Power Purchase Agreement (PPA) Platform Market Outlook:

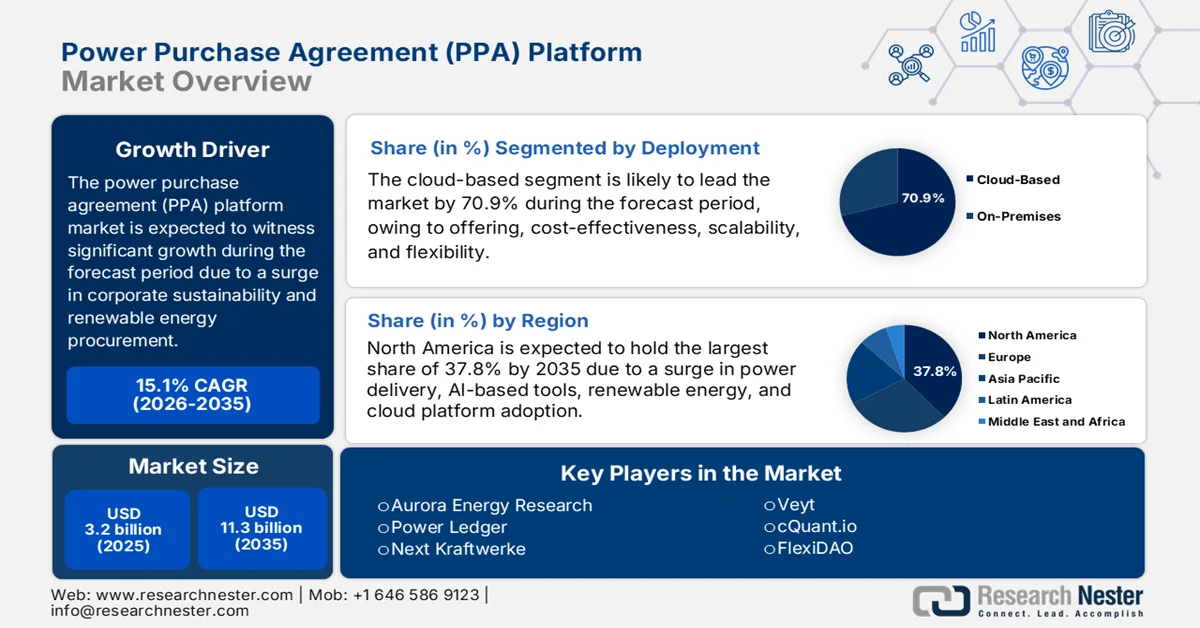

Power Purchase Agreement (PPA) Platform Market size was valued at over USD 3.2 billion in 2025 and is projected to reach USD 11.3 billion by the end of 2035, with a CAGR of 15.1% during the forecast period, i.e., 2026-2035. In 2026, the industry size of power purchase agreement (PPA) platform is assessed at USD 3.6 billion.

The power purchase agreement (PPA) platform market is readily shaped by different ancillary factors, including an increase in the sophistication of corporate sustainability frameworks, the adoption of verifiable renewable energy procurement methods, a rise in the availability of high-frequency weather and grid data, and the continued growth of venture capital as well as private equity funding for technological software startups. According to official statistics published by the IRENA Organization in 2025, there is an increasing demand for immediate and rapid action for reducing global net anthropogenic carbon dioxide emissions by nearly 50% by the end of 2030. Besides, as per the 2026 IEA Organization article, the renewable power capacity growth is gradually continuing, with a rise in overall renewable electricity capacity to 4,500 GW, thus expanding contracts for different businesses.

Global Net Renewable Electricity Capacity by Technology, 2017-2024

|

Year |

PV-Utility |

PV-Distributed |

Onshore Wind |

Offshore Wind |

Hydropower |

Bioenergy |

Others |

|

2017 |

63.0 GW |

35.0 GW |

43.7 GW |

3.8 GW |

24.5 GW |

6.4 GW |

0.7 GW |

|

2018 |

57.3 GW |

42.0 GW |

44.3 GW |

4.2 GW |

23.1 GW |

8.5 GW |

1.2 GW |

|

2019 |

67.3 GW |

44.1 GW |

53.1 GW |

6.2 GW |

18.2 GW |

7.7 GW |

1.3 GW |

|

2020 |

86.5 GW |

61.1 GW |

104.1 GW |

5.9 GW |

18.4 GW |

9.2 GW |

0.7 GW |

|

2021 |

89.5 GW |

73.8 GW |

74.9 GW |

19.8 GW |

30.0 GW |

9.9 GW |

0.3 GW |

|

2022 |

112.6 GW |

107.4 GW |

63.0 GW |

11.4 GW |

32.4 GW |

7.8 GW |

1.1 GW |

|

2023 |

150.8 GW |

136.2 GW |

107.1 GW |

17.0 GW |

22.4 GW |

6.5 GW |

2.6 GW |

|

2024 |

167.2 GW |

140.3 GW |

103.1 GW |

18.1 GW |

24.0 GW |

7.9 GW |

1.9 GW |

Source: IEA Organization

Furthermore, the embedded carbon accounting integration, behavioral nudges and gamification for procurement teams, and secondary PPA trading marketplaces are a few trends that are responsible for boosting the power purchase agreement (PPA) platform market globally. As stated in a data report published by the Department of Energy in February 2024, the worldwide renovation and construction of buildings effectively caters to 5% if energy utilization, along with 10% of carbon emissions. Therefore, to gain low-carbon new construction buildings, increased efforts are necessary to diminish the embodied carbon of buildings. Besides, construction organizations, designers, and architects have a suitable opportunity to lower embodied carbon through approaches, including construction practices and improved designs, thereby making it suitable for bolstering the power purchase agreement (PPA) platform market expansion.

Key Power Purchase Agreement (PPA) Platform Market Insights Summary:

Regional Highlights:

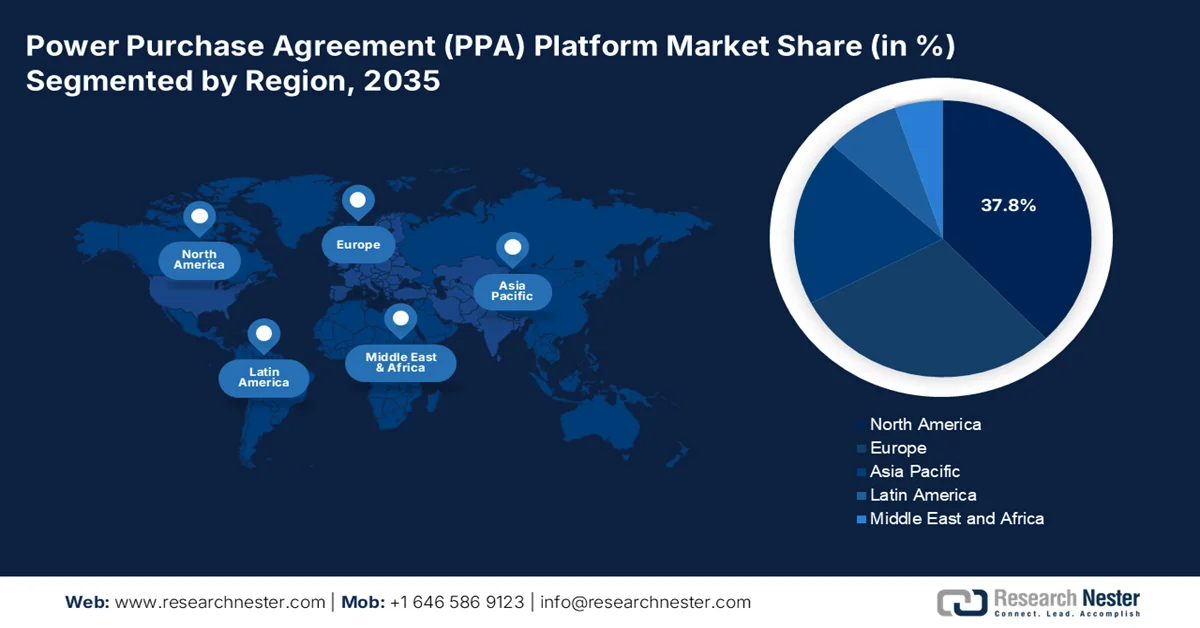

- North America is projected to dominate the power purchase agreement (PPA) platform market with a 37.8% share by 2035, propelled by accelerating renewable energy adoption and increasing integration of AI-driven contract optimization tools

- Asia Pacific is anticipated to witness the fastest growth in the forecast period, impelled by expanding renewable energy investments and rising digitalization of energy procurement processes

Segment Insights:

- Cloud-based segment in the power purchase agreement (PPA) platform market is projected to account for a 70.9% share by 2035, driven by increasing demand for scalable, flexible, and cost-efficient cloud infrastructure solutions

- Software sub-segment is expected to secure the second-highest share over the forecast period 2026–2035, owing to rising global software investments and its role in enhancing development efficiency and system maintainability

Key Growth Trends:

- Decentralized renewable energy assets

- Rise in energy price volatility across liberalized economies

Major Challenges:

- Credit risk and counterparty trust deficit

- Integration with legacy energy systems

Key Players: Schneider Electric, Enel SpA, RWE, Statkraft, ENGIE, LevelTen Energy, Pexapark, REsurety, Aurora Energy Research, Power Ledger, Next Kraftwerke, Zeigo, Anthesis, Veyt, cQuant.io, FlexiDAO, KYOS, Astatine Ltd., Ecohz.

Global Power Purchase Agreement (PPA) Platform Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.2 billion

- 2026 Market Size: USD 3.6 billion

- Projected Market Size: USD 11.3 billion by 2035

- Growth Forecasts: 15.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (37.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, Canada

- Emerging Countries: India, Japan, Australia, South Korea, Brazil

Last updated on : 21 April, 2026

Power Purchase Agreement (PPA) Platform Market - Growth Drivers and Challenges

Growth Drivers

- Decentralized renewable energy assets: The worldwide transition from central power generation to distributed energy resources, such as community wind projects, behind-the-meter batteries, and rooftop solar, is significantly driving the power purchase agreement (PPA) platform market globally. According to official statistics published by the World Bank Organization in June 2025, 92% of the world population presently has basic accessibility to electricity. In addition, this denotes a suitable improvement since 2022, wherein the accessibility was decreased, with more than 666 million people devoid of the access. Besides, over 2 million people rely on hazardous and polluting fuels, including charcoal and firewood, for cooking demands, thereby denoting a huge growth opportunity for the market across different countries.

- Rise in energy price volatility across liberalized economies: The presence of deregulated electricity industries across regions, such as the UK, Germany, and Texas, has witnessed price spikes, which are positively enhancing the power purchase agreement (PPA) platform market demand. As stated in an article published by the OECD in April 2026, energy-based prices readily account for a massive share of consumer expenditure, ranging from nearly 12% in Brazil to almost 6% in Canada. However, to overcome this, fuel tax reductions are the most widely utilized instrument to lower the tax on retail prices directly. For instance, Latvia successfully diminished diesel excise duties by almost 15%, amounting to USD 0.08 per liter, and meanwhile, Ireland reduced them by USD 0.2 per liter, thus positively fueling the market demand globally.

- Maturation of green hydrogen project financing: The green hydrogen production has deliberately shifted from pilot phase to commercial-scale project development, which is yet another driver for the power purchase agreement (PPA) platform market globally. As per an article published by the IRENA Organization in 2025, electrification, renewables, and energy efficiency tend to achieve 70% of mitigation demand, based on which there is an increase in the need for hydrogen for decarbonizing end uses, wherein other options are usually expensive and less mature. Besides, considering this particular application, hydrogen is intended to contribution 10% of the mitigation required to meet the IRENA 1.5 degrees Celsius, along with 12% of the finalized energy demand. Therefore, with all these benefits, the demand for hydrogen is continuously increasing, which is proliferating the power purchase agreement (PPA) platform market growth.

Challenges

- Credit risk and counterparty trust deficit: Contracts in the power purchase agreement (PPA) platform market usually span 10 to 20 years, making counterparty creditworthiness a paramount concern. Digital platforms, despite their efficiency, cannot fully eliminate the deep-seated anxiety buyers and sellers feel about long-term financial commitments made through software intermediaries. Besides, corporate buyers, especially smaller or mid-sized firms, might lack investment-grade credit ratings, making developers hesitant to commit renewable capacity to them. Conversely, developers on platforms may be early-stage or independent power producers with unproven track records, raising red flags for risk-averse corporate treasurers. Traditional credit assessment methods are slow, opaque, and poorly suited to the dynamic nature of platform-based deal flow.

- Integration with legacy energy systems: Most electricity grids and utility back-offices were designed decades ago for centralized, predictable power flows, and not for the decentralized, dynamic nature of corporate renewable PPAs. PPA platforms generate optimized contract terms and schedules, but executing those contracts requires seamless integration with grid operators, metering systems, billing engines, and settlement platforms. Unfortunately, many utilities still operate on mainframe-based systems with limited API capabilities. Real-time generation data from renewable assets often flows through proprietary monitoring systems that resist external access. This disconnect means that even after a PPA is signed digitally, and the actual delivery, measurement, and settlement processes remain manual, error-prone, and time-consuming, which negatively impacts the power purchase agreement (PPA) platform market globally.

Power Purchase Agreement (PPA) Platform Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

15.1% |

|

Base Year Market Size (2025) |

USD 3.2 billion |

|

Forecast Year Market Size (2035) |

USD 11.3 billion |

|

Regional Scope |

|

Power Purchase Agreement (PPA) Platform Market Segmentation:

Deployment Segment Analysis

Based on the deployment, the cloud-based segment is anticipated to garner the highest share of 70.9% in the power purchase agreement (PPA) platform market by the end of 2035. The segment’s upliftment is primarily attributed to its importance for modernized businesses in providing suitable benefits in flexibility, scalability, and cost efficiencies, and also in combating the demand for maintaining physical and on-premise infrastructure. According to official statistics published by the World Bank Organization in March 2025, the adoption of Europe-specific highly secured and environmentally friendly edge nodes, along with effectively promoting businesses’ engagement in artificial intelligence and big data, led to cloud computing unlocking 55% of the overall economic valuation. Besides, Argentina has deliberately aimed to bolster data utilization for digital transformation through a cloud-first policy by targeting a migration of 80% of domestic government to cloud-driven systems by the end of 2027, thus driving the segment’s growth globally.

Component Segment Analysis

During the forecast period, the software sub-segment, which is part of the component segment, is projected to account for the second-highest share in the power purchase agreement (PPA) platform market. The sub-segment’s growth is effectively driven by its importance in developing blocks in modernized software engineering for enhancing developmental speed, and ensuring quality and maintainability through reutilization. As stated in an article published by the World Intellectual Property Organization (WIPO) in June 2025, the worldwide software expenditure has successfully reached USD 675 billion as of 2024, demonstrating almost 50% from the previous 2020 level of USD 454 billion. Based on this growth, the U.S. deliberately maintains a suitable lead in software investment, amounting to USD 368.5 billion in 2024, which is over half of the world’s overall and almost 6-times the upcoming largest spender. Therefore, with such a focus on generous investment, there is a huge growth opportunity for the sub-segment.

Type Segment Analysis

The virtual PPA sub-segment, which is part of the type segment, is expected to grab the third-highest share in the power purchase agreement (PPA) platform market by the end of the stipulated timeline. The sub-segment’s development is highly propelled by enabling corporations to support renewable energy development without the need for direct ownership and providing a hedge against sustainability objectives, long-lasting price predictability, and electricity price volatility. As per an article published by NLM in July 2022, countries, such as Europe, have effectively pledged to achieve carbon neutrality by the end of 2050 to restrict worldwide warming below 1.5 degrees Celsius. This achievement demands an increase in shares for intermittent renewable energy generation and the adaptation of high grids, thereby making it suitable for fueling the sub-segment.

Our in-depth analysis of the power purchase agreement (PPA) platform market includes the following segments:

|

Segment |

Subsegments |

|

Deployment |

|

|

Component |

|

|

Type |

|

|

End use |

|

|

Application |

|

|

Solution |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Power Purchase Agreement (PPA) Platform Market - Regional Analysis

North America Market Insights

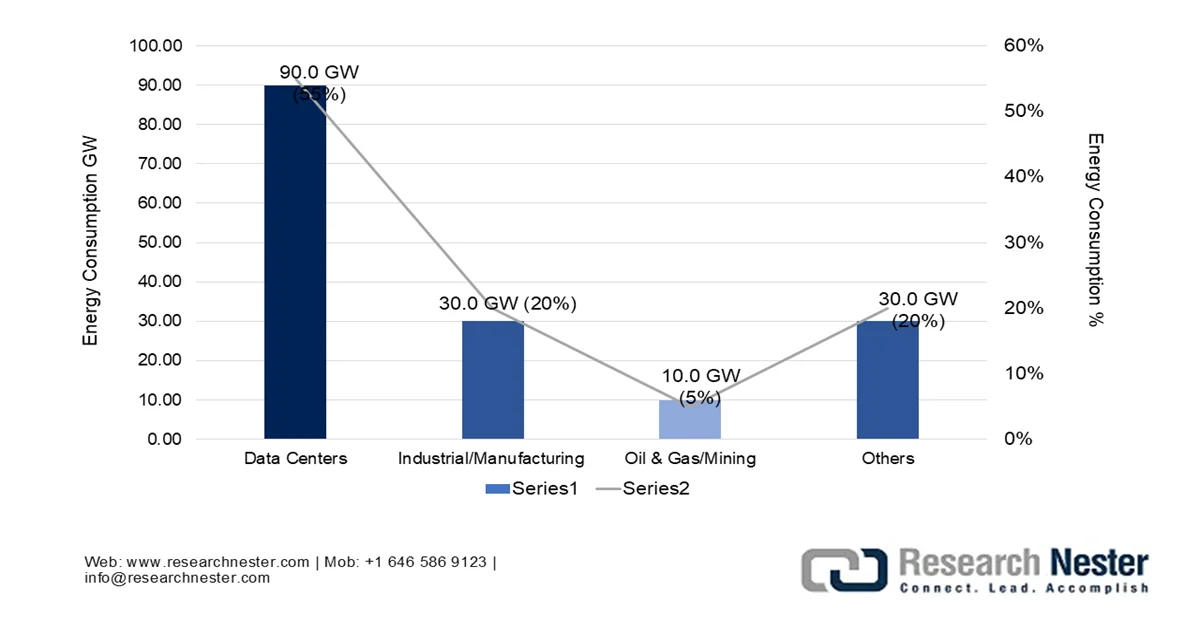

North America in the power purchase agreement (PPA) platform market is anticipated to grab the largest share of 37.8% by the end of 2035. The market’s upliftment in the region is primarily fueled by the robust renewable energy adoption in both the U.S. and Canada, the increasing adoption of cloud-based platforms, the rise in virtual PPA for ensuring financial settlement without physical power delivery, and the integration of AI-driven valuation tools for contract optimization. According to official statistics published by the World Resources Institute in February 2024, 90% of the latest energy capacity added in the U.S. derived from clean sources. Besides, there is a demand for electricity as of 2025, demonstrating a 2% rise from 2024 and 9% from 2020. Moreover, there has also been a rise in utilities projects demanding a 32% domestic rise in the energy demand, with data centers consuming 9% to 17% of overall electricity by the end of 2030, thus boosting the power purchase agreement (PPA) platform market growth.

Data Centers Driving the Energy Demand in the U.S., 2025-2030

Source: World Resources Institute

The power purchase agreement (PPA) platform market in the U.S. is growing significantly, owing to the hyperscaler-based data center demand surge, the policy-based economy complexity and escalation, along with a focus on ESG mandates and corporate decarbonization commitments. As stated in an article published by NLM in November 2023, the federal government in the country has readily established objectives of electrifying 50% of the latest light-duty vehicle sales by the end of 2030. Additionally, this is projected to diminish domestic-wide greenhouse gas emissions by 50% to 52% by the end of the same year. Besides, emissions are further expected to be reduced by 45% based on achieving both grid decarbonization and vehicle electrification objectives by the end of 2035. Therefore, all these projections and goals are readily responsible for bolstering the market in the country.

The provincial policy divergence and industry rebalancing, the long-lasting corporate demand pipeline, and indigenous-based development with the newest structures are certain factors for driving the power purchase agreement (PPA) platform market in Canada. As per an article published by the Government of Canada in October 2023, of the USD 22.6 billion spent on in-house research and development by industry in the country, 7.5% or USD 1.7 billion was based on energy. In addition, fossil fuels significantly make up the largest energy-based R&D at 32%, despite there has been a decrease in spending for 8 consecutive years. Moreover, the government in the country is generously investing and funding different electrification as well as smart renewables pathway projects. Therefore, based on all these developments and approaches, the power purchase agreement (PPA) platform market is continuously expanding in the country.

Funding/Investments for Smart Renewables and Electrification Pathways Program in Canada, 2025-2026

|

Project Name |

Organization Name |

Project Location |

Deployment or Capacity Building |

SREPs Funding |

Overall Project Expenses |

Announcement Date |

|

Grid Forward Saint John Project |

The Power Commission of the City of Saint John |

New Brunswick |

Deployment |

USD 9,736,427 |

USD 19,472,854 |

March 2027 |

|

Mersey River Wind Farm |

Mersey River Wind Inc. |

Nova Scotia |

Deployment |

USD 25,000,000 |

USD 292,935,303 |

February 2026 |

|

Atlantic Offshore Wind & Transmission Readiness Program |

Net zero Atlantic |

Nova Scotia |

Capacity Building |

USD 4,848,200 |

USD 5,546,880 |

February 2026 |

|

WMA Capacity Development |

Wskijinu’k Mtmo’taqnuok |

Nova Scotia |

Capacity Building |

USD 220,210 |

USD 420,210 |

January 2026 |

|

Reinforcing Canadian Energy Modelling Capacities |

The Governors of the University of Calgary |

Alberta |

Capacity Building |

USD 4,999,999 |

USD 6,784,704 |

December 2025 |

|

Développement du projet de centrale hydroélectrique Matawak |

Énergie Matawak société en commandite |

Québec |

Deployment |

USD 1,763,213 |

USD 2,350,950 |

October 2025 |

Source: Natural Resources Canada

APAC Market Insights

The Asia Pacific in the power purchase agreement (PPA) platform market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by an increase in expanding renewable energy, particularly in India and China, growing corporate decarbonization commitments, and an increase in digitalizing energy procurement processes, and the integration of AI-based risk analytics. According to official statistics published by the UNECE in June 2025, the transition to clean energy in the region effectively requires generous investments, which are estimated to be worth USD 150 billion by the end of 2030. Moreover, by relatively embracing digitalization for transmission, generation, end use, and distribution, along with integrating renewable energy for reducing carbon emissions by almost 70% and energy expenses by 80%, thus proliferating the market development.

The power purchase agreement (PPA) platform market in China is gaining increased traction, owing to gaining electricity from renewables, implementing suitable policies for encouraging corporate renewable procurement, as well as an increase in pressure for the chemical and industrial sectors to decarbonize and the creation of a sustained need for digital PPA platforms. As stated in an article published by the State Council Information Office in January 2026, there has been a remarkable expansion in the country’s overall installed capacity by 600 million kilowatts in November 2025. Based on this, the country’s total installed power-generating capacity has effectively reached 3.7 billion kW by the end of 2025, indicating a 17.1% year-on-year (YoY) increase. Besides, the solar power capacity grew by 41.9% YoY, which is 1.1 million kW, thus denoting an optimistic outlook for the power purchase agreement (PPA) platform market development.

The aspects of the rapid renewable energy growth, the chemical manufacturing units adopting a renewable procurement framework, sustainability requirements, cost considerations, open accessibility to large-scale industrial and commercial for energy procurement, an increase in corporate renewable transactions, and energy costs for chemical production are a few trends that are significantly responsible for bolstering the power purchase agreement (PPA) platform market in India. Based on government estimates published by the PIB Government in January 2026, there has been an expansion in natural gas pipelines by 25,400 km, deliberately enabling almost 100% CGD geographical coverage throughout the nation. Besides, ethanol blending effectively reached 19.0% in ESY between 2024 and 2025, which approached the 20% national target. Moreover, in terms of clean cooking energy accessibility, the Pradhan Mantri Ujjwala Yojana (PMUY) expanded, with domestic beneficiaries reaching almost 104 million in January 2026, thus boosting the market upliftment.

Europe Market Insights

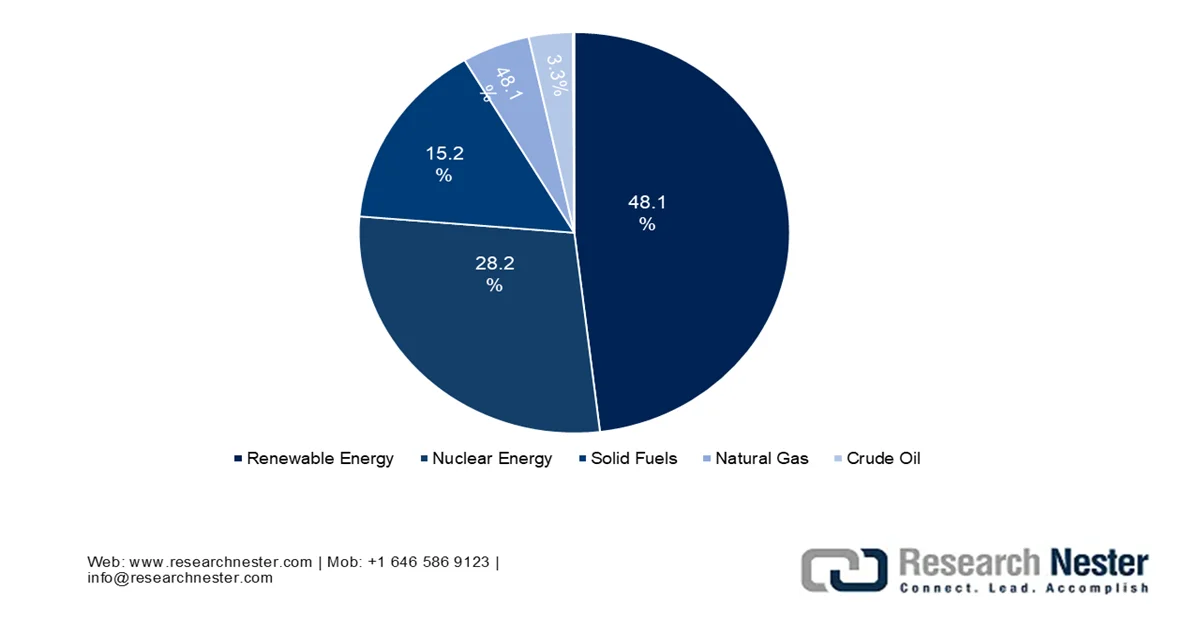

Europe in the power purchase agreement (PPA) platform market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is readily fueled by the ambitious decarbonization agenda, the phase-out of fossil-fuel generation, the hybridization of PPAs for combined solar and wind, along with the emergence of green hydrogen production. According to official statistics published by the Europe Commission in 2026, the region produced 43% of its own energy and significantly imported 57% as of 2024. In addition, the energy mix in the region is mainly comprised 38% of crude oil and petroleum products, 21% of natural gas, 20% of renewable energy, 12% of nuclear energy, and 10% of solid fuels. Out of these, petroleum-based products were extremely high in Cyprus, accounting for 86%, which is followed by 85% in Malta and 60% in Luxembourg, thus bolstering the power purchase agreement (PPA) platform market in the region.

Energy Production by Source in Europe, 2024

Source: Europe Commission

The power purchase agreement (PPA) platform market in Germany is gaining increased exposure, owing to the aggressive expansion in renewables, the presence of massive consumers and its central geographic role as the ultimate electricity trading facility, the growing integration of PPA platforms with industrial energy management systems, and government support for digital energy trading infrastructure. As stated in an article published by the IEA Organization in 2026, the largest sources of electricity generation accounted for 27% of wind and 24% of coal in the country. Based on these two essential sources, the overall domestic electricity production caters to 510,034 GWh as of 2024, which is about 12% of the global trend. Besides, the net electricity imports accounted for 5.8% of the 2024 total electricity finalized consumption, along with 81% trend in electricity imports, thus driving the market expansion.

The increased solar energy volume, a favorable regulatory environment for generously attracting investments in renewable generation, utilization of digitalized platforms by manufacturers to ensure long-lasting fixed-price renewable contracts, matured hydrogen projects, and the robust participation from technological industry buyers are a few trends propelling the power purchase agreement (PPA) platform market in Spain. As per an article published by the Global Energy Monitor Organization in June 2024, the country accounts for the largest utility-scale solar capacity in operation, with 29.5 GW than any other country in the overall region. Additionally, the country also has increased capacity under construction, catering to 7.8 GW and 106.1 GW in the early stages of development. Therefore, with this accountability and additional solar energy sources for different application is readily responsible for boosting the market in the country.

Key Power Purchase Agreement (PPA) Platform Market Players:

- Schneider Electric (France)

- Enel Spa (Italy)

- RWE (Germany)

- Statkraft (Norway)

- ENGIE (France)

- LevelTen Energy (U.S.)

- Pexapark (Switzerland)

- REsurety (U.S.)

- Aurora Energy Research (UK)

- Power Ledger (Australia)

- Next Kraftwerke (Germany)

- Zeigo (UK)

- Anthesis (UK)

- Veyt (Norway)

- cQuant.io (U.S.)

- FlexiDAO (Spain)

- KYOS (Netherlands)

- Astatine Ltd. (UK)

- Ecohz (Norway)

- CFP FlexPower GmbH (Germany)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Schneider Electric provides digital power purchase agreement (PPA) platform market integrated within its broader energy management ecosystem, enabling corporate buyers to match renewable generation with real-time consumption patterns. The company focuses on streamlining the entire PPA lifecycle, from origination to compliance reporting, through its cloud-based software solutions.

- Enel Spa operates proprietary power purchase agreement (PPA) platform market that leverage its vast renewable asset portfolio to offer flexible, customized contracting options for industrial and commercial clients. The company emphasizes digital tools that simplify long-term price hedging and renewable energy certificate management for its counterparties.

- RWE has developed sophisticated PPA platforms that primarily serve its utility-scale wind and solar projects, allowing off-takers to secure stable green power directly from the developer. The platform prioritizes transparent pricing models and contract standardization to reduce negotiation friction between buyers and sellers.

- Statkraft offers a PPA platform renowned for its advanced risk management capabilities, helping corporate clients navigate volatile energy markets with tailored hedging strategies. The company integrates its deep hydropower expertise into the platform, providing baseload stability that intermittent sources cannot guarantee alone.

- ENGIE delivers a multi-service PPA platform that combines renewable procurement with energy efficiency analytics and carbon offset tracking under one digital roof. The platform is designed to serve diverse client segments, from small commercial entities to large industrial facilities, through modular contract structures.

Here is a list of key players operating in the global power purchase agreement (PPA) platform market:

The power purchase agreement (PPA) platform market is rapidly evolving and highly competitive, characterized as a technology-driven space where energy producers and corporate buyers connect through digital solutions. The market features a moderately fragmented landscape with several established Europe-based energy giants and specialized software providers competing for market share. The top five players collectively held the majority of the global market share in 2025, indicating a consolidated yet contestable competitive environment. Besides, in October 2025, ENGIE entered into a PPA with Meta for its latest Swenson Ranch solar farm in Texas. This particular 600 MW project is ENGIE’s largest asset in the overall U.S., with the availability of over 11 GW of capacity in operation and under construction, particularly for batteries, wind, and solar, which is positively impacts the power purchase agreement (PPA) platform industry globally.

Corporate Landscape of the Power Purchase Agreement (PPA) Platform Market:

Recent Developments

- In December 2025, NextEra Energy Resources, LLC and Meta Platforms Inc. successfully strengthened their energy leadership by reaching an estimated 2.5 GW of clean energy contracts, and further enabled 2.1 GW of clean energy through 9 projects across the Electric Reliability Council of Texas (ERCOT), Southwest Power Pool (SPP), AND Midcontinent Independent System Operator (MISO).

- In November 2025, TotalEnergies and Google significantly signed a 15-year PPA to supply a total volume of 1.5 TWh of certified renewable electricity from the Montpelier solar farm in Ohio, which is extremely suitable for supporting the data center operations of Google.

- In November 2025, EnBW Energie Baden-Württemberg AG and Siemens Energy signed a long-lasting PPA for the Frankenförde photovoltaic plant in Brandenburg, which is a solar park that is located at an estimated 60 kilometers from Berlin, suitable for supplying Siemens with green electricity based on a 10-year contract.

- Report ID: 8522

- Published Date: Apr 21, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.