Silicon on Insulator Market Outlook:

Silicon On Insulator Market size was valued at USD 2.1 billion in 2025 and is projected to reach USD 8.1 billion by the end of 2035, rising at a CAGR of 15% during the forecast period, i.e., 2026-2035. In 2026, the industry size of silicon on insulator is estimated at USD 3.5 billion.

The silicon on insulator market is undergoing a sophisticated global supply chain that includes the procurement of ultra-high-purity silicon, advanced fabrication methods, and international distribution networks. Key production techniques such as SIMOX (Separation by IMplantation of OXygen), wafer bonding, and Smart Cut require highly specialized materials and precision engineering, often relying on cross-border sourcing. As a result, the market is sensitive to global political and economic instability. For instance, supply interruptions of high-purity silicon or critical implantation tools can significantly delay manufacturing and inflate costs. The global migration of SOI wafers and associated inputs is also controlled by trade regulations and tariffs, which directly impact pricing and product availability across regions.

Technological advancement remains a primary driver for the SOI industry. Government bodies and research institutions have substantially invested in improving SOI technologies. The U.S. Department of Energy, for instance, has backed research into next-generation semiconductor materials and fabrication technologies, which may improve SOI performance and reduce costs. These initiatives target improved wafer quality and wider applicability in sectors such as automotive and telecom. Public-private collaborations further accelerate commercialization, allowing laboratory innovations to scale to industrial production. Although specific investment figures are not provided, the trajectory clearly reflects continued strategic investment in SOI R&D.

Key Silicon on Insulator Market Insights Summary:

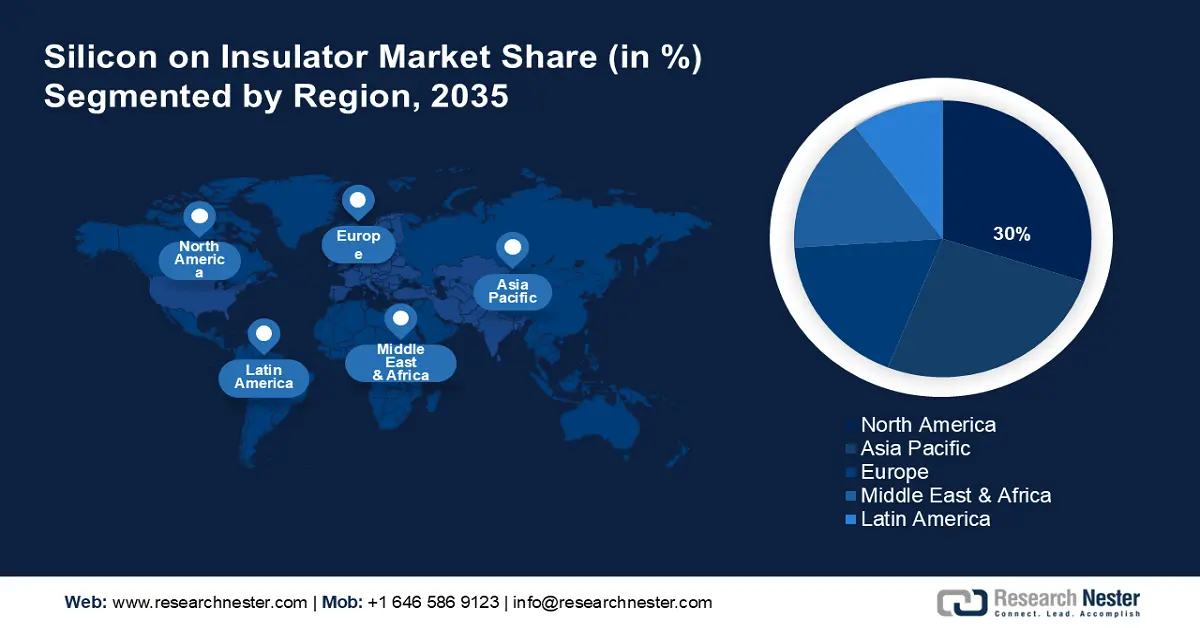

Regional Insights:

- North America is expected to register a 30% share by 2035, fueled by rising demand across modern communication and automotive industries.

- Asia Pacific is projected to grow at 16.5% during the forecast period, impelled by its pivotal role in semiconductor manufacturing and rising adoption of high-performance, low-power electronics.

Segment Insights:

- The Fully Depleted SOI (FD-SOI) segment is projected to account for a 39.5% share by 2035, owing to its superior energy efficiency and performance benefits.

- The Radio-Frequency Front-End Module (RF FEM) segment is anticipated to hold a 58.5% share by 2037, driven by the global rollout of 5G networks and rising demand for high-frequency communication devices.

Key Growth Trends:

- Rising demand for energy-efficient semiconductors

- Expansion of 5G and advanced RF applications

Major Challenges:

- High manufacturing costs

- Complexity in fabrication and design

Key Players: Soitec SA, GlobalWafers Co., Ltd., GlobalFoundries Inc., STMicroelectronics, ON Semiconductor Corporation (onsemi), NXP Semiconductors N.V., Tower Semiconductor Ltd., United Microelectronics Corporation, Siltronic AG, Okmetic Oy, Silicon Valley Microelectronics Inc., SUMCO Corporation, Shin-Etsu Chemical Co., Ltd., Murata Manufacturing Co., Ltd., Sony Semiconductor Solutions Corp.

Global Silicon on Insulator Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.1 billion

- 2026 Market Size: USD 3.5 billion

- Projected Market Size: USD 8.1 billion by 2035

- Growth Forecasts: 15% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (30% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Japan, South Korea, Germany, China

- Emerging Countries: India, Taiwan, Singapore, Israel, Vietnam

Last updated on : 8 September, 2025

Silicon on Insulator Market - Growth Drivers and Challenges

Growth Drivers

- Rising demand for energy-efficient semiconductors: The transition to low-power electronics is a primary driver for SOI adoption, especially through FD-SOI technology. FD-SOI allows up to 40% lower power consumption as compared to traditional bulk CMOS, making it suitable for battery-powered devices like smartphones, IoT sensors, and wearables. As energy efficiency becomes a design priority in all electronics sectors, the advantages of FD-SOI in minimizing leakage current and optimizing thermal performance continue to support demand.

- Expansion of 5G and advanced RF applications: The expansion of 5G infrastructure worldwide is significantly boosting the adoption of Radio Frequency SOI (RF-SOI). According to a report by 5G Americas, with 2.25 billion 5G connections globally in 2024, the global wireless telecommunications sector reached a significant milestone. RF-SOI substrates offer extremely superior signal quality and integration for RF front-end modules used in 5G smartphones and base stations. The scalability and efficiency of RF-SOI make it a foundational technology for high-frequency communication systems.

- Rising adoption in automotive and industrial sectors: SOI's built-in radiation hardness and thermal stability make it ideal for harsh environments such as automotive and industrial systems. In Advanced Driver Assistance Systems (ADAS), electric vehicles, and Micro-Electro-Mechanical Systems (MEMS), SOI provides high reliability under severe conditions. For instance, auto manufacturers such as BMW, Ford, Mercedes-Benz (Daimler Chrysler), GM, and VW are using SOI based chips in autonomous driving, infotainment, and automotive networking protocols. In January 2023, Mercedes-Benz partnered with Wolfspeed to deliver silicon carbide power semiconductors. Wolfspeed's SiC semiconductors will be utilized by Mercedes-Benz in the electric vehicles' future platform drive systems.

Challenges

- High manufacturing costs: The high production cost of SOI wafers compared to conventional bulk silicon wafers is a significant challenge to the SOI market. SOI manufacturing includes complex processes such as Smart Cut, SIMOX, and wafer bonding, all of which require specialized equipment, precision engineering, and high-purity materials. These processes significantly increase the capital and cost of operational expenditures. This pricing gap restricts adoption in cost-sensitive segments such as entry-level consumer electronics or emerging market devices. Furthermore, the limited number of SOI wafer suppliers worldwide, such as Soitec and Shin-Etsu, contributes to supply constraints and pricing rigidity, making it harder for new entrants or small-scale manufacturers to compete effectively.

- Complexity in fabrication and design: Creating integrated circuits on SOI substrates adds further complications as compared with bulk silicon processes. In addition, not all design teams or foundries have the skill sets, nor do they have the EDA tool capabilities, to realize all those benefits. Blue Chip organizations see these hurdles as risks that contribute to falling back into bulk technologies. Addressing and simplifying the SOI design ecosystem will be key for organizations that truly want to change and embrace SOI.

Silicon on Insulator Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

15% |

|

Base Year Market Size (2025) |

USD 2.1 billion |

|

Forecast Year Market Size (2035) |

USD 8.1 billion |

|

Regional Scope |

|

Silicon on Insulator Market Segmentation:

Wafer Type Segment Analysis

The Fully Depleted SOI (FD-SOI) segment is poised to account for a 39.5% share throughout the forecast timeline owing to its superior energy efficiency and performance benefits. FD-SOI wafers allow up to 40% lower power consumption and reduced leakage current, making them ideal for low-power applications like wearables, smartphones, and IoT devices. Additionally, the FD-SOI tech solves a vital pain point by providing outstanding heat management, which is significant in 5G and automotive electronics. In terms of deployment, leading semiconductor manufacturers such as GlobalFoundries and Samsung have adopted FD-SOI for advanced node development.

Product Segment Analysis

The Radio-Frequency Front-End Module (RF FEM) segment is anticipated to account for a significant revenue share of 58.5% by the end of 2037 due to the global rollout of 5G networks and rising demand for high-frequency communication devices. RF FEMs built on SOI substrates offer superior signal integrity, reduced power loss, and better integration of multiple RF components. The heightened demand is set to emerge from economies that have been at the forefront of nationwide 5G penetration, as the segment is pivotal in the push for advanced wireless connectivity.

Technology Segment Analysis

Smart Cut continues to be the most significant category because the technology is well-suited for producing high quality, ultra-thin SOI wafers with excellent performance and uniformity. As demand for low-power-consuming high-performance chips rises, so will the use of smart cut technology. The versatility of smart cut also allows manufacturers to alter wafer specifications to suit unique and wide-ranging applications, and in turn allows for more design flexibility. The continued development of the 5G, AI, and electric vehicle markets fuels the adoption of smart cut technology.

Our in-depth analysis of the silicon on insulator market includes the following segments:

|

Segment |

Subsegments |

|

Wafer Type |

|

|

Product |

|

|

Technology |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Silicon on Insulator Market - Regional Analysis

North America Market Insights

The North America silicon on insulator market is expected to register a dominant revenue share of 30% by the end of 2035, due to rising demand across the modern communication and automotive industries. Increased investment in smart infrastructure and edge computing is increasing the use of SOI wafers due to their low power consumption and thermal efficiency. Top players in the region are broadening manufacturing capacity by collaborating with government agencies on semiconductor innovation. Additionally, the strong semiconductor ecosystem in North America supports R&D and streamlines market integration.

The U.S. silicon-on-insulator market is expanding rapidly due to substantial government funding and private sector innovation in high-performance electronics. Programs such as the CHIPS Act and BEAD are motivating domestic semiconductor capabilities, indirectly promoting SOI-based technologies. The rollout of 5G and autonomous vehicle development is leading to demand for RF-SOI and FD-SOI solutions. U.S. companies are highly utilizing AI and IoT advancements, where SOI's energy efficiency offers an added advantage. As of 2023, the U.S. was a key player in patents and research output related to SOI applications, reinforcing its leadership in the global market.

The Canada Silicon-on-Insulator (SOI) market is thriving and growing, with several trends combining to create a tremendous market opportunity. Canada's dedicated and near-permanent semiconductor R&D ecosystem, largely supported by leading universities and government support, is driving innovation in SOI technologies and applications. Government investments and funding programs enhance the advancement of semiconductor capabilities, creating opportunities for further growth with foreign investment. Emphasis on clean technology also brings emphasis to the use of energy-efficient SOI components, such as in electric vehicles and batteries.

Asia Pacific Market Insights

Asia Pacific is projected to exhibit the fastest growth of 16.5% during the forecast period due to the region’s key role in semiconductor manufacturing globally and rising demand for high-performance, low-power electronics. Countries such as China, South Korea, and Japan are accelerating the adoption of SOI-based solutions to support advancing 5G infrastructure, EV production, and consumer electronics. Regional foundries are also forming strategic partnerships to advance FD-SOI and RF-SOI capabilities. The market is further propelled by favorable government policies and regional supply chain integration.

China is anticipated to lead the Asia-Pacific market in revenue by the end of 2037, fueled by its national push for semiconductor self-sufficiency and high-end chip development. The Ministry of Industry and Information Technology (MIIT) has prioritized funding for next-generation IC technologies, including FD-SOI, to reduce dependence on imports. Major foundries in the country are expanding production of silicon to address huge demand from 5G, smart manufacturing, and AI industries. In 2023, SOI-based RF chips recorded a notably higher integration in domestic smartphone brands. Additionally, government-backed research institutions are driving innovation in SOI processes, keeping China as a rising force in the global SOI landscape.

The India SOI market is rapidly growing, due to many factors driving demand and development in the semiconductor industry. With India’s rapidly growing electronics manufacturing industry focused on producing electronics hardware, many changes are influencing the industry supply chain to adopt SOI. The growing demand for energy-efficient and high-performance chips in automotive, consumer electronics, and telecommunications. Established global companies are aligning with India, and technology transfer is helping strengthen local industry segments, strengthening their capabilities for the next generation impact of semiconductor technologies.

Europe Market Insights

The Europe silicon-on-insulator (SOI) market is experiencing strong growth, particularly with the regional commitment to advanced semiconductor technologies. With Europe as a leader in electric vehicles (EVs) and autonomous driving technologies, demand for SOI wafers is expected to grow significantly. Due to their high reliability, lower power requirements, and improved thermal management, SOI is positioned to meet the rapid demands of automotive applications. Additionally, European governments and the EU launched a number of funding programs and strategic initiatives to increase semiconductor manufacturing.

The SOI market in France is expanding quickly because of the country’s unique emphasis on semiconductor development and its leadership position in global SOI wafer manufacturing. The expanding automotive and aerospace sectors are a panoply of SOI technology development. SOI technology is being used to develop energy-efficient, high-performance power chips mandated by regulations requiring electric vehicles, autonomous systems, and avionics. The French government is also funding advanced manufacturing initiatives and research collaborations to develop SOI Smart Cut wafer technology. The demand for 5G infrastructure and Internet of Things (IoT) sensors is also creating demand for SOI wafers.

Germany's SOI market growth is largely fueled by the industrial backbone of the country. As the world leader in electric vehicle production and in Industry 4.0 technologies, Germany is increasingly dependent on SOI-BASED semiconductors given their low power consumption, high reliability, and favorable thermal management. Germany can also leverage European Union funding to boost the semiconductor supply chain and reduce dependency on non-native chips. Increased demand for 5G growth and increasingly smart devices also leads many other businesses away from ANSI into SOI applications, making Germany a major growth market for SOI in Europe.

Key Silicon on Insulator Market Players:

- Soitec SA

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- GlobalWafers Co., Ltd.

- GlobalFoundries Inc.

- STMicroelectronics

- ON Semiconductor Corporation (onsemi)

- NXP Semiconductors N.V.

- Tower Semiconductor Ltd.

- United Microelectronics Corporation

- Siltronic AG

- Okmetic Oy

- Silicon Valley Microelectronics Inc.

- SUMCO Corporation

- Shin-Etsu Chemical Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Sony Semiconductor Solutions Corp.

The global silicon on insulator market features a competitive landscape of both established leaders and emerging contenders, competing through technological innovation and market expansion. Dominant players such as Shin-Etsu Chemical and Soitec maintain their higher edge with strong R&D efforts and strategic partnerships. Meanwhile, Japanese firms such as Murata and Sony are applying their strengths in materials science and miniaturization to address the rising demand for SOI in sectors like consumer electronics and automotive. These initiatives reflect the sector’s dedication to innovation, resilience, and meeting evolving ICT industry demand. Given below is a table of the top players in the market with their respective shares.

Recent Developments

- In March 2025, Shin-Etsu Chemical introduced a renewable energy project in Rayong Province, Thailand, using a biomass cogeneration system powered by locally sourced wood chips. Implemented with NS-OG Energy Solutions (Thailand) Ltd., the project is set to cut greenhouse gas emissions by about 48,000 tons annually, underscoring Shin-Etsu’s promise of sustainable SOI wafer production.

- In December 2024, Soitec collaborated with GlobalFoundries to supply 300mm RF-SOI wafers for GF’s new 9SW radio platform, targeted at powering advanced 5G and Wi-Fi solutions. This alliance supports the growing demand for high-efficiency, compact RF chips essential for next-gen wireless technologies like 5 G-Advanced and future 6G applications.

- Report ID: 5270

- Published Date: Sep 08, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.