Orthopedic Bone Cement Market Outlook:

Orthopedic Bone Cement Market size was over USD 723.5 million in 2025 and is expected to reach USD 1.27 billion by the end of 2035, growing at around 5.8% CAGR during the forecast period, i.e., between 2026-2035. In 2026, the industry size of orthopedic bone cement is estimated at USD 765.5 million.

The global orthopedic bone cement market is supported by sustained growth in orthopedic surgical volumes, aging populations, and expanding public healthcare expenditure directed toward musculoskeletal care. According to the World Health Organization (WHO) July 2023 data, approximately 528 million people globally were living with osteoarthritis, representing a major patient pool for joint reconstruction procedures that frequently utilize bone cement in implant fixation. The burden is expected to increase as populations age; WHO October 2025 data projects that the global population aged 60 years and older will reach 1.4 billion by 2030, compared with 1 billion in 2020.

In the U.S., the American Medical Council April 2025 reported that national health expenditures reached approximately USD 4.9 trillion in 2023, accounting for 17.6% of GDP, supporting continued access to elective orthopedic procedures. Public health systems across Europe are also increasing investments to address surgical backlogs and mobility-related disorders. For example, NHS England’s elective recovery initiatives continue to prioritize high-volume specialties such as orthopedics, helping increase procedural capacity. These demographic and funding trends are creating a favorable environment for orthopedic implant procedures, particularly hip and knee arthroplasty, where bone cement remains widely used among elderly patients and individuals with reduced bone quality.

Key Orthopedic Bone Cement Market Insights Summary:

Regional Highlights:

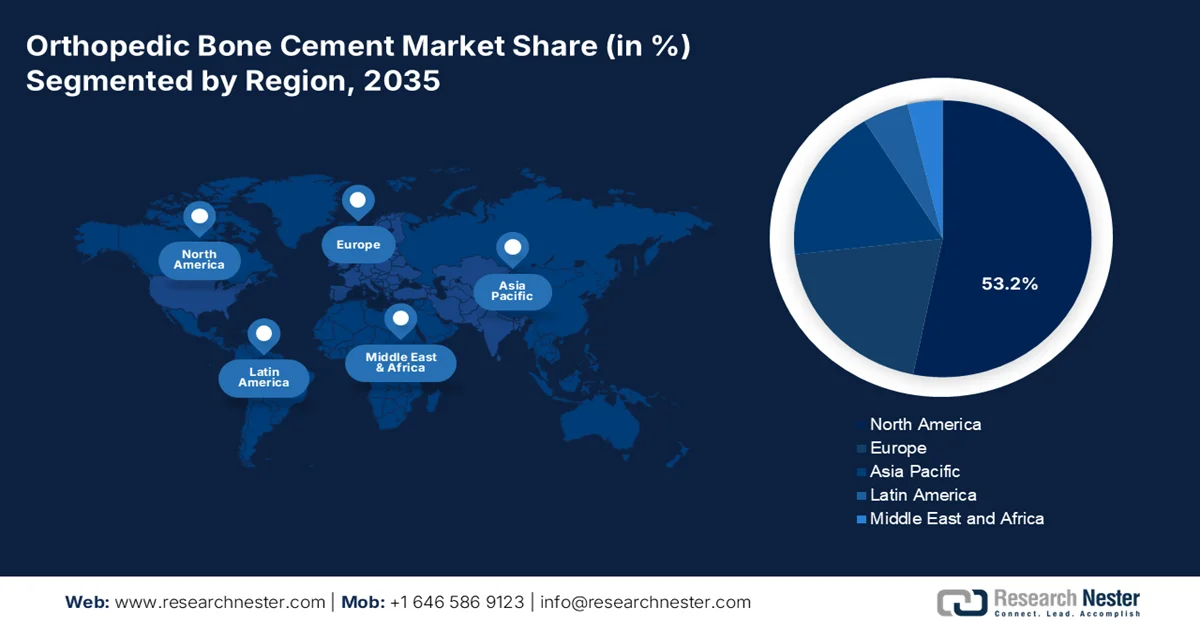

- The orthopedic bone cement market in North America is forecast to secure a 53.2% revenue share by 2035, underpinned by the region's highest per-capita joint replacement procedure rates among developed economies

- Asia Pacific is anticipated to witness the fastest expansion during 2026-2035, fueled by rapidly scaling orthopedic procedure volumes across emerging economies and increasing penetration of multinational and local bone cement suppliers

Segment Insights:

- The orthopedic bone cement market antibiotic loaded cements segment is anticipated to capture a 57.3% share by 2035, bolstered by robust clinical evidence demonstrating its effectiveness in reducing periprosthetic joint infections

- Hospitals and specialized orthopedic clinics are expected to account for nearly 75% of global consumption by 2035, stimulated by the high concentration of primary and revision arthroplasties performed in these settings alongside expanding adoption of robotic-assisted surgeries

Key Growth Trends:

- Rising government investment in joint replacement

- Increasing volume of hip and knee arthroplasty procedures

Major Challenges:

- Stringent regulatory approvals

- High R&D and clinical trial costs

Key Players: Stryker Corporation, Johnson & Johnson, Zimmer Biomet Holdings, Inc., Medtronic plc, Heraeus Medical GmbH, G-21 S.r.l.

Global Orthopedic Bone Cement Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 723.5 million

- 2026 Market Size: USD 765.5 million

- Projected Market Size: USD 1.27 billion by 2035

- Growth Forecasts: 5.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (53.2% share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, Canada

- Emerging Countries: China, India, Brazil, South Korea, Saudi Arabia

Last updated on : 22 June, 2026

Orthopedic Bone Cement Market - Growth Drivers and Challenges

Growth Drivers

- Rising government investment in joint replacement: One of the strongest demand drivers for the global orthopedic bone cement market is the increasing allocation of public healthcare budgets toward joint replacement procedures and musculoskeletal disease management. Governments are investing heavily in orthopedic infrastructure to address the growing burden of osteoarthritis, fractures, and age-related mobility disorders. Bone cement remains essential in cemented hip and knee arthroplasty procedures, particularly among elderly patients. The Centers for Medicare & Medicaid Services January 2026 data indicated that Medicare spending grew 7.8%, with joint replacement surgeries among the most reimbursed orthopedic procedures. Similarly, NHS England continues to expand orthopedic capacity under elective recovery programs aimed at reducing surgical backlogs. These investments directly support higher procedure volumes and consequently greater bone cement consumption.

- Increasing volume of hip and knee arthroplasty procedures: The growing number of joint replacement surgeries globally is directly expanding the orthopedic bone cement market. Total knee arthroplasty and total hip arthroplasty remain among the most common orthopedic procedures requiring polymethyl methacrylate (PMMA)-based bone cement. According to the American Joint Replacement Registry (AJRR) November 2024 data, more than 3.7 million hip and knee arthroplasty procedures have been recorded since registry inception, demonstrating the continued growth of orthopedic surgery volumes. As surgical access improves and waiting lists decline, hospitals are expected to increase procurement of bone cement products.

Challenges

- Stringent regulatory approvals: Navigating FDA (USA), CE Mark (Europe), and country-specific medical device regulations is a formidable barrier. Each jurisdiction demands rigorous biocompatibility, sterility, and mechanical strength testing, often requiring years for full clearance. Smaller entrants lack the regulatory affairs expertise and financial reserves to manage parallel submissions.

- High R&D and clinical trial costs: Developing a novel bone cement formulation—whether antibiotic-loaded, radiopaque, or low-viscosity—requires substantial investment in materials science, preclinical animal studies, and multi-center human trials. These costs easily exceed millions of dollars, with no guaranteed market approval. Some smaller firms attempt to license existing formulations or pursue 510(k) equivalence pathways, yet clinical outcome data requirements continue to escalate annually.

Orthopedic Bone Cement Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.8% |

|

Base Year Market Size (2025) |

USD 723.5 million |

|

Forecast Year Market Size (2035) |

USD 1.27 billion |

|

Regional Scope |

|

Orthopedic Bone Cement Market Segmentation:

Product Segment Analysis

Under the product segment, the antibiotic loaded cements are leading and is poised to hold the largest share value of 57.3% by the end of 2035. The segment is driven due to the clinical evidence demonstrating its efficacy in reducing periprosthetic joint infections, which remain the leading cause of revision surgeries. According to the NLM August 2023 study, encompassing nearly 3 million primary TKAs, confirmed that ALBC was used in 77% of all procedures, with gentamicin being the predominant antibiotic (94%) and Palacos R+G the most common formulation (62%). Notably, ALBC usage varied widely—from 100% in Norway to just 31% in the U.S. highlighting regional practice differences. This registry-level data underscores ALBC's entrenched clinical acceptance while identifying significant international heterogeneity in adoption and formulation choices.

End user Segment Analysis

Hospitals and specialized orthopedic clinics remain the predominant end-user segment, accounting for nearly three-fourths of global bone cement consumption, as these facilities perform the vast majority of primary and revision joint arthroplasties. This segment benefits from integrated surgical suites, trained anesthesia teams, and postoperative care infrastructure essential for cemented implant procedures. Strategic initiatives here include hospital group purchasing agreements that bundle bone cements with implants and mixing devices, driving volume-based pricing. Furthermore, the rising trend of robotic-assisted surgeries is concentrated in tertiary hospitals, directly boosting cement utilization per procedure. The NLM January 2022 study report states that over 82% of all total knee and hip replacements in the US were performed in hospital-based settings, cementing this end-user segment's undisputed leadership.

Application Segment Analysis

Total knee arthroplasty stands as the single largest application for orthopedic bone cement, driven by the exponential rise in knee osteoarthritis among aging populations and the proven long-term survival of cemented TKA designs. Cemented fixation in TKA offers superior tibial component stability and lower aseptic loosening rates compared to cementless alternatives, particularly in patients over 65 years. The application is further propelled by the shift toward outpatient TKA, which demands fast-curing cements with predictable setting profiles to enable same-day discharge. Additionally, robotic platforms are standardizing cement application volumes per procedure, increasing per-surgery consumption.

Our in-depth analysis of the orthopedic bone cement market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Application |

|

|

Indication |

|

|

Product |

|

|

End user |

|

|

Distribution Channel |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Orthopedic Bone Cement Market - Regional Analysis

North America Market Insights

North America is dominating the orthopedic bone cement market and is expected to capture the regional revenue share of 53.2% by the end of 2035. The region is driven by the highest per-capita joint replacement procedure rates among developed regions. The United States and Canada share similar demographic pressures from aging populations, yet diverge in procurement structures—the U.S. operates on a mixed public-private reimbursement model with significant ASC migration, while Canada follows centralized provincial tendering with strict health technology assessments. Surgeon preference for established cement brands remains deeply entrenched, creating high barriers for new entrants. Infection control mandates and antibiotic-loaded cement adoption are accelerating, while robotic-assisted platforms are standardizing application techniques. Competitive dynamics are shaped by bundled payment models in the U.S. and provincial bulk-buying programs in Canada, both exerting downward pricing pressure on suppliers.

The growing elderly population and a rising burden of musculoskeletal disorders that require surgical intervention is shaping the market in the U.S. According to the Michigan 2025 data, the number of Americans aged 65 years and older reached approximately 59.2 million in 2023, accounting for about 17.7% of the population, expanding the patient base for hip and knee replacement procedures where bone cement is commonly used. In addition, the Centers for Disease Control and Prevention (CDC) February 2024 data reported, 18.9% of U.S. adults had arthritis, highlighting the substantial prevalence of joint-related conditions that can progress to surgical treatment. Continued investments in orthopedic care infrastructure, outpatient surgery capacity, and mobility-restoration programs are expected to support stable demand for orthopedic bone cement products across hospitals and surgical centers.

The increasing orthopedic procedure volumes and sustained public healthcare investment in musculoskeletal care is driving the market in Canada. According to the Canadian Institute for Health Information May 2023 data, Canada performed approximately 137,000 hip and knee replacements, reflecting continued demand for implant fixation materials used in arthroplasty procedures. Additionally, NLM January 2026 study reported that individuals aged 65 years and older represented 19.3% of the Canadian population, highlighting the expanding demographic most susceptible to osteoarthritis, osteoporosis, and joint degeneration. As provincial health systems continue to address surgical wait times and improve access to orthopedic services, demand for orthopedic bone cement is expected to remain strong across hospitals and specialized orthopedic centers throughout the country.

APAC Market Insights

The Asia Pacific is projected to emerge rapidly during the assessed period, 2026 to 2035 in the orthopedic bone cement market. The region is characterized by stark contrasts between mature, technology-driven markets and rapidly scaling, price-sensitive emerging economies. Japan and Australia follow Western-aligned clinical protocols with high antibiotic-loaded cement adoption, while India and Southeast Asian nations prioritize cost-effective plain cement formulations for high-volume public hospital tenders. Surgeons in emerging markets exhibit strong reliance on established multinational brands, though local suppliers are gaining traction through aggressive pricing. Infrastructure gaps in cold-chain logistics remain a persistent challenge across archipelagic and rural areas.

The market in India is expanding due to increasing healthcare infrastructure development, a growing elderly population, and rising access to orthopedic surgery. According to the PIB March 2026 data, the number of operational Ayushman Arogya Mandirs exceeded 180,000, strengthening referral networks and access to surgical care across urban and rural regions. Additionally, the National Health Authority (NHA) reported that hospital admissions had been authorized under the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana, improving affordability for procedures including orthopedic interventions. The expansion of publicly funded healthcare coverage, coupled with increasing treatment capacity in tertiary hospitals, is supporting greater utilization of orthopedic implants and associated bone cement products throughout India.

The demographic shifts and increasing healthcare service utilization is driving the market in China. According to the NDP December 2025 data, the population aged 65 years and above reached approximately 220 million, accounting for about 15.6% of the country's total population and expanding the pool of patients susceptible to osteoarthritis and degenerative joint diseases. In addition, the NLM October 2025 data reported that China's medical and health institutions recorded approximately 9.55 billion healthcare visits in 2023, reflecting substantial demand for diagnostic and surgical services, including orthopedic care. Ongoing investments in hospital infrastructure, orthopedic specialty departments, and elderly healthcare programs are expected to support procedure growth and strengthen demand for orthopedic bone cement products across primary and revision orthopedic surgeries.

Europe Market Insights

The orthopedic bone cement market in Europe is characterized by significant regional heterogeneity in clinical practice, procurement frameworks, and regulatory oversight. Western European nations—Germany, France, the UK, and Italy—maintain high adoption rates of antibiotic-loaded cements, driven by national infection control guidelines from agencies like ECDC and national arthroplasty registries. The Nordic countries demonstrate near-universal cemented fixation for primary TKAs and hip replacements in elderly patients, reflecting long-standing registry-based evidence. Eastern European markets exhibit growing procedural volumes but remain price-sensitive, favoring cost-competitive formulations. The EU Medical Device Regulation (MDR) has raised compliance barriers, consolidating market share among established players with robust clinical documentation. Centralized hospital tenders and group purchasing organizations increasingly dictate pricing and product specifications across public healthcare systems.

The increasing adoption of dual antibiotic-loaded bone cement, particularly in arthroplasty procedures performed after femoral neck fractures is driving the market in Germany. According to the NLM April 2023 data, an analysis of 26,845 hemiarthroplasty (HA) and total hip arthroplasty (THA) cases found that dual antibiotic-loaded cement accounted for 7.3% of all procedures, including 7.86% of HA cases. Clinical outcomes also indicate potential benefits in infection prevention, with periprosthetic joint infection (PJI) rates of 1.5% after five years for dual antibiotic-loaded cement compared with 2.3% for single antibiotic-loaded cement. These findings support growing demand for advanced bone cement formulations in Germany, particularly for high-risk orthopedic patients and revision-sensitive procedures.

The widespread use of cemented fixation in total hip arthroplasty is shaping the market in he UK. According to a NLM March 2026 study covering 515,433 primary elective THA procedures performed between 2003 and 2024, bone cement remains a key component of joint replacement surgery across the UK. The study found that Heraeus Medical Palacos R+G high-viscosity cement accounted for 68.2% of all cemented procedures, demonstrating its dominant position in clinical practice. Furthermore, five alternative cement formulations were associated with significantly higher revision rates, with DePuy CMW3 medium-viscosity cement showing an incidence rate ratio of 2.21 compared to the reference cement. These findings emphasize the importance of clinically proven bone cement products in supporting long-term implant outcomes.

Key Orthopedic Bone Cement Market Players:

- Stryker Corporation (U.S.)

- Johnson & Johnson (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Medtronic plc (U.S.)

- Heraeus Medical GmbH (Germany)

- G-21 S.r.l. (Italy)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Stryker maintains a dominant position in the market through its proprietary Cemex® and Simplex® P bone cement lines, which are widely recognized for their high radiopacity and antibiotic-loaded variants. The company’s strategic initiatives focus on continuous formulation improvements to reduce polymerization exotherms and enhance handling characteristics for joint arthroplasty and vertebroplasty procedures.

- Johnson & Johnson, through its DePuy Synthes subsidiary, is a cornerstone innovator in the market, primarily driven by its flagship SmartSet® GHV and CMW™ cement brands. The company’s strategic roadmap emphasizes antibiotic-loaded cements for infection prophylaxis in primary and revision total joint replacements, a critical differentiator in value-based care models.

- Zimmer Biomet commands a significant share of the market through its heritage Palacos® and Optivac® cement systems, which are gold standards for total knee and hip arthroplasties. The company’s key strategic initiative revolves around smart cement platforms that incorporate radiopaque barium sulfate and gentamicin, coupled with vacuum-mixing technologies to minimize porosity and enhance mechanical strength.

- Medtronic is a formidable force in the market, particularly through its acquired portfolio of Vertebroplasty and Kyphoplasty cement systems. The company’s strategic emphasis lies in high-viscosity, cannula-injectable cements tailored for percutaneous vertebral augmentation, differentiating itself from competitors focused solely on joint arthroplasty.

- Heraeus Medical is the preeminent European pure-play specialist in the market, renowned for its Palacos® and Copal® cement families, which are extensively used in revision surgeries due to their high gentamicin and vancomycin release profiles. The company’s strategic initiatives center on antimicrobial innovation, including next-generation cements with dual-antibiotic combinations and bioresorbable carriers to combat periprosthetic joint infections.

Here is a list of key players operating in the global orthopedic bone cement market:

The orthopedic bone cement market is highly consolidated, dominated by multinational giants like Stryker and Johnson & Johnson (DePuy Synthes), which leverage extensive R&D and broad distribution networks. However, regional players are gaining traction through cost-effective alternatives and innovative antibiotic-loaded or radiopaque formulations. Key strategic initiatives include portfolio expansions via acquisitions, investments in low-viscosity cements for vertebroplasty, and partnerships with hospitals in emerging economies. For example, in July 2025, XLO offers the most extensive range of cementless & cemented joint replacement implants, trauma implants, 3d printed patient specific implants & instruments along with bone cement. Sustainability and digital surgical integration are emerging differentiators. While US and European firms lead in premium segments, Asian manufacturers are aggressively scaling up to serve local high-volume demand, intensifying price competition.

Corporate Landscape of the Market:

Recent Developments

- In April 2025, Heraeus Medical LLC, a leading provider of bone cements and biomaterials for surgical orthopedics and trauma surgery and an expert in infection management and legal entity of Heraeus Medical has acquired the product Synthecure® from Austin Medical Ventures.

- In March 2025, Zimmer Biomet Holdings has unveiled the launch of Tekcem 1G and Tekcem 3G antibiotic bone cements in India. The TEKCEM G bone cements are used for prosthesis fixation to living bone in joint reconstruction and arthroplasty procedures following trauma, including primary and revision surgeries.

- In April 2024, Heraeus Medical announced that the U.S. Food & Drug Administration has cleared COPAL® G+V, the company’s antibiotic-loaded PMMA bone cement with gentamicin and vancomycin to support PJI treatment.

- Report ID: 8619

- Published Date: Jun 22, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.