Silicon Capacitors Market Outlook:

Silicon Capacitors Market size was valued at USD 2 billion in 2025 and is expected to reach USD 4.1 billion by the end of 2036, registering a CAGR of 6.5% during the forecast period, i.e., 2026-2036. In 2026, the industry size of silicon capacitors is evaluated at USD 2.1 billion.

The rising demand for miniaturized and high-reliability components across different industries, including automotive, telecommunications, medical, defense and aerospace, and high-performance computing, is expected to fuel the global silicon capacitor market growth. As reported by the European Automobile Manufacturers’ Association in March 2025, around 10.6 million units of car sales took place in 2024 in Europe, an increase of 2.5% compared to 2023. Such a high rate of car sales indicates that there is a constant demand for silicon capacitors in the automobile sector for voltage stabilization, prevention of electrical disturbances, and noise suppression in vehicles.

Adequate silicon production across countries, including Spain, Australia, China, India, Ukraine, Poland, and Canada, is another factor influencing the further growth of the market. Silicon production in these countries is also massive, where automotive and other industries are rapidly expanding. For instance, as per the report by the United States Geological Survey (USGS), in 2024, China accounted for around 80% of the total estimated silicon production. It ensures a disruption-free supply of silicon wafers needed to keep the cost of producing silicon capacitors under control. Thus, the market is likely to obtain the opportunity to contribute to fulfilling the high demand for miniaturized and high-reliability components cost-effectively.

Key Silicon Capacitors Market Insights Summary:

Regional Highlights:

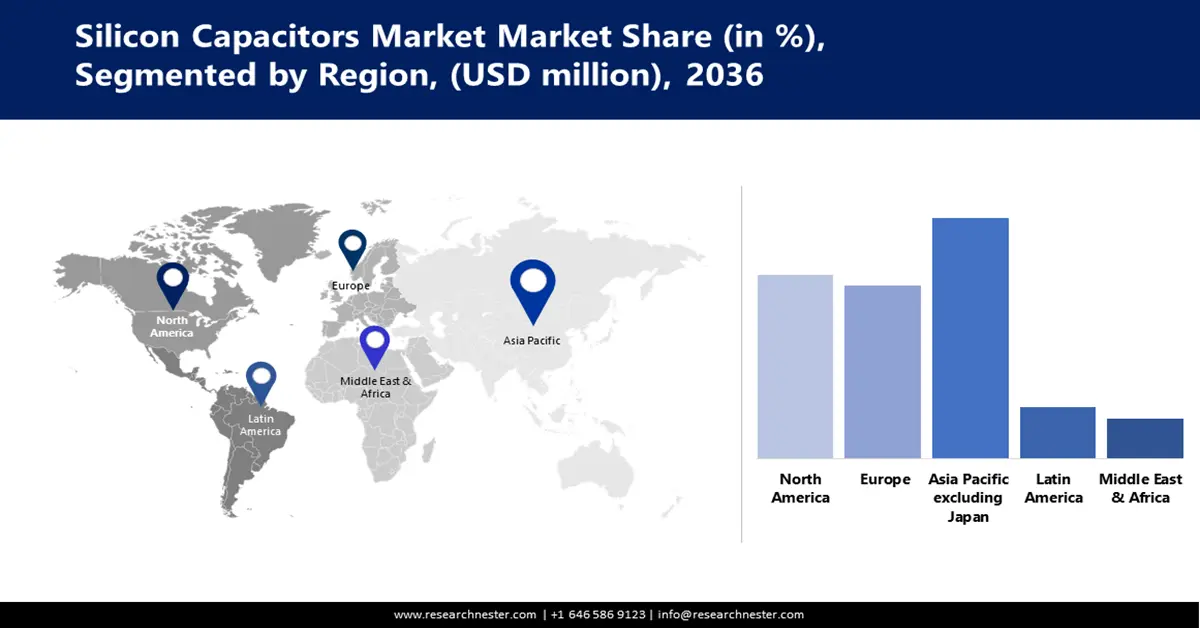

- Asia Pacific excluding Japan silicon capacitors market is projected to hold a dominant share of 49.1% by 2036, impelled by robust 5G infrastructure development and the region’s position as a global electronics manufacturing hub.

- North America silicon capacitors market is anticipated to witness a CAGR of 6.2% during 2026–2035, spurred by government-backed semiconductor production initiatives under the CHIPS Act 2022.

Segment Insights:

- The automotive segment in the Silicon Capacitors Market is expected to secure a 28.5% share by 2036, propelled by the increasing adoption of EVs and wider deployment of ADAS technologies.

- The silicon substrate segment is estimated to capture 78.4% of the market share by 2036, driven by the growing demand for miniaturized, high-reliability components in 5G infrastructure and consumer electronics.

Key Growth Trends:

- The development of implantable and portable medical devices

- Proliferation of 5G base stations and mobile devices

Major Challenges:

- The dominance of MLCCs due to scale and cost-effectiveness

- Lower capacitance values of silicon capacitors than ceramic or electrolytic types

Key Players: Vishay Intertechnology, Inc., KEMET Corporation, AVX Corporation, Samsung Electro-Mechanics, Yageo, ABB Ltd, Darfon Electronics Group, Elna, Nippon Chemi-Con Corporation, Schneider Electric, Siemens Industry Inc.

Global Silicon Capacitors Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2 billion

- 2026 Market Size: USD 2.1 billion

- Projected Market Size: USD 4.1 billion by 2036

- Growth Forecasts: 6.5% CAGR (2026-2036)

Key Regional Dynamics:

- Largest Region: Asia Pacific excluding Japan (49.1% Share by 2036)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, South Korea, Germany

- Emerging Countries: India, Taiwan, Vietnam, Mexico, Malaysia

Last updated on : 29 September, 2025

Silicon Capacitors Market - Growth Drivers and Challenges

Growth Drivers

- The development of implantable and portable medical devices: The development of implantable and portable medical devices, such as pacemakers, artificial joints, cochlear implants, intraocular lenses, portable blood pressure monitors, digital thermometers, handheld ECG monitors, and others, is expected to fuel the sales of silicon capacitors. In these medical devices, silicon capacitors are used to decouple power supplies to enable stability, high-frequency capabilities, and produce them in small sizes. Companies are continually developing novel implantable and portable medical devices, fulfilling the demand for and use of silicon capacitors. For instance, in February 2024, Butterfly Network Inc. launched Butterfly iQ3, a third-generation handheld point-of-care ultrasound (POCUS) system, incorporated with silicon capacitors. The product also received FDA approval.

- Proliferation of 5G base stations and mobile devices: The proliferation of 5G base stations and mobile devices, driven by high user adoption and widespread deployment, is expected to boost the global market growth during the forecast period. For example, in December 2024, Bharti Airtel provided Ericsson with a multi-year deal for 4G & 5G extension. As per the contract, Ericsson was supposed to deploy centralized RAN and Open RAN-ready solutions to enable network transmission with the motive to help consumers experience wider coverage and improved network capacity. A silicon capacitor is an ideal component for RAN and RAN-ready solutions as it enables decoupling of high-frequency signal filtering and others, so that the capacity and coverage area of the network can be expanded.

- Demand in ADAS, EV power modules, and infotainment: The rising demand for ADAS, EV power modules, and infotainment is boosting the demand for silicon capacitors, due to the need for miniaturized and high-reliability components. To meet such market demands, companies are investing in the production of ADAS, EV power modules, and relevant infotainment. For example, in January 2024, Qualcomm Technologies, Inc. and Robert Bosch GmbH unveiled the first central vehicle computer at CES. The computer has the capacity to run infotainment and ADAS on a single system-on-chip (SoC). In this type of single-chip, silicon capacitors play a crucial role in mitigating challenges related to power integration.

Challenges

- The dominance of MLCCs due to scale and cost-effectiveness: The industry of MLCCs has a high dominance globally and is producing a high volume of components each business year. Companies across countries, such as Japan, China, Taiwan, South Korea, and others, are actively producing MLCCs. Mass production and the use of cheap base metal electrodes help to keep the prices of MLCCs lower compared to silicon capacitors. Thus, the MLCC industry influences competitive challenges for the global market.

- Lower capacitance values of silicon capacitors than ceramic or electrolytic types: Compared to silicon capacitors, the ceramic or electrolytic capacitors contain higher capacitance values, due to high bias voltage. Companies are involved in research and development to increase capacitance values of ceramic and electrolytic capacitors. Thinner layers of insulating material are used by ceramic and electrolytic capacitors compared to silicon capacitors. Thus, the alternatives of silicon capacitors acquire a broader surface area, a key determinant of capacitance. As a result, the attractiveness of silicon capacitors decreases in terms of capacitance values.

Silicon Capacitors Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2036 |

|

CAGR |

6.5% |

|

Base Year Market Size (2025) |

USD 2 billion |

|

Forecast Year Market Size (2036) |

USD 4.1 billion |

|

Regional Scope |

|

Silicon Capacitors Market Segmentation:

Application Segment Analysis

The automotive segment is expected to account for 28.5% of market share by the end of 2036, owing to the growing adoption of EVs and the rising deployment of ADAS. As reported by the International Energy Agency (IEA), global spending for EVs exceeded USD 425 billion in 2022, an increase of 50% in relation to the previous business year. EV manufacturers are likely to adopt silicon capacitors increasingly in their production. Silicon capacitors incorporated in ADAS and EVs offer precise control over voltage fluctuation in batteries. Thus, the powertrain performance and energy management systems are enhanced in ADAS and EVs through the use of silicon capacitors.

|

Company / Brand |

Product Series (Silicon Capacitors) |

Functions / Key Features |

Automotive Highlights |

|

Murata |

ATSC, WASC |

Wire-bondable and embedded silicon capacitors; low ESL for LiDAR pulse generation (1.5 ns, 100 W), silicon IPD enables even narrower pulses (~0.9 ns, 120 W). |

AEC-Q100 certified, up to 200 °C. |

|

IPDiA |

ATS series |

Ultra-miniature silicon capacitors (0202, 0505, 0605 sizes), –55 °C to +200 °C, low ESR/ESL, low leakage (< 0.5 nA). |

AEC-Q100 qualified, automotive voltage (16 V). |

|

ROHM |

— |

Silicon capacitors (planar and trench types); stable, low profile, no piezoelectric noise; some with built-in TVS protection. |

Used across automotive systems. |

Source: Murata, ROHM

Material Segment Analysis

The silicon substrate segment, encompassing monocrystalline silicon, polycrystalline silicon, and SOI (Silicon-on-Insulator), is anticipated to acquire a revenue share of 78.4% by the end of 2036. The rising demand for miniaturized and high-reliability components in consumer electronics, and in the development of 5G infrastructures and EVs, is expected to fuel the segment growth. The dominance of the segment is also boosted by the development of silicon wafers, compatible with silicon capacitors. For instance, in October 2024, Infineon unveiled the thinnest silicon power wafer globally, capable of pushing technological boundaries and enhancing energy efficiency. The wafer has a thickness of 20 micrometers and a diameter of 300 millimeters only.

Voltage Segment Analysis

By 2036, the low voltage segment is expected to acquire 47.3% of revenue share, owing to the expansion of the consumer electronics sector. Businesses associated with the consumer electronics industry are constantly developing newer smartphone models, increasing the use of silicon capacitors. One such example is the launch of Apple’s new smartphone series, iPhone 16 and iPhone 16 Plus, in September 2024. These new models of smartphones contain new, advanced miniaturized components. For the management of power transmitted to processors in smartphones, low-voltage silicon capacitors play a crucial role. The expansion of the 5G infrastructure globally, which needs frequency filtering, decoupling, and others at higher frequencies, boosts the demand for low-voltage silicon capacitors.

Our in-depth analysis of the market includes the following segments:

|

Segments |

Subsegments |

|

Application |

|

|

Material |

|

|

Voltage |

|

|

Product |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Silicon Capacitors Market - Regional Analysis

Asia Pacific Excluding Japan Market Insights

Asia Pacific excluding Japan silicon capacitors industry is expected to emerge as a dominating one by acquiring a share of 49.1% by the end of 2036, on account of the region’s exposure as the hub of electronics manufacturing globally. Robust 5G infrastructure development is another significant factor fueling the market growth. As revealed by the GSM Association in July 2025, around USD 220 billion was spent in the Asia Pacific on different technological advancements. The majority of financial capital was earmarked for the development of 5G infrastructure.

The market in China is anticipated to witness a robust expansion at a CAGR of 7.7% during the forecast period, as a consequence of the investment by the government for the development of semiconductor manufacturing. As reported by the University of California Institute on Global Conflict and Cooperation (IGCC), in May 2024, the government decided to pump an investment of USD 47.5 billion into the development of the semiconductor industry. The emergence of China as the largest manufacturer of automotive products also fuels the demand for silicon capacitors to be incorporated in vehicles.

India is expected to emerge as an expanding silicon capacitors market at a CAGR of 8.8% between 2026 and 2036, due to the motive of government to reduce import dependence. This has led the government to invest in the establishment of a favorable environment that is likely to be highly compatible with electronics manufacturing. In March 2025, the Press Information Bureau (PIB) disclosed that the government of India increased funding to USD 1.0 billion from USD 652.1 million for the development of technologies. Such financial support increases the scope of accessing adequate funding required for the production of silicon capacitors. Rising adoption of EVs across India also fuels the demand for silicon components. Growing electronics production in India is also expected to boost the demand for silicon capacitors. Electronics production in India is likely to reach USD 500 billion by 2030 from USD 155 billion in 2023. The expansion of the consumer electronics sector in India is driven by government support, demand among consumers, and the proliferation of national supply chain capacity.

North America Market Insights

North America silicon capacitors market is anticipated to expand at a CAGR of 6.2% during the forecast period, due to the expansion of industries, including automotive, IT and telecommunication, consumer electronics, aerospace and defense, fueling the demand for silicon capacitors. Support from the governments also drives innovation and increased production in North America. As reported by the Council on Foreign Relations in April 2024, the announcement of the CHIPS Act 2022 in the U.S. is significantly promoting the production of semiconductors. Adhering to the law, the government invested USD 53 billion to boost the production of semiconductors, fueling the demand for silicon capacitors.

The silicon capacitors market in the U.S. is expected to witness rapid growth during the forecast period, owing to demand for ultra-wide bandgap semiconductors in the defense sector. Companies are also initiating the production of the same, fueling the use of silicon capacitors across a variety of applications. The development of 5G infrastructure across the country also fuels the market growth by influencing the increasing use of the component. Governmental bodies significantly support the development of 5G infrastructure in the U.S., influencing the rising adoption of silicon capacitors. For instance, in September 2023, the National Science Foundation (NSF) announced funding of USD 25 million for the advancement of 5G communication infrastructure and to overcome relevant challenges.

The silicon capacitors market in Canada is anticipated to experience a robust expansion between 2026 and 2036, owing to government efforts towards zero emissions through the promotion of EV adoption. The development of EV charging infrastructure is another factor that is fueling the demand for silicon capacitors to be used as the advanced power management component. Such a development is driven by investment by companies operating in the automotive sector. For example, a subsidiary of Volkswagen Group, Electricity Canada, inaugurated 68 new DC fast chargers between March 2024 and March 2025. The establishments were initiated across New Brunswick and Nova Scotia.

Europe Market Insights

Europe silicon capacitors market is anticipated to expand at a CAGR of 5.6% throughout the forecast period, due to the growing demand for miniaturized medical devices to achieve enhanced mobility, continuous tracking of health, and access to personalized care options. The initiatives by regulatory bodies to foster the development of telecom infrastructure also boost the demand for silicon capacitors for filtering purposes and to incorporate in the impedance-matching circuits. As per the report by the GSM Association, published in January 2025, around 30% of the mobile connections in Europe were based on 5G in 2024. By 2030, 80% of the connections across the region are likely to be 5G.

The market in Germany is anticipated to expand at a 6.4% CAGR during the forecast period, on account of increasing investment in smart manufacturing. Companies are investing heavily to contribute to the establishment of Industry 4.0. The government is also supporting the establishment of enhanced smart manufacturing, increasing the adoption of silicon capacitors. Silicon capacitor manufacturers based in Germany are also developing silicon carbides to enable smart manufacturing and cater to the need for silicon capacitors.

The UK silicon capacitors market is anticipated to expand at a CAGR of 6.1%, as a consequence of the zero-emission vehicle mandate imposed by the government. In January 2024, the government announced the zero-emission vehicle (ZEV) mandate for automotive manufacturers. The aim was to provide a wider range of EV options to consumers. The announcement also obligated to enable of a minimum proportion of sales of zero-emission vehicles, increasing the need to use silicon capacitors. The advancement of 5G infrastructure across the country is also increasing the use of silicon capacitors.

Key Silicon Capacitors Market Players:

- Vishay Intertechnology, Inc.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- KEMET Corporation

- AVX Corporation

- Samsung Electro-Mechanics

- Yageo

- ABB Ltd

- Darfon Electronics Group

- Elna

- Nippon Chemi-Con Corporation

- Schneider Electric

- Siemens Industry Inc

The competitive landscape of the global silicon capacitors market is dominated by a few numbers of component suppliers and conglomerates of semiconductors. These companies account for the majority of the revenue share and make the market moderately concentrated. Key players associated with the market are also collaborating with other industrial organizations to supply silicon capacitors seamlessly, so that a disruption-free production of items that need silicon capacitors can be enabled. Businesses associated with the industry are also supported by the government for the production and development of silicon capacitors.

Below is the list of the key players associated with the global silicon capacitor market:

Recent Developments

- In September 2025, Samsung revealed its involvement in bulk production of silicon capacitors. Last year, it supplied the components to the customers, and now it has enabled mass production for AI servers and high-performance semiconductor packages.

- In November 2024, Murata Manufacturing Co., Ltd. announced the establishment of a new 200-mm mass production line. The initiative was taken with the motive of bolstering the organizational capabilities of silicon capacitor production.

- In March 2024, a leading company supplying customized memory solutions, AP Memory, unveiled its newly developed generation stack silicon capacitor (S-SiCapTM) Gen3. It is a very low profile (<100um thin) and high capacitance density silicon capacitor, compatible with System-on-Chip (SoC).

- Report ID: 8137

- Published Date: Sep 29, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2036

Copyright @ 2026 Research Nester. All Rights Reserved.