAmpac acquired TC Transcontinental Packaging from TC Transcontinental. The major players are also focusing on the development of smart packaging technologies to enhance supply chain transparency and consumer engagement. For example, Amcor plc, the leading player in the market has invested USD 17, in R&D to advance the packaging solutions. These strategies are intensifying competition mainly in emerging markets where dairy consumption is rising rapidly.

Corporate Landscape of the Dairy Packaging Solutions Market:

Recent Developments

- In December 2025, Tetra Pak, in collaboration with García Carrión, unveiled the first-ever use of its paper-based barrier technology for juice packaging. This innovation in sustainable food packaging solutions marks a significant step towards reducing reliance on fossil-based materials, with the new packaging material now being rolled out across multiple markets.

- In August 2025, ProAmpac has announced the commercial launch of its ProActive Recycle-Ready polyolefin-based platform engineered specifically for high-speed chunk cheese applications. This launch marks a significant advancement in Recycle-Ready dairy packaging, offering exceptional performance without compromising shelf life and its run time.

- In February 2025, Huhtamak announced the development of the recyclable single coated paper cups ProDairy, specifically designed for yogurt and dairy products. Yogurt is a product with high food safety requirements. This highly functional and innovative packaging solution meets all the requirements and delivers a lower polymer content than traditional alternative products.

- Report ID: 8500

- Published Date: Apr 06, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.