Surfactants Market Outlook:

Surfactants Market size was valued at USD 50.1 billion in 2025 and is projected to account for USD 83.1 billion by 2035, rising at a CAGR of 5.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of surfactants is assessed at USD 52.7 billion.

The surfactants market is supported by long-term demand from industrial and institutional cleaning, household care manufacturing, agriculture, pharmaceuticals, and water treatment applications. Demand conditions remain closely linked to population growth, urbanization, sanitation investments, and industrial output. According to the United Nations July 2024, the global population is projected to increase from approximately 8.2 billion people in 2024 to about 10.3 billion by 2080, expanding consumption of cleaning and hygiene-related products across both developed and emerging economies. The NLM January 2023 study reports that more than 55% of the world’s population now lives in urban areas, a trend that continues to increase demand for municipal cleaning services, wastewater management, and consumer packaged goods that utilize surfactant-based formulations.

At the same time, governments and public agencies continue to emphasize hygiene and infection prevention. Data from the WHO/UNICEF Joint Monitoring Programme indicate that billions of people still lack adequate hygiene services, creating sustained requirements for cleaning products and sanitation-related investments. For manufacturers, these conditions support stable procurement activity from detergent producers, institutional cleaning suppliers, and industrial formulators. Demand is also being reinforced by regulatory attention to product safety, biodegradability, and environmental performance, promotes reformulation efforts and the adoption of approved ingredients that meet evolving compliance requirements in major markets. The World Economic Forum's March 2022 estimates that manufacturing contributes roughly 16% of global GDP, highlighting the scale of industrial sectors that rely on formulated chemicals for processing, cleaning, lubrication, coatings, and specialty applications.

Key Surfactants Market Insights Summary:

Regional Insights:

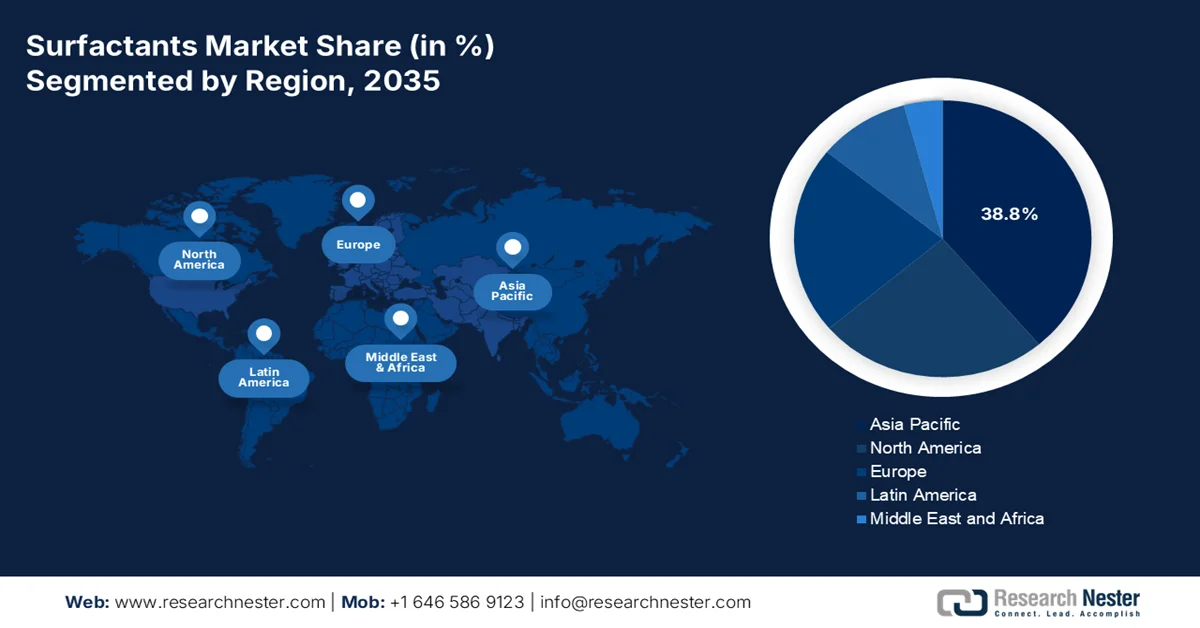

- Asia Pacific is anticipated to secure 38.8% of the surfactants market by 2035, reinforced by rapid urbanization, expanding manufacturing capacity, and rising household cleaning product consumption

- North America is forecast to register robust growth throughout 2026–2035 in the market, stimulated by stringent environmental regulations promoting biodegradable and bio-based surfactant alternatives

Segment Insights:

- The petroleum based segment is projected to capture 88.7% of the surfactants market by 2035, benefiting from abundant and cost-effective feedstocks such as linear alkylbenzene, ethylene, and propylene derived from crude oil and natural gas

- The household detergents and cleaners segment is expected to remain a key demand contributor over 2026–2035, accelerated by sustained consumer preference for soap-based cleaning solutions that effectively remove contaminants and pathogens

Key Growth Trends:

- Long-term water and wastewater infrastructure investment

- Rising government healthcare expenditure

Major Challenges:

- Regulatory compliance and environmental restrictions

- Raw material supply chain volatility

Key Players: BASF (Germany), Dow Inc. (U.S.), Croda International (UK), Evonik Industries (Germany), Stepan Company (U.S.), Solvay (Belgium), Clariant (Switzerland), Kao Corporation (Japan), Lion Specialty Chemicals (Japan), Mitsubishi Chemical Corporation (Japan), Huntsman Corporation (U.S.), Galaxy Surfactants (India), Godrej Industries (India), KLK OLEO (Malaysia), PCC SE (Germany), Sanyo Chemical Industries (Japan), Enaspol (Czech Republic), Musim Mas (Singapore), Sironix Renewables (U.S.), AGC (Japan).

Global Surfactants Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 50.1 billion

- 2026 Market Size: USD 52.7 billion

- Projected Market Size: USD 83.1 billion by 2035

- Growth Forecasts: 5.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (38.8% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, India, Japan, Germany

- Emerging Countries: Indonesia, Vietnam, Malaysia, South Korea, Thailand

Last updated on : 8 June, 2026

Surfactants Market - Growth Drivers and Challenges

Growth Drivers

- Long-term water and wastewater infrastructure investment: The GAO July 2024 data depicts that U.S. Environmental Protection Agency (EPA) estimates that more than USD 630 billion will be needed over the next 20 years to repair, replace, and upgrade clean water and wastewater infrastructure across the United States. This planned investment encompasses treatment plants, sewer networks, pumping stations, and water distribution systems, creating sustained demand for industrial cleaning agents, water treatment formulations, membrane maintenance chemicals, and facility sanitation products that utilize surfactants. As utilities modernize aging infrastructure and expand treatment capacity, procurement requirements for operational and maintenance chemicals are expected to increase. Suppliers offering environmentally compliant and performance-oriented formulations are likely to benefit from long-term public infrastructure spending and water quality improvement initiatives.

- Rising government healthcare expenditure: Healthcare systems worldwide continue to expand spending on hospital sanitation, infection prevention, and medical facility maintenance, creating sustained demand for cleaning and disinfection products that rely on surfactant-based formulations. According to the American Medical Association, April 2025 data, U.S. national health expenditures reached approximately USD 4.9 trillion in 2023, accounting for nearly 17.6% of GDP. Growing healthcare infrastructure requires increased procurement of cleaning agents for hospitals, clinics, laboratories, and long-term care facilities. This is encouraging suppliers to develop formulations that meet both performance and sustainability standards. Companies serving healthcare-related applications are also benefiting from the expansion of public hospitals and diagnostic facilities in emerging economies, where healthcare access remains a government priority.

Challenges

- Regulatory compliance and environmental restrictions: With increasingly stringent regulations surrounding water pollution and biodegradability, surfactant producers face significant compliance burdens. These regulatory frameworks require costly reformulations and extensive testing, diverting resources away from new product development and adding to operational overheads. In the personal and home care sectors, adapting existing surfactants to meet enhanced wastewater discharge standards extends time-to-market and compresses margins. Such regulatory pressure adversely impacts market agility and innovation, as manufacturers are compelled to prioritize compliance and cost-efficiency over sustainability and differentiation, ultimately slowing the overall pace of growth across the surfactant value chain.

- Raw material supply chain volatility: The surfactants industry relies heavily on raw materials imported internationally, such as crop derivatives and special chemicals. Supply chain interference through geopolitical tensions, volatility over crop output due to climate uncertainty, and traffic congestion has caused irregular availability and steep price volatility. These instabilities raise the manufacturing cost and make inventory planning difficult for household and personal cleaning product makers. Uncertainty hinders long-term planning, postpones product launching, and betrays competitiveness, a substantial barrier to uniform market expansion.

Surfactants Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.2% |

|

Base Year Market Size (2025) |

USD 50.1 billion |

|

Forecast Year Market Size (2035) |

USD 83.1 billion |

|

Regional Scope |

|

Surfactants Market Segmentation:

Origin Segment Analysis

Under the origin segment, the petroleum based is dominating and is poised to hold the share value of 88.7% by the end of 2035 in the surfactants market. the segment is driven due to abundant and cost-effective feedstocks such as linear alkylbenzene (LAB), ethylene, and propylene derived from crude oil and natural gas. Synthetic surfactants offer consistent performance in high-temperature industrial processes, heavy-duty laundry, and oilfield applications where bio-based alternatives may degrade. According to the U.S. Energy Information Administration (EIA), August 2024 data, global petroleum consumption totaled 103 million barrels per day, ensuring stable supply for synthetic surfactant manufacturing. Despite rising environmental regulations, manufacturers continue to invest in readily biodegradable synthetic variants, sustaining their market leadership.

Application Segment Analysis

Within the application segment, the household detergents and cleaners’ sub-segment of the surfactants market are a critical volume driver. Unlike alcohol-based hand sanitizers, which do not remove contaminants like feces, dirt, and pesticides and fail to kill all organisms such as norovirus, traditional soap and water remain the gold standard for thorough cleaning. Surfactants in soap work by emulsifying oils and lifting particulate soils, physically removing pathogens and chemical residues from the skin. The Washington State Department of Health November 2023 data recommends washing with soap and water whenever possible, noting that hand sanitizers with at least 60% alcohol are only a backup when soap is unavailable. This preference sustains strong surfactant demand in hand soaps globally.

End user Industry Segment Analysis

The consumer goods sector stands as the largest end-user industry within the surfactants market, driven by everyday products used in households worldwide. Surfactants serve as essential ingredients in laundry detergents, dishwashing liquids, fabric softeners, surface cleaners, shampoos, body washes, hand soaps, toothpaste, and cosmetics. In laundry and dish care, surfactants remove grease, oil, and dirt particles from fabrics and hard surfaces. In personal care, they provide foaming, emulsifying, and cleansing properties while maintaining mildness to skin and hair. The growing consumer preference for concentrated liquid formats, eco-friendly packaging, and plant-based formulations continues to shape product development. Emerging markets contribute significantly to volume growth as rising disposable incomes increase per capita consumption of branded household and personal care products.

Our in-depth analysis of the surfactants market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Origin |

|

|

Application |

|

|

End user Industry |

|

|

Substrate |

|

|

Product Form |

|

|

Function |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Surfactants Market - Regional Analysis

APAC Market Insights

The Asia Pacific is dominating the surfactants market and is expected to hold the regional revenue share of 38.8% by the end of 2035. The region is driven by rapid urbanization, expanding manufacturing capacity, and rising household cleaning product consumption. China and India dominate regional demand due to their large populations and growing middle-class spending on laundry detergents, personal care products, and industrial cleaners. Southeast Asian nations including Indonesia, Malaysia, and Vietnam serve as both significant consumers and production hubs, benefiting from access to palm oil and coconut oil feedstocks for bio-based surfactant manufacturing. Japan and South Korea lead in specialty surfactant innovation for high-performance personal care and electronics cleaning applications. Price sensitivity remains high in developing economies, favoring large-scale producers with cost advantages. Regulatory enforcement on biodegradability varies significantly across countries, creating a fragmented compliance landscape.

The surfactants market in India is benefiting from government initiatives aimed at expanding the country's chemical and plastics manufacturing base. According to the PIB April 2025 data, India ranked as the 12th-largest exporter of plastics globally in 2022, with exports increasing from approximately USD 8.2 billion in 2014 to USD 27 billion in 2022. To support further industrial growth, the government has promoted the development of Plastic Parks, including projects approved in Gorakhpur (Uttar Pradesh) and Ganjimutt (Karnataka), equipped with common infrastructure such as effluent treatment and recycling facilities. These investments are strengthening downstream chemical production, improving manufacturing efficiency, and creating favorable conditions for surfactant demand across industrial and consumer applications.

The strong industrial production and continued expansion of the country's chemical manufacturing sector is shaping the market in China. According to the People’s Republic of China January 2025 data, the value added of China's industrial enterprises above designated size increased by 5.8% in 2024, reflecting sustained growth in manufacturing activities that consume surfactants across cleaning, textile, agricultural, and industrial applications. In addition, the August 2025 data show that China's total imports and exports of goods reached approximately USD 6.16 trillion in 2024, highlighting the scale of industrial and trade activity supporting demand for chemical intermediates and specialty ingredients. These factors, combined with ongoing investments in advanced manufacturing and industrial upgrading, continue to create favorable growth opportunities for the China surfactants market.

North America Market Insights

North America is projected to emerge rapidly during the assessed period, 2026 to 2035 in the surfactants market. the region is mature and regulation-driven, with the U.S. accounting for the majority of regional demand. Industrial and institutional cleaning represents the largest application segment, followed by personal care and oilfield chemicals. Environmental regulations enforced by the Environmental Protection Agency and Environment and Climate Change Canada continue to shape product formulations, pushing manufacturers toward readily biodegradable and bio-based surfactant alternatives. The region benefits from a well-established chemical manufacturing infrastructure, including sulfonation and ethoxylation facilities concentrated along the U.S. Gulf Coast. Market participants compete primarily on product performance, regulatory compliance support, and supply chain reliability rather than price. Cross-border trade between the U.S. and Canada remains significant under USMCA trade terms.

The large and diversified chemical industry, supported by strong domestic consumption and international trade activity is driving the market in the U.S. According to OEC 2024 data, the U.S. was the world’s largest importer of chemical products (HS Section VI), with imports valued at approximately USD 333 billion in 2024, reflecting substantial demand for chemical raw materials and specialty ingredients across industrial and consumer sectors. Additionally, the Federal Reserve reported that U.S. industrial production for chemicals increased during 2024, indicating expanding manufacturing activity that supports surfactant consumption in cleaning, personal care, agriculture, and industrial applications. These trends, combined with ongoing investments in domestic production capacity, continue to strengthen growth prospects for the U.S. surfactants market.

The growth in domestic chemical manufacturing and rising demand from cleaning, personal care, industrial processing, and environmental applications is driving the surfactants market in Canada. According to Chemistry Industry Association of Canada 2025 data, the nation has manufactured USD 77 billion worth products, reflecting strong activity across the country's chemical value chain that supports surfactant production and consumption. In addition, IISD December 2024 data reported that the federal government committed approximately USD 650 million through the Freshwater Action Plan to protect and restore major freshwater ecosystems, driving investments in water treatment and environmental management. These developments are increasing demand for specialty chemicals used in treatment, cleaning, and industrial maintenance applications, creating favorable conditions for continued growth of the Canadian market.

Europe Market Insights

The surfactants market in Europe is characterized by stringent environmental regulations and strong demand for premium, bio-based, and readily biodegradable products. Germany, France, the United Kingdom, and Italy represent the largest national markets, driven by mature household cleaning, personal care, and industrial institutional sectors. The European Union's regulatory framework, including REACH and the Ecolabel program, imposes rigorous testing and registration requirements for surfactant manufacturers, favoring established players with substantial compliance resources. Consumer awareness of ecological impact has pushed formulators toward non-ionic and amphoteric surfactants derived from renewable feedstocks. Eastern European nations offer lower production costs and serve as manufacturing bases for export to Western Europe. The region maintains advanced sulfonation and ethoxylation capacity but faces energy cost pressures affecting production economics.

The robust industrial trade and the country's position as a major European chemical manufacturing hub is shaping the surfactants market in Germany. According to the Destatis Npvember 2025 data, Germany exports increased by 1.0% in 2025, while imports rose by 4.4% compared with the previous year after calendar and seasonal adjustment. In December 2025 alone, exports grew by 2.7% year-over-year, reflecting continued momentum in manufacturing and industrial supply chains. Higher trade volumes support demand for chemical intermediates and specialty ingredients used across cleaning, personal care, textile, and industrial applications. Combined with Germany’s advanced production infrastructure, these trends create favorable conditions for sustained growth in the domestic surfactants market.

The surfactants market in UK is benefiting from improving economic conditions and a strong chemical manufacturing sector. According to the Office for National Statistics March 2025 data, the UK's real annual GDP increased by 1.1% in 2024, up from the initial estimate of 0.9%, following growth of 0.4% in 2023. Stronger economic activity is supporting demand across consumer goods, industrial processing, and cleaning applications that rely on surfactants. Additionally, the UK exported approximately USD 58.2 billion worth of chemical products (HS Section VI), highlighting the country's significant role in global chemical trade, as per the OEC 2024 data. Continued industrial output, export strength, and investment across chemical value chains are creating favorable conditions for sustained growth in the UK surfactants market.

Key Surfactants Market Players:

- BASF (Germany)

- Dow Inc. (U.S.)

- Croda International (UK)

- Evonik Industries (Germany)

- Stepan Company (U.S.)

- Solvay (Belgium)

- Clariant (Switzerland)

- Kao Corporation (Japan)

- Lion Specialty Chemicals (Japan)

- Mitsubishi Chemical Corporation (Japan)

- Huntsman Corporation (U.S.)

- Galaxy Surfactants (India)

- Godrej Industries (India)

- KLK OLEO (Malaysia)

- PCC SE (Germany)

- Sanyo Chemical Industries (Japan)

- Enaspol (Czech Republic)

- Musim Mas (Singapore)

- Sironix Renewables (U.S.)

- AGC (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- BASF leads the global surfactants market through integrated Verbund production and bio-based innovations. The company leverages digital formulation tools to develop high-performance, biodegradable surfactants for detergents and personal care. Strategic capacity expansions in Asia ensure supply chain resilience while meeting tightening environmental regulations worldwide. In 2024, the company has made sales of €65.3 billion.

- Dow Inc. dominates the surfactants market with its extensive ethylene oxide derivatives portfolio. The company develops smart surfactant systems that adapt to water hardness and temperature, enabling energy-efficient cold-water cleaning. Dow's circular economy initiatives include recycled-content surfactants and strategic partnerships for sustainable formulation technologies. In 2025, the company has made a net sales of USD 40 billion.

- Croda excels in the premium surfactants market, focusing on naturally derived, mild surfactants for personal care. The company pioneers biodegradable marine-safe surfactants and microbiome-friendly technologies. Strategic acquisitions and carbon-negative manufacturing commitments reinforce its leadership in sustainable, high-value surfactant solutions for eco-conscious consumers.

- Evonik drives innovation in the specialty surfactants market with responsive technologies for agrochemicals and oilfields. Its AI-driven high-throughput screening accelerates biosurfactant development, including rhamnolipids via industrial fermentation. Evonik's dynamic surfactant systems alter interfacial properties under varying conditions, optimizing performance in complex field environments.

- Stepan focuses on the surfactants market through sulfonation and quaternary ammonium compounds for institutional cleaning. The company engineers low-temperature, high-hardness water surfactant blends that reduce energy consumption. Vertical integration into LAB raw materials and global capacity expansions in Brazil and China support its competitive positioning.

Here is a list of key players operating in the global surfactants market:

The global surfactant market is highly consolidated, led by multinational chemical giants competing on scale, innovation, and sustainability. Key players are aggressively shifting toward bio-based, renewable feedstocks and green chemistries to meet tightening environmental regulations and consumer demand. Strategic initiatives include significant capacity expansions in Asia-Pacific, vertical integration to secure raw materials, and acquisitions to diversify product portfolios for high-growth applications like personal care, agrochemicals, and enhanced oil recovery. For example, in May 2025, Musim Mas has agreed to acquire a manufacturing facility located in Bauan, Batangas province, Philippines. Collaborative R&D with end-user industries is also intensifying, aiming to develop mild, high-performance surfactants while reducing carbon footprints across supply chains.

Corporate Landscape of the Market:

Recent Developments

- In March 2026, Sironix Renewables announced its expansion into the personal care sector with the launch of Furasoft™-SF and Furasoft™-LFS, two high-performance, bio-based and cost-competitive surfactants.

- In March 2026, BASF Hannong Chemicals Solutions Ltd. announced the inauguration of its new non-ionic surfactant (NIS) site located in the Daesan Industrial Complex in Seosan, Chungcheongnam-do, Korea.

- In July 2025, AGC announced the launch of surfactant and fluorinated polymerization solvent-free grades in its fluoroelastomer AFLAS™ FFKM series; the SF grades. The newly developed products are manufactured entirely without the use of any surfactants or fluorinated polymerization solvents.

- Report ID: 8132

- Published Date: Jun 08, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.