Plant-based Food Market Outlook:

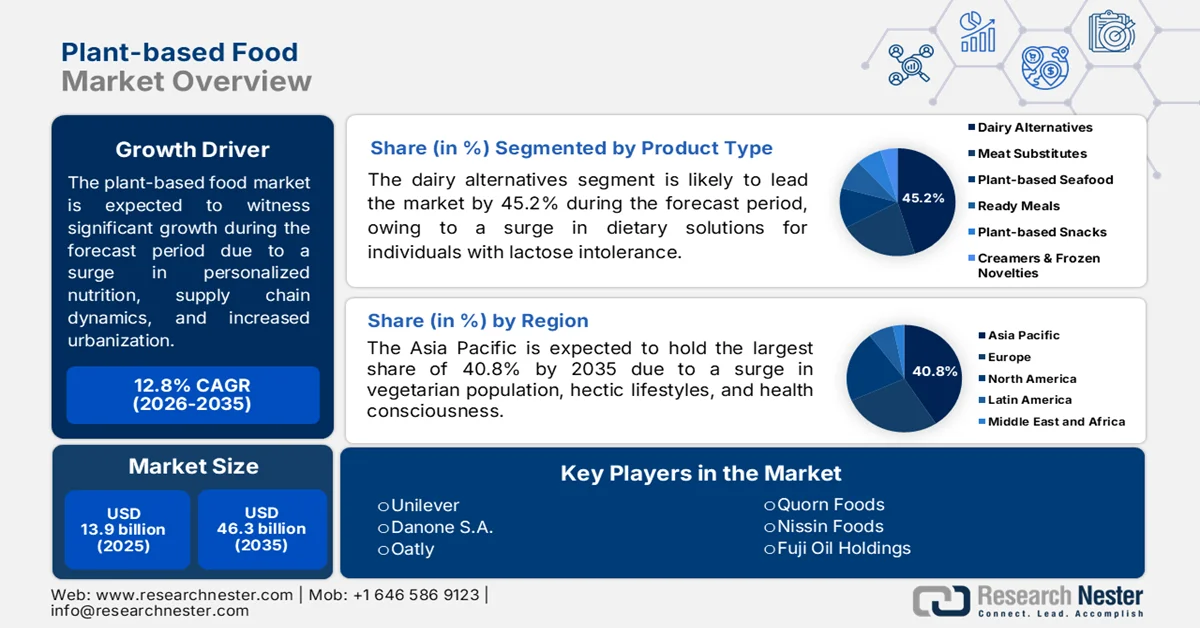

Plant-based Food Market size was valued at USD 13.9 billion in 2025 and is poised to reach USD 46.3 billion by the end of 2035, expanding at around 12.8% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of plant-based food is estimated at USD 15.6 billion.

The worldwide plant-based food market is continuously increasing, owing to climate volatility, rapid urbanization, workforce dynamics, the rise of personalized nutrition, trade dynamics for soy protein, and suitable export restrictions on notable agricultural commodities. According to official statistics published by NLM in September 2025, over 650 million adults are overweight, and almost 20% of the global population is projected to be affected by the end of 2030. Likewise, 537 million adults suffered from diabetes, and this is also expected to surge to 783 million by the end of 2045. Therefore, to address these issues, personalized nutrition is crucial, and dietary recommendations have always been wide-ranging. In this regard, soy protein intake is highly nutritious, and its continuous export and import across the world are positively impacting market growth.

2024 Soybeans Global Export and Import Analysis

|

Countries/Components |

Export (USD) |

Import (USD) |

|

Brazil |

44.5 billion |

- |

|

U.S. |

24.3 billion |

- |

|

Paraguay |

3.2 billion |

- |

|

China |

- |

47.6 billion |

|

Argentina |

- |

3.1 billion |

|

Mexico |

- |

3.0 billion |

|

Global Trade Valuation |

81.5 billion |

|

|

Global Trade Share |

0.3% |

|

Source: OEC

Furthermore, the presence of hybrid products, such as plant proteins and blended animal products, increased focus on upcycled ingredient utilization, and the existence of ambient plant-based products are a few trends that are responsible for fueling the plant-based food market globally. As stated in an article published by the Frontiers Organization in January 2022, plant-based sources readily dominate the supply of 57% of proteins, with the remaining 43% comprising 10% of dairy products, 6% of fish and shellfish, 18% of meat, and 9% of other products from animals. Besides, the pricing strategy of plant-based products, particularly in the U.S., amounts to an estimated 940 million, which is predicted to increase by 38% in the upcoming years. Therefore, with the increased presence of plant-based alternatives, with the food industry focused on maintaining the quality, there is a huge growth opportunity for the plant-based food market.

Key Plant-based Food Market Insights Summary:

Regional Highlights:

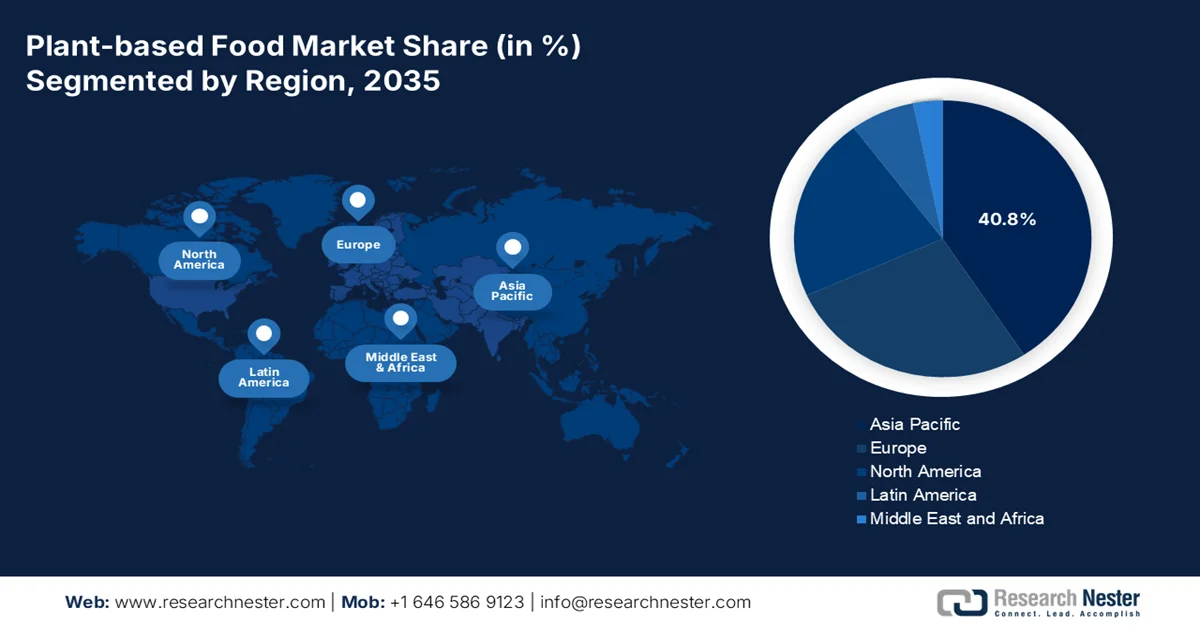

- Asia Pacific is projected to capture 40.8% share by 2035, stimulated by rising disposable incomes, expanding vegetarian demographics, rapid urbanization, and increasing demand for ready-to-eat plant-based options

- North America is anticipated to register the fastest expansion in the plant-based food market throughout 2026-2035, catalyzed by advancements in texture and taste enhancement, sustainability-focused consumer preferences, and increasing fast-food collaborations

Segment Insights:

- The dairy alternatives segment is anticipated to account for 45.2% share by 2035, buoyed by increasing demand from vegan consumers and individuals with lactose intolerance and milk allergies

- The extrusion sub-segment is expected to secure the second-largest share in the plant-based food market during 2026-2035, accelerated by its commercial scalability, continuous production efficiency, and capability to create meat-like textures using widely available plant proteins

Key Growth Trends:

- Institutional procurement commitments

- Precision in fermentation commercialization

Major Challenges:

- Supply chain fragility for alternative proteins

- Regulatory and labeling hurdles

Key Players: Beyond Meat, Impossible Foods, Kellogg's MorningStar Farms, Conagra Brands Gardein, Tofurky, Nestlé, Unilever, Danone S.A., Oatly, Rügenwalder Mühle, Quorn Foods, Nissin Foods, Fuji Oil Holdings Daiz, v2food, Fable Food Co., UNLIMEAT, GoodDot, Blue Tribe Foods, Phuture Foods, The Vegetarian Butcher, Cargill, Voyage Foods.

Global Plant-based Food Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 13.9 billion

- 2026 Market Size: USD 15.6 billion

- Projected Market Size: USD 46.3 billion by 2035

- Growth Forecasts: 12.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (40.8% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: India, South Korea, Brazil, Canada, Australia

Last updated on : 20 May, 2026

Plant-based Food Market - Growth Drivers and Challenges

Growth Drivers

- Institutional procurement commitments: The presence of massive private and public institutions, such as corporate cafeteria operators, university dining systems, school districts, and hospital networks, is continuously incorporating plant-based procurement. According to official statistics published by NLM in October 2022, the plant-based food industry was worth USD 30 billion, which is further projected to increase to USD 160 billion by the end of 2030. Based on this growth, the commitment towards healthy consumer choice is frequently embedded in a wide-ranging sustainability or carbon reduction pledges. This eventually creates high-volume and predictable demand for stabilizing the overall plant-based food market, which is also proliferating its growth and expansion worldwide.

- Precision in fermentation commercialization: The suitable commercialization of precise fermentation by utilizing micro-organisms for producing specific proteins, including egg white, collagen, whey, and casein, is readily altering the plant-based food market supply chain. As stated in an article published by NLM in November 2023, fermented straight carrot juice is found to constitute a 27% reduction in sugar. Besides, emerging fermentation technologies have increasingly revolutionized, demonstrating an upsurge in sulforaphane yields by 16 times, especially when broccoli florets are pre-heated at 65 degrees Celsius for 3 minutes, which is effectively followed by lactic acid bacteria and maceration fermentation in a laboratory scale, thereby making it suitable for positively driving the market demand.

Challenges

- Supply chain fragility for alternative proteins: The plant-based food market depends on a handful of specialty protein isolates and concentrates, including pea, soy, fava, mung bean, and increasingly fermented mycoprotein or precision-fermented casein. These ingredients require dedicated fractionation and drying facilities, which are in short supply globally. Besides, any disruption, such as crop failure due to weather, logistical bottlenecks, or sudden demand spikes, can cause severe raw material shortages. Unlike conventional meat or dairy, which benefit from decades of diversified, resilient supply chains, the plant-based sector operates on a thinner, more centralized network. Moreover, smaller manufacturers face minimum order quantities that they cannot afford, leading to inconsistent production.

- Regulatory and labeling hurdles: Legislative battles over terms, such as milk, burger, sausage, and yogurt, continue to fragment the plant-based food market. In Europe, amendments restrict plant-based products from using dairy-related terms, even with qualifiers, including oat drink instead of oat milk. Likewise, in the U.S., several states have passed laws prohibiting plant-based meat from being labeled as meat or a burger. These restrictions confuse consumers, force costly repackaging, and limit marketing effectiveness. Simultaneously, regulations around novel ingredients, particularly precision-fermented dairy proteins or cultivated fat added to plant-based products, vary dramatically by country, slowing cross-border expansion.

Plant-based Food Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

12.8% |

|

Base Year Market Size (2025) |

USD 13.9 billion |

|

Forecast Year Market Size (2035) |

USD 46.3 billion |

|

Regional Scope |

|

Plant-based Food Market Segmentation:

Product Type Segment Analysis

Based on the product type, the dairy alternatives segment is anticipated to garner the largest share of 45.2% in the plant-based food market by the end of 2035. The segment’s upliftment is primarily driven by the provision of crucial solutions for individuals with vegan diets, milk allergies, and lactose intolerance. According to official statistics published by NLM in March 2026, the worldwide plant-based dairy substitutes industry is projected to grow at an average annual growth rate of 9% by the end of 2032. Besides, a decrease in lactose digestion has been witnessed among 65% of the population, based on a study conducted by the U.S. National Library of Medicine. Additionally, lactose intolerance impacts 70% to 100% of people in East Asia, due to which there is a huge demand for plant-based alternatives for dairy consumers, which is rapidly proliferating the segment’s growth.

Technology Segment Analysis

The extrusion sub-segment, part of the technology segment, is projected to grab the second-largest share in the plant-based food market by the end of the forecast period. The sub-segment’s growth is effectively attributed to the most commercially mature and widely deployed technology in the plant-based food market. The process works by subjecting plant protein concentrates or flours to high heat, pressure, and mechanical shear inside a barrel, then forcing the molten mass through a die to create fibrous, meat-like structures. Two primary forms dominate: low-moisture extrusion produces shelf-stable crumbles or chunks that rehydrate for use in nuggets, patties, and sausages; high-moisture extrusion generates a cooler, hydrated fibrous product that mimics whole-muscle textures such as chicken breast or beef steak. The technology's advantages include scalability, continuous production, and the ability to use widely available proteins, such as pea, soy, gluten, and fava bean.

End user Segment Analysis

By the end of the stipulated timeline, the flexitarians sub-segment, which is part of the end user segment, is expected to account for the third-largest share in the plant-based food market. The sub-segment’s development is highly propelled by its consumption pattern for effectively prioritizing plant-based foods that permit animal and meat products in moderation. Unlike vegans or vegetarians, flexitarians do not adhere to strict dietary exclusions. Instead, they reduce animal product consumption for reasons spanning health improvement, environmental concern, animal welfare awareness, or simple culinary variety. This behavioral flexibility makes them the largest addressable target for mainstream plant-based brands. Moreover, flexitarians evaluate plant-based products against the taste, texture, price, and convenience of conventional meat.

Our in-depth analysis of the plant-based food market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Technology |

|

|

End user |

|

|

Distribution Channel |

|

|

Source Type |

|

|

Form |

|

|

Application |

|

|

Packaging Type |

|

|

Claim/Positioning |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Plant-based Food Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the plant-based food market is anticipated to account for the largest share of 40.8% by the end of 2035. The market’s upliftment in the region is primarily attributed to a rise in disposable incomes, a massive vegetarian population, an increase in health consciousness, hectic lifestyles, rapid urbanization, and the availability of ready-to-eat plant-based options. According to official statistics published by the Nutrition Research and Practice in April 2026, the Korea-specific Vegetarian Union estimated that roughly 1.5 million to 2 million people, which is approximately 3% to 4% of the population, are vegetarians as of 2022. In addition, among the population aged more than 60 years, an estimated 1 in 3 individuals recognized themselves as vegetarians or aspiring to adopt vegetarianism, thus bolstering the market demand in the overall region.

The plant-based food market in China is growing significantly, owing to a rise in the middle class, an upsurge in disposable income, an expansion in purchasing power for premium plant-based products, the existence of the conventional domestic dietary wisdom, the demand for immunity-boosting and preventive nutrition, and suitable governmental support for organic farming. As stated in a data report published by the Organic Eprints Organization in 2026, the country is the global leader in organic agriculture and is currently positioned in fourth place with certified organic hectares of 3,589,807. Simultaneously, the country is recognized as the third-largest economy for organic food with USD 17.9 million yearly retail sales. Likewise, the country is also the world’s most prominent leader in organic cereal hectares at 2,009,240 hectares, thereby denoting an optimistic outlook for the plant-based food market growth.

The aspects of increased consciousness about protein food, an increase in the demand for functional food, the focus on diminishing chronic diseases by gradually shifting to plant-based food options, the trading ecosystem, and suitable government policies are certain factors that are driving the plant-based food market in Japan. The industrial growth in the country was initially valued at USD 6.2 billion as of 2025, which is later projected to be worth USD 7 billion by 2026, and further by USD 20.4 billion by the end of 2035, along with a 12.5% growth rate. Besides, as per an article published by NLM in April 2025, the strategy of school lunch programs is increasingly implemented across nearly 99% of elementary schools, and more than 91% of junior high schools. In addition, these schools are readily served an estimated 190 times every year. Moreover, the consumption expenditure in terms of the gross domestic product (GDP) is also driving the market in the country.

Consumption Expenditure in Japan, 2014-2024

|

Year |

Consumption (GDP %) |

|

2014 |

77.6 |

|

2015 |

75.4 |

|

2016 |

74.4 |

|

2017 |

74.0 |

|

2018 |

74.3 |

|

2019 |

74.5 |

|

2020 |

75.0 |

|

2021 |

74.7 |

|

2022 |

76.9 |

|

2023 |

75.3 |

|

2024 |

74.7 |

Source: World Bank Organization

North America Market Insights

North America in the plant-based food market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by texture and taste improvement, an expansion in fast-food partnerships, the growing emphasis on sustainability and health claims, the tactical transition to operational efficiency, and optimized nutritional profiles. According to official statistics published by the Health Affairs Organization in March 2025, poor nutrition in the U.S. leads to over 600,000 deaths and a roughly USD 1.1 trillion in healthcare expenditure and yearly lost productivity, along with profound health disparities. Meanwhile, more than 2/3rd of the population prefers that Medicaid and Medicare services should be generously assisted in paying for health programs, thus denoting a huge growth opportunity for the market in the region.

The plant-based food market in the U.S. is gaining increased traction, owing to state-level policy and procurement mandates, and litigation-based clean label reformulation. As stated in an article published by NLM in February 2026, 53% of consumers in the country are readily concerned about ultra-processed foods, with concern increasing among 71% of health-conscious consumers, while 14% of overall consumers consume a few snack bars due to this reason. Based on this, the domestic snack bar industry was worth between USD 11 billion and USD 13.2 billion as of 2024, significantly accounting for 39% to 43% of the overall global industry. Besides, nutrition and energy bars readily dominate the nation’s space, catering to 66.2% of overall snack bar revenue in the same year. Besides, the aspect of protein bar formulations also denotes an optimistic outlook for the market in the country.

Protein Bar Formulations for Single Batch, 2026

|

Ingredient |

Manufacturer |

21% Protein Bar g (% w/w) |

24% Protein Bar g (% w/w) |

27% Protein Bar g (% w/w) |

30% Protein Bar g (% w/w) |

|

Dried Beef |

Publix Super Market, Inc. |

632.4 (30.6) |

690.4 (33.5) |

742.9 (36.0) |

790.9 (38.3) |

|

Grass-Fed Beef Tallow |

The Fat Lady Tallow |

1,058.2 (51.3) |

971.2 (47.1) |

892.5 (43.3) |

820.4 (39.8) |

|

Dried Mango |

Anna and Sarah, Somerset |

316.2 (15.3) |

345.2 (16.7) |

371.4 (18.0) |

395.4 (19.1) |

|

Black Pepper |

Badia Spices, LLC. |

13.4 (0.6) |

|||

|

White Pepper |

Felicific, Inc. |

13.4 (0.6) |

|||

|

Garlic Powder |

Badia Spices, LLC. |

13.4 (0.6) |

|||

|

Habanero Powder |

Sonoran Spice |

13.4 (0.6 |

|||

Source: NLM

The presence of federal protein industries focusing on the supercluster initiative, along with the domestic plant-based food approach under the food policy are responsible for fueling the plant-based food market in Canada. As per an article published by the Government of Canada in October 2024, there was the provision of USD 62.6 million as a generous investment for more than 5 years to ensure domestic families have the accessibility to cost-effective and healthy food, such as localized food, which commenced with USD 10.4 billion. Additionally, this particular investment also assisted in supporting different program modifications, and also launching a Harvesters Support Grant to readily support indigenous harvesters in engaging in conventional harvesting and hunting activities, thereby making it extremely suitable for driving the market development.

Europe Market Insights

Europe in the plant-based food market is projected to witness suitable growth and expansion by the end of the stipulated timeline. The market’s growth in the region is effectively fueled by an increase in health awareness, the association of plant-based diets to diminish the risks of chronic diseases, environmental sustainability, a rise in flexitarianism, and an expansion in food and retail services. According to official statistics published by OECD in November 2024, more than 1/3rd of adults in the region, which is 35%, reported residing with a long-term illness or health issues as of 2023. In addition, 37% of the women population in the region is affected with a chronic condition, in comparison to 33% of the men population. Moreover, 60% of people aged more than 65 years in the region have almost one chronic condition as of 2023, thereby enhancing the market demand.

The plant-based food market in Germany is gaining increased exposure, owing to the well-developed vegan food culture, the organic retail infrastructure, consumers demonstrating high awareness of environmental sustainability, and the government support for agricultural transition. As stated in an article published by NLM in September 2024, there has been an increase in the proportion of adolescents in the country, aged between 12 and 17 years, by 1.6% to 5%. Besides, as per the January 2023 USDA Government data report, the number of vegans in the country readily reached more than 1.5 million people as of 2022, and almost 8 million people strictly follow a vegetarian diet. Moreover, almost 10 million people are increasingly choosing to follow a standard diet without fish or meat and entirely without animal products, thus driving the plant-based food market growth.

The surge in consumer base, an increase in the demand for clean-label products, the preference for plant-based products, the existence of the most dynamic retail environments, the foodservice adoption, the presence of the flexitarian population, the development of regulatory frameworks, and suitable funding mechanisms are a few trends that are fueling the plant-based food market in the UK. As per an article published by the USDA Government in December 2025, the foodservice industry in the country is valued at USD 133 billion as of 2025, despite the surge in expenses in energy, labor, consumer demands, and regulatory modifications for cost-effective food options. Moreover, the thriving food-to-go sector, with cafes, coffee shops, bakeries, and sandwich serve as a notable driver for the sector, which is also responsible for enhancing the market in the country.

Key Plant-based Food Market Players:

- Beyond Meat (U.S.)

- Impossible Foods (U.S.)

- Kellogg's (MorningStar Farms) (U.S.)

- Conagra Brands (Gardein) (U.S.)

- Tofurky (U.S.)

- Nestlé (Switzerland)

- Unilever (UK)

- Danone S.A. (France)

- Oatly (Sweden)

- Rügenwalder Mühle (Germany)

- Quorn Foods (UK)

- Nissin Foods (Japan)

- Fuji Oil Holdings (Daiz) (Japan)

- v2food (Australia)

- Fable Food Co. (Australia)

- UNLIMEAT (South Korea)

- GoodDot (India)

- Blue Tribe Foods (India)

- Phuture Foods (Malaysia)

- The Vegetarian Butcher (Netherlands)

- Cargill (U.S.)

- Voyage Foods (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Beyond Meat focuses on replicating the taste and texture of beef, pork, and poultry using simple, plant-based ingredients. The company maintains strong partnerships with major fast-food chains to drive everyday accessibility.

- Impossible Foods leverages heme technology to deliver a meat-like sensory experience that appeals strongly to meat-eaters. The brand prioritizes foodservice expansion while gradually building retail presence across grocery chains.

- MorningStar Farms significantly benefits from Kellogg's extensive distribution network and decades of consumer trust in vegetarian products. The brand continues to expand beyond classic veggie patties into plant-based chicken and burger alternatives.

- Conagra Brands (Gardein) offers a wide range of frozen plant-based products, from crispy tenders to fishless fillets, targeting convenience-focused consumers. The brand emphasizes bold flavors and easy home preparation without compromising on texture.

- Tofurky positions itself as a long-standing, ethical brand appealing primarily to vegetarians and vegans rather than flexitarians. The company specializes in tofu-based roasts, deli slices, and sausages with a distinctly homegrown identity.

Here is a list of key players operating in the global plant-based food market:

The global plant-based food market is highly competitive, characterized by pioneering U.S. brands driving innovation alongside major multinational food corporations leveraging extensive distribution networks. Strategic initiatives center on heavy research and development investment to enhance taste and texture parity with animal-based products. Key players are aggressively pursuing partnerships with global quick-service restaurants (QSRs) such as McDonald's, KFC, and Burger King to drive mainstream adoption and trial. Besides, in May 2026, Cargill and Voyage Foods introduced NextCoa™, which is a suitable confectionery alternative to chocolate, especially in the U.S., North America. The purpose was to deliver a chocolate-based taste without the use of cocoa and increasingly utilizing advanced ingredients, thus bolstering the plant-based food industry worldwide.

Corporate Landscape of the Plant-based Food Market:

Recent Developments

- In October 2025, Beyond Meat, Inc. introduced its newest iterations of the Beyond Beef and Beyond Burger, underscoring the shared objective of both brands by offering clean food, which is made with simple ingredients for nourishing the body and supporting the planet.

- In July 2025, Danone successfully acquired the majority of stake in Kate Farms, and readily offering a comprehensive array of plant-based and organic nutrition products for both regular and medical demands.

- In October 2024, Impossible Foods unveiled 3 new family-friendly and retail products that are nutrient-dense meat from plants, known as Impossible™ Disney, the Lion King Chicken Nuggets, Impossible™ Meal Makers, and Impossible™ Corn Dogs.

- Report ID: 8574

- Published Date: May 20, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Plant-based Food Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.