Sterility Testing Market Outlook:

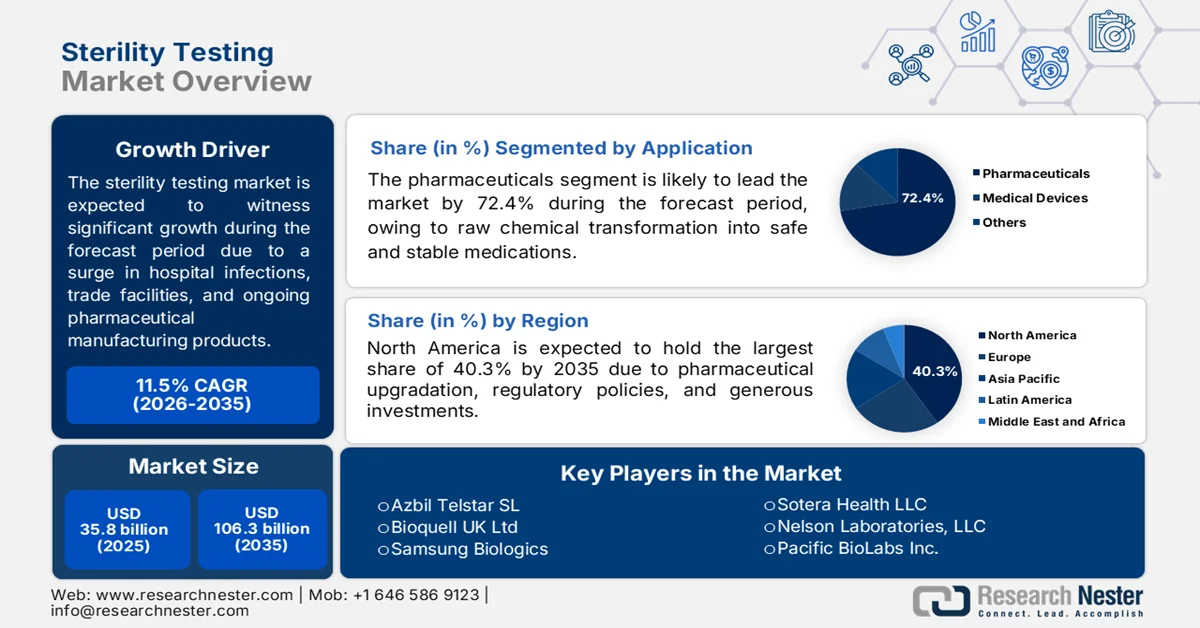

Sterility Testing Market size was over USD 35.8 billion in 2025 and is expected to cross USD 106.3 billion by the end of 2035, growing at more than 11.5% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of sterility testing is assessed at USD 39.9 billion.

The worldwide sterility testing market is shaped by several factors, including the rise in hospital-acquired infections, an increase in consolidation from contract testing laboratories, acceleration in automation implementation, supply chain dynamics, and continuous manufacturing in pharmaceutical production. According to official statistics published by OECD in 2023, 16 defined daily doses of antibiotics per 1,000 population were prescribed across different countries as of 2023. Besides, the pharmaceutical industry gained USD 11.5 billion in external funding for research and development, indicating 10% of overall pharmaceutical expenditure. Additionally, subsidies catered to 1% of the expenditure, particularly in Japan, followed by 2% in Switzerland, 20% in Germany, and 49% in the UK. Therefore, this denotes a massive growth in pharmaceutical manufacturing, which is positively impacting the sterility testing market upliftment.

Worldwide Antibiotics Prescription Volume Analysis, 2013-2023

|

Countries |

Volume (Defined Daily Doses) |

|

|

2013 |

2023 |

|

|

Greece |

28 |

27 |

|

Korea |

23 |

25 |

|

Spain |

16 |

23 |

|

Poland |

20 |

22 |

|

France |

24 |

22 |

|

Ireland |

20 |

21 |

|

Italy |

23 |

21 |

|

Luxembourg |

23 |

19 |

|

Australia |

23 |

18 |

|

Japan |

14 |

10 |

Source: OECD

Furthermore, the digital integration and laboratory informatics, along with the presence of decentralized testing models, patient-based release testing, and multi-modal contamination detection, are a few trends that are responsible for driving the sterility testing market globally. As stated in an article published by the CDC Government in September 2025, hospitals, such as Mbagathi Hospital, effectively serve more than 1,000 patients regularly and also conduct 20,000 laboratory tests every month. Moreover, there was a rise in the World Health Organization Stepwise Laboratory Improvement Program Towards Accreditation (SLIPTA) performance, from 55% to 90%. Besides, of the 64 routine test conductions, 70% were readily enrolled in an external quality assurance program and continuously achieved performance above 80%, thereby positively fueling the market’s growth and demand.

Key Sterility Testing Market Insights Summary:

Regional Highlights:

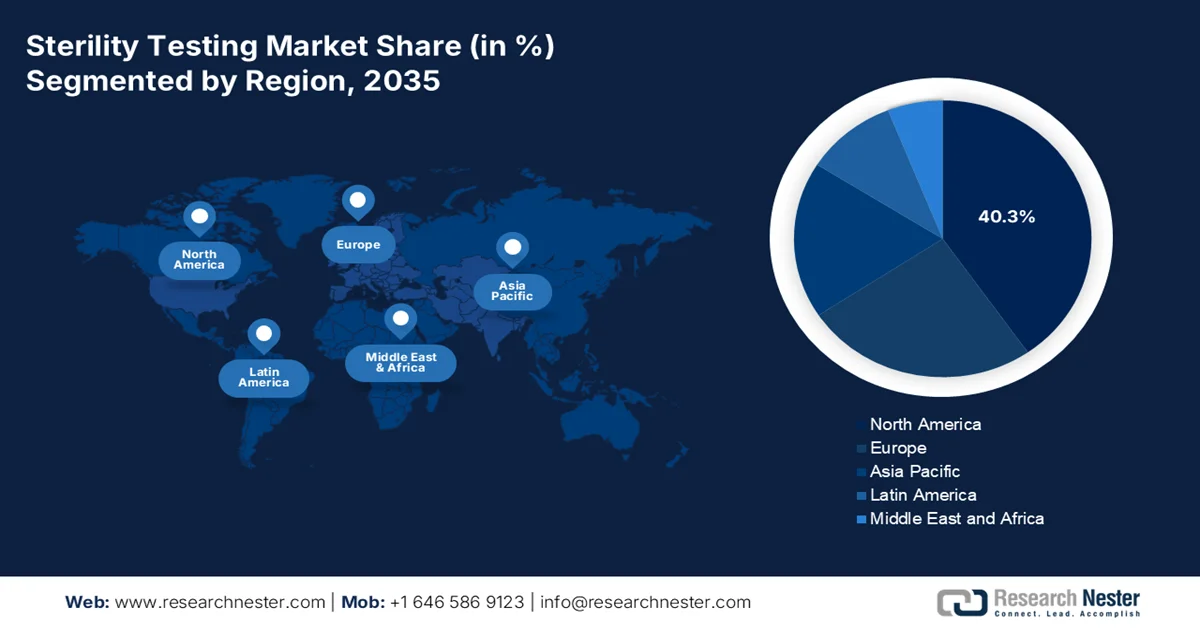

- North America is projected to command a 40.3% revenue share by 2035, propelled by pharmaceutical facility upgradation, regulatory enforcement, expanding demand for kits and reagents, and increasing provincial investments

- Asia Pacific is poised to witness the fastest growth in the sterility testing market throughout 2026–2035, impelled by expanding sterile manufacturing capabilities, rising pharma investments, regulatory scrutiny, and rapid microbiological method adoption

- The sterility testing market in the U.S. accounts for 78.5% of the share in North America, which is driven by the robust presence of biotechnology and pharmaceutical organizations, along with a surge in the need for sterile drug manufacturing.

Segment Insights:

- The pharmaceuticals segment in the sterility testing market is anticipated to account for a dominant 72.4% share by 2035, supported by rising pharmaceutical expenditure and the growing need for stable, safe, and effective medicines

- The membrane filtration segment is projected to secure the second-largest share during 2026–2035, stimulated by its increasing adoption as an efficient semi-permeable separation process for microorganisms, solutes, and particles

Key Growth Trends:

- Biosimilar industry maturation

- Surge in medical device products

Major Challenges:

- False positives and manufacturing disruptions

- Method validation burden for rapid technologies

Key Players: Charles River Laboratories International Inc., Merck KGaA, bioMérieux SA, Thermo Fisher Scientific Inc., Sartorius AG, SGS SA, Eurofins Scientific SE, WuXi AppTec, STERIS Plc, Sotera Health LLC, Nelson Laboratories LLC, Pacific BioLabs Inc., Becton Dickinson and Company, Ecolab Inc., Toxikon Corporation, Boston Analytical Inc., Azbil Telstar SL, Bioquell UK Ltd, Samsung Biologics, Sigma-Aldrich, Lonza.

Global Sterility Testing Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 35.8 billion

- 2026 Market Size: USD 39.9 billion

- Projected Market Size: USD 106.3 billion by 2035

- Growth Forecasts: 11.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: U.S., Germany, China, Japan, India

- Emerging Countries: South Korea, Singapore, Malaysia, Thailand, Vietnam

Last updated on : 29 May, 2026

Sterility Testing Market - Growth Drivers and Challenges

Growth Drivers

- Biosimilar industry maturation: The biologic patent wave has increasingly unleashed different biosimilars globally, which is significantly driving the sterility testing market. According to official statistics published by the OECD in November 2025, initially biosimilars represented only 1% of the industry volume, which later on surged to 22% as of 2023. This particular increase highlighted the growing integration and acceptance of biosimilars in global healthcare systems. Moreover, in the same year, biosimilars constituted over one-quarter of the accessible global economy across countries, including Portugal, Austria, Sweden, Spain, and Italy. Besides, the biosimilar availability varies from country to country, thus proliferating the sterility testing market growth.

Country-Wise Biosimilars in Biologic Industry Share Analysis, 2023

|

Countries |

Share % |

|

Italy |

46 |

|

Spain |

30 |

|

Sweden |

30 |

|

Austria |

29 |

|

Portugal |

28 |

|

Finland |

24 |

|

Ireland |

21 |

|

France |

20 |

|

Latvia |

18 |

|

Germany |

16 |

|

Lithuania |

16 |

|

Czechia |

13 |

|

Poland |

11 |

|

Slovak Republic |

10 |

|

Belgium |

10 |

|

Switzerland |

8 |

|

Slovenia |

8 |

|

Hungary |

8 |

Source:OECD

- Surge in medical device products: Devices, such as prefilled syringes, antimicrobial catheters, and drug-eluting stents with suitable drug coatings, need standard testing capabilities, leading to the sterility testing market demand. As per an article published by NLM in December 2025, the growth of prefilled syringes is predicted to be more than double by the end of 2030, with expected yearly growth rates of over 10% globally. With this growth, there is a huge opportunity for misutilization, for instance, in 2025, approximately 330 patients were impacted with human immunodeficiency virus (HIV), Hepatitis C virus (HCV), and Hepatitis B virus (HBV) testing at Chesapeake Regional Medical Center in the U.S., thereby enhancing the sterility testing market demand.

Challenges

- False positives and manufacturing disruptions: The aspect of false test results, wherein a test incorrectly indicates microbial contamination, represents a severe operational and financial challenge. A single false positive can trigger a full batch investigation, quarantine of numerous products, line shutdowns, and potential batch rejection. The root cause investigation is resource-intensive, requiring environmental monitoring review, operator retraining, equipment recertification, and repeat testing. In many cases, the contaminant is traced to laboratory errors such as airborne contamination during sample handling, contaminated growth media, or improper aseptic technique rather than actual product contamination, thereby limiting the sterility testing market.

- Method validation burden for rapid technologies: Rapid microbiological methods (RMM) usually offer significant time savings, but the regulatory pathway to replacing compendial methods is extraordinarily demanding. Besides, manufacturers willing to adopt PCR, ATP bioluminescence, or flow cytometry for sterility testing must conduct comprehensive validation studies demonstrating that the alternative method is equivalent or superior to traditional 14-day culture methods. Moreover, validation requires testing across multiple product matrices, demonstrating robustness against diverse microbial species, including bacteria, yeast, and mold, establishing detection limits, and proving the absence of inhibitory effects from the product itself. Additionally, for each product type, this validation process can take months and amount to a huge expense, thereby causing a hindrance in the sterility testing market.

Sterility Testing Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.5% |

|

Base Year Market Size (2025) |

USD 35.8 billion |

|

Forecast Year Market Size (2035) |

USD 106.3 billion |

|

Regional Scope |

|

Sterility Testing Market Segmentation:

Application Segment Analysis

The pharmaceuticals segment, which is part of the application, is anticipated to capture the largest share of 72.4% in the sterility testing market by the end of 2035. The segment’s upliftment is primarily attributed to its importance in translating raw chemical discoveries into effective, stable, and safe medicines. According to official statistics published by OECD in November 2025, the per capita spending on retail pharmaceuticals significantly amounted to USD 766 across different countries as of 2023. In this regard, the U.S. recorded the highest expenditure, amounting to USD 1,713, which is followed by USD 1,158 in Germany and USD 1,061 in Sweden. Besides, in the lower end, Denmark accounted for USD 404, while Chile accounted for USD 455, and Estonia for USD 458, indicating the spending rate below 60%. Therefore, the pharmaceutical expenditure across these nations denotes a huge contribution towards the sterility testing market upliftment globally.

Global Retail Pharmaceuticals Per Capita Expenditure Analysis, 2023

|

Countries |

Expenditure (USD PPP) |

|

Canada |

990 |

|

Japan |

983 |

|

Greece |

921 |

|

Bulgaria |

883 |

|

Australia |

872 |

|

Korea |

851 |

|

Italy |

846 |

|

Austria |

845 |

|

France |

813 |

|

Slovenia |

770 |

Source: OECD

Test Type Segment Analysis

During the forecast period, the membrane filtration segment, which is part of the test type, is projected to garner the second-largest share in the sterility filtration market. The segment’s growth is effectively fueled by its crucial role as a separation process that utilizes a semi-permeable gap for separating solutes, microorganisms, and particles from liquids based on chemical properties and size. As stated in an article published by the Chemical Engineering Journal in June 2025, air-based direct membrane filtration tends to produce high-quality permeate but restricted carbon recovery of approximately 21%, and also yields a retention with an estimated 2,500 mg/L and 11-fold concentration. Therefore, this particular test type segment has readily gained increased traction and evolved as an emerging strategy, thus driving the market expansion.

Site Segment Analysis

Based on the site, the outsourced testing segment is expected to account for the third-largest share by the end of the stipulated timeline. The segment’s development is highly propelled by representing a transformative shift in the sterility testing market, as pharmaceutical and biopharmaceutical companies increasingly delegate quality control functions to specialized contract testing laboratories (CTLs) and contract development and manufacturing organizations (CDMOs). This strategic pivot enables drug manufacturers to convert fixed capital expenditures into variable costs, access state-of-the-art rapid microbiological methods (RMM), and achieve flexible capacity scaling without in-house infrastructure investments, thus fueling the sterility testing market exposure.

Our in-depth analysis of the sterility testing market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Test Type |

|

|

Site |

|

|

Type |

|

|

End user |

|

|

Sample Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Sterility Testing Market - Regional Analysis

North America Market Insights

North America in the sterility testing market is anticipated to garner the highest share of 40.3% by the end of 2035. The market’s upliftment in the region is primarily fueled by pharmaceutical facility upgradation, the presence of regulatory enforcement, organizational contributions, the increased demand for kits and reagents, and generous provincial investments. According to official statistics published by Brookings in March 2026, 70% to 80% of active pharmaceutical ingredients (APIs) are increasingly utilized in the U.S., with medicines originating from other countries, such as India and China, serving as dominant suppliers. Besides, in terms of prescription drug availability in the region, the pricing strategy in the U.S. was more than 250%, in comparison to 32 OECD-based nations. In addition, cross-border pharmaceutical goods purchasing through standards supply chain dynamics is also enhancing the market exposure in the region.

2024 Pharmaceutical Goods Export and Import Analysis in North America

|

Countries |

Export (USD) |

Import (USD) |

|

U.S. |

95.7 million |

59.2 million |

|

Mexico |

14.8 million |

27.9 million |

|

Canada |

5.5 million |

10.5 million |

|

Dominican Republic |

5.7 million |

3.7 million |

|

Costa Rica |

112,000 |

901,000 |

|

Panama |

36,500 |

885,000 |

Source: OEC

The sterility testing market in the U.S. is growing significantly, owing to an acceleration in the demand for regulatory intensification, rapid novel drug approvals, the transition toward increased testing methods, and an expansion in Medicare coverage services. As stated in an article published by NLM in January 2026, the U.S. Food and Drug Administration (FDA) has successfully approved 44 newest drugs as of 2025. This readily demonstrated a minor decrease in comparison to previous years, but was suitable for overall maintaining trends in domestic pharmaceutical advancements. Based on this, biologics accounted for 25% of approvals, which included 9 monoclonal antibodies, 2 antibody-drug conjugates, and 1 fusion protein, with cancer evolving as the ultimate therapeutic focus, thereby proliferating the market expansion in the overall country.

U.S. FDA Novel Drug Therapy Approval, 2026

|

Drug Name |

Active Ingredient |

Approval Timeline |

Application |

|

Decnupaz |

Pivekimab Sunirine-pvzy |

May 2026 |

Aiding adults with blastic plasmacytoid dendritic cell neoplasm. |

|

Hepcludex |

Bulevirtide-gmod |

May 2026 |

Treating chronic hepatitis delta virus infection in adults without cirrhosis or with compensated cirrhosis. |

|

Idvynso |

Doravirine and Islatravir |

April 2026 |

Aid HIV-1 infection by replacing the present antiretroviral regimen in adults with no history of virologic treatment failure and no known substitutions associated with resistance to doravirine. |

|

Foundayo |

Orforglipron |

April 2026 |

Diminish excess body weight and maintain weight reduction in adults with obesity or overweight. |

|

Awiqli |

Insulin Icodec-abae |

March 2026 |

Optimize glycemic control in adults with Type 2 diabetes mellitus. |

|

Lifyorli |

Relacorilant |

March 2026 |

Treat platinum-resistant epithelial ovarian, fallopian tube, or primary peritoneal cancer. |

|

Loargys |

Pegzilarginase-nbln |

February 2026 |

Aid hyperarginemia in adults and pediatric patients with Arginase 1 Deficiency. |

|

Bysanti |

Milsaperidone |

February 2026 |

Treat schizophrenia and manic or mixed episodes associated with bipolar I disorder. |

|

Adquey |

Difamilast |

February 2026 |

Aiding mild to moderate atopic dermatitis. |

|

Zycubo |

Copper Histidinate |

January 2026 |

Treatment provision for Menkes disease. |

Source: FDA Government

The presence of pharmaceutical standards mandating rigorous protocols for both medical device and biologic approvals, the allocation of generous budgets for quality assurance, an expansion in domestic biosimilars and biologics industries, an increase in testing capabilities, and a surge in conducting clinical trials are certain factors that are bolstering the sterility testing market in Canada. As per an article published by the Government of Canada in May 2022, the sales of biologic medicines in the country have significantly tripled, rising from USD 3.3 billion to USD 10 billion, indicating a 10-year yearly growth rate of 13.2%, along with a 14.6% increase. Besides, the pricing strategy of these medicines usually amounts to USD 262 per person, which is more than the global median of USD 156, thereby denoting an optimistic outlook for the market expansion.

APAC Market Insights

The Asia Pacific in the sterility testing market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly attributed to the existence of an efficient manufacturing center for sterile production, suitable investments from global pharma firms, regulatory scrutiny, and the rapid adoption of microbiological methods. According to official statistics published by NLM in December 2022, South and Southeast Asia comprise the unmet demand for surgical procedures for 5,627 cases per 100,000 population. Based on this, 3.7 billion individuals are at a massive risk of catastrophic health spending. Of the roughly USD 12.3 trillion in economic loss, which is expected to be witnessed by the end of 2030, owing to surgical conditions in low and middle-income countries, USD 6.1 trillion is poised to occur in East and Southeast Asia, thereby denoting a huge growth opportunity for the market in the region.

The sterility testing market in China is gaining increased traction, owing to strict compliance standards, upgradation in manufacturers, generous investments, an escalation in drug approval pathway, an increase in the volume of biosimilars and biologics, and a focus on the assurance component. As stated in an article published by NLM in April 2025, 79 drugs have been approved in the country, with their global sales accounting for 3% of innovative drugs. Besides, as of 2023, a total of 256 drugs have also been approved in the country, constituting the highest number of drugs in comparison to other countries. In this regard, Class 1 innovative drug approvals successfully reached 101 in 2023, and meanwhile, the tally of these drugs further reached 33, denoting a 136% surge, and making it suitable for driving the market growth and expansion in the country.

The aspects of a strong biologics pipeline, mature pharmaceutical industry, strict quality controls, the development of regenerative medicine and cell therapy, innovative healthcare infrastructure, regulatory frameworks, and the adoption of bioluminescence are a few trends that are uplifting the sterility testing market in Japan. As per an article published by the ITA in November 2025, the domestic industry for non-prescription and prescription pharmaceuticals amounted to USD 88 billion as of 2023, and 93% of the industry constituted prescription pharmaceuticals. Based on this, the prescription drugs sector exceeded USD 68.9 billion as of 2022, and is projected to increase to USD 75.2 billion by the end of 2029, demonstrating a yearly growth range between 0.9% t 1.9% for 5 years, thereby positively impacting the market development in the overall country.

Japan’s Pharmaceutical Industry Size Analysis, 2022-2025 estimated

|

Components (USD Million) |

2022 |

2023 |

2024 |

2025e |

|

Industry Size |

90,275 |

87,845 |

84,042 |

87,373 |

|

Overall Exports |

8,619 |

8,745 |

8,805 |

8,981 |

|

Overall Imports |

43,815 |

33,599 |

32,536 |

33,187 |

|

U.S. Imports |

10,106 |

7,750 |

5,728 |

5,975 |

|

Trade Surplus |

6,969 |

4,643 |

3,012 |

3,513 |

|

Exchange Rates |

131.5 |

140.7 |

151.5 |

151.5 |

Source: ITA

Europe Market Insights

Europe in the sterility testing market is projected to witness considerable expansion by the end of the stipulated timeline. The market’s growth in the region is effectively driven by regulatory compliance, the existence of contamination control approaches, an increase in implementing isolator technology, a focus on a dual-tier consumer base, and strict good manufacturing practices. According to official statistics published by NLM in January 2025, in terms of pharmaceutical reforms, the average duration from marketing authority to oncology medicine availability ranged from 102 days in Germany to 991 days in Romania. Additionally, taking into consideration the availability, 98% of 46 approved medicines were available in Germany, in comparison to 2% in Malta, thereby demonstrating an overall average of 50%, which is enhancing the market growth.

The sterility testing market is gaining increased exposure in Germany, owing to the existence of the pharmaceutical manufacturing center, an increase in the production capacity, expansion in cell and gene therapy, the establishment of a regulatory authority for biologics, and the rapid adoption of microbiological methods. As stated in an article published by Germany Trade and Invest (GTAI) in 2026, the pharmaceutical industry's revenue in the country was worth USD 69.4 billion, accounting for a 6.4% yearly growth rate, along with the presence of more than 600 pharmaceutical organizations. Besides, in terms of research and development investment, domestic companies generously invested USD 11.1 billion, along with the registration of 613 patents with the European Patent Office by the domestic industry, thereby making it suitable for fueling the market growth.

The existence of a strong vaccine manufacturing ecosystem, the advanced therapy development, a suitable investment plan, innovations in biopharmaceuticals, and the presence of specialized testing protocols are a few factors that are responsible for boosting the sterility testing market in France. As per an article published by NLM in January 2025, a clinical study was conducted on a patient pool of 20 million individuals aged 25 years in the country to evaluate therapy services. The study demonstrated that there was an increase in outpatient psychiatric consultations among women, with a relative risk of 1.1 for individuals aged 13 to 17 years and 1.0 for 18 to 25 years. Moreover, there was also an increase in hospitalizations, with a relative risk of 1.07 for individuals aged 18 to 25 years. Therefore, this overall study indicates the demand for therapy for which the market is continuously expanding in the country.

Key Sterility Testing Market Players:

- Charles River Laboratories International Inc. (U.S.)

- Merck KGaA (Germany)

- bioMérieux SA (France)

- Thermo Fisher Scientific Inc. (U.S.)

- Sartorius AG (Germany)

- SGS SA (Switzerland)

- Eurofins Scientific SE (Luxembourg)

- WuXi AppTec (China)

- STERIS Plc (UK)

- Sotera Health LLC (U.S.)

- Nelson Laboratories, LLC (U.S.)

- Pacific BioLabs Inc. (U.S.)

- Becton Dickinson and Company (U.S.)

- Ecolab Inc. (U.S.)

- Toxikon Corporation (U.S.)

- Boston Analytical Inc. (U.S.)

- Azbil Telstar SL (Spain)

- Bioquell UK Ltd (UK)

- Samsung Biologics (South Korea)

- Sigma-Aldrich (Merck Group) (U.S.)

- Lonza (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Charles River Laboratories International Inc. provides comprehensive sterility testing services through its extensive network of cGMP-compliant facilities, supporting pharmaceutical and medical device clients globally. The company has strengthened its position in outsourced sterility testing through strategic acquisitions that expanded its biologics and cell therapy testing capabilities.

- Merck KGaA offers a broad portfolio of sterility testing products, including ready-to-use culture media, membrane filtration systems, and rapid microbial detection technologies. The company leverages its deep expertise in pharmaceutical quality control to serve both in-house and outsourced testing markets across Europe, America, and the Asia Pacific.

- bioMérieux SA specializes in rapid microbiological methods for sterility testing, providing automated solutions that significantly reduce time-to-result compared to traditional compendial methods. The company’s diagnostics expertise enables integrated approaches to contamination control and sterility assurance for pharmaceutical manufacturers worldwide.

- Thermo Fisher Scientific Inc. supplies sterility testing instruments, consumables, and growth media through its microbiological product lines serving quality control laboratories. The company’s extensive distribution network and manufacturing scale make it a reliable supplier for sterility testing products across all major pharmaceutical markets.

- Sartorius AG provides sterility testing systems, including membrane filtration devices, incubators, and rapid testing platforms designed for GMP-compliant pharmaceutical laboratories. The company focuses on integrating digital data management solutions into sterility testing workflows to enhance compliance and traceability.

Here is a list of key players operating in the global sterility testing market:

The sterility testing market is characterized by a diverse competitive landscape comprising specialized contract research organizations (CROs), testing service providers, and diversified life science conglomerates. Key players are pursuing strategic initiatives, including geographic expansion through acquisitions, the development of rapid microbiological methods, and the launch of advanced isolator workstations. Besides, in August 2025, bioMérieux launched GENE-UP® PRO HRM, which is the first-ever DNA-based test, commercially developed for detecting heat-resistant molds at the molecular level. This particular product was developed by partnering with Ocean Spray Cranberries, Inc., to ensure innovation, thereby making it suitable for enhancing the sterility testing industry globally.

Corporate Landscape of the Market:

Recent Developments

- In January 2026, Charles River Laboratories International, Inc. acquired K.F. Ltd. and PathoQuest SAS, with the intention of strengthening the DSA supply chain, with the transaction expected to amount to an estimated USD 0.25 per share by the end of 2026 and USD 0.6 by 2027.

- In October 2025, Lonza signed an agreement and successfully acquired Redberry SAS to effectively include the Red One™ solid-phase cytometry platform to ensure rapid sterility and bioburden testing.

- In July 2025, Thermo Fisher Scientific Inc. expanded its tactical partnership with Sanofi for enabling the addition of drug manufacturing in the U.S. by acquiring the Manufacturing facility in New Jersey.

- Report ID: 8591

- Published Date: May 29, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.