Satellite Propulsion System Market Outlook:

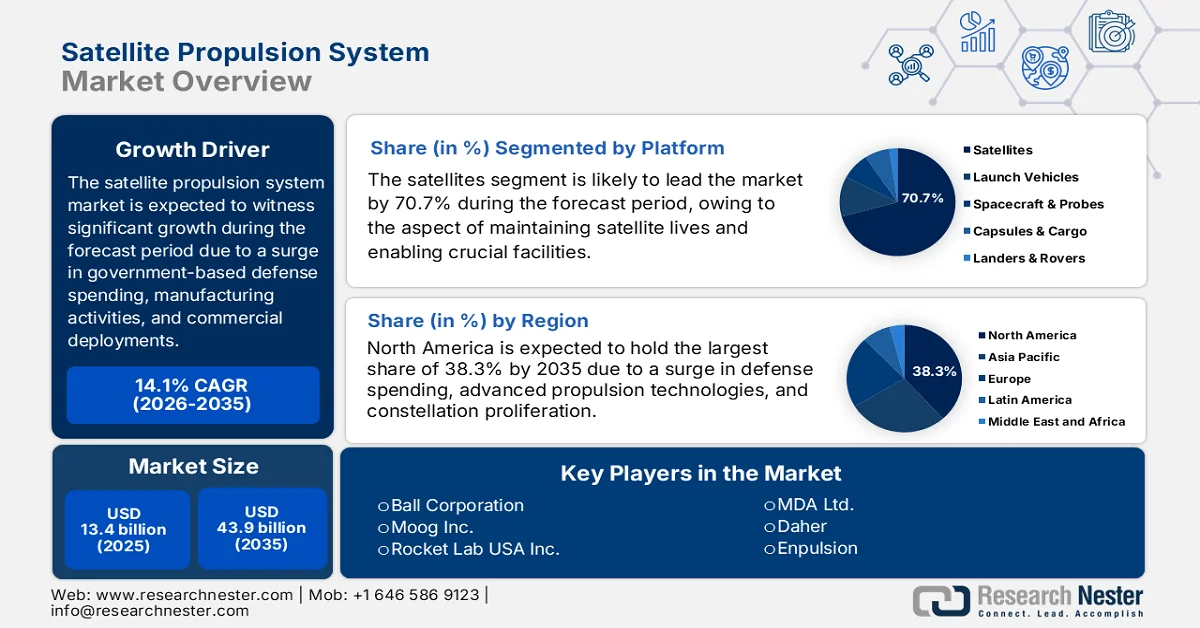

Satellite Propulsion System Market size was valued at over USD 13.4 billion in 2025 and is expected to reach USD 43.9 billion by the end of 2035, growing at a CAGR of 14.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of satellite propulsion system is evaluated at USD 15.2 billion.

The worldwide satellite propulsion system market is significantly expanding, owing to foundational factors such as government defense spending, commercial mega-constellation deployments, structural transformation of manufacturing paradigms, tactical reorientation toward in-orbit services, and the integration of AI into propulsion management. According to official statistics published by the Satellite Industry Association (SIA) in June 2022, a total of 1,713 commercial satellites have been deployed, denoting an increase by more than 40%. In addition, a total of 4,582 satellites are readily circling the earth, indicating an upsurge by 179% over the past 5 years. Besides, the commercial satellite industry is continuing to dominate, with an increase to USD 279 billion and also accounting for 72% of the global space business, thus making it suitable for bolstering the market growth.

Furthermore, the additive manufacturing for propulsion components, growth in the propellant refueling and in-orbit servicing infrastructure, AI-implemented propulsion management systems, and the presence of modular propulsion kits for rapid integration are certain trends that are fueling the satellite propulsion system market globally. As stated in an article published by the International Journal of Hydrogen Energy in November 2024, the aviation industry is anticipated to account for a 20% increase by the end of 2040, demonstrating a surge in the fuel demand of almost 38% or 120 billion liters, which is projected only in the U.S. Additionally, this growth is further predicted to cause a 12% upsurge in emissions in this industry. Besides, the industry caters to challenging targets for diminishing carbon dioxide content per passenger by 75%, along with nitrogen oxide emissions by 90% by the end of 2050, which is positively impacting the market development.

Key Satellite Propulsion System Market Insights Summary:

Regional Highlights:

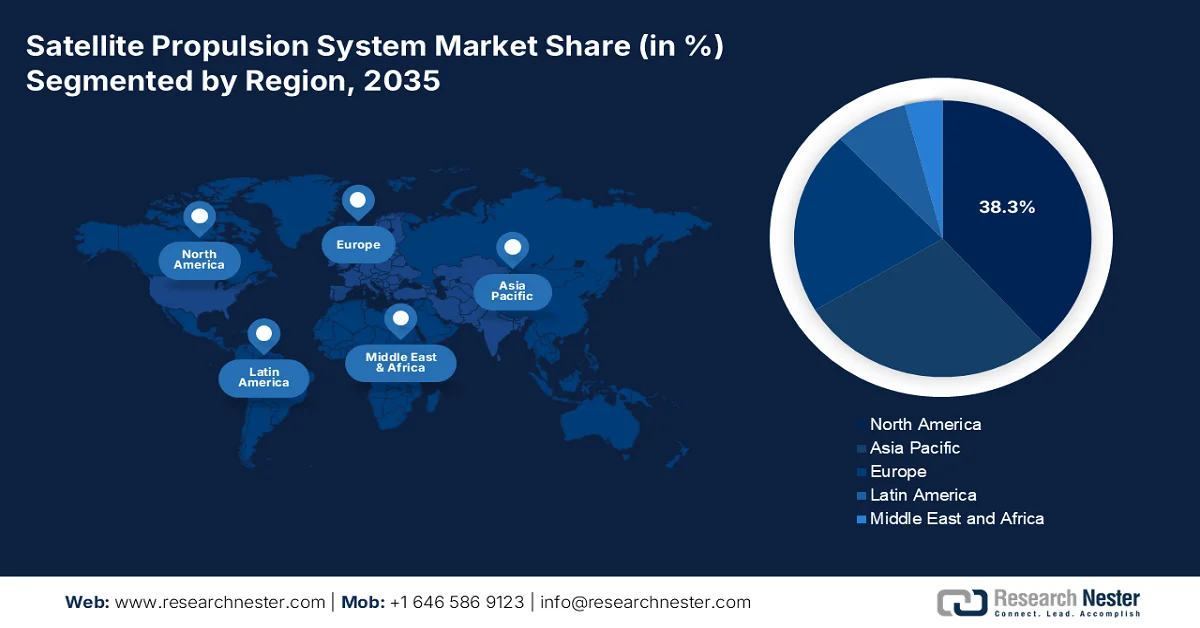

- North America is anticipated to capture a dominant 38.3% share of the satellite propulsion system market by 2035, fueled by rising defense expenditure and rapid expansion of LEO satellite constellations.

- Europe is expected to witness the fastest growth during 2026–2035, propelled by increasing government investments and a strong shift toward green propulsion technologies.

Segment Insights:

- The satellites sub-segment is projected to account for a leading 70.7% share of the satellite propulsion system market by 2035, driven by its critical role in satellite maneuvering, lifespan extension, and essential orbital functions.

- The large satellites (>1,000 kg) segment is poised to secure the second-highest share by 2035, impelled by its extensive utilization in defense, telecommunications, and high-power space missions.

Key Growth Trends:

- The commercialization of deep-space and lunar infrastructure

- The shift to non-xenon electric propulsion

Major Challenges:

- Regulatory, export control, and compliance complexities

- Technological obsolescence and integration risks

Key Players: Northrop Grumman Corporation (U.S.), Lockheed Martin Corporation (U.S.), The Boeing Company (U.S.), L3Harris Technologies Inc. / Aerojet Rocketdyne Holdings Inc. (U.S.), Space Exploration Technologies Corp. (SpaceX) (U.S.), Blue Origin LLC (U.S.), Safran S.A. (France), Airbus Defence and Space (France), Thales Alenia Space (France), ArianeGroup GmbH (France/Germany), OHB SE (Germany), Mitsubishi Electric Corporation (Japan), IHI Corporation (Japan), Ball Corporation (U.S.), Moog Inc. (U.S.), Rocket Lab USA Inc. (U.S.), Bellatrix Aerospace Private Limited (India), Indian Space Research Organization (ISRO) (India), Rafael Advanced Defense Systems Ltd. (Israel), MDA Ltd. (Canada), Daher (France), Enpulsion (Austria).

Global Satellite Propulsion System Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 13.4 billion

- 2026 Market Size: USD 15.2 billion

- Projected Market Size: USD 43.9 billion by 2035

- Growth Forecasts: 14.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.3% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, Germany, Netherlands, China, Japan

- Emerging Countries: India, Brazil, South Korea, Mexico, Indonesia

Last updated on : 27 March, 2026

Satellite Propulsion System Market - Growth Drivers and Challenges

Growth Drivers

- The commercialization of deep-space and lunar infrastructure: The successful establishment of planned lunar gateways, commercial space stations, and surface habitats has developed the need for propulsion systems, which, in turn, is positively uplifting the satellite propulsion system market globally. As per an article published by Georgia Tech in October 2025, almost 10 to 20 satellite missions are predicted to head towards the moon in the upcoming few years. Besides, cislunar space is expanding from geostationary orbit out to the moon, demonstrating an area with a suitable volume 2,000 times large that the Earth’s orbital area. Simultaneously, each of the 50 satellites in the lunar orbit requires the ability to maneuver 4 times every year on average to overcome potential crashes, which is suitable for the satellite propulsion system market development.

- The shift to non-xenon electric propulsion: The volatile pricing strategy and restricted availability of xenon, which is the propellant choice for electric thrusters, have escalated the adoption and development of alternative propellants, which are driving the satellite propulsion system market. This particular shift is highly fueled by the economic realities of mega-constellations needing different thrusters, wherein propellant expenses represent a suitable operational expenditure. As stated in a data report published by the High Power Electric Propulsion Laboratory in December 2024, the 3,000 HET Hall Thruster, launched in 2022, accounts for 150 to 500 watts of power, along with a 9 to 22 mN thrust, 1,100 to 1,700 Kr second, and 0.2 to 0.3 efficiency, denoting a huge growth opportunity for the market.

- Vertical integration among satellite operators: The presence of satellite constellation operators is increasingly internalizing propulsion manufacturing capabilities rather than depending on third-party suppliers. Based on an article published by ISRO in April 2023, the present space object propulsion comprises over 7,000 operational satellites that are orbiting the Earth at varying altitudes with different pieces of space debris. Moreover, a total of 2,533 objects from 179 launches have been successful as of 2022, in comparison to 1,860 objects from 135 launches. These particular launches denote a 32% increase in launches, along with a 36% increase in the number of objects significantly inserted in orbit. Therefore, with such continuous developments in satellite operations, there is a huge demand for vertical satellites, which is uplifting the satellite propulsion system market.

Challenges

- Regulatory, export control, and compliance complexities: The satellite propulsion system market is heavily constrained by a dense web of international, national, and intergovernmental regulations that govern the development, transfer, and deployment of space technologies. Besides, export control regimes, most notably the International Traffic in Arms Regulations (ITAR) in the U.S., classify many propulsion systems, components, and technical data as defense articles, imposing stringent restrictions on foreign collaboration, data sharing, and international sales. While ITAR serves national security objectives, it simultaneously fragments the global supply chain, limits market access for non-U.S. manufacturers, and complicates joint development programs between allied nations.

- Technological obsolescence and integration risks: The rapid pace of technological advancement in the satellite propulsion system market creates a persistent risk of obsolescence for both hardware and intellectual property, challenging manufacturers to balance innovation with the long lifecycle requirements of space systems. A propulsion system designed today may face competition from more efficient electric thrusters, novel propellant combinations, or entirely new architectural paradigms, such as in-space servicing and refueling, by the time it achieves flight qualification. This compression of technology cycles is particularly acute in the commercial sector, where operators of large constellations demand continuous improvements in specific impulse, thrust-to-power ratios, and cost per unit.

Satellite Propulsion System Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

14.1% |

|

Base Year Market Size (2025) |

USD 13.4 billion |

|

Forecast Year Market Size (2035) |

USD 43.9 billion |

|

Regional Scope |

|

Satellite Propulsion System Market Segmentation:

Platform Segment Analysis

The satellites sub-segment, which is part of the platform segment, is anticipated to grab the highest share of 70.7% in the satellite propulsion system market by the end of 2035. The sub-segment’s upliftment is primarily attributed to its importance for extending, maneuvering, and maintaining the life of satellites, along with ensuring essential functions, such as orbit insertion, attitude control, and station-keeping. According to official statistics published by the Space Foundation Organization in January 2025, there has been an increase in orbital launches by 16%, as well as spacecraft mass to orbit by 40%. This resulted in 259 satellite launches as of 2024, which occurred on an average of 1 in every 34 hours, 5 hours more than in 2023. This particular launch pace further grew in 2025, with launch operators ensuring site improvements, frequent launches, and first flights of 24 launch vehicles, thus making it suitable for boosting the sub-segment growth.

Satellite Mass Segment Analysis

During the forecast period, the large satellites (>1,000 kg) segment, part of the satellite mass, is projected to garner the second-highest share in the satellite propulsion system market. The segment’s growth is significantly driven by its critical role in defense, telecommunications, navigation, and scientific exploration. These particular satellites, typically deployed in Geostationary Earth Orbit (GEO) and Medium Earth Orbit (MEO), are preferred for missions requiring high-power payloads, robust radiation-hardened electronics, and operational lifespans extending beyond 15 years. The segment's growth is further propelled by escalating defense investments in space-based C4ISR capabilities to modernize strategic space assets, much of which is allocated to large, resilient satellites.

Propulsion Type Segment Analysis

The electric propulsion segment in the satellite propulsion system market is expected to hold the third-highest share by the end of the stipulated timeline. The segment’s development is highly propelled by its implementation in modernized marine and aerospace applications, and provides less fuel utilization in comparison to chemical systems. As per a data report published by the EPO Organization in May 2024, space propulsion systems have observed a robust surge in patent activity over the past 20 years, and significantly averaging out at 9% every year. Besides, there has been a remarkable increase in the number of satellites, deliberately rising from an average of 300 per year to more than 2,800 as of 2023, thereby enhancing the demand for electric propulsion globally.

Our in-depth analysis of the satellite propulsion system market includes the following segments:

|

Segment |

Subsegments |

|

|

|

Satellite Mass |

|

|

Propulsion Type |

|

|

End user |

|

|

Orbit Type |

|

|

Component |

|

|

Technology |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Satellite Propulsion System Market - Regional Analysis

North America Market Insights

North America in the satellite propulsion system market is anticipated to garner the largest share of 38.3% by the end of 2035. The market’s upliftment in the region is primarily attributed to an increase in the levels of defense and government expenditure, the rapid proliferation of commercial low-earth orbit (LEO) constellations, as well as a tactical pivot towards efficient and advanced propulsion technologies. According to official statistics published by the Aerospace America Organization in January 2026, in terms of high-powered systems, NASA’s very own Jet Propulsion Laboratory has been evaluating a LaB6 hollow cathode at 250A to effectively benchmark models for 200-kW-class Hall thrusters. This particular evaluation surpassed 2,500 hours of operation, owing to the completion of the 4,000-hour test duration, thereby making it suitable for bolstering the market in the overall region.

The satellite propulsion system market in the U.S. is growing significantly, owing to an escalation in defense spending, a thriving commercial space industry, sustained government support for cutting-edge technological development, increased priority on the warfighting domain, and urgency for resilient satellite networks. Based on government estimates published by the GSA Government in September 2022, the country comprises nearly 5,500 active satellites in orbit, and it is further estimated to launch an additional 58,000 satellites by the end of 2030. Besides, this projected increase in satellite launches has ensured an increase in orbital debris, emissions into the upper atmosphere, and disruption of astronomy. Therefore, to combat these, the country’s government has developed suitable policies, which are creating an optimistic outlook for the market’s growth.

The presence of governmental funding programs, increasing participation in international space collaborations, the emergence of a specialized industrial base, which is focused on next-generation space technologies, and the sustained commitment to space research and development through the Space Technology Development Program (STDP) are certain factors to uplift the satellite propulsion system market in Canada. As per an article published by the Agence Spatiale Canadienne in November 2025, non-profit organizations and businesses are readily associated with the domestic space economy, with 64% of large-scale organizations generating the highest revenues, and 39% of small and medium-sized enterprises (SMEs) are deliberately capturing a suitable portion of the export industry. Additionally, research centers and universities also support a substantial workforce of nearly 2,800 employees, thus enhancing the satellite propulsion system market growth.

Europe Market Insights

Europe in the satellite propulsion system market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by generous government investments, a strong aerospace industrial base, an increase in commercial satellite activities, and the shift toward green and electric propulsion technologies supported by strict sustainability initiatives and regulations. Based on government estimates published by the UK Government in 2025, the country has 17% of the worldwide industry for aerospace, and significantly provides more than 100,000 direct employment opportunities. In addition, the industry in the country generated USD 32.5 billion of the domestic revenue, of which 75% is readily exported. Therefore, with all these expansions, there is a huge growth opportunity for the market in the region.

The satellite propulsion system market in France is gaining increased traction, owing to its unparalleled concentration of space industry infrastructure, government commitment, technological leadership, generous funding opportunities, the development of aerospace vehicles, and the incorporation of chemical propulsion systems. As stated in a data report published by the Aerospace Security Organization in March 2024, the Centre National D’Etudes Spatiales (CNES) ensures a huge contribution to the French space industry, with the largest budget of a civil space agency, amounting to USD 2.5 billion. Besides, the North Atlantic Treaty Organization (NATO) has significantly pledged USD 1.1 billion, with its spread expected to reach by the end of 2034 for developing suitable satellite communication services in the country, thus bolstering the market expansion.

The combination of tactical government investments, the development of a small-scale satellite industry, the emergence of advanced propulsion startups, substantial funding directed towards propulsion technology creation, and increased focus on innovative materials for aerospace applications are responsible for fueling the satellite propulsion system market in Italy. As stated in an article published by the IAI in January 2023, the country utilized an opportunity provided by the Europe Recovery Fund for allocating generous resources for space activities for over USD 2.3 billion by the end of 2026. Therefore, with such fund allocation, the country remains effectively engaged in such a fast-pacing technological industry, wherein informed and rapid decision-making is essential, thus positively impacting the market development.

APAC Market Insights

The Asia Pacific in the satellite propulsion system market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by generous governmental investments in national space programs across South Korea, Japan, India, and China, as well as the rapid proliferation of commercial satellite constellations and indigenous launch vehicle development, expansion in defense space budgets, and the growing emphasis on self-reliance in propulsion technologies. According to official statistics published by the International Institute for Strategic Studies in February 2026, the defense spending in the region has increased, with the combined total reaching USD 573 billion. Additionally, in 2025, the region witnessed an uplift of 5.7%, which is slightly more than the 2024’s YoY increase of 5.5%. Moreover, the Military Balance has estimated to constitute a baseline defense budget of USD 251.3 billion, thus bolstering the market exposure.

The satellite propulsion system market in China is gaining increased exposure, owing to the most ambitious satellite deployment schedule, vertically integrated industrial capabilities, unparalleled governmental investment, and the development of sophisticated hydrogen-oxygen cryogenic and semi-cryogenic upper stage engines for heavy-lifting missions. As stated in an article published by the State Council Information Office in May 2025, the overall output valuation of the country’s satellite navigation and position service sector reached USD 79.9 billion as of 2024, denoting an increase by 7.3% YoY. Besides, there has been an increase in the number of satellite navigation patent applications by 129,000, and an estimated 288 million mobile phones are gradually equipping the BeiDou Navigation Satellite System (BDS), thereby making it suitable for skyrocketing the satellite propulsion system market growth.

The aspects of strong technology development programs by the Indian Space Research Organization (ISRO), the increased emergence of private space startups under space sector policies, and an increase in funding for innovative materials and green propellant development are certain trends that are boosting the satellite propulsion system market in India. Based on government estimates published by the ISRO in May 2025, there have been 261 launch attempts, of which 254 launches have been successful, leading to an additional 2,578 operational satellites. Besides, a total of 2,963 objects have been placed in orbit, which is fewer than 3,135 objects from 212 launches as of 2023. Furthermore, the fragmentation incidents originating from debris accounted for 702 in 2024, in comparison to 69 as of 2023. In addition, the collision avoidance maneuvers (CAMs) performance on earth-orbiting satellites is also positively impacting the market expansion in the country.

Cumulative Number of CAMs Performance for Earth-Orbiting Satellites in India (2010-2024)

|

Year |

Cumulative Number of CAM |

|

2010 |

1 |

|

2011 |

3 |

|

2012 |

4 |

|

2013 |

8 |

|

2014 |

8 |

|

2015 |

11 |

|

2016 |

16 |

|

2017 |

21 |

|

2018 |

29 |

|

2019 |

37 |

|

2020 |

49 |

|

2021 |

68 |

|

2022 |

89 |

|

2023 |

112 |

|

2024 |

122 |

Source: ISRO

Key Satellite Propulsion System Market Players:

- Northrop Grumman Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- The Boeing Company (U.S.)

- L3Harris Technologies Inc. / Aerojet Rocketdyne Holdings Inc. (U.S.)

- Space Exploration Technologies Corp. (SpaceX) (U.S.)

- Blue Origin LLC (U.S.)

- Safran S.A. (France)

- Airbus Defence and Space (France)

- Thales Alenia Space (France)

- ArianeGroup GmbH (France/Germany)

- OHB SE (Germany)

- Mitsubishi Electric Corporation (Japan)

- IHI Corporation (Japan)

- Ball Corporation (U.S.)

- Moog Inc. (U.S.)

- Rocket Lab USA Inc. (U.S.)

- Bellatrix Aerospace Private Limited (India)

- Indian Space Research Organization (ISRO) (India)

- Rafael Advanced Defense Systems Ltd. (Israel)

- MDA Ltd. (Canada)

- Daher (France)

- Enpulsion (Austria)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Northrop Grumman Corporation is a dominant force in the satellite propulsion system market, leveraging its extensive heritage in solid, liquid, and electric propulsion systems across both national security and civil space applications. The company integrates propulsion capabilities into its end-to-end spacecraft platforms, positioning itself as a vertically integrated supplier for critical defense and exploration missions.

- Lockheed Martin Corporation serves as a prime integrator of advanced propulsion systems across its extensive portfolio of military, civil, and commercial satellites, emphasizing reliability and mission assurance. The company invests heavily in next-generation electric and hybrid propulsion technologies to meet the evolving demands of proliferated LEO constellations and deep-space exploration.

- The Boeing Company maintains a longstanding presence in the satellite propulsion sector through its heritage in large GEO communications satellites and advanced space systems requiring robust chemical and electric propulsion. The company continues to develop innovative in-space propulsion solutions, including electric propulsion systems for its satellite platform, to support both commercial and government customers.

- L3Harris Technologies Inc. has solidified its position as a premier pure-play propulsion supplier, delivering a comprehensive portfolio of liquid, solid, and electric rocket engines for satellites, launch vehicles, and missile defense systems. This vertical integration strategy enables the company to offer mission-critical propulsion components across the full spectrum of space and defense applications.

- Space Exploration Technologies Corp. (SpaceX) has redefined the satellite propulsion landscape through its vertically integrated approach, manufacturing its own Hall-effect thrusters and propulsion systems for the Starlink mega-constellation and other spacecraft platforms. The company's focus on high-volume, cost-efficient production has set new benchmarks for scalability and rapid deployment in the commercial satellite propulsion sector.

Here is a list of key players operating in the global satellite propulsion system market:

The satellite propulsion system market is characterized by a consolidated competitive landscape, with the top five players collectively holding the majority of the global market share. The industry is dominated by large, vertically integrated U.S. defense primes and Europe-based aerospace conglomerates that leverage extensive government contracts and deep technological heritage. Besides, notable strategic initiatives include vertical integration through acquisitions, such as L3Harris's acquisition of Aerojet Rocketdyne, to consolidate propulsion supply chains. Moreover, in August 2024, Safran Electronics & Defense developed its U.S.-based manufacturing capabilities for small-scale satellite propulsion systems to cater to the increasing demand in both the defense and commercial industries. This strategic initiative supported the expected growth of the small satellite industry in North America, which is predicted to reach over USD 5 billion by the end of 2030, thus driving the satellite propulsion system industry globally.

Corporate Landscape of the Satellite Propulsion System Market:

Recent Developments

- In June 2025, Daher, along with Safran and Collins Aerospace and Ascendance, completely supports international and national roadmaps for decarbonizing the aviation industry by targeting 6-10-seat aircraft, accounting for 25,000 in operation globally.

- In May 2025, Enpulsion launched Nexus, which is the most advanced propulsion system, deliberately designed for spacecraft of 500 kilograms. This is suitable for significantly delivering increased thrust and enhanced orbit-raising capabilities for catering to the growing need for high-performance and responsive electric propulsion in small missions.

- In February 2023, Thales Alenia Space, formed by the joint venture between 67% of Thales and 33% of Leonardo, has successfully signed a contract with the Korea Aerospace Research Institute (KARI) to offer electric propulsion for incorporating on their very own GEO-KOMPSAT-3 (GK3) satellite.

- Report ID: 8476

- Published Date: Mar 27, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Satellite Propulsion System Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.