Power Inductor Market Outlook:

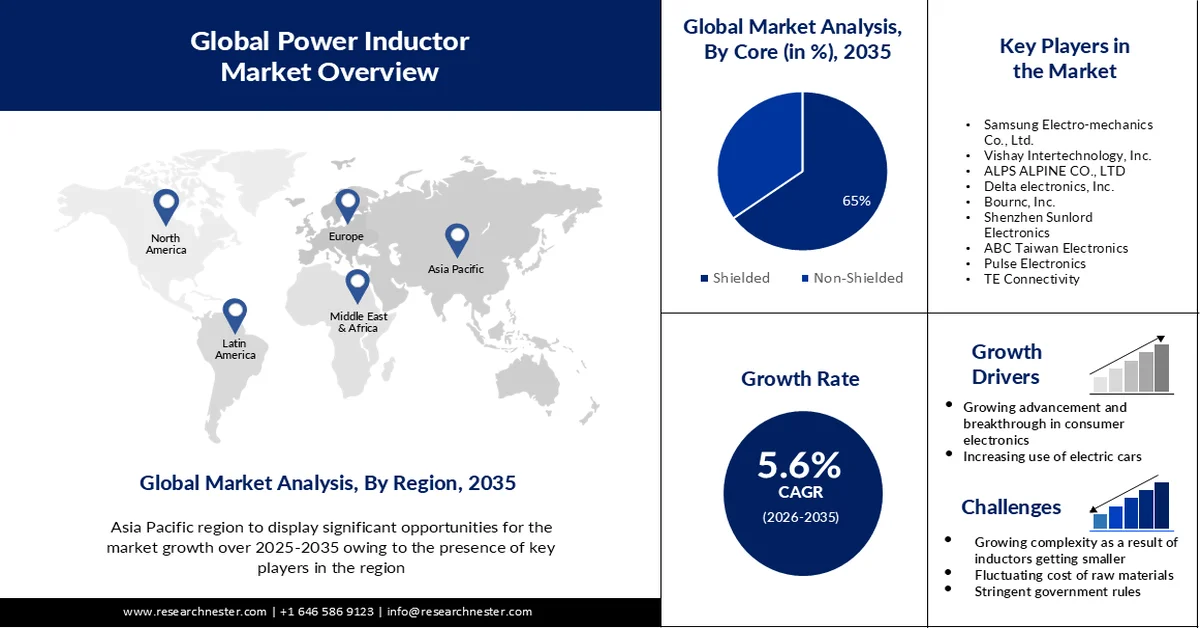

Power Inductor Market size was valued at USD 3.71 billion in 2025 and is set to exceed USD 6.4 billion by 2035, registering over 5.6% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of power inductor is estimated at USD 3.9 billion.

The growth of the market is due to the need for power inductors in power supply circuits followed by the quick rise in the use of smartphones and other devices that need to be very reliable. Research indicates that 80% of people worldwide use smartphones. Apps account for 91% of the time spent on cellphones.

In addition, the production of metal alloy power inductors, which offer excellent performance and great dependability in small medical devices, is being increased by manufacturers in the power inductor industry. Metal windings, ferrite windings, and multilayer construction are features of robust power inductors that come in a range of sizes and configurations.

Key Power Inductor Market Insights Summary:

Regional Insights:

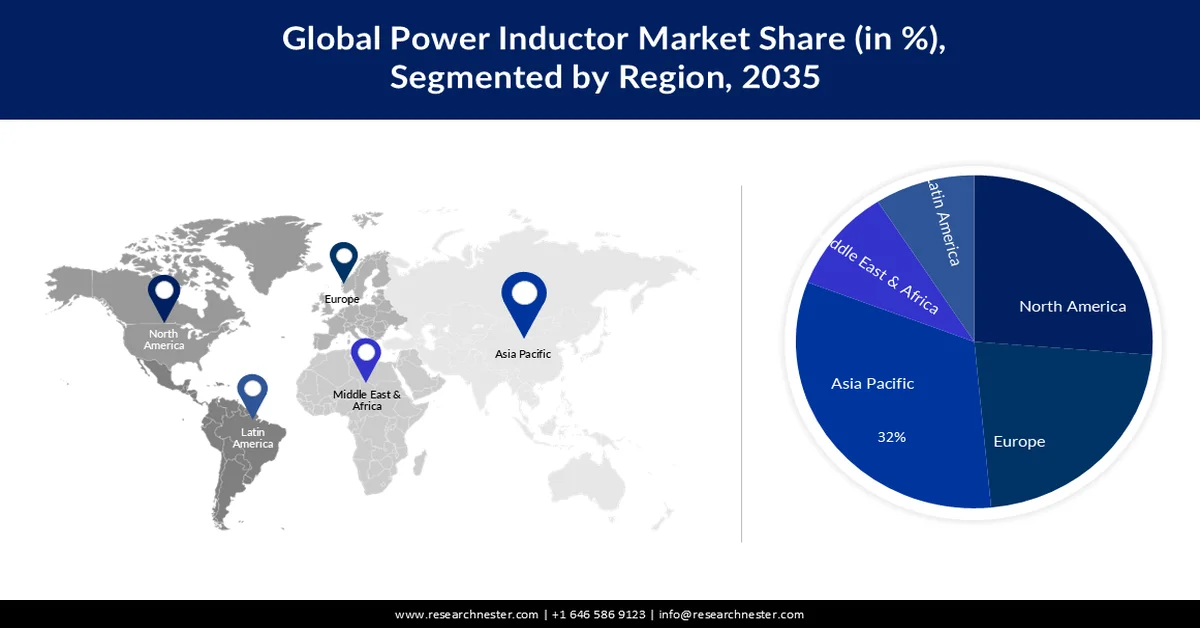

- The power inductor market in Asia Pacific is projected to command the largest share of about 32% during the forecast period, propelled by the region’s strong electronics manufacturing base and rising demand for power management solutions.

- North America is anticipated to capture nearly 26% share of the market over the forecast period, stimulated by the expanding adoption of consumer electronics and ongoing digital transformation.

Segment Insights:

- In the power inductor market, the shielded segment is expected to dominate with approximately 65% revenue share during the forecast period, driven by its superior capability to minimize power supply noise across commercial, automotive, and industrial applications.

- The air core segment is projected to represent around 40% share of the global power inductor market by 2035, attributed to its extensive utilization in electronic devices such as radios and computers.

Key Growth Trends:

- Growing Advancements and Breakthroughs in Consumer Electronics

- Increasing Use of Electric Cars

Major Challenges:

- Growing complexity as a result of inductors getting smaller

- The unstable costs of the basic materials needed to produce power inductors is hampering the growth of the power inductor market.

Key Players: Croda International Plc, KOKYU ALCOHOL KOGYO CO., LTD., Oleon NV, Nissan Chemical Corporation, Emery Oleochemicals, Jarchem Innovative Ingredients LLC, KLK EMMERICH GmbH, Santa Cruz Biotechnology, Inc., Vantage Specialty Chemicals.

Global Power Inductor Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.71 billion

- 2026 Market Size: USD 3.9 billion

- Projected Market Size: USD 6.4 billion by 2035

- Growth Forecasts: 5.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (32% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, Japan, United States, Taiwan, South Korea

- Emerging Countries: China, India, Japan, South Korea, Taiwan

Last updated on : 25 February, 2026

Power Inductor Market - Growth Drivers and Challenges

Growth Drivers

- Growing Advancements and Breakthroughs in Consumer Electronics- The consumer electronics sector is one that is dynamic and changing quickly, with market competitors competing fiercely and game-changing technological advancements happening all the time. Consumer electronics producers are benefiting from these technical advancements and improvements as they work to improve the features and caliber of their goods. Additionally, it is anticipated that they would increase the overall quantity of inductors utilized in the consumer electronics industry. Moreover, the adoption of inductors has been driven by manufacturers' growing focus on new technologies and the growing uptake of some of the major emerging technologies, such as artificial intelligence (AI) and the Internet of Things (IoT). By 2024, the IoT market is expected to reach a value of over USD 1 trillion, according to Exploding Topics. By 2030, 500 billion gadgets are anticipated to be online, according to recent research. Moreover, nearly 127 new IoT devices connect to the internet every second.

- Increasing Use of Electric Cars- The production of electric vehicles has increased significantly in recent years and is predicted to continue to grow in the years to come. The development of electric vehicles has advanced at an extremely rapid rate. Due to the growing popularity of electric vehicles, electronic components will play a bigger role in the development of linked automobiles and advanced driving assistance systems (ADAS). The demand for passive components is predicted to rise as a result of numerous large automakers and recently established automakers increasing the production volume of electric vehicles in response to tighter environmental restrictions. These electric cars are powered by IoT and AI and come with new technology installed. Inductors will likely become more in demand in the upcoming years as electric car use rises.

- Data-driven Decisions Aid Businesses in Supply Chain Optimisation- Businesses in the power inductor market are scaling up component manufacturing in different parts of the world based on the severity of the pandemic in those areas by using data-driven insights. Rich companies are working harder to automate data collecting procedures as quickly as possible. To optimise their supply chains, they are innovating and making investments in all of the various sales channels, including E-Commerce.

Challenges

- Growing complexity as a result of inductors getting smaller- Products are getting smaller and have more features, but they are also getting more sophisticated. The size of mobile devices with sophisticated complex functions is continuously decreasing. Reduced size and thickness are necessary for the power inductor for such products, which include wristband-style wearables, smartwatches, and Internet of Things devices like sensor network devices. For extended operation times, these devices also require extremely efficient power supply circuits. There is a rise in the use of multi-core and higher-speed processors for efficiency and performance due to the shrinking size and thickness of wearables like smartwatches. This opens the door for all necessary components, including inductors, to get smaller.

- The unstable costs of the basic materials needed to produce power inductors is hampering the growth of the power inductor market.

- Tight government rules that place a cap on manufacturers are impeding the expansion of the power transformer business.

Power Inductor Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.6% |

|

Base Year Market Size (2025) |

USD 3.71 billion |

|

Forecast Year Market Size (2035) |

USD 6.4 billion |

|

Regional Scope |

|

Power Inductor Market Segmentation:

Core Segment Analysis

Power inductor market from the shielded segment is anticipated to hold largest revenue share of about 65% during the forecast period. The shielded inductor’s ability to effectively reduce power supply noise in commercial, automotive, and industrial units and designs has resulted in their widespread application and rapid segment expansion. In April 2022 to March 2023, the industry produced 2,59,31,867 vehicles, including passenger cars, commercial vehicles, three-wheelers, two-wheelers, and quadricycles, compared to 2,30,40,066 units from April 2021 to March 2022 in India.

Material Segment Analysis

The air core segment is expected to account for 40% share of the global power inductor market by 2035. The growth of the market is because of its practical uses in a variety of electrical devices, including radios and computers. In 2019, it was estimated that about half of private households globally owned a computer. In contrast, the percentage of homes in industrialized nations that owned a personal computer was closer to 80 percent.

Application (Consumer Electronics, Automotive, Industrial, Healthcare)

The consumer electronics segment in the power inductor market is poised to hold 42% of the revenue share by 2035. The advent of new technologies such as wearables, 5G-enabled smartphones, and smart homes will require high voltages, which will drive additional expansion in the market for power inductors. The number of wearable devices that are connected worldwide grew significantly between 2019 and 2022. This figure increased from 929 million to around 1.1 billion in 2022.

Our in-depth analysis of the global power inductor market includes the following segments:

|

Core |

|

|

Material |

|

|

Mounting |

|

|

Type |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Power Inductor Market - Regional Analysis

APAC Market Insights

Power inductor market for Asia Pacific region is projected to hold largest share of about 32% during the projected period. Asia Pacific is essential to the growth of the electronics and electrical industries, due to some of the top Asia-Pacific-based manufacturers of inductors. Numerous electronic manufacturing firms in other regions delegate their production to Asian nations with lower labor costs. This is especially noticeable in industries where labor-intensive jobs are in greater demand, such as passive electronic component assembly and testing, and semiconductor assembly. The majority of inductors are produced in Asia Pacific and shipped to different regions due to the region's low labor costs. The need for power is rising dramatically, which makes power management more important and drives up the demand for inductors. By 2023, internet sales will account for 11.0% of the Consumer Electronics market's overall revenue in the Asia Pacific region. In 2024, Asia pacific consumer electronics industry is projected to rise by 2.0% in volume.

North American Market Insights

Power inductor market in North America region is predicted to hold second largest share of about 26% during the forecast period. There is expected to be a rise in demand for power inductors in North America is because of the increased use of consumer electronics and the digital transition. With advancements in advanced technology for effective voltage regulation, the power inductor market is anticipated to have promising growth.

Power Inductor Market Players:

- Kyocera AVX Component Corporation

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Samsung Electro-mechanics Co., Ltd.

- Vishay Intertechnology, Inc.

- ALPS ALPINE CO., LTD

- Delta electronics, Inc.

- Bournc, Inc.

- Shenzhen Sunlord Electronics

- ABC Taiwan Electronics

- Pulse Electronics

- TE Connectivity

Recent Developments

- Bourns Inc release the new Model SRP03-LAB, SRP04-LAB, SRP05-LAB and SRP06-LAB Low Profile Shielded Power Inductor Design Kits. These design kits contain inductors that provide engineers with various inductances, rated currents, and sizes for quick-turn prototype testing.

- Vishay Intertechnology, Inc. today expanded its IHLE® series of low profile, high current inductors featuring integrated E-field shields for the reduction of EMI with new commercial and Automotive Grade devices in the 5 mm by 5 mm by 3.4 mm 2020 case size. The smallest such devices on the market, the Vishay Dale IHLE-2020CD-51 and IHLE-2020CD-5A lower costs and save board space by eliminating the need for separate board-level Faraday shielding.

- Report ID: 5379

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.