Spine Biologic Market Outlook:

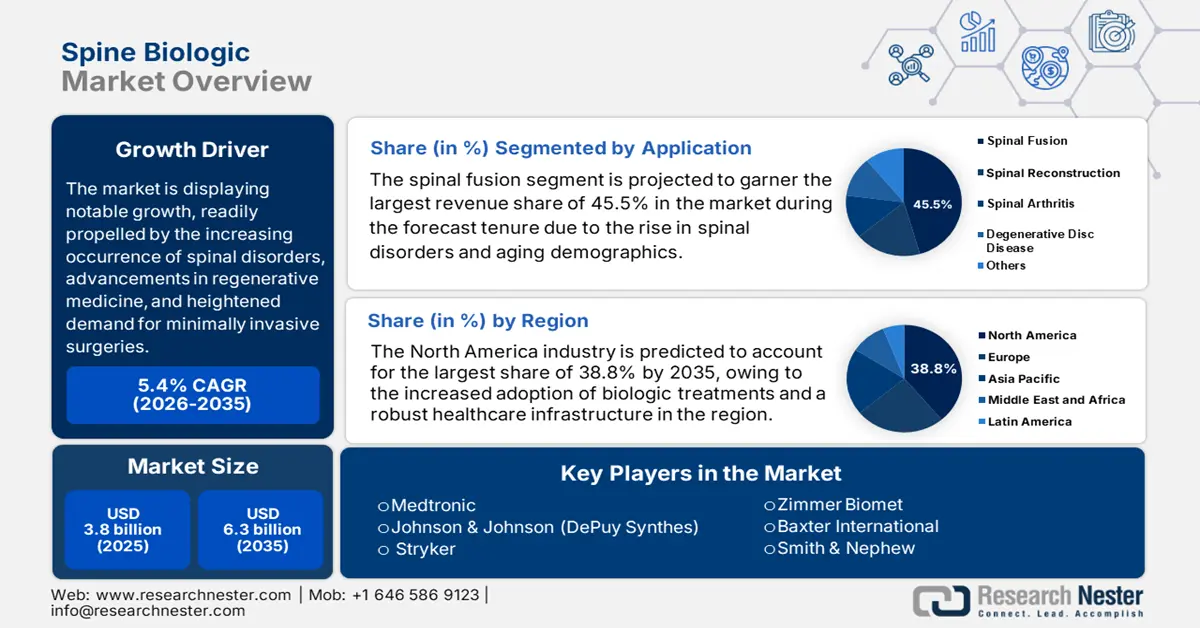

Spine Biologics Market size was valued at USD 3.8 billion in 2025 and is projected to reach USD 6.3 billion by the end of 2035, rising at a CAGR of 5.4% during the forecast period, i.e., 2026-2035. In 2026, the industry size of spine biologic is estimated at USD 4 billion.

The global market is displaying notable growth, readily propelled by the increasing occurrence of spinal disorders, advancements in regenerative medicine, and heightened demand for minimally invasive surgeries. As per an article published by the World Health Organization in April 2024, Spinal cord injury (SCI) affects over 15 million people in almost all nations, wherein most cases are a result of trauma such as falls, accidents, or violence. It also underscored that in 2021, nearly 15.4 million people were living with SCI, hence reflecting the presence of a reliable consumer base.

On the economic front, spine biologics are enabling long-term cost savings with a great reduction of revision surgeries and minimizing post-operative complications as well. Therefore, payers are increasingly recognizing these therapies due to their reduced hospital stays and enhanced patient outcomes. The report from Spine Journal in September 2021 revealed that spine care is a key target in the U.S. healthcare system’s shift to value-based models, with degenerative spinal pathologies costing around USD 80 to USD 100 billion on a yearly basis. It also underscored that Walmart mandated its 1.1 million employees undergo spine surgery only at designated Centers of Excellence to ensure quality and reduce variability in care.

Key Spine Biologics Market Insights Summary:

Regional Highlights:

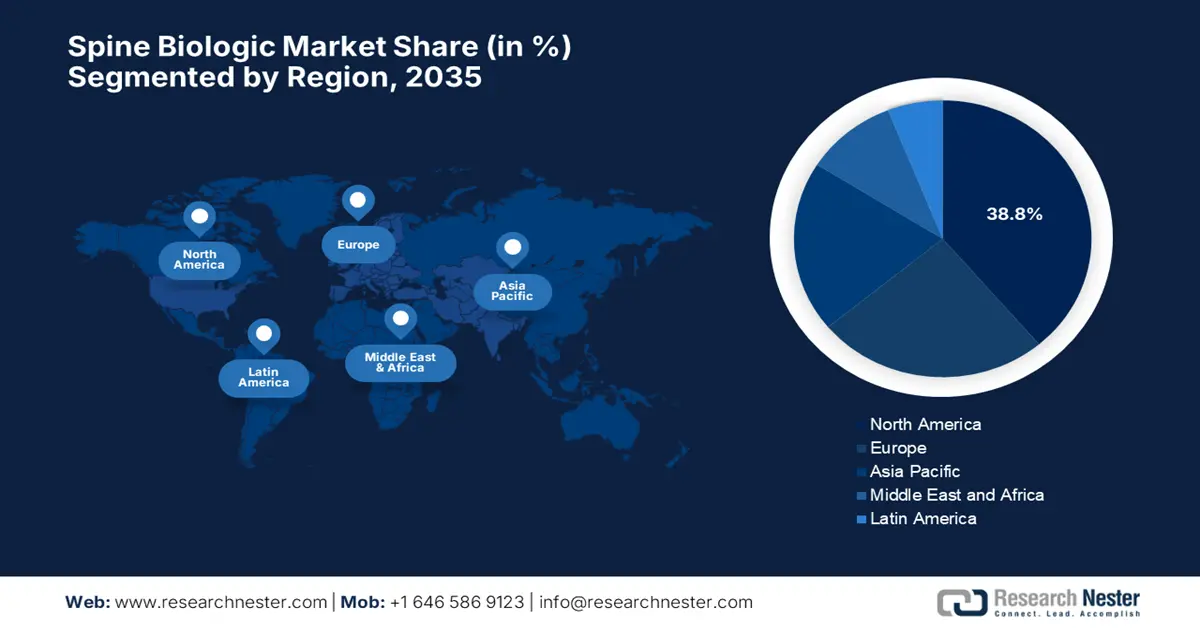

- North America is forecast to hold a 38.8% share by 2035 in the spine biologics market, bolstered by heightened biologic adoption and strong healthcare infrastructure.

- Asia Pacific is poised for the fastest expansion through 2035, accelerated by its large patient base, rising treatment awareness, and expanding healthcare infrastructure.

Segment Insights:

- The spinal fusion segment is projected to command a 45.5% share by 2035 in the spine biologics market, sustained by rising spinal disorder incidence and aging demographics.

- The hospitals segment is set to attain a 38.3% share by 2035, propelled by the need for advanced clinical infrastructure and specialist-driven surgical care.

Key Growth Trends:

- Rising aging demographic

- Continued advancements in biologic technologies

Major Challenges:

- Increasing costs & inadequate reimbursement

- Administrative obstacles

Key Players: Medtronic, Johnson & Johnson (DePuy Synthes), Stryker, Zimmer Biomet, Baxter International, Smith & Nephew, Globus Medical, NuVasive, Orthofix Medical, SeaSpine Holdings, Osstem Implant, Lotus Surgicals, Futura Medical, Biovencer Healthcare, CeramTec

Global Spine Biologics Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.8 billion

- 2026 Market Size: USD 4 billion

- Projected Market Size: USD 6.3 billion by 2035

- Growth Forecasts: 5.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: USA, Germany, China, Japan, United Kingdom

- Emerging Countries: India, Brazil, South Korea, Australia, Singapore

Last updated on : 20 August, 2025

Spine Biologic Market - Growth Drivers and Challenges

Growth Drivers

- Rising aging demographics: The market is vigorously benefiting from the presence of rising aging demographics, as age-associated musculoskeletal issues are highly prevalent. The WHO report published in October 2024 states that the people who are aged 60 and above are expected to double from 1 billion in 2020 to 2.1 billion by the end of 2050. It also reported that by the end of 2030, one out of every six people will be aged more than 60. Therefore, this demographic shift will enable a profitable business environment in this field, leading to increased demand for biologic-based spinal treatments.

- Continued advancements in biologic technologies: The aspect of continuous innovation in biologic materials, such as bone graft substitutes, growth factors, and stem cell therapies, is reshaping the foundation of the market. For instance, in March 2022 Biocomposites reported that it has signed a multiyear exclusive distribution agreement with Zimmer Biomet for the Genex Bone Graft Substitute in the U.S. It also stated that the product has been efficiently upgraded with a new closed mixing system that deliberately reduces the preparation duration and the comes with enhanced delivery options making it preferable both by surgeons and patients.

- Growing preference for biologics: There has been consistent progress in the preference for biologics over traditional bone grafting, which provides an encouraging opportunity for pioneers involved in the market. As per an ASPE July 2025 study, only 19% of off-patent biologics have biosimilars, wherein 94% of sales volume is retained by original manufacturers, highlighting the extended trust in biologic solutions. The rise of unbranded biologics, priced 25% to 50% lower, reflects the presence of strategic pricing without disrupting premium product dominance, positioning them as a preferred alternative to traditional bone grafting in spine care.

Historic Patient Growth in Musculoskeletal Diseases in the Aging U.S. Population (2015-2020)

|

Age Group |

2015 (Millions) |

2020 (Millions) |

Growth (2015-2020) |

|

10-19 |

~1.2 |

~1.3 |

+8.3% |

|

20-29 |

~2.5 |

~2.7 |

+8.0% |

|

30-39 |

~3.8 |

~4.1 |

+7.9% |

|

40-49 |

~5.0 |

~5.4 |

+8.0% |

|

50-59 |

~7.2 |

~7.8 |

+8.3% |

|

60-69 |

~9.5 |

~10.4 |

+9.5% |

|

70-79 |

~11.0 |

~12.2 |

+10.9% |

|

80-89 |

~8.0 |

~8.9 |

+11.3% |

|

≥90 |

~3.5 |

~4.0 |

+14.3% |

|

Total |

~51.7 |

~56.8 |

+9.9% (CAGR) |

Source: The Lancet Healthy Longevity May 2025

Revenue Opportunity Snapshot

|

Manufacturer |

Strategic Initiative |

Year |

Revenue Opportunity |

|

Scholar Rock |

FDA submission for Apitegromab as SMA treatment |

2025 |

Potential new revenue from SMA treatment |

|

Stryker |

Launch of Pangea Plating System with FDA clearance |

2024 |

Expanded trauma fixation devices portfolio |

|

Medtronic |

Launch of new spine surgery tech and Siemens Healthineers partnership |

2024 |

Growth in advanced spine surgery and imaging |

Source: Company Official Press Releases

Challenges

- Increasing costs & inadequate reimbursement: The lack of proper reimbursement and the expensive nature of spine biologics hamper the expansion of the market in almost all nations. The advanced materials, such as bone morphogenetic proteins, stem cell-based therapies, and synthetic graft substitutes, come with high manufacturing and storage costs, making it challenging for people from price-sensitive regions to leverage them. Also, most of the insurance providers and government payers hesitate to offer full reimbursement, classifying them as non-essential until there is strong clinical evidence, hence hindering market progression.

- Administrative obstacles: The existence of regulatory challenges is the principal factor posing significant restraint for the market to capture desired capital. The U.S. FDA distinguishes between the minimally manipulated tissues, Class III devices, and biologics under different approval pathways, such as 510(k), PMA, or Biologics License Application. On the other hand, these products necessitate extensive preclinical and clinical trial evidence, which adds to development costs, thereby delaying market entry.

Spine Biologic Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.4% |

|

Base Year Market Size (2025) |

USD 3.8 billion |

|

Forecast Year Market Size (2035) |

USD 6.3 billion |

|

Regional Scope |

|

Spine Biologic Market Segmentation:

Application Segment Analysis

The spinal fusion segment is projected to garner the largest revenue share of 45.5% during the forecast tenure. The rise in spinal disorders and aging demographics is the key factor behind the subtype’s leadership. In this regard, in November 2024, Theradaptive announced the peer-reviewed publication of a preclinical spinal fusion study featuring their lead candidate, OsteoAdapt SP, in the journal Spine. The study observed that OsteoAdapt SP promoted faster and more robust bone formation compared to the gold standard autograft in a large animal model, hence denoting a positive segment outlook.

End user Segment Analysis

The hospitals segment is set to capture a significant share of 38.3% in the spine biologic market by the end of 2035. Spinal surgeries require advanced healthcare infrastructure and specialist care, making the subtype gold standard to generate revenue in this sector. As per a July 2025 NIH article, spine surgery volumes reached 30,485 by 2023, surpassing pre-pandemic levels. It also stated that the average ICD10 diagnoses per claim rose from 9.8 in 2019 to a peak of 10.6 in 2021, stabilizing around 10.3 by 2023. Degenerative spine disease claims increased from 70.6% in 2019 to 79.5% in 2023, while spine trauma surgeries decreased from 9.4% to 8.4% indicating a wider segment scope.

Product Type Segment Analysis

The bone morphogenetic proteins (BMP) segment is expected to gain a significant share of 32.7% in the spine biologic market during the forecast tenure. The growth in the segment originates from their pivotal role in bone healing and regeneration, making them highly preferable in spine biologics. Journal of Neurosurgery in September 2023 revealed that 22,139 spinal fusion patients received BMP, with propensity score matching for age, sex, tobacco use, and surgery year. Post-surgery, 3.1% of the BMP group developed solid organ malignancies versus 3.5% in the non-BMP group. Therefore, these results indicate no increased malignancy risk associated with BMP use in thoracolumbar fusion, enabling its utilization among a wider group of audience.

Our in-depth analysis of the spine biologic market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

End use |

|

|

Product Type |

|

|

Surgery Type |

|

|

Material |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Spine Biologic Market - Regional Analysis

North America Market Insights

North America in the global spine biologic market is considered to be extremely dominating, which is set to grab the largest revenue share of 38.8% by the end of 2035. The region benefits from increased adoption of biologic treatments and a robust healthcare infrastructure. For instance, in April 2025, Roche announced that it made an investment of USD 50 billion in the U.S. over the next five years, expanding its pharmaceuticals and diagnostics operations. It also stated that the investment exclusively focuses on R&D centers, upgraded manufacturing facilities across multiple states, and a state-of-the-art gene therapy site in Pennsylvania, hence denoting a positive market outlook.

The U.S. is deliberately enhancing its presence in the regional spine biologic market on account of suitable reimbursement policies and innovations in recombinant bone morphogenic proteins and stem cell therapies. In this regard, the Centers for Medicare & Medicaid Services (CMS in February 2025 revealed that lower back pain caused by degenerative disc disease affects up to 80% of adults and costs the U.S. healthcare system between USD 19.6 billion to USD 118.8 billion on a yearly basis. Therefore, the presence of these factors drives the growing demand for advanced spine biologic treatments to restore spinal stability and reduce pain, thereby benefiting overall market growth.

Cerapedics’ Spine Biologic Milestones & Market Impact in the U.S.

|

Year |

Development Phase |

Key Achievement |

Market Impact |

|

2025 |

First Commercial Use |

First U.S. patient treated with PearlMatrix™ P-15 Peptide Enhanced Bone Graft at AdventHealth Avista post-FDA approval |

Influences $1.2 billion lumbar fusion segment as the first and only bone growth accelerator for lumbar fusion |

|

2024 |

FDA Submission |

Final PMA module submitted for P-15 Peptide Bone Graft (TLIF indication), using Bayesian Multiple Imputation |

Positioned to become Cerapedics’ second Class III drug/device combo product in lumbar spine fusion |

|

2023 |

Facility Expansion |

Cerapedics expands Denver HQ to support growth of FDA-approved i-FACTOR® and next-gen lumbar fusion product (PearlMatrix) |

Signals commercial readiness and infrastructure scaling for national rollout of advanced bone grafts |

Source: Company official Press Release

Canada in the spine biologic market is growing rapidly, facilitated by huge government funding grants. In this regard, Health Canada in March 2022 declared that the country’s federal government announced an additional USD 2 billion in one-time funding to provinces and territories to help reduce healthcare backlogs caused by the COVID-19 pandemic. This funding was intended to support hundreds of thousands of delayed surgeries and medical procedures, addressing an estimated backlog of 700,000 cases. IT also stated that the funds will be distributed equally per capita to improve timely access to high-quality, publicly funded healthcare across the country.

APAC Market Insights

Asia Pacific in the spine biologic market is representing the fastest growth due to its large patient population, increasing awareness of advanced treatment options, and expanding healthcare infrastructure across the region’s prominent countries. Also, there has been consistent progress in the demand for minimally invasive surgeries and biological solutions as well. On the other hand, the governments across the region are undertaking numerous initiatives with a key emphasis on improving healthcare access coupled with ready investments in research and investment, hence an optimistic market opportunity.

China holds a prominent position in the regional spine biologic market owing to the heightened demand for advanced surgical interventions. Besides, the government investments are on a surge, encouraging both national and international firms to operate in the country’s market. For instance, in May 2023, SpineGuard and XinRong Medical together declared that they expanded their partnership to distribute SpineGuard’s full DSG (Dynamic Surgical Guidance) product portfolio across China. They also stated that XinRong will fund the NMPA registration process for new products with a €500K equity investment, acquiring 1.28% of SpineGuard's shares, hence suitable for standard market growth.

India also follows the regional growth in the spine biologics market, which is influenced by increasing preference for both minimally invasive and biologic treatment options and the government’s financial assistance. As per a December 2023 article released by the NIC Scheme for Financial Assistance to Spinal Injury Centers (ASIC), provides critical support for spinal surgeries by funding 25 free beds at the Indian Spinal Injuries Centre (ISIC), New Delhi, and establishing State Spinal Injury Centres (SSICs) across the country. Under this initiative, eligible patients with spinal cord injuries and annual family incomes below ₹3 lakh receive free treatment and rehabilitation, with reimbursement rates of ₹7,000 per bed per day at ISIC and ₹1,000 per bed/day at SSICs.

Europe Market Insights

Europe is representing steady progress in the spine biologic market, which is due to the increasing adoption of advanced biologic-based treatments. The region also benefits from the presence of prominent manufacturers and their implementation of strategies to elevate the market potential. In this regard, BEGO Implant Systems and NovaBone entered a strategic alliance in March 2025 to enhance the distribution of advanced bone graft substitutes across the region. Also, under the agreement, BEGO will distribute NovaBone’s biocompatible, clinically proven bone regeneration products throughout the region, hence positively influencing market development.

U.K. is gaining expedited traction in the spine biologic market owing to the expanding clinical usage of regenerative therapies in spinal procedures. Besides, surgeons are increasingly adopting biologic grafts in spinal fusion surgeries. For instance, in June 2024, Osteotec reported that it entered into an alliance with Additive Surgical to bring advanced 3D-printed titanium spinal implants to the country, marking Osteotec’s entry into the spine sector. The report also underscored that the implants feature PorOssity technology, with biomimetic lattices and targeted porosity designed to enhance bone growth. This collaboration empowers UK surgeons with customizable features, thereby allowing a steady cash influx in the field.

Germany’s spine biologic market is advancing rapidly, primarily fueled by a high volume of spinal procedures and a heightened demand for biologic solutions that improve fusion rates and recovery outcomes. Therefore, in March 2023, Evonik and BellaSeno declared that they have expanded their partnership to commercialize 3D-printed, fully resorbable bone scaffolds made with Evonik’s RESOMER polymers. Also, BellaSeno has received market authorization for custom-made implants designed for large and complex bone defects, hence driving market growth.

Cost-Effectiveness: Decellularised vs. Fresh-Frozen Bone Allograft (UK) 2022

|

Parameter |

Decellularised Bone Allograft |

Fresh-Frozen Bone Allograft |

|

Total cost per surgery (£) |

£ 39,017 |

£ 16,343 |

|

Average grafts used per surgery (femoral heads) |

2.43 |

2.43 |

|

QALYs post-revision (base case) |

0.685 |

0.685 |

|

QALYs post-re-revision |

0.397 |

0.397 |

|

Discount rate applied |

3.5% per year |

3.5% per year |

Source: NIH

Key Spine Biologic Market Players:

- Medtronic

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Johnson & Johnson (DePuy Synthes)

- Stryker

- Zimmer Biomet

- Baxter International

- Smith & Nephew

- Globus Medical

- NuVasive

- Orthofix Medical

- SeaSpine Holdings

- Osstem Implant

- Lotus Surgicals

- Futura Medical

- Biovencer Healthcare

- CeramTec

The worldwide market of spine biologics is extremely united with the domination of U.S.-based pioneers such as Medtronic and Johnson & Johnson, who are emphasizing FDA-approved products. Meanwhile, the players from Europe, such as Smith & Nephew, CeramTech, are concentrating on regenerative technologies. On the other hand, player organizations based in Japan, such as Terumo & Olympics, lead in terms of ceramics and collagen scaffolds, thereby aligning with precision manufacturing strengths. Furthermore, strategic acquisitions, R&D in stem cells, and cost-focused expansion are a few assets of this merchandise, providing an encouraging market opportunity.

Recent Developments

- In June 2025, Bone Biologics Corporation stated that it had filed a U.S. patent application for its recombinant human NELL-1 (rhNELL-1) protein, with a key emphasis on bone regeneration in spinal fusion procedures. The technology is designed in such a way as to enhance bone growth and fusion outcomes.

- In February 2025, Medtronic finalized the acquisition of key nanotechnology assets from Nanovis, including its FDA-accepted OsteoSync titanium pads, to enhance the osseointegration of its PEEK spinal implants. The deal integrates Nanovis’ nanotube surface technologywhich is proven to accelerate bone fusion into Medtronic’s next-gen interbody devices.

- Report ID: 8009

- Published Date: Aug 20, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.