Polymer Electrolyte Membrane (PEM) Fuel Cells Market Outlook:

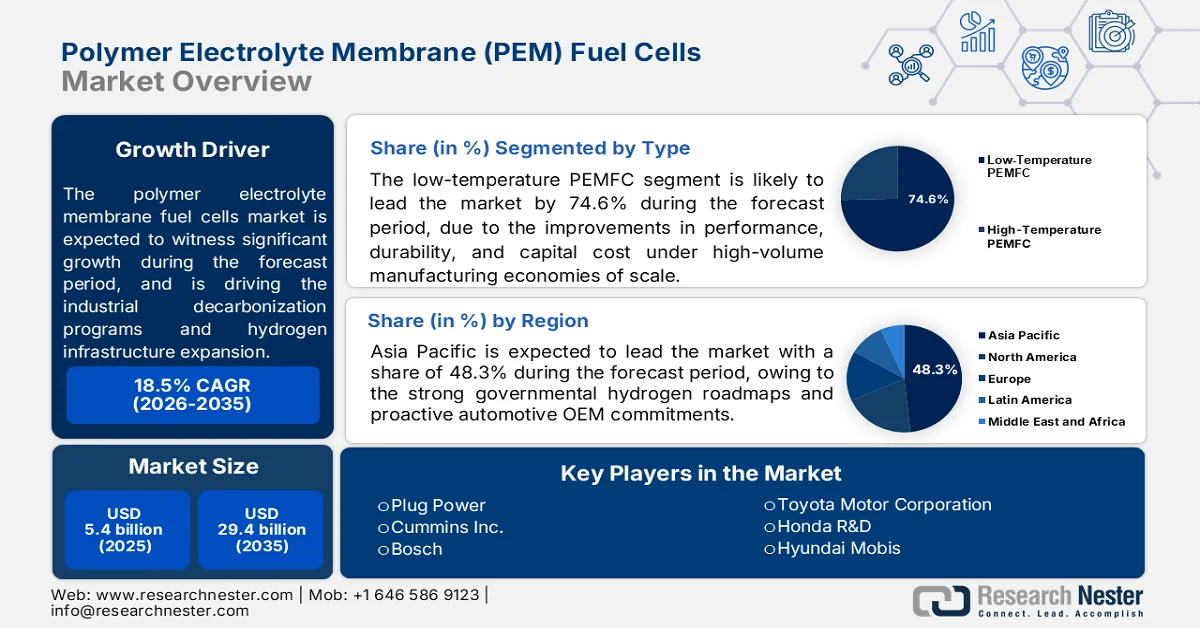

Polymer Electrolyte Membrane (PEM) Fuel Cells Market size was valued at USD 5.4 billion in 2025 and is projected to cross USD 29.4 billion by the end of 2035, rising at a CAGR of 18.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of polymer electrolyte membrane (PEM) fuel cells is assessed at USD 6.4 billion.

The polymer electrolyte membrane (PEM) fuel cells market is benefiting from sustained public-sector investment, industrial decarbonization programs, and hydrogen infrastructure expansion across major economies. According to the RMI January 2024 data, in the U.S., the Department of Energy (DOE) has positioned clean hydrogen as a strategic component of industrial and transportation decarbonization, supported by multi-billion-dollar federal initiatives. Through the Regional Clean Hydrogen Hubs program, the DOE has committed up to USD 7 billion to accelerate hydrogen production, transport, storage, and end-use deployment across multiple states. These investments are creating demand for fuel cell systems in heavy-duty transportation, logistics equipment, backup power, and distributed energy applications.

The International Energy Agency (IEA) 2025 data reported that the global fuel cell electric vehicle fleet exceeded 90,000 units, reflecting gradual but measurable infrastructure growth. Government-backed procurement programs for buses, trucks, rail systems, and municipal fleets are also supporting commercial adoption. In parallel, public research institutions continue to fund improvements in fuel cell durability, stack performance, and manufacturing efficiency, helping reduce lifecycle costs and strengthen the supply chain for membrane materials, catalysts, and balance-of-plant components. As governments continue funding hydrogen production, storage, and distribution projects, procurement opportunities are expected to expand for membrane manufacturers, stack integrators, catalyst suppliers, and system developers serving transportation, industrial, and grid-support applications.

Key Polymer Electrolyte Membrane (PEM) Fuel Cells Market Insights Summary:

Regional Highlights:

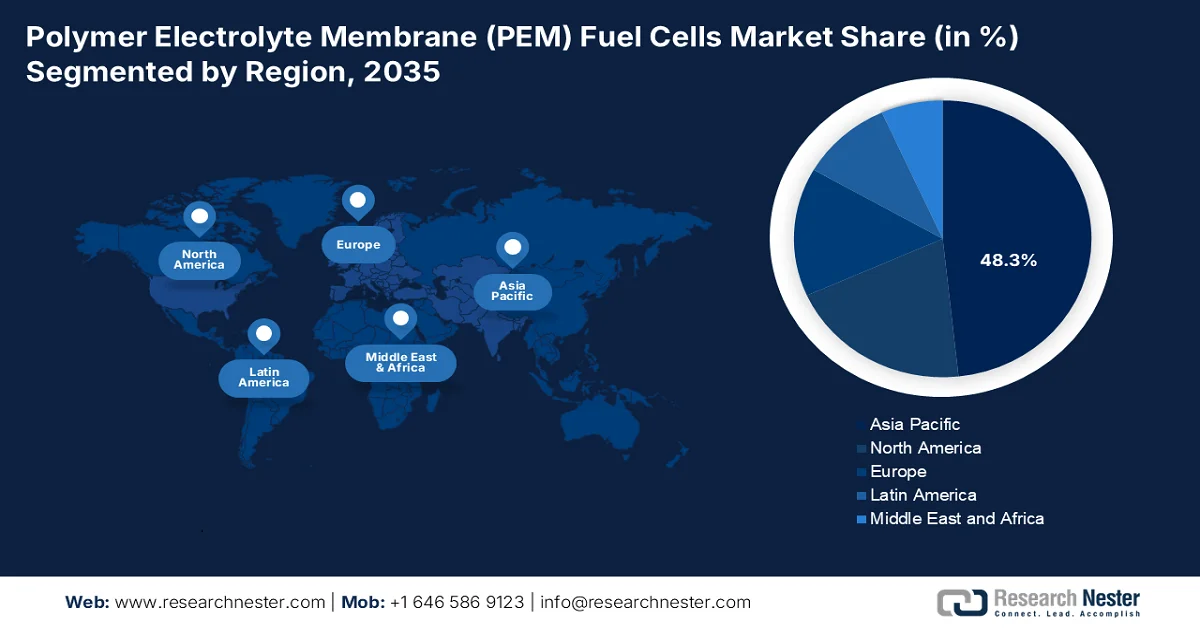

- Asia Pacific is anticipated to command 48.3% of the polymer electrolyte membrane (PEM) fuel cells market by 2035, underpinned by strong governmental hydrogen roadmaps

- North America is projected to witness the fastest expansion in the market throughout 2026-2035, fostered by a strong collaborative ecosystem between government agencies, automotive OEMs, and industrial conglomerates driving innovation across transportation, stationary power, and backup generation applications

Segment Insights:

- The low-temperature PEMFC segment is expected to capture 74.6% of the polymer electrolyte membrane (PEM) fuel cells market by 2035, propelled by the U.S. DOE's aggressive cost-reduction targets for green hydrogen production requiring simultaneous improvements in performance, durability, and capital cost under high-volume manufacturing economies of scale

- Liquid cooling remains the leading cooling method in the market during 2026-2035, reinforced by its ability to maintain stack temperatures within the critical 60–120 °C operating range to balance performance and durability

Key Growth Trends:

- Public investment in heavy-duty transportation

- Rising industrial decarbonization spending

Major Challenges:

- High platinum group metal catalyst costs

- Membrane durability and chemical degradation

Key Players: Plug Power (U.S.), Cummins Inc. (U.S.), Bosch (Germany), Toyota Motor Corporation (Japan), Honda R&D (Japan), Hyundai Mobis (South Korea), COMSOL (U.S.).

Global Polymer Electrolyte Membrane (PEM) Fuel Cells Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.4 billion

- 2026 Market Size: USD 6.4 billion

- Projected Market Size: USD 29.4 billion by 2035

- Growth Forecasts: 18.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (48.3% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, Japan, United States, South Korea, Germany

- Emerging Countries: India, Malaysia, Canada, Australia, Saudi Arabia

Last updated on : 1 July, 2026

Polymer Electrolyte Membrane (PEM) Fuel Cells Market - Growth Drivers and Challenges

Growth Drivers

- Public investment in heavy-duty transportation: Heavy-duty transportation is becoming a major demand center for PEM fuel cells due to government-backed decarbonization programs. Public authorities are directing funding toward fuel-cell buses, trucks, and commercial fleets where battery-only solutions face range and refueling constraints. The U.S. DOT 2026 data allocated approximately USD 1.5 billion metropolitan planning organizations, and local governments in constructing transportation projects. These initiatives create recurring demand for PEM fuel cell stacks and associated hydrogen infrastructure. Long-distance logistics and public transit remain among the most commercially attractive applications, encouraging manufacturers to scale production and invest in localized supply chains.

- Rising industrial decarbonization spending: Industrial decarbonization policies are increasing demand for hydrogen technologies that support emissions reductions in manufacturing, chemicals, refining, and energy-intensive sectors. Governments are allocating significant resources to help industries transition away from fossil fuels. Hydrogen-based systems and fuel cells are increasingly considered for distributed power generation and backup energy applications within industrial facilities. The International Energy Agency (IEA) 2024 data reported global hydrogen demand reached approximately 97 million tons, reflecting growing industrial interest in hydrogen-related investments. This trend supports long-term procurement of PEM fuel cell components and system integration services.

Challenges

- High platinum group metal catalyst costs: Platinum and iridium remain essential for PEMFC catalysts. Manufacturers struggle with price volatility and supply chain concentration in South Africa and Russia. Companies like Toyota are developing PGM-free catalysts, while Ballard Power focuses on reducing platinum loading through advanced alloy formulations to achieve cost parity with internal combustion engines.

- Membrane durability and chemical degradation: Perfluorosulfonic acid membranes degrade under radical attack during start-stop cycling and low-humidity operation. Membrane thinning and pinhole formation reduce stack lifetime below commercial requirements. Manufacturers invest in reinforced composite membranes and cerium-based radical scavengers. Gore and Chemours lead in developing mechanically strengthened membranes that extend operational life.

Polymer Electrolyte Membrane (PEM) Fuel Cells Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

18.5% |

|

Base Year Market Size (2025) |

USD 5.4 billion |

|

Forecast Year Market Size (2035) |

USD 29.4 billion |

|

Regional Scope |

|

Polymer Electrolyte Membrane (PEM) Fuel Cells Market Segmentation:

Type Segment Analysis

Under the type segment, the low-temperature PEMFC is dominating and is poised to hold the share value of 74.6% by the end of 2035. The segment is driven by the U.S. DOE's aggressive cost-reduction targets for green hydrogen production, requiring simultaneous improvements in performance, durability, and capital cost under high-volume manufacturing economies of scale. As outlined in DOE's 2026 data, all metrics must be achieved on the same stack or system to meet levelized cost targets, with 2026 and ultimate goals assuming high-volume manufacturing economies of scale. Current status, based on H2NEW Consortium analysis, includes an end-of-life performance loss of 10% and a degradation rate evaluated at nominal operating points. Notably, reducing iridium-based platinum group metal loading at the anode is prioritized to lower costs without compromising durability, while system cost values exclude installation expenses such as permitting and construction.

Cooling Method Segment Analysis

Liquid cooling is the dominant cooling method in the polymer electrolyte membrane (PEM) fuel cells market, as it effectively maintains stack temperatures within the critical 60–120 °C band to balance performance and durability, as per the NLM July 2025 study. Operating below this range slows electrochemical reactions, while exceeding it risks membrane dehydration and thermal degradation, compromising lifespan. Although liquid cooling proves significantly more effective than air cooling, which suffers from ambient dependency, temperature uniformity across the Membrane Electrode Assembly remains a persistent challenge. Consequently, researchers are actively developing next-generation working fluids to enhance heat transfer and spatial uniformity, particularly for automotive applications where transient load cycles demand rapid, precise thermal response without localized hot spots.

Application Segment Analysis

The automotive application remains the most prominent driver of the polymer electrolyte membrane (PEM) fuel cells market, as original equipment manufacturers increasingly adopt PEMFC technology for passenger cars, commercial trucks, and transit buses. Automotive integration demands compact, lightweight stacks with rapid cold-start capability and exceptional durability under variable load cycles. Strategic collaborations between automakers and hydrogen infrastructure providers are accelerating fleet deployments across logistics corridors and urban transport networks. Thermal and water management remain critical engineering challenges, as fluctuating power demands during acceleration and regenerative braking exert stress on the membrane electrode assembly. Nevertheless, continuous innovations in bipolar plate design, catalyst durability, and system simplification are progressively enhancing the commercial viability of PEMFC-powered vehicles for mainstream adoption.

Our in-depth analysis of the polymer electrolyte membrane (PEM) fuel cells market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Cooling Method |

|

|

Power Output |

|

|

Application |

|

|

End user |

|

|

Component |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Polymer Electrolyte Membrane (PEM) Fuel Cells Market - Regional Analysis

APAC Market Insights

Asia Pacific is dominating the polymer electrolyte membrane (PEM) fuel cells market and is expected to hold the regional revenue share of 48.3% by the end of 2035. The region is driven by the strong governmental hydrogen roadmaps and proactive automotive OEM commitments across Japan, South Korea, China, and emerging economies like India and Malaysia. China focuses on commercial vehicle fleet deployment through state-backed pilot cities, while Japan advances residential co-generation systems alongside automotive applications. South Korea leverages its robust electronics and shipbuilding industries to integrate PEMFCs into maritime and stationary power solutions. Thermal management, water balance, and membrane durability remain central R&D focal points, addressing diverse climatic and operational conditions.

The government-led hydrogen initiatives and increasing investment in clean energy infrastructure is driving the polymer electrolyte membrane (PEM) fuel cells market in India. In March 2026, the Government of India approved the National Green Hydrogen Mission with an outlay of INR 19,744 crore to accelerate domestic hydrogen production, electrolyzer manufacturing, and end-use applications, including fuel cells. Furthermore, the PIB March 2026 data depicts that the Ministry of New and Renewable Energy (MNRE) targets 5 million metric tonnes of annual green hydrogen production capacity, creating a substantial foundation for fuel-cell adoption in transportation and industrial sectors. These policy measures are encouraging public and private investment across the hydrogen value chain, supporting future demand for PEMFC systems, components, and associated infrastructure throughout the country.

The strong government support for hydrogen mobility and fuel-cell commercialization is shaping the polymer electrolyte membrane (PEM) fuel cells market in China. According to IEA September 2025 data, hydrogen development plan, the country targets production of 100,000–200,000 tonnes of renewable hydrogen annually by 2025 and aims to establish a nationwide hydrogen supply framework. In addition, China’s Ministry of Finance and related ministries continued implementation of the fuel cell vehicle demonstration city cluster program, under which participating regions are working toward deployment of approximately 50,000 fuel cell vehicles by 2025. These initiatives are stimulating investments in hydrogen refueling infrastructure, fuel-cell manufacturing, and supply-chain localization, supporting growing demand for PEMFC systems across transportation, logistics, and distributed power applications.

North America Market Insights

North America is projected to emerge rapidly during the assessed period, 2026 to 2035 in the polymer electrolyte membrane (PEM) fuel cells market. The region is driven by the strong collaborative ecosystem between government agencies, automotive OEMs, and industrial conglomerates, driving innovation across transportation, stationary power, and backup generation applications. Strategic partnerships between PEMFC stack manufacturers and logistics providers are accelerating real-world demonstrations, while cross-border hydrogen corridor initiatives aim to standardize refueling infrastructure. Thermal and water management remain engineering priorities, with ongoing advancements in membrane durability and system integration steadily improving commercial viability.

The increased federal support for hydrogen deployment, domestic manufacturing, and clean transportation initiatives is shaping the polymer electrolyte membrane (PEM) fuel cells market in the U.S. According to the DOE January 2025 data, the U.S. Department of the Treasury and Internal Revenue Service implemented the Clean Hydrogen Production Tax Credit, providing incentives of up to USD 3 per kilogram of clean hydrogen produced, improving the economics of hydrogen supply for fuel-cell applications. Additionally, the U.S. IEA September 2024 data reported that its Hydrogen Shot initiative targets an 80% reduction in clean hydrogen costs, supporting broader commercial adoption of PEMFC technologies across transportation and stationary power sectors. These policy measures are strengthening investment confidence and accelerating deployment opportunities throughout the hydrogen value chain.

The federal and provincial governments prioritize hydrogen commercialization, clean mobility, and industrial decarbonization is shaping the polymer electrolyte membrane (PEM) fuel cells market in Canada. Natural Resources Canada announced million through the Clean Hydrogen Investment Tax Credit to support eligible hydrogen production projects and strengthen the domestic hydrogen value chain. Additionally, according to the Government of Canada’s January 2026 data Hydrogen Strategy progress updates, the country aims to supply up to 30% of its end-use energy from hydrogen by 2050, creating long-term demand for fuel cell technologies across transportation, power generation, and industrial applications. These initiatives are encouraging investments in hydrogen infrastructure, fuel cell manufacturing, and research activities, positioning Canada as a key North American market for PEMFC deployment and commercialization.

Europe Market Insights

The polymer electrolyte membrane (PEM) fuel cells market in Europe is shaped by stringent carbon neutrality mandates and a well-coordinated public-private partnership framework, with Germany, France, the UK, and the Nordic countries leading deployment across heavy-duty transport, marine, and stationary power applications. Europe's distinct emphasis on cross-border hydrogen backbone infrastructure and standardized refueling corridors facilitates fleet operators' transition to PEMFC-powered trucks and buses, while aggressive research programs target high-temperature membrane development and durability improvements for extreme duty cycles. Key players collaborate with rail and maritime OEMs to repower existing assets, leveraging PEMFC's modularity and fast refueling. Water management, freeze-start capability, and system simplification remain prominent engineering priorities, supported by robust supply chains for bipolar plates and membrane electrode assemblies.

The substantial public investment in hydrogen infrastructure and industrial decarbonization is driving the polymer electrolyte membrane (PEM) fuel cells market in Germany. According to the Hydrogen Europe January 2025 report, approved funding for the national hydrogen core network, which is expected to comprise approximately 9,040 kilometers of hydrogen pipelines by 2032, creates a foundation for large-scale hydrogen distribution and fuel-cell deployment. Additionally, under Germany’s updated National Hydrogen Strategy, the government raised its domestic electrolysis capacity target, strengthening long-term hydrogen availability for transportation and stationary fuel-cell applications. These measures are encouraging investment in fuel-cell technologies, hydrogen mobility projects, and localized supply chains, reinforcing Germany’s position as one of Europe’s leading PEMFC markets.

The polymer electrolyte membrane (PEM) fuel cells market in the UK is gaining traction as the government expands support for hydrogen production and low-carbon energy systems. The UK Parliament May 2026 data published its Hydrogen Production Delivery Roadmap, reaffirming a target of up to 10 GW of low-carbon hydrogen production capacity by 2030, with at least half expected to come from green hydrogen sources. Additionally, the Government of UK December 2023 data depicted that Department for Energy Security and Net Zero announced the first Hydrogen Allocation Round in 2023, supporting 11 hydrogen production projects with a combined capacity of 125 MW. These initiatives are strengthening the domestic hydrogen ecosystem, encouraging investment in fuel-cell-powered transportation, distributed power generation, and industrial applications, thereby supporting future demand for PEMFC technologies across the UK market.

Key Polymer Electrolyte Membrane (PEM) Fuel Cells Market Players:

- Plug Power (U.S.)

- Cummins Inc. (U.S.)

- Bosch (Germany)

- Toyota Motor Corporation (Japan)

- Honda R&D (Japan)

- Hyundai Mobis (South Korea)

- COMSOL (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Plug Power has solidified its leadership in the polymer electrolyte membrane (PEM) fuel cells market by aggressively scaling from material-handling forklifts into stationary power and over-the-road heavy-duty trucks.

- Cummins Inc. has transformed its legacy diesel engine expertise into a formidable force in the polymer electrolyte membrane (PEM) fuel cells market through its New Power division and the strategic acquisition of Hydrogenics.

- Bosch has emerged as a powerhouse in the polymer electrolyte membrane (PEM) fuel cells market by applying its automotive-grade manufacturing precision to mass-produce PEMFC stacks at gigawatt-scale facilities in Germany and China.

- Toyota Motor Corporation remains a trailblazer in the market through its second-generation Mirai sedan and modular "fuel cell modules" designed for buses, ships, and stationary generators.

- Honda R&D has carved a distinct niche in the polymer electrolyte membrane (PEM) fuel cells market by focusing on co-generation systems that combine PEM power with residential heat recovery, alongside its fuel-cell Clarity vehicle platform.

Here is a list of key players operating in the global polymer electrolyte membrane (PEM) fuel cells market:

The competitive landscape of the polymer electrolyte membrane (PEM) fuel cells market is intensely fragmented, yet increasingly consolidated around automotive and stationary power leaders. Strategic initiatives center on vertical integration, gigafactory-scale manufacturing to slash costs, and joint ventures with heavy-duty truck and marine OEMs. Key players are also pivoting to high-temperature PEM membranes for durability and leveraging government hydrogen subsidies. Simultaneously, partnerships for green hydrogen production and distribution are critical, as are acquisitions of specialized stack component startups to secure supply chains and intellectual property against Asian and European rivals.

Corporate Landscape of the Market:

Recent Developments

- In January 2026, Tosoh Corporation announced the development of a hydrocarbon‑based polymer electrolyte for polymer electrolyte membrane (PEM) water electrolysis systems. Growing interest in hydrogen energy for carbon neutrality is increasing attention on PEM water electrolysis, a leading hydrogen production technology.

- In November 2024, COMSOL has introduced COMSOL Multiphysics® version 6.3, which is a new interface to model transport in any electrolyte solution, improved features and variables for two-phase flow, and new capabilities for parameter estimation. Read more about these updates below.

- In January 2024, Hyundai Motor Company, Kia Corporation (Kia) and W. L. Gore & Associates (Gore) has announced that they have signed an agreement at the Mabuk Eco-Friendly R&D Center, Korea, to collaborate on the development of advanced polymer electrolyte membrane (PEM) for hydrogen fuel cell systems.

- Report ID: 8650

- Published Date: Jul 01, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Polymer Electrolyte Membrane (PEM) Fuel Cells Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.