Cold Chain Packaging Market Outlook:

Cold Chain Packaging Market size was valued at USD 34.8 billion in 2025 and is projected to reach USD 103.7 billion by the end of 2035, rising at a CAGR of 12.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of cold chain packaging is estimated at USD 39.2 billion.

The worldwide surging demand for biologics and the international trade of perishables are the main factors responsible for the tremendous growth of the cold chain packaging market. As per an article published by the World Trade Organization (WTO) in 2025, food exports reached a significant value of USD 766 billion from Europe in 2024, underscoring the volume of temperature-sensitive goods moving across borders. The region also led the total agricultural exports, which were valued at USD 861 billion, reflecting strong outbound flows of fresh produce, meat, and dairy products, which necessitate controlled logistics. Meanwhile, Brazil’s food exports were valued at a remarkable USD 136 billion and China's at USD 70 billion in 2024, denoting the presence of a global supply base for perishables. Therefore, from a trade structure perspective, food products are driving a huge reliance on temperature-controlled packaging and handling systems, denoting a lucrative growth opportunity for the cold chain packaging market.

Top Global Exporters of Perishable Food Products in 2024: Export Values in USD Billion

|

Category |

Exporter |

Export Value (USD Billion) |

|

Agricultural Products |

European Union |

861 |

|

U.S. |

176 |

|

|

Brazil |

155 |

|

|

China |

94 |

|

|

Food Products |

European Union |

766 |

|

Brazil |

136 |

|

|

U.S. |

91 |

|

|

China |

70 |

|

|

Canada |

70 |

|

|

Mexico |

53 |

|

|

India |

44 |

|

|

Thailand |

44 |

|

|

Australia |

39 |

Source: WTO

Furthermore, continued trade flows of frozen food products, as well as a heightened focus on sustainability, are certain factors that are efficiently boosting the cold chain packaging market. As per the official statistics published by the Observatory of Economic Complexity (OEC) in 2024, global trade in frozen fruits and nuts surpassed a total of USD 7.5 billion, which marks a 4.5% growth when compared to 2023 and a 7.3% annualized increase over five years. The report also highlighted that Thailand led exports with almost USD 675 million, whereas the U.S. is identified as the largest importer at USD 1.3 billion. In addition, the major by-products in this trade are frozen fruits & nuts, strawberries, raspberries, and mulberries, highlighting strong demand across diverse markets. Therefore, from a strategic perspective, this reflects the presence of insatiable demand for cold chain packaging, encouraging more pioneers to make investments in this field.

Top Exporters, Importers, By-Products, and Growth Potential of Frozen Fruits and Nuts in 2024

|

Metric |

Country / Product |

Value in USD |

|

Top Exporter |

Thailand |

675 million |

|

Poland |

638 million |

|

|

Serbia |

516 million |

|

|

Top Importer |

U.S. |

1.3 billion |

|

China |

931 million |

|

|

Germany |

690 million |

|

|

Major By-product |

NES (Uncooked/Steamed/Boiled, NES) |

4.7 billion |

|

Strawberries (Frozen) |

1.4 billion |

|

|

Raspberries/Mulberries (Frozen) |

1.2 billion |

|

|

Export Dependence |

Grenada |

10.5% |

|

Palestine |

3.8% |

|

|

Serbia |

1.4% |

Source: OEC

Key Cold Chain Packaging Market Insights Summary:

Regional Highlights:

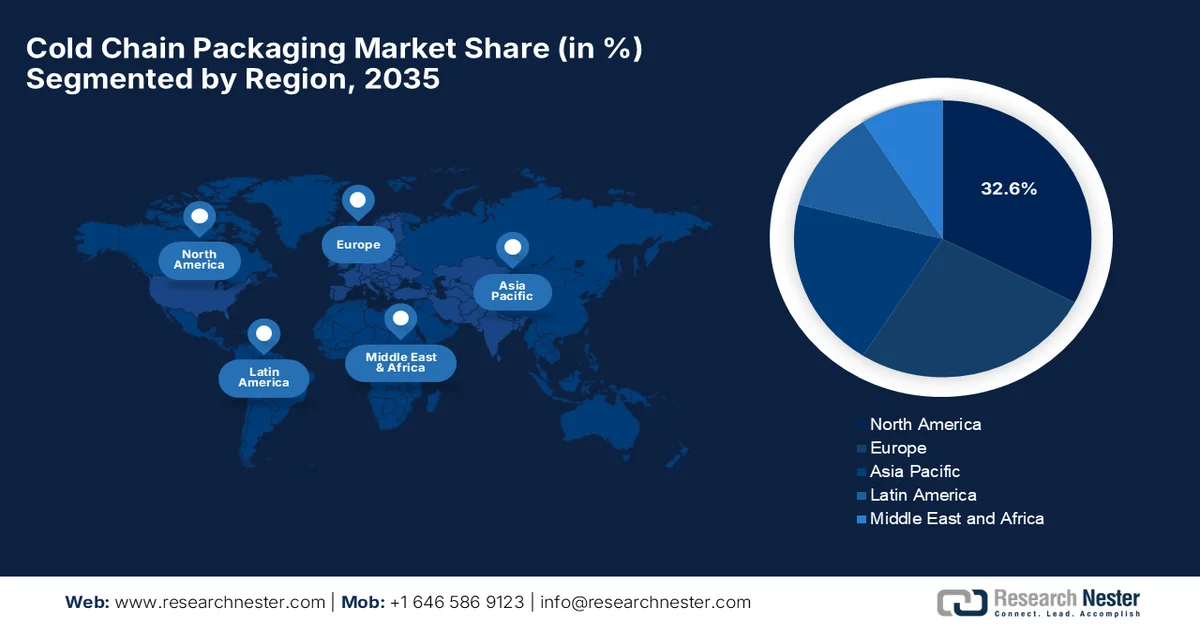

- By 2035, North America in the cold chain packaging market is projected to hold a 32.6% share, attributed to advanced pharmaceutical cold chain infrastructure and supportive regulatory frameworks.

- Across 2026–2035, Asia Pacific cold chain packaging market is anticipated to witness the fastest growth, fueled by rising consumption of fresh and processed food products alongside increasing disposable incomes.

Segment Insights:

- By 2035, insulated materials subsegment in the cold chain packaging market is expected to capture a 66.4% share, propelled by high thermal efficiency, reusability, and compliance with long-duration shipping requirements.

- During 2026–2035, fish, seafood, and meat segment is likely to secure a notable revenue share, impelled by increasing global demand and the need for temperature-controlled logistics to prevent spoilage.

Key Growth Trends:

- Rising demand for temperature‑sensitive pharmaceuticals

- E‑Commerce & last‑mile delivery expansion

Major Challenges:

- Complex regulatory compliance requirements

- Environmental concerns and sustainability pressure

Key Players: Cold Chain Technologies, LLC (U.S.), Sonoco ThermoSafe (U.S.), Cryopak Industries Inc. (U.S.), Sealed Air Corporation (U.S.), CSafe Global LLC (U.S.), TemperPack Technologies, Inc. (U.S.), Inmark LLC (U.S.), Softbox Systems Ltd. (UK), Intelsius (DGP Intelsius LLC) (UK), Sofrigam SA Ltd. (France), EMBALL’ISO (France), va-Q-tec AG (Germany), Envirotainer AB (Sweden), Tower Cold Chain Solutions (UK), Nippon Express (Japan), Cryoport Systems (U.S.), Peli BioThermal (U.S.), BioLife Solutions (U.S.), Maersk (Denmark), Vizient (U.S.), Nordic Cold Chain Solutions (U.S.), Indicold Private Limited (India), Snowman Logistics Ltd. (India).

Global Cold Chain Packaging Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 34.8 billion

- 2026 Market Size: USD 39.2 billion

- Projected Market Size: USD 103.7 billion by 2035

- Growth Forecasts: 12.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (32.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, India

- Emerging Countries: Brazil, South Korea, Indonesia, Mexico, Vietnam

Last updated on : 26 March, 2026

Cold Chain Packaging Market - Growth Drivers and Challenges

Growth Drivers

- Rising demand for temperature‑sensitive pharmaceuticals: There has been a stronger growth in biopharmaceuticals, vaccines, and some of the special drugs, necessitating efficient temperature control during transport as well as storage. According to an article published by the Centers for Disease Control and Prevention (CDC) in June 2024, proper storage and handling of immunobiologics are highly essential, since failure to maintain the suggested conditions can reduce the total potency and reduce the immune response. On the other hand, vaccines need to be stored at 2°C to 8°C unless otherwise specified, and the report also highlighted that providers are responsible for monitoring storage, transport, and inventory of vaccines. These products need to be inspected at the time of delivery and during storage to ensure quality, denoting a positive outlook for the cold chain packaging market’s growth and exposure.

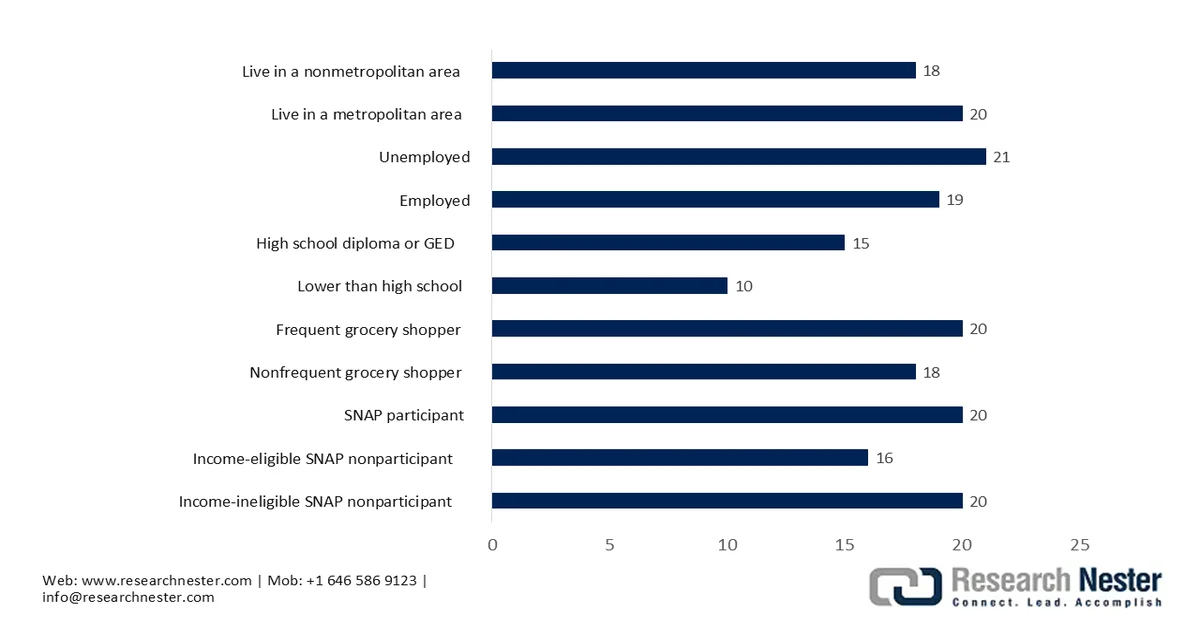

- E‑Commerce & last‑mile delivery expansion: There has been a boom in online grocery shopping, meal‑kit services, and direct‑to‑consumer pharmaceutical deliveries, which elevates the need for thermal packaging solutions. This raises the need for solutions that are capable of maintaining required temperatures through last‑mile logistics, benefiting the overall cold chain packaging market. As per the report published by the U.S. Department of Agriculture (USDA) in July 2024, about 1 in 5 U.S. grocery shoppers, which is 19.4%, purchased groceries online in 2022 and 2023. Younger adults who were aged 15 to 24 were most likely at 26%, when compared with 12% of those 55 and older. The article also stated that 22% of women shopped online more than men, i.e., 16%, and households with children, which is 23%, were more engaged than those without, which was 18%.

Online Grocery Shopping Trends by Demographics: Official U.S. Data (2022-2023)

Source: USDA

- Technological advancements: Introduction of smart packaging, GPS trackers, improved insulation materials, i.e., phase change materials, and vacuum insulated panels are readily boosting the overall uptake in the cold chain packaging market. These solutions enhance performance and regulatory compliance, boosting adoption among eco-conscious consumers. Tower Cold Chain, in April 2024, introduced a live tracking and monitoring feature in partnership with ELPRO, with a prime focus to enhance its passive temperature-controlled containers for pharmaceutical logistics. Besides, this particular system provides near real-time understandings into temperature, shock, tilt, altitude, and location, ensuring transparency and compliance for sensitive shipments. Hence, with constant efforts from global pioneers, the industry is set to witness exceptional growth in the upcoming years.

Challenges

- Complex regulatory compliance requirements: The cold chain packaging needs to navigate through extremely strict regulatory standards, especially in the case of pharmaceuticals and food. Also, these standards keep altering across different nations and regions, which causes complications for global supply chains. In this context, companies need to ensure that the packaging solution maintains specific temperature ranges, provides traceability, and meets safety recommendations, which in turn necessitates constant monitoring as well as documentation. Keeping pace with continuously changing regulations requires heavy investment in testing, certification, and quality assurance. The existence of regulatory obstacles in the cold chain packaging market ultimately slows down innovation and increases operational complexity, especially for companies that are operating across multiple jurisdictions.

- Environmental concerns and sustainability pressure: The cold chain packaging market faces increasing scrutiny due to its environmental impact. Most of the packaging solutions depend on single-use plastics, non-biodegradable insulation materials, and energy-intensive cooling methods. As sustainability becomes a priority, companies are under pressure to develop eco-friendly alternatives without compromising performance. At the same time, the sustainable materials are expensive and may not match the efficiency of traditional options. Recycling challenges and waste management issues, in turn, complicate this situation. Therefore, balancing environmental responsibility with operational effectiveness is a major hurdle, encouraging companies to innovate by meeting both regulatory requirements and consumer expectations for greener solutions.

Cold Chain Packaging Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

12.9% |

|

Base Year Market Size (2025) |

USD 34.8 billion |

|

Forecast Year Market Size (2035) |

USD 103.7 billion |

|

Regional Scope |

|

Cold Chain Packaging Market Segmentation:

Material Segment Analysis

In the material segment, the insulated materials subsegment is expected to attain the largest share of 66.4% in the cold chain packaging market by the conclusion of the forecast period. The dominance is effectively attributable to their high thermal efficiency, reusability, and compliance with long-duration shipping requirements. In April 2025, Tiger Corporation announced the launch of stainless-steel vacuum insulation panels for cold transport at the Osaka-Kansai Expo 2025, using vacuum-insulated reefer containers, protect boxes, and roll boxes in collaboration with Nippon Express and Gifu Plastic Industry. Besides, the company notes that TIVIP creates a vacuum inside stainless steel panels, achieving very low heat conduction, non-flammability, and long-lasting thermal insulation, maintaining performance for over 30 years while being thin and space-efficient, hence denoting a wider segment scope.

Application Segment Analysis

The fish, seafood, and meat segment is predicted to capture a significant revenue share in the cold chain packaging market during the discussed timeframe. The growing global demand for meat and seafood, along with increased production of these products, is efficiently driving the adoption of cold chain packaging. On the other hand, the naturally occurring bio-physiochemical changes in meat and fish accelerate spoilage, reflecting the importance of temperature-controlled logistics. As per the official statistics by the European Union in 2024, global fisheries and aquaculture reached a significant value of 223.2 million tons in 2022, with aquaculture surpassing capture fisheries for the first time, producing 94.4 million tons. The report also stated that international trade reached USD 195 billion, with low- and middle-income countries achieving a net export value of USD 45 billion in 2022, hence denoting a positive outlook for the segment’s growth and exposure.

End use Industry Segment Analysis

Under the end use industry segment, the pharmaceutical is anticipated to garner the lucrative revenue share in the cold chain packaging market by the end of 2035. Growth of the segment is largely driven by the heightened demand for temperature-sensitive biologics, vaccines, and gene therapies. On the other hand, the expansion of global immunization programs and personalized medicine also accelerates the adoption of advanced cold chain packaging. In January 2025, DS Smith announced the launch of TailorTemp, which is a fiber-based temperature-controlled packaging solution. Besides, it is made from recyclable corrugated cardboard with insulating inserts, and it keeps products cool for up to 36 hours, thereby supporting pharma and biotech sustainability goals. Hence, from a strategic perspective, such instances reflect the continued investments in sustainable cold chain packaging solutions to preserve the integrity of temperature-sensitive products.

Our in-depth analysis of the cold chain packaging market includes the following segments:

|

Segment |

Subsegments |

|

Material |

|

|

Application |

|

|

End use Industry |

|

|

Packaging Format |

|

|

Temperature Range |

|

|

Product |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Cold Chain Packaging Market - Regional Analysis

North America Market Insights

The cold chain packaging market in North America is expected to attain the largest share of 32.6% during the discussed timeframe. The region’s leadership is effectively attributable to advanced pharmaceutical cold chain infrastructure and supportive regulatory frameworks. The rising production of meat, processed foods, and fruits & vegetables, coupled with strong consumer demand for fresh and packaged food products, is prompting a favorable business ecosystem in the region. In this context, OEC stated that in 2024, the U.S. was the largest importer of frozen vegetables, wherein the imports were valued at USD 1.3 billion. Besides, the major suppliers were China, Belgium, and Spain, reflecting an insatiable demand for frozen produce across the country. The U.S. registered a trade deficit of USD 1.1 billion in this category, reflecting the strong dependency on imports. In addition, the key imported subproducts were frozen miscellaneous vegetables, vegetable mixtures, and peas, which form a significant portion of the nation’s frozen vegetable consumption and cold storage supply chain, hence denoting a positive cold chain packaging market outlook.

A robust logistics infrastructure, stringent regulatory standards, and strong demand from the food, pharmaceutical, and biotechnology sectors are certain drivers that are responsible for uplifting the overall cold chain packaging market in the U.S. The expansion of online grocery services is also boosting demand for efficient cold chain packaging across the country’s market. In June, 2024, the U.S. General Services Administration (GSA) finalized a rule encouraging federal supply schedule contractors to offer single-use plastic-free packaging. This particular move deliberately supports President Biden’s Federal Sustainability Plan by reducing plastic waste in federal supply chains. Besides having more than 14,500 contractors and USD 45 billion in annual sales, this is the first broad federal acquisition rule tackling plastic waste, thus solidifying the country’s position in sustainability and a transition toward a circular economy.

Canada cold chain packaging market has gained enhanced exposure owing to the strong expansion of the biopharmaceutical sector and a clear shift away from traditional plastics toward recyclable paper-based insulators and high-efficiency vacuum panels. The cold chain packaging market is also supported by a mix of domestic manufacturers and global logistics specialists who are focused on last-mile delivery across Canada’s vast geography. Based on the government data published in June 2024, Canada’s goods and services exports rose by 1.4% to USD 965.1 billion in 2023, whereas imports grew 3.1% to a total of USD 978.2 billion, with services driving export growth and goods contracting by 1.2%. In addition, the international investment flows rebounded, with foreign direct investment in Canada increasing 3.7% and the country’s direct investment abroad rising 1.8%, highlighting the continuing importance of supply chains in the economy.

APAC Market Insights

Asia Pacific cold chain packaging market is expected to grow at the fastest rate from 2026 to 2035. The region’s prominence is largely attributable to the growing consumption of fresh fruits, vegetables, meat, and seafood. The region benefits from a large youth demographic, increasing employment, shifting population dynamics, and rising disposable incomes, all of which are boosting demand for processed food. As per an article published by the USDA in June 2025, Japan’s frozen food industry reached USD 12.5 billion in 2023, growing 3.4% year-over-year, with imports accounting for 37.5% of the cold chain packaging market, largely driven by frozen vegetables, 65%. In a span of one decade, the market has expanded by around 30%, supported by rising household consumption, which has surpassed commercial usage. Frozen food imports have grown significantly, and the total imports reached notable volumes, including 1.15 million MT of frozen vegetables in 2022, making it suitable for bolstering the region’s cold chain packaging market growth.

Japan Frozen Food Consumption by Category (2023): Import Share, Value Breakdown & Market Composition

|

Category |

Value (10,000 USD) |

Composition Rate |

|

Fishery Products |

434 |

3.50% |

|

Farm Products (Imported) |

3,234 |

25.90% |

|

Imported Portion |

3,042 |

24.4% |

|

Livestock Products |

30 |

0.4% |

|

Prepared Foods (Imported) |

8,408 |

67.4% |

|

Imported Portion |

1,631 |

13.11% |

|

Confectionery |

366 |

2.9% |

|

Total (Imported) |

12,472 |

100% |

|

Imported Share |

4,673 |

37.5% |

Source: USDA

The expanding pharmaceutical exports are positioning China cold chain packaging market at the forefront of revenue contribution in this region. On the other hand, supportive government initiatives are accelerating investments in terms of refrigerated transportation and infrastructure. At the same time, manufacturers in China are highly focused on sustainable materials such as biodegradable and recyclable options and adopting smart packaging technologies to ensure temperature control by complying with global quality and safety standards. In June 2023, the country’s government data disclosed that China’s cold-chain logistics sector maintained noteworthy growth in the first five months of 2023, reaching a total value of USD 369.11 billion, which is up 4.1% year-on-year. Besides, investment in cold-chain infrastructure exceeded USD 1.9 billion, which marks a 6.6% increase when compared to the previous year. Therefore, this expansion reflects rising demand across diverse areas, which include cold-chain distribution centers and industry parks for premade meals.

The cold chain packaging market in India is entering a new phase of growth, which is propelled by its position as a global hub for generic drugs and vaccine production. The country’s agricultural sector and expanded production capacities also efficiently fuel the need for cold chain packaging. As per the article published by the Agricultural and Processed Food Products Export Development Authority (APEDA), India produced 112.98 million MT of fruits and 207.21 million MT of vegetables in FY24 across 18.36 million hectares. It ranks first globally in bananas with 26.22%, mangoes 42.84%, and papayas 36.5%, along with onions and okra among vegetables. In FY2025, exports of fresh fruits and vegetables totaled USD 1,818.56 million, whereas fruits contributed almost USD 999.55 million and vegetables USD 819 million. In addition, the major export destinations were Bangladesh, UAE, Iraq, Netherlands, and Nepal, with strong investments in cold chain infrastructure and quality assurance initiatives.

Europe Market Insights

Europe cold chain packaging market is supported by perishable food products and e-commerce deliveries. Rising investments in advanced insulation and temperature-controlled packaging technologies are accelerating adoption across the region. Besides the expansion of logistics networks and heightened focus on maintaining product quality, are driving market growth. In April 2025, the article published by the European Commission stated that the region’s agri-food exports reached USD 254.2 billion and imports USD 185.6 billion in 2024, resulting in a strong trade surplus of around USD 68.7 billion. It also noted that the UK remained the largest export destination, accounting for 23% of total exports worth USD 58.2 billion. A few of the main export categories included cereal preparations, dairy products, and wine, whereas olives and cocoa products saw the highest value growth, thus driving standard cold chain packaging market expansion.

The strict regulations, technological upgradations, and heightened demand from the pharma, food, and e-commerce sectors are responsible for uplifting the overall cold chain packaging market in Germany. Also, the country’s robust cold chain infrastructure ensures high standards of product safety, solidifying its leading position in the region. In December 2025, the Federal Ministry of Labour and Social Affairs stated that Germany’s Supply Chain Act, which became effective on January 1, 2023, legally requires companies with headquarters or branches in Germany to respect human rights across their global supply chains. Initially applying to firms with more than 3,000 employees and extended to those with above 1,000 employees from 2024, the law mandates risk management systems, preventive measures, complaint procedures, and regular reporting. It mentioned that non-compliance can lead to fines of up to USD 8.7 million or 2% of global turnover for companies, along with exclusion from public contracts.

The cold chain packaging market in the UK is largely driven by the rise of high-value biologics and cell therapies, which is fueling a shift toward high-performance vacuum insulation and reusable packaging systems. The regulatory adjustments encourage track-and-trace-enabled solutions to ensure compliance during cross-border transit. As per the article published by Cold Chain Federation in September 2024, the UK cold chain contributed about USD 18 billion in gross value added to the country’s economy in 2023. Besides, the sector deliberately supported almost 184,000 jobs and generated around USD 4.7 billion in tax revenue for the UK government. In trade terms, the country reported USD 15 billion worth of exports and USD 41 billion of chilled and frozen imports. The report also stated that nearly 49 % of UK food and beverages, i.e., USD 64 billion, required cold chain handling, thus underscoring its role in manufacturing and international supply chains.

Key Cold Chain Packaging Market Players:

- Cold Chain Technologies, LLC (U.S.)

- Sonoco ThermoSafe (U.S.)

- Cryopak Industries Inc. (U.S.)

- Sealed Air Corporation (U.S.)

- CSafe Global LLC (U.S.)

- TemperPack Technologies, Inc. (U.S.)

- Inmark LLC (U.S.)

- Softbox Systems Ltd. (UK)

- Intelsius (DGP Intelsius LLC) (UK)

- Sofrigam SA Ltd. (France)

- EMBALL’ISO (France)

- va-Q-tec AG (Germany)

- Envirotainer AB (Sweden)

- Tower Cold Chain Solutions (UK)

- Nippon Express (Japan)

- Cryoport Systems (U.S.)

- Peli BioThermal (U.S.)

- BioLife Solutions (U.S.)

- Maersk (Denmark)

- Vizient (U.S.)

- Nordic Cold Chain Solutions (U.S.)

- Indicold Private Limited (India)

- Snowman Logistics Ltd. (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Sonoco ThermoSafe is widely regarded as a global leader in temperature-controlled packaging. The company’s strength lies in combining passive and active packaging systems, which is supported by strong engineering and testing capabilities. Sonoco is also focused on automation and capacity expansion to meet surging worldwide demand.

- Pelican BioThermal is also a major player in this field, which is best known for its reusable temperature-controlled packaging solutions. The firm is highly focused on product durability, long-duration thermal performance, and sustainability, making it a preferred partner for life sciences logistics.

- Cold Chain Technologies is a prominent provider of both reusable and single-use thermal packaging solutions. Besides, the company offers a wide range of containers, refrigerants, and advanced materials such as vacuum-insulated panels and phase-change materials, thereby solidifying its position as a full-service cold chain solutions provider.

- va-Q-tec AG is a technology-driven company that specializes in high-performance vacuum insulation panels along with phase-change materials. The firm maintains a strong position through strong R&D capabilities, patented technologies, and a focus on sustainability, including climate-neutral production.

- Softbox Systems Ltd. is yet another central player in this field and is a leading provider of temperature-controlled packaging for pharmaceutical and life sciences applications. In addition, the company offers a diverse portfolio that includes insulated shippers, parcel solutions, and temperature-controlled bags.

Below is the list of some prominent players operating in the global cold chain packaging market:

The cold chain packaging market is extremely competitive, wherein the leading players are focused on advanced insulation materials, reusable packaging systems, and digital tracking technologies. Mergers & acquisitions and geographic expansion into growing economies are the primary strategies adopted by the leading pioneers to strengthen their market positions. Companies are also making investments in terms of sustainable solutions, i.e., recyclable and phase-change materials, to meet environmental goals. In October 2025, Peli BioThermal announced the acquisition of Evo from BioLife Solutions to expand its portfolio of temperature-controlled logistics solutions for the pharmaceutical sector. The Evo line, which includes cryogenic shippers and evoIS technology, strengthens capabilities in the fast-growing cell and gene therapy sector, where precision and reliability are highly essential.

Corporate Landscape of the Cold Chain Packaging Market:

Recent Developments

- In July 2025, Maersk inaugurated a 17,500-square-meter integrated packing and cold storage hub in Olmos, northern Peru, with a main aim to strengthen the region’s agro-export sector. The facility offers end-to-end cold chain services, such as processing, packaging, storage, and customs handling.

- In July 2025, Nordic Cold Chain Solutions introduced the Nordic Express Pack, which is the first packaging solution specifically designed and tested for GLP-1 medications. It supports specialty pharmacies and distributors with faster packing, reduced storage needs, and integrated temperature indicators for compliance.

- In September 2024, Cryopak was chosen as a contracted cold chain packaging partner for Vizient Pharmacy Aggregation Groups. The company will provide prequalified temperature-sensitive packaging solutions ranging from 2°C to 8°C and CRT options, including sustainable and reusable designs.

- Report ID: 4532

- Published Date: Mar 26, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.