Preclinical CRO Market Outlook:

Preclinical CRO Market size was valued at USD 7.2 billion in 2025 and is expected to grow significantly to USD 14.5 billion by 2035, expanding at a CAGR of 8.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of preclinical CRO is estimated at USD 7.7 billion.

The preclinical CRO market is poised for immense growth owing to the escalating complexity of drug discovery, especially in terms of biopharmaceuticals, cell and gene therapies, and oncology. Biopharma companies across the globe are outsourcing early-stage research, including GLP-compliant toxicology, ADME, PK, and bioanalytical studies, to specialized providers to accelerate timelines and reduce fixed in-house costs. In this context, the article published by CCRPS Organization stated that the 2025 global CRO landscape was effectively driven by rising demand for outsourced clinical trials, with a market value of USD 90 billion, and steady outsourcing from pharmaceutical, biotech, and medical device sponsors. Growth is also supported by increased trial complexity, including decentralized and digitally enabled studies, as well as expanding activity in emerging regions such as the Asia Pacific and Latin America, which offer broader patient access and cost advantages, thus positively impacting preclinical CRO market growth.

Top 10 Global Clinical Research Organizations (CROs) in 2025 by Revenue, Headquarters, and Key Pharma Partnerships

|

CRO Name |

Headquarters |

Specialization |

Revenue / Size |

Notable Clients or Partnerships |

|

ICON plc |

Dublin, Ireland |

Full-service |

USD 6.5 Billion |

Pfizer, Bristol Myers Squibb |

|

IQVIA |

Durham, North Carolina, U.S. |

Full-service |

USD 15 Billion |

Novartis, Merck |

|

Parexel |

Newton, Massachusetts, U.S. |

Late-phase, full-service |

USD 2.5 Billion (est.) |

GlaxoSmithKline, AstraZeneca |

|

Syneos Health |

Morrisville, North Carolina, U.S. |

Full-service |

USD 5 Billion |

Eli Lilly, Johnson & Johnson |

|

Medpace |

Cincinnati, Ohio, U.S. |

Niche (oncology, rare disease) |

USD 1.5 Billion |

Roche, Gilead |

|

PPD (Thermo Fisher Scientific) |

Wilmington, North Carolina, U.S. |

Full-service |

USD 4.7 Billion |

Sanofi, Pfizer |

|

WuXi AppTec |

Shanghai, China |

Full-service, lab services |

USD 6 Billion |

Bayer, Bristol Myers Squibb |

|

Charles River Laboratories |

Wilmington, Massachusetts, U.S. |

Preclinical, early-phase |

USD 4 Billion |

Biogen, Regeneron |

|

Labcorp Drug Development |

Burlington, North Carolina, U.S. |

Full-service |

USD 4.6 Billion |

Pfizer, GSK |

Source: CCRPS

Key trends reshaping the preclinical CRO market are the inclusion of AI in drug design, the rising adoption of advanced in vitro models such as organ-on-chip, and a strategic shift towards end-to-end service partnerships. As per an article published by the National Institute of Health (NIH) in May 2022 under the Blueprint MedTech initiative, it was looking for a qualified CRO to provide end-to-end regulatory affairs and compliance support for medical device development from preclinical stages through first-in-human clinical studies. The scope includes preparation of FDA submissions (IDE, 510(k), De Novo, PMA, HDE), regulatory strategy development, quality system establishment, compliance program creation, and support for clinical study oversight under GCP standards. The selected CRO will be assisting with market research, commercialization planning, and reimbursement strategy development. This particular contract is structured as a 5-year IDIQ award with task orders issued based on NIH program needs, reflecting a flexible federal outsourcing model for complex neurotechnology and medical device translation.

Key Preclinical CRO Market Insights Summary:

Regional Highlights:

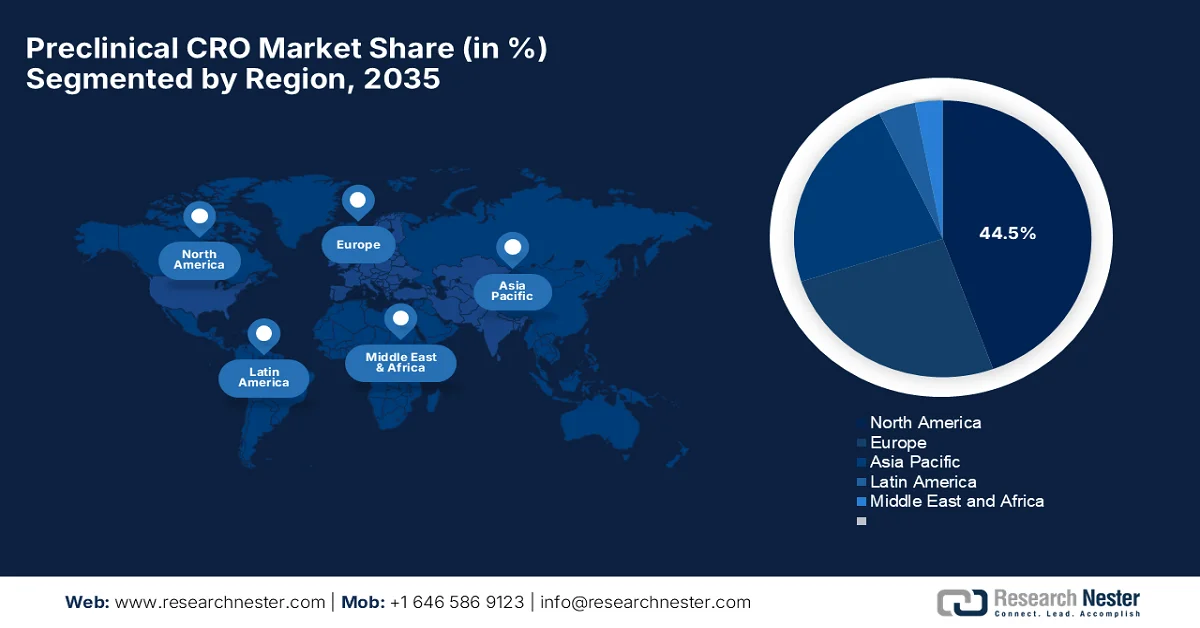

- North America preclinical CRO market is projected to hold a dominant 44.5% share by 2035, reinforced by a well-established pharmaceutical ecosystem and advanced research infrastructure

- Asia Pacific is anticipated to register the fastest growth during 2026–2035, fueled by increasing chronic disease prevalence and rising outsourcing of preclinical services to regional providers

Segment Insights:

- In the preclinical CRO market, the Biopharmaceuticals segment is expected to account for a leading 62.6% share by 2035, propelled by increasing R&D complexity and cost pressures

- The toxicology segment is set to secure a considerable revenue share by 2035, impelled by stringent regulatory requirements prior to human trials

Key Growth Trends:

- Rising R&D expenditure in pharma & biotech

- Increasing drug development complexity

Major Challenges:

- Regulatory complexity and compliance burden

- High operational costs and pricing pressure

Key Players: Charles River Laboratories International, Inc. (U.S.), Labcorp Drug Development (U.S.), WuXi AppTec Co., Ltd. (China), Eurofins Scientific SE (Luxembourg), ICON plc (Ireland), Evotec SE (Germany), Medpace Holdings, Inc. (U.S.), Thermo Fisher Scientific (PPD) (U.S.), Parexel International Corporation (U.S.), SGS SA (Switzerland), RSSL (UK), ERBC (Italy), Crown Bioscience (United States), Turbine (Netherlands), Menarini Biotech (Italy), X-Chem (U.S.), QPS (U.S.), Ryght AI (U.S.), Intertek Group plc (UK), Pharmaron Beijing Co., Ltd. (China), JOINN Laboratories (China), Inotiv, Inc. (U.S.), Syngene International Limited (India), Jubilant Biosys Limited (India), Frontage Laboratories, Inc. (U.S.), Altasciences Company Inc. (Canada), CMIC Holdings Co., Ltd. (Japan), Novotech (Australia).

Global Preclinical CRO Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 7.2 billion

- 2026 Market Size: USD 7.7 billion

- Projected Market Size: USD 14.5 billion by 2035

- Growth Forecasts: 8.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (44.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, South Korea, Australia, Singapore, Canada

Last updated on : 23 April, 2026

Preclinical CRO Market - Growth Drivers and Challenges

Growth Drivers

- Rising R&D expenditure in pharma & biotech: Both the pharmaceutical and biotech companies are remarkably increasing their investments in drug discovery and early-stage development. Since the preclinical studies are mostly expensive and resource-intensive, this leads firms to outsource to CROs to optimize costs and speed. In March 2026, the article published by NIH disclosed that there has been a continued growth in biomedical research investment, awarding USD 35.3 billion in extramural grants. The year saw a notable rise in competition, with RPG applications increasing by 12.9%. Although funding remained strong, the shift toward fewer but higher-value awards reflected rising average project costs and forward funding strategies. Overall, NIH maintained stable investment levels, whereas research demand and competition intensified, thus benefiting the overall preclinical CRO market.

NIH FY 2023-2025 Extramural Research Funding, Applications, Awards, and Success Rates: Comprehensive Year-on-Year Statistical Overview

|

Metric |

2023 |

2024 |

2025 |

% Change (2024→2025) |

|

Total extramural awards |

59,102 |

59,063 |

55,394 |

-6.2% |

|

Total extramural funding (USD Billion) |

35.22 |

35.15 |

35.30 |

+0.4% |

|

RPG applications |

51,883 |

55,418 |

62,592 |

+12.9% |

|

New/renewed RPG awards |

11,052 |

10,265 |

8,161 |

-20.5% |

|

RPG success rate |

21.3% |

18.5% |

13.0% |

-29.6% |

|

RPG funding (USD Billion) |

25.365 |

25.729 |

26.503 |

+3.0% |

|

R01-equivalent applications |

35,072 |

37,478 |

42,022 |

+12.1% |

|

R01-equivalent awards |

7,592 |

7,000 |

5,471 |

-21.8% |

|

R01 success rate |

21.6% |

18.7% |

13.0% |

-30.3% |

|

R01 funding (USD Billion) |

19.761 |

20.024 |

20.840 |

+4.1% |

Source: NIH

- Increasing drug development complexity: Modern therapeutics such as biologics, gene therapies, cell therapies, ADCs, and mRNA-based drugs require highly specialized preclinical testing, i.e., toxicology, bioanalysis, and DMPK. This complexity is encouraging companies to opt for a CRO rather than in-house capabilities. According to the article published by NIH in May 2024, the WRIB White stated that modern therapeutics such as gene therapies, cell therapies, mRNA vaccines, and ADCs have increased bioanalytical complexity, which necessitates advanced methods such as LC–MS, MS, immunogenicity testing, and DMPK studies. Besides, it notes key challenges, i.e., nanoparticle quantification, lipid metabolism, and FFPE tissue analysis, which often exceed routine in-house capabilities. As a result, CROs and specialized labs are being used to handle these regulated, high-complexity workflows under frameworks such as ICH M10 and FDA guidance, thus driving upliftment of the preclinical CRO market.

- Regulatory pressure and compliance requirements: Bureaucratic agencies such as the FDA, EMA, and PMDA necessitate huge GLP-compliant preclinical data before clinical trials. Meeting these stringent standards increases outsourcing demand, as CROs already maintain validated regulatory infrastructure. In February 2026, the U.S. Food & Drug Administration (FDA) introduced draft guidance to accelerate individualized therapies for ultra-rare diseases by mainly focusing on genome editing and RNA-based treatments when traditional trials aren’t feasible. It also mentioned that the plausible mechanism framework emphasizes targeting the root genetic cause, leveraging natural history data, and demonstrating evidence even in the case of small patient populations. This initiative aims to streamline approvals, encourage innovation, and expand access to life-saving therapies for patients with rare conditions, thus increasing uptake of the preclinical CRO market.

Challenges

- Regulatory complexity and compliance burden: One of the major burdens hindering expansion of the preclinical CRO market is navigating through strict global regulatory networks, especially good laboratory practice standards. In this context, CROs need to ensure high-quality reproducible data in order to meet requirements from agencies such as the U.S. Food and Drug Administration and Europe Medicines Agency. On the other hand, any variability in regional regulations causes complications to operations for worldwide CROs. Maintaining compliance necessitates continuous investments in infrastructure, training, and quality systems, thereby increasing operational costs. In addition, the continuously evolving regulatory expectations for biologics, gene therapies, and novel modalities add complexity, making it challenging for CROs to stay updated.

- High operational costs and pricing pressure: Preclinical CROs are facing rising operational costs influenced by advanced technologies, skilled workforce requirements, and infrastructure investments. In this context, studies that involve biologics, complex disease models, and specialized assays remarkably increase expenses. At the same time, intense competition, especially from cost-effective regions such as India and China, creates extensive pricing pressure on global players in the preclinical CRO market. Sponsors demand faster timelines and lower costs, which in turn forces CROs to balance profitability along with competitiveness. Investments in terms of automation, digital platforms, and facility upgrades add a huge strain on budgets. Smaller CROs find it struggling to scale operations while maintaining margins, leading to consolidation in the industry.

Preclinical CRO Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.1% |

|

Base Year Market Size (2025) |

USD 7.2 billion |

|

Forecast Year Market Size (2035) |

USD 14.5 billion |

|

Regional Scope |

|

Preclinical CRO Market Segmentation:

End use Segment Analysis

Biopharmaceuticals in the end use segment are forecasted to emerge as the largest, capturing a share of 62.6% in the preclinical CRO market during the forecast period. The segment’s dominance is effectively propelled by increasing R&D complexity and cost pressures. Also, the large pipelines and patent cliffs further drive outsourcing, positioning the segment as the main growth catalyst for the market’s expansion. In August 2025, Altasciences announced that it was selected by Steel Therapeutics to conduct a GLP-compliant pivotal toxicology study for Fizurex. The study, conducted at Altasciences’ preclinical facility, reflects the company’s role in providing integrated preclinical services to accelerate early-stage drug development. This collaboration reflects the prominence of biopharmaceutical development programs that depend on CRO partners for complex preclinical toxicology work.

Service Segment Analysis

In the service segment, toxicology is anticipated to grow with a considerable revenue share in the preclinical CRO market by the end of 2035. The segment’s growth is largely driven by mandatory regulatory requirements before human trials. Meanwhile, the rise of biologics, gene therapies, and complex molecules readily increases demand for advanced safety testing. As stated by the U.S. FDA, its National Center for Toxicological Research (NCTR), in collaboration with Elsevier’s Life Sciences, has uncovered that drug interactions with UGT enzymes are strong predictors of drug-induced liver injury. Besides, their study of 317 drugs showed that pure UGT inhibitors are three times more likely to pose high DILI risk, whereas drugs acting as both substrates and inhibitors raise the risk 13-fold. These findings, part of the liver toxicity knowledge base project, highlight UGT interactions as complementary to the rule-of-two (RO2) in predicting liver toxicity, thus denoting a wider scope for the segment’s growth.

Study Phase Segment Analysis

By the end of 2035, the IND-enabling study in the study phase segment is predicted to grow with a considerable revenue share in the preclinical CRO market as they bridge preclinical and clinical phases. These studies include toxicology, pharmacokinetics, and safety pharmacology that are required for regulatory submissions. Regulatory frameworks make IND-enabling packages essential for clinical approval. In September 2025, the U.S. FDA stated that its official IND framework requires that any drug must undergo an investigational new drug application process before human clinical trials can begin, thereby serving as a legal exemption for interstate distribution and clinical testing. In addition, it also stated that this application needs to include preclinical data such as toxicology, pharmacology, and safety assessments to ensure that the product does not expose humans to unreasonable risk.

Our in-depth analysis of the preclinical CRO market includes the following segments:

|

Segment |

Subsegments |

|

End use |

|

|

Service |

|

|

Study Phase |

|

|

Model Type |

|

|

Service Mode |

|

|

Therapeutic Area |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Preclinical CRO Market - Regional Analysis

North America Market Insights

The North America preclinical CRO market is anticipated to garner the largest share of 44.5% by the conclusion of the forecasted period. The region benefits from a well-established pharmaceutical industry and advanced research infrastructure. In addition, the region’s strong focus on innovation, drug safety, and scientific excellence continues to drive sustained preclinical CRO market growth. As per the article published by CCRPS in September 2025, the U.S. preclinical and clinical CRO ecosystem is highly concentrated, wherein the major organizations such as IQVIA, ICON, Parexel, and Fortrea actively support large-scale drug development programs across therapeutic areas. It states that these CROs play a central role in delivering clinical operations services, including monitoring, data management, and trial execution for pharmaceutical and biotechnology sponsors. Their continued expansion reflects strong outsourcing demand from biopharma companies, particularly in early- and late-stage drug development programs requiring specialized clinical research support.

A high concentration of pharmaceutical and biotechnology companies is responsibly driving the preclinical CRO market in the U.S. Strong regulatory standards, rapid adoption of advanced technologies, and an ongoing focus on early-stage drug development ensure the country’s unprecedented leadership in outsourcing preclinical research services. In July 2025, Veranex announced the launch of the industry’s first Innovation CRO (iCRO), which is an integrated platform designed to accelerate medical device and IVD development from concept to commercialization with speed, efficiency, and payer-ready evidence. It is built on four pillars, i.e., capital efficiency, evidence integration, device-specific expertise, and regulatory alignment, whereas the model reduces timelines and budget variance while ensuring global market access, thus suitable for bolstering the country’s preclinical CRO market growth.

In Canada, the preclinical CRO market has gained enhanced exposure owing to the rising R&D investments from biotechnology and pharmaceutical companies who are looking to accelerate early-stage drug development. Specialized services, particularly in bioanalysis, drug metabolism and pharmacokinetics, and safety pharmacology, are in high demand to support growing biologics and cell therapy pipelines. In April 2026, the government of Canada generously invested a total of USD 50 million to support the Canadian Critical Drug Initiative (CCDI) in Edmonton, Alberta, to strengthen domestic pharmaceutical manufacturing capacity. This funding will help Applied Pharmaceutical Innovation and the University of Alberta build the Critical Medicines Production Centre, enabling large-scale production of essential medicines, thus denoting an optimistic preclinical CRO market opportunity.

APAC Market Insights

The Asia Pacific preclinical CRO market is expected to witness the fastest growth from 2026 to 2035. The region’s growth in this field is mainly attributable to rising chronic disease prevalence and the outsourcing of toxicology, bioanalysis, and drug metabolism and pharmacokinetics studies to high-quality regional providers. Key hubs such as China, India, and Japan are experiencing accelerated growth due to supportive government policies, adoption of advanced technologies, i.e., AI/cloud, and specialized services, including patient-derived organoid and xenograft models for oncology research. Based on government data published in December 2025, Australia’s R&D tax incentive program is the government’s largest lever for funding innovation, which has been jointly administered by the ATO and the Department of Industry, Science, and Resources. It encourages companies to undertake R&D, boosting competitiveness and productivity across the economy. It raised the expenditure threshold to USD 150 million and strengthened anti-avoidance rules.

The increasing domestic pharmaceutical R&D expenditure, rising demand for biologics and cell therapy development, and the modernization of regulatory standards are responsible for uplifting the preclinical CRO market in China. The country’s market growth is heavily supported by regulatory shifts aligning with international standards, thereby encouraging the outsourcing of non-core research activities to enhance efficiency and accelerate drug discovery. In October 2025, the National Medical Products Administration introduced a 30-day expedited clinical trial review pathway along with the existing 60-day implicit approval system to accelerate innovative drug development. This pathway balances speed with safety by adhering to ICH standards, requiring early risk management planning, and strengthening collaboration among sponsors, investigators, and ethics committees. Therefore, such regulatory support indicates that China is strengthening its preclinical and clinical research ecosystem, accelerating IND-enabling timelines, and increasing reliance on CRO services for faster drug development.

The preclinical CRO market in India is growing exponentially as a predominant hub for drug discovery, toxicology testing, and bioanalysis. Driven by increased outsourcing from pharmaceutical companies, key players are adopting advanced technologies such as AI and specialized modeling to accelerate R&D. In March 2026, the Journal of Medicinal Chemistry reported that India, long recognized as the world’s pharmacy and a global leader in generics and vaccines, is now seeing CROs emerge as vital innovation partners. Talent migration from pharma and on-the-job learning have enabled CROs to support biotech firms and academia in advancing novel drug candidates. At the same time, opportunities are present in their operational efficiency, end‑to‑end capabilities, and integration with global partnerships, academia, and government initiatives, thus positively impacting the preclinical CRO market’s growth and exposure.

Europe Market Insights

Europe preclinical CRO market is anticipated to grow considerably during the discussed timeframe. The region’s market is effectively driven by increasing pharmaceutical R&D spending, rising demand for advanced therapeutic studies, and the need for specialized toxicology and bioanalytical services. The region's clinical trials regulation, which has been effective since January 2022, harmonizes the assessment and supervision of clinical trials across Member States and EEA countries. It introduced the clinical trials information system, which allows sponsors to submit a single online application for multinational trials, improving efficiency, transparency, and participant safety. A transition period ended in January 2023, making CTIS mandatory for new trials, and by January 2025, all ongoing trials under the old directive complied with the new regulation, marking a major step in fostering larger collaborative studies in Europe.

The heightened demand for advanced biologics and high-quality GLP-compliant services are certain factors boosting the preclinical CRO market in Germany. Key trends reshaping the country’s market include a strong focus on personalized medicine, oncology, and the adoption of complex, non-animal testing models, alongside the increasing need for specialized services in mRNA therapeutics. In April 2026, Dynamic42 GmbH and EPO Berlin-Buch formed a strategic collaboration with a collective goal to integrate organ-on-chip technology into preclinical glioblastoma research, aiming to improve translational relevance. By combining Dynamic42’s BBB-on-chip model with EPO’s expertise in translational oncology and patient-derived tumor material, the partnership seeks to generate more human-relevant data and reduce late-stage drug development failures. Hence, such instances will position CROs as innovation partners that deliver more predictive data and reduce late-stage drug development failures.

The preclinical CRO market in the UK is growing at an extensive pace, attributable to the strong integration of academic excellence, translational research networks, and a supportive regulatory environment. The country also benefits from its emphasis on early-stage innovation, especially through collaborations between universities, biotech startups, and CROs that specialize in complex modalities such as cell and gene therapies. Based on the government data published in October 2025, the country halved clinical trial approval times from 91 to 41 days through AI-driven tools and regulatory reforms, giving patients faster access to life-saving treatments. The MHRA’s risk-proportionate approach, digital dashboards, and AI compliance checkers streamline reviews while maintaining safety standards. Therefore, these changes strengthen the country’s global research appeal, modernize trial processes, and position it as a leader in clinical innovation, thus making it suitable for standard preclinical CRO market growth.

Key Preclinical CRO Market Players:

- Charles River Laboratories International, Inc. (U.S.)

- Labcorp Drug Development (U.S.)

- WuXi AppTec Co., Ltd. (China)

- Eurofins Scientific SE (Luxembourg)

- ICON plc (Ireland)

- Evotec SE (Germany)

- Medpace Holdings, Inc. (U.S.)

- Thermo Fisher Scientific (PPD) (U.S.)

- Parexel International Corporation (U.S.)

- SGS SA (Switzerland)

- RSSL (UK)

- ERBC (Italy)

- Crown Bioscience (United States)

- Turbine (Netherlands)

- Menarini Biotech (Italy)

- X-Chem (U.S.)

- QPS (U.S.)

- Ryght AI (U.S.)

- Intertek Group plc (UK)

- Pharmaron Beijing Co., Ltd. (China)

- JOINN Laboratories (China)

- Inotiv, Inc. (U.S.)

- Syngene International Limited (India)

- Jubilant Biosys Limited (India)

- Frontage Laboratories, Inc. (U.S.)

- Altasciences Company Inc. (Canada)

- CMIC Holdings Co., Ltd. (Japan)

- Novotech (Australia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Charles River Laboratories International is one of the most dominant players in this sector, which is offering a complete spectrum of services from early discovery to safety assessment and IND-enabling studies. At the same time, the company has spent years building a strong global footprint through acquisitions and facility expansion, positioning itself as an end-to-end partner for biopharma clients.

- Labcorp Drug Development is also a prominent player in this field that provides inclusive non-clinical and preclinical services along with clinical development capabilities. Besides, the firm leverages its scale, data capabilities, and global infrastructure to support complex studies, including toxicology and bioanalytical services.

- WuXi AppTec is a leading global CRO that is best known for its extensive service portfolio spanning discovery, preclinical testing, and manufacturing. The company makes continued investments in advanced technologies and capacity expansion to meet rising demand for outsourced R&D services, especially in terms of biologics and cell and gene therapies.

- Eurofins Scientific has been operating as a big network of laboratories across the globe by providing preclinical testing, bioanalysis, and safety assessment services. The company’s decentralized and highly specialized lab structure allows it to manage different client needs across multiple therapeutic areas.

- Syngene International is a prominent CRO based in India, and it offers integrated discovery and preclinical services to global pharmaceutical and biotech companies. In addition, the company is expanding its infrastructure and partnerships by focusing on biologics, toxicology, and translational research to strengthen its position in the global outsourcing landscape.

Below is the list of some prominent players operating in the global preclinical CRO market:

The preclinical CRO market is considered to be moderately consolidated, which is being led by global players such as Charles River, Labcorp, and WuXi AppTec, along with regional specialists in the Asia Pacific and Europe. Competition in this field is effectively driven by integrated service offerings, technological capabilities, and geographic expansion. At the same time, key preclinical CRO market pioneers are opting for AI-based drug discovery tools, advanced in vitro models, and organoid platforms with the main goal to enhance efficiency and translational accuracy. Strategic initiatives pursued are mergers and acquisitions, partnerships with biotech firms, and expansion of GLP-compliant facilities, particularly in cost-efficient economies such as India and China. In September 2025, RSSL and ERBC formed a strategic partnership by combining preclinical safety and regulatory knowledge with GMP analytical capabilities to deliver seamless, end-to-end drug development support.

Corporate Landscape of the Preclinical CRO Market:

Recent Developments

- In April 2026, Crown Bioscience partnered with Turbine to integrate AI-based in silico predictions with tumor organoid validation, creating a connected workflow for translational oncology research. This collaboration links predictive modeling with experimental validation to improve accuracy.

- In December 2025, ERBC and Menarini Biotech formed a strategic partnership to streamline biopharmaceutical development from preclinical research to first-in-human trials through an integrated CRO-CDMO approach. This collaboration aims to accelerate IND readiness, reduce development bottlenecks, and enable cost-effective transition to clinical stages.

- In October 2025, Charles River announced a partnership with X-Chem to integrate its DNA-encoded library of 15 billion compounds with Charles River’s hit identification expertise. This collaboration creates a seamless workflow from hit discovery to lead optimization, accelerating early drug development for biopharma clients.

- In January 2025, QPS partnered with Ryght AI as its exclusive AI collaborator to optimize and automate clinical trials globally, while adding QPS’s 750 research sites across 17 countries to the Ryght Research Network. This alliance combines Ryght’s generative AI technology with QPS’s clinical expertise to streamline site selection, enrollment, and workflows.

- Report ID: 8530

- Published Date: Apr 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.