Retail Core Banking Systems Market Outlook:

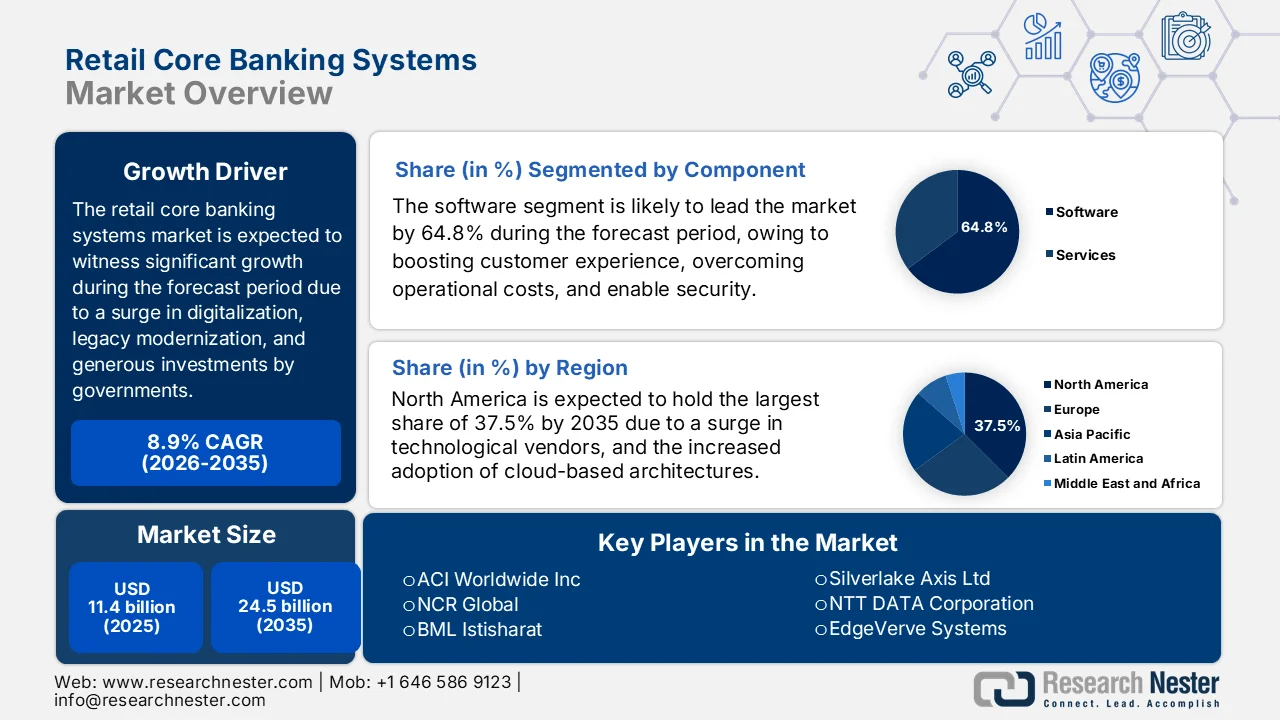

Retail Core Banking Systems Market size was valued at over USD 11.4 billion in 2025 and is expected to reach USD 24.5 billion by the end of 2035, growing at a CAGR of 8.9% over 2026-2035. In 2026, the industry size of retail core banking systems is assessed at USD 12.4 billion.

The worldwide retail core banking systems market is being gradually reshaped by a confluence of factors, including digital adoption, legacy modernization, increased rate fluctuations, operational efficiencies, technological partnerships, and cross-border data flows. According to official statistics published by the World Bank Organization in July 2025, mobile phone technology readily plays a key role in digital banking, with 10% of the adult population across developing economies utilizing a mobile-money account for saving, which denotes a 5%-point increase. Besides, as of 2024, 40% of adults in developing countries successfully saved a financial account, demonstrating a 16%-point increase. For instance, in Sub-Sahara Africa, there has been an increase in financial accounts by 12 percentage points for 35% of adults, thereby denoting an optimistic outlook for the market growth globally.

Furthermore, the increased focus on AI-based hyper-personalization and automation, along with API-specific and composable architectures for ecosystem banking and the adoption of SaaS and cloud-native for agility, are certain trends that are responsible for bolstering the retail core banking systems market globally. As per a data report published by the World Economic Forum in 2025, financial services organizations significantly spent USD 35 billion on AI as of 2023. Based on this, the projected investment across insurance, capital markets, payments, and banking is poised to reach USD 97 billion by the end of 2027. Besides, 70% of financial service operators believe that AI can directly support revenue growth in upcoming years by boosting consumer experiences, enabling innovative offerings, optimizing security against potential threats, making services and products relevant and personalized, and empowering cross- and up-selling.

Key Retail Core Banking Systems Market Insights Summary:

Regional Highlights:

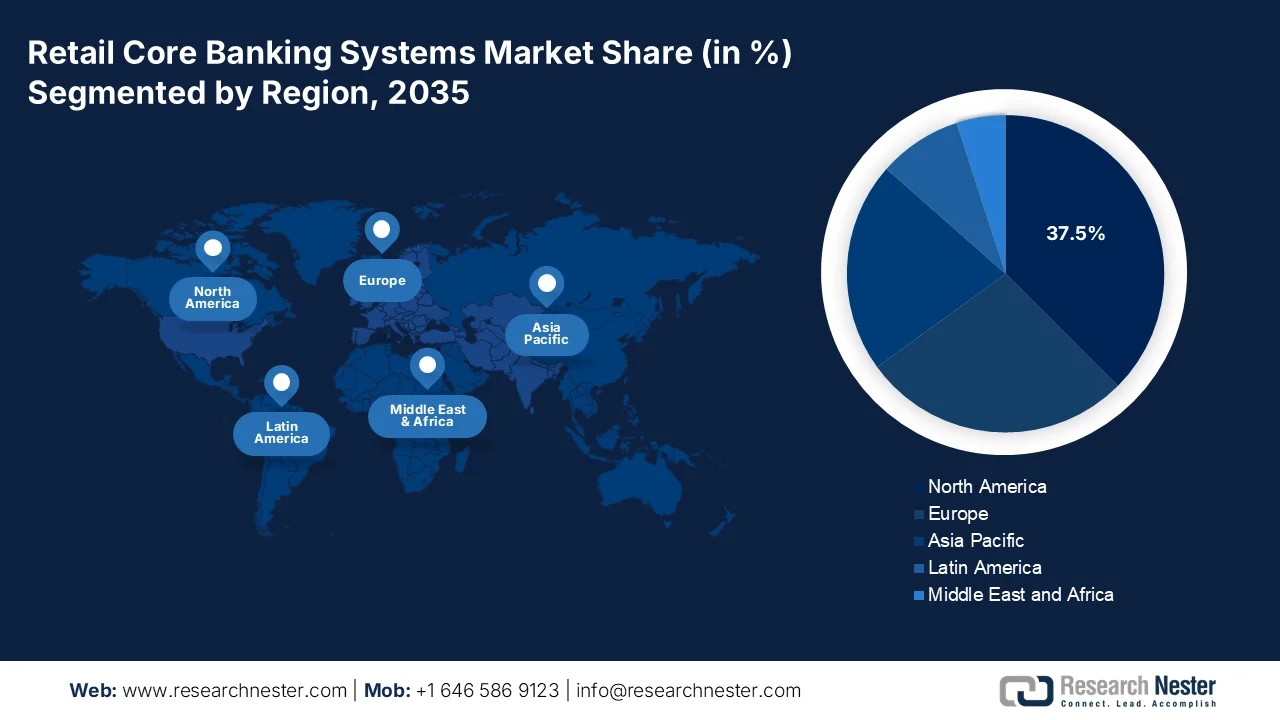

- North America is projected to hold a 37.5% share in the retail core banking systems market, owing to the rising demand for legacy system modernization and increasing adoption of cloud-based and API-driven architectures

- Asia Pacific is anticipated to register the fastest growth during 2026–2035, fueled by expanding urbanization, rising smartphone penetration, and increasing demand for digital banking services

Segment Insights:

- By 2035, the software sub-segment in the retail core banking systems market is expected to capture a 64.8% share, driven by increasing adoption of AI-powered solutions to enhance customer experience and operational efficiency

- During the forecast period 2026–2035, the cloud-based sub-segment is likely to hold the second-largest share, propelled by growing need for cost efficiency, scalability, and enhanced security in financial institutions

Key Growth Trends:

- Escalating demand for digital-first banking

- Increase of risk management through automated regulatory

Major Challenges:

- Regulatory compliance and data sovereignty pressures

- High implementation expenditure and uncertain return on investment

Key Players: Fiserv, Inc., Fidelity National Information Services Inc. (FIS), Jack Henry & Associates, Inc., Oracle Corporation, Temenos AG, SAP SE, Finastra, Tata Consultancy Services (TCS), Infosys Limited, Avaloq Group AG, Sopra Steria Group, Intellect Design Arena Limited, Silverlake Axis Ltd, NTT DATA Corporation, EdgeVerve Systems, Q2 Holdings, Inc., ACI Worldwide Inc, NCR Global, BML Istisharat, InfrasoftTech Limited

Global Retail Core Banking Systems Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 11.4 billion

- 2026 Market Size: USD 12.4 billion

- Projected Market Size: USD 24.5 billion by 2035

- Growth Forecasts: 8.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (37.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, United Kingdom, Germany, Japan

- Emerging Countries: India, Brazil, Indonesia, Vietnam, Mexico

Last updated on : 20 March, 2026

Retail Core Banking Systems Market - Growth Drivers and Challenges

Growth Drivers

- Escalating demand for digital-first banking: This is the primary driver for the retail core banking systems market, which has relentlessly created a surge in the customer adoption of internet and mobile banking. As stated in an article published by the World Bank Group in June 2022, 76% of adults globally have a bank account, thus denoting an increase from 68% and 51% in previous years. This particular growth has been highly concentrated in both China and India, with account ownership increasing by double digits across 34 nations. Moreover, the pandemic also paved the way for the increased utilization of digital payments, with 40% of adults in low and middle-income countries initiating merchant online or in-store payments by utilizing a phone, the internet, or a card, thereby fueling the market expansion.

- Increase of risk management through automated regulatory: The increased complexity and expense of regulatory compliance is one of the powerful drivers for the retail core banking systems market. In this regard, modern core systems that cater to built-in compliance modules, strong data management capabilities, and real-time monitoring are becoming crucial across overall banking institutions globally. These tend to reduce the risk of penalties, automate reporting, shift compliance from an expensive burden to an integrated function, and enhance security. Besides, stringent government regulations for financial transactions and data protection are pressuring banks to implement suitable solutions for safeguarding consumer information and ensuring compliance.

- Competitive necessity to modernize legacy infrastructure: The inflexibility and unsustainable expense of maintaining historic legacy systems significantly hinder a bank’s capability to integrate and innovate with fintechs and ensure upscaling efficiently, which is positively driving the retail core banking systems market worldwide. According to official statistics published by the World Bank Group in May 2025, there has been an acceleration in energy and equitable transition by committing more than USD 13 billion to ensure renewable energy generation. Additionally, nearly 2/3rd of this particular support is for distribution and transmission infrastructure to readily facilitate the implementation of renewable energy and upstream support for enabling institutions, regulations, and policies to up-scale private investments for renewable energy, thus fueling the market growth.

Challenges

- Regulatory compliance and data sovereignty pressures: Stringent and evolving regulatory requirements across jurisdictions create significant friction for the retail core banking systems market deployments and upgradations. Financial institutions must ensure that their core platforms comply with a complex patchwork of regulations governing data privacy, security, anti-money laundering, open banking, and operational resilience. In Europe, the Revised Payment Services Directive mandates stringent API standards and customer authentication protocols, while in the U.S., regulations vary at both the federal and state levels. Besides, cross-border institutions face the additional challenge of reconciling conflicting requirements, such as data localization laws in countries, such as India and Russia, that mandate customer data remain within national borders.

- High implementation expenditure and uncertain return on investment: The substantial financial investment required for the retail core banking systems market replacement presents a daunting barrier, particularly for mid-sized and smaller financial institutions. Implementation costs encompass not only software licensing fees but also significant expenditures for systems integration, data migration, business process reengineering, and staff training. These projects typically require multi-year commitments with costs escalating well beyond initial estimates, while the anticipated benefits in terms of operational efficiency, revenue growth, and customer acquisition often take years to materialize, thus causing a hindrance in the market expansion.

Retail Core Banking Systems Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.9% |

|

Base Year Market Size (2025) |

USD 11.4 billion |

|

Forecast Year Market Size (2035) |

USD 24.5 billion |

|

Regional Scope |

|

Retail Core Banking Systems Market Segmentation:

Component Segment Analysis

The software sub-segment, part of the component segment, is anticipated to garner the largest share of 64.8% in the retail core banking systems market by the end of 2035. The sub-segment’s upliftment is highly fueled by its importance for enhancing consumer experience, combating operational expenses, ensuring suitable security, and enabling 24/7 digitalized accessibility. According to official statistics published by the World Economic Forum in January 2025, with suitable developments in generative AI, it has been demonstrated that 32% to 39% of operations performed across capital economies, along with banking and insurance businesses constituting a high potential to be automated, and 34% to 37% accounting increased augmentation. Besides, financial services organizations spent USD 35 billion on AI in 2023, with expected investments across payment businesses, capital markets, and banking to reach USD 97 billion by the end of 2027, thus boosting the sub-segment’s exposure in the overall market.

Deployment Segment Analysis

During the forecast period, the cloud-based sub-segment, which is part of the deployment segment, is projected to hold the second-largest share in the retail core banking systems market. The sub-segment’s growth is highly driven by its importance for modernized financial institutions to gain cost-effectiveness, rapid scalability, and enhanced safety. As per an article published by the Journal of Financial Stability in December 2022, an estimated 14% of commercial retail banking revenues are effectively attributed to agile and cloud technology-specific new entrants. Besides, based on a survey analysis conducted on 391 financial institutions, 41% have significantly applied cloud computing, and 47% are in progress to adopt. Therefore, with an increase in cloud adoption by financial organizations, there is a huge growth opportunity for the sub-segment across different regions.

End user Segment Analysis

The commercial banks segment in the retail core banking systems market is expected to account for the third-largest share by the end of the stipulated timeline. The segment’s development is highly propelled by its operation with immense scale and complexity that demand robust, feature-rich core platforms capable of processing millions of daily transactions across diverse product lines, including deposits, loans, mortgages, and wealth management services. The modernization imperative for commercial banks stems from the crushing burden of legacy infrastructure, with many operating mainframe-based cores that hinder agility, inflate maintenance costs, and impede integration with modern digital channels and fintech partners. Unlike small-scale institutions that can adopt lightweight, standardized solutions, commercial banks require highly configurable platforms that accommodate complex product structures, multi-entity hierarchies, and sophisticated risk management frameworks.

Our in-depth analysis of the retail core banking systems market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Deployment |

|

|

End user |

|

|

Solution Type |

|

|

Application |

|

|

Functionality |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Retail Core Banking Systems Market - Regional Analysis

North America Market Insights

North America in the retail core banking systems market is anticipated to garner the highest share of 37.5% by the end of 2035. The market’s upliftment in the region is highly attributed to the urgent demand for modernizing decades-old legacy facilities, the increased concentration of notable technology vendors, and a shift from on-premise monolithic systems to cloud-based and API-specific architectures. According to official statistics published by the Census Government in September 2025, in terms of technology, almost 78% of organizations in the region reported utilizing AI as of 2024, denoting an increase from 55% in 2023. Besides, 3.9% of businesses utilized robots, and 3.3% utilized AI. Meanwhile, AI accounted for 40.7%, which is followed by 50.2% for specialized equipment, and 56.6% for robotics, thereby positively impacting the retail core banking systems market growth in the overall region.

Increased Skill Analysis Uplifting Banking Systems in North America (2025)

|

Technology Type |

Skills Growth |

|

AI |

29.8% |

|

Specialized Software |

20.2% |

|

Robotics |

23.4% |

|

Cloud-Based |

21.7% |

|

Specialized Equipment |

22.7% |

Source: Census Government

The retail core banking systems market in the U.S. is growing significantly, owing to a rise in consumer expectations for seamless digital experiences, modernization strategies, focus on API-based solutions for integrating with current systems to deliver targeted advancements in customer engagement, fraud detection, and payment innovations. As per a data report published by the U.S. Department of the Treasury in September 2022, banks and other institutions in the country tend to access central bank reserve balances, with Federal Reserve notes accounting for USD 2.2 trillion, USD 3.3 trillion in reserve balances, and USD 50 billion in coin outstanding. In addition, the country significantly comprises almost USD 19.4 trillion in private money, which is positively fueling financial institutions. Therefore, with the availability of both private and public money, there is a huge scope for payment advancements in the country, which positively impacts the market expansion.

The strong push towards open banking architectures, cloud-native services, and tactical partnerships to foster advancements, along with drive product innovation, and regulatory support, and an increase in the AI incorporation, are certain factors that are bolstering the retail core banking systems market in Canada. As per an article published by the Bank of Canada in September 2024, AI has the capability to automate 25% of overall tasks and bolster the total factor productivity (TFP) by 9% in the upcoming decade. Similarly, a sustained improvement in TFP in the country is expected to increase the average income per-person by approximately USD 4,000 every year. This particular productivity boost not only originates from automating banking operations, but also from productive employment opportunities in the economy. Based on this, there is the development of the latest services and products, which is suitable for driving the market demand in the country.

APAC Market Insights

The Asia Pacific in the retail core banking systems market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by an increase in urbanization, an upsurge in smartphone penetration, the presence of a burgeoning middle class seeking digitalized banking services, and generous investments by the government. According to official statistics published by the UN-HABITAT Organization in 2026, more than 1 million homes have been developed, and over 3 million people offer basic services based on the People’s Process strategy for community-based settlements upgradation. The overall region is supported by 18 countries for developing urban-specific policies and over 100 cities in incorporating sustainable urbanization over the past 5 years, thus fueling the market demand in the overall region.

The retail core banking systems market in China is gaining traction, owing to the presence of massive state-owned commercial banks, rapid digital transformation, comprehensive adoption of digital banking and mobile payments, prioritizing financial technology, and a strong push for cloud computing and AI implementation in financial services. As stated in an article published by the State Council Information Office in May 2025, the digital industry in the country has generated a revenue of almost USD 1.1 trillion in the first quarter of 2025, demonstrating an increase by 9.4%. Besides, the country has unveiled an action plan for building a Digital China by outlining notable initiatives, including AI Plus for infrastructure upgradation, along with digital talent and data industry development, thus creating an optimistic outlook for the retail core banking systems market development.

The aspects of technological adoption across different sectors, an increase in mobile banking customers, the introduction of banking services and products, the government’s commitment towards digital financial institutions, rapid expansion in the fintech ecosystem, and an increase in the demand for sustainability-based financing services are boosting the retail core banking systems market in India. Based on government estimates published by the Invest UP in October 2024, the fintech industry in the country is regarded as one of the fastest-growing sectors globally, with a market size amounting to USD 111.1 billion as of 2024, and is further predicted to reach USD 421.4 billion by the end of 2029. Based on this growth, Uttar Pradesh, especially Noida, is emerging as the most significant facility for fintech startups, with more than 239 companies operating in the overall country, thus making it suitable to drive the market development.

Europe Market Insights

Europe in the retail core banking systems market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by the presence of suitable banking solutions, strong financial institutions, technological advancements, as well as a surge in superior banking solutions and fintech partnerships. For instance, in July 2023, Visa made a suitable expansion in its Fintech Fast Track in the overall region for escalating advanced approaches to initiate payment. This particular service has been designed to ensure the next generation of fintech to join the company’s network and develop outstanding digitalized commerce experiences for merchants and consumers. As a result, there has been an increase in fintech services by 360% year-over-year (YoY), which denotes an optimistic outlook for the retail core banking systems market in the overall region.

The retail core banking systems market in Germany is gaining increased exposure, owing to the strong financial services industry, international banking software providers, commitment towards industrial transformation through substantial government investment for bank modernization, and the existence of research leadership that supports innovation. As stated in an article published by the German Trade and Invest in 2026, there exist 1,400 credit institutions in the country, followed by more than 500 insurance organizations that are effectively active in the domestic insurance sector. In addition, the gross value added of the banking sector amounts to USD 86.5 billion, while the premium income in the sector amounts to USD 260.6 billion. Besides, by the end of 2023, financial assets of private households in the nation amounted to nearly USD 8.8 trillion, demonstrating an increase of about 6.6% in comparison to 2022, which is positively impacting the market growth.

The acceleration in fintech upliftment, open banking integration, an increase in collaborations, modernization of traditional banking institutions, ensuring sustainable manufacturing strategies, banking partnerships to support green finance products, and generous investments in banking technology are proliferating the retail core banking systems market in the UK. Based on government estimates published by the ITA in January 2023, the fintech sector comprises more than 1,600 firms, which is further projected to double by the end of 2030. Besides, London is considered one of the biggest fintech centers globally, with USD 3.6 trillion of regular foreign exchange transactions. Moreover, increased levels of investment is a driving force behind the industrial upliftment, with domestic investment reaching USD 11.6 billion, thereby making it suitable for the market upliftment.

Key Retail Core Banking Systems Market Players:

- Fiserv, Inc. (U.S.)

- Fidelity National Information Services Inc. (FIS) (U.S.)

- Jack Henry & Associates, Inc. (U.S.)

- Oracle Corporation (U.S.)

- Temenos AG (Switzerland)

- SAP SE (Germany)

- Finastra (UK)

- Tata Consultancy Services (TCS) (India)

- Infosys Limited (India)

- Avaloq Group AG (Switzerland)

- Sopra Steria Group (France)

- Intellect Design Arena Limited (India)

- Silverlake Axis Ltd (Malaysia)

- NTT DATA Corporation (Japan)

- EdgeVerve Systems (India)

- Q2 Holdings, Inc. (U.S.)

- ACI Worldwide Inc (U.S.)

- NCR Global (U.S.)

- BML Istisharat (Jordan)

- InfrasoftTech Limited (India/UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Fiserv is a leading provider of core processing solutions for financial institutions, offering its flagship DNA platform to enable account processing, lending, and digital banking capabilities. The company focuses on delivering open, API-first architectures that help banks and credit unions modernize their core systems and create seamless omnichannel customer experiences.

- Fidelity National Information Services Inc. (FIS) provides comprehensive core banking platforms, including its Modern Banking Platform, which supports real-time processing, deposit management, and lending operations for financial institutions globally. The company is actively transitioning clients to cloud-native, SaaS-based delivery models to enhance scalability and accelerate innovation in digital banking.

- Jack Henry & Associates, Inc. specializes in core processing solutions designed specifically for community banks and credit unions, offering platforms such as Symitar and SilverLake Systems. The company emphasizes its collaborative approach, providing integrated, open-architecture cores that enable institutions to easily connect with fintech partners and deliver personalized digital experiences.

- Oracle Corporation offers its Oracle Banking Core Platform, a cloud-native, microservices-based solution that supports retail banking operations, including deposits, loans, and customer account management. The platform leverages the company’s robust technology infrastructure to provide financial institutions with scalability, real-time data processing, and embedded AI capabilities for enhanced decision-making.

- Temenos AG provides its flagship Temenos Transact core banking solution, a cloud-native, API-first platform designed to power retail, corporate, and wealth management operations for banks worldwide. The company focuses on continuous innovation through its extensive partner ecosystem and commitment to open banking standards, enabling financial institutions to rapidly deploy new products and services.

Here is a list of key players operating in the global retail core banking systems market:

The competitive landscape of the retail core banking systems market is characterized by a mix of established U.S.-based giants and innovative players from Europe and the Asia Pacific, creating a dynamic and fiercely contested environment. Key strategic initiatives are sharply focused on cloud-native, API-based architectures to enable open banking and real-time processing. Major players are aggressively pivoting to SaaS models, with many forming ecosystem partnerships with fintechs to accelerate innovation and bridge execution gaps. For instance, in March 2023, Bank ABC signed an agreement with Temenos and NdcTech for replacing its core banking systems for its wholesale, corporate, and retail businesses. Additionally, the agreement’s purpose is also to effectively power its subsidiary, ila Bank, with Temenos’ core banking platform on the cloud, thus proliferating the retail core banking systems market globally.

Corporate Landscape of the Retail Core Banking Systems Market:

Recent Developments

- In February 2025, Tencent Cloud significantly provided its support to assist Fusion Bank in successfully completing its migration to the latest core banking system within 10 months and effectively setting a modernized industrial benchmark for core banking upgradation, particularly in Hong Kong.

- In January 2025, WeBank Technology Services demonstrated its global expansion in Hong Kong by underscoring its technological prowess and extending its presence across different regions by signing deals with Hong Leong Bank, Mega Corp, and Fusion Bank.

- In May 2023, North East Small Finance Bank effectively migrated its core banking system to M2P’s Turing CBS to ensure a digital accelerator platform that comprises integrated payment options and back-office platforms to track compliance.

- Report ID: 8454

- Published Date: Mar 20, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.