Optoelectronic Transistor Market Outlook:

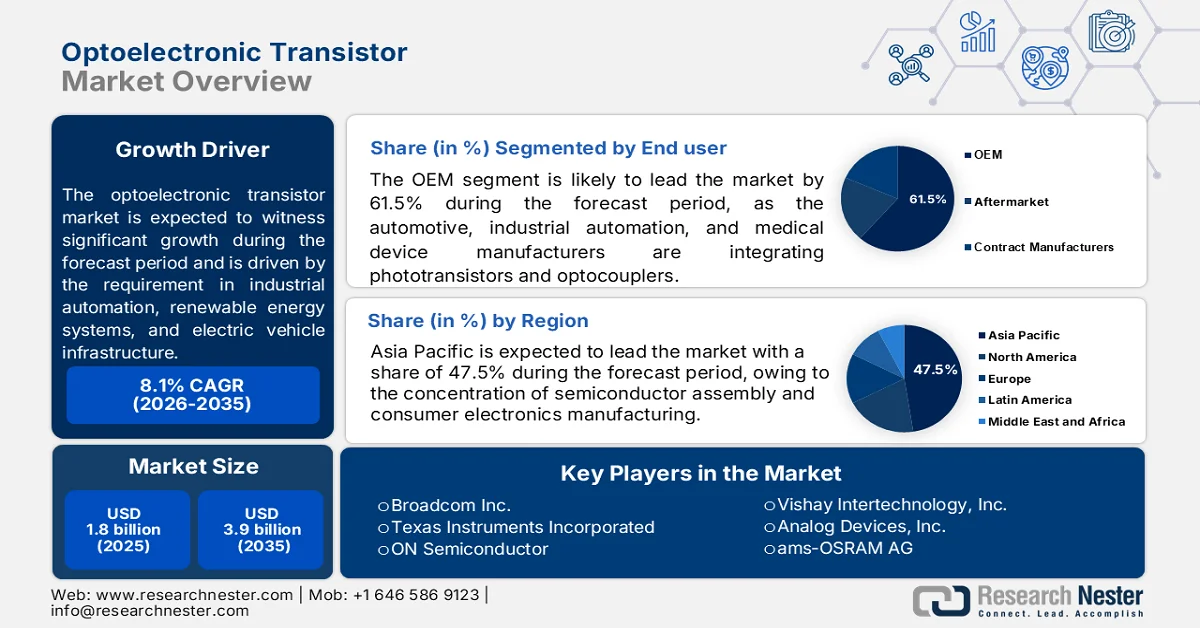

Optoelectronic Transistor Market size was valued at USD 1.8 billion in 2025 and is expected to cross USD 3.9 billion by the end of 2035, registering more than 8.1% CAGR during the forecast period i.e., 2026-2035. In 2026, the industry size of optoelectronic transistor is estimated at USD 1.9 billion.

The global optoelectronic transistor market is concentrated in industrial automation, renewable energy systems, and electric vehicle infrastructure. According to the International Energy Agency (IEA), June 2023 data, the global annual solar photovoltaic capacity additions reached approximately 450 GW, with each large-scale inverter requiring multiple optocoupler and phototransistor isolation circuits. The 2026 Clean Energy Ministerial reports that industrial motor drives account for over 40% of global electricity consumption, and safety standards under the International Electrotechnical Commission mandate galvanic isolation in variable frequency drives, directly driving demand for transistor output optocouplers. Moreover, the National Institute of Standards and Technology continues to fund research into silicon photonic integration for automotive and industrial end-users.

Solar PV Manufacturing Capacity by Region and Component, 2022-2023

|

|

U.S. (GW) |

India (GW) |

Europe (GW) |

|

Integrated |

9.0 |

37.5 |

- |

|

Thinfilm |

6.1 |

3.4 |

- |

|

Modules |

191 |

0.5 |

11.2 |

|

Cells/Modules |

3.3 |

7.4 |

7.8 |

|

Wafers/Ingots |

11.5 |

- |

- |

|

Polysilicon |

7.5 |

- |

- |

Source: IEA May 2023

Besides, the regional manufacturing patterns shape the optoelectronic transistor market supply landscape. The U.S. Department of Commerce, through the CHIPS for America program, has allocated direct funding incentives for domestic semiconductor production, including mature node facilities that produce silicon phototransistors and optocouplers for automotive and defense applications. On the other hand, the Climate Analytics 2026 data shows that cumulative wind and solar capacity is projected to reach 1400 TWh of solar and 1600 TWh of wind by 2030, of which a certain percentage is currently served by optoelectronic transistors. The U.S. Department of Energy January 2024 data notes that electric vehicle sales reached 1.4 million units in the U.S., with each onboard charger containing optocouplers for primary-secondary side isolation. These data show an active market growth globally.

Key Optoelectronic Transistor Market Insights Summary:

Regional Highlights:

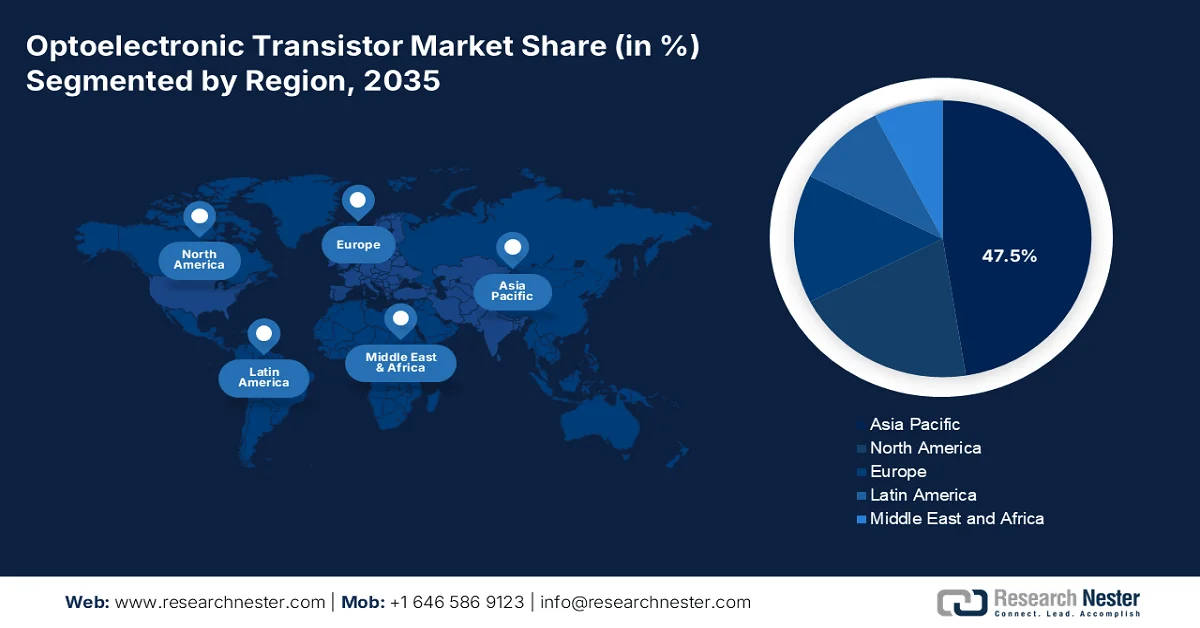

- Asia Pacific optoelectronic transistor market is anticipated to capture 47.5% regional revenue share by 2035, fueled by the strong presence of semiconductor assembly, consumer electronics manufacturing, and automotive production

- North America is projected to witness the fastest CAGR of 8.2% in the market during 2026–2035, propelled by rising demand from industrial automation, defense electronics, and electric vehicle infrastructure

Segment Insights:

- The OEM sub-segment is expected to command a 61.5% share of the optoelectronic transistor market by 2035, supported by increasing integration of phototransistors and optocouplers into automotive, industrial automation, and medical device equipment designs

- Surface-mount technology is projected to remain the dominant mounting style in the market throughout 2026–2035, attributed to its compatibility with high-speed automated assembly processes and reduced manufacturing costs

Key Growth Trends:

- Semiconductor and photonics integration funding

- NASA optical communications and space grade photonic systems

Major Challenges:

- Heterogeneous material integration complexity

- Skilled talent shortage

Key Players: Broadcom Inc. (U.S.), Texas Instruments Incorporated (U.S.), ON Semiconductor (U.S.), Vishay Intertechnology, Inc. (U.S.), Analog Devices, Inc. (U.S.), ams-OSRAM AG (Austria), Infineon Technologies AG (Germany), STMicroelectronics N.V. (Switzerland), NXP Semiconductors N.V. (Netherlands), Sony Semiconductor Solutions Corporation (Japan), Toshiba Electronic Devices & Storage Corporation (Japan), Renesas Electronics Corporation (Japan), Rohm Co., Ltd. (Japan), Sharp Corporation (Japan), Seoul Semiconductor Co., Ltd. (South Korea), Samsung Electronics Co., Ltd. (South Korea), LG Innotek (South Korea), Ayar Labs (U.S.), Comptek Solutions (Finland), Merck (Germany).

Global Optoelectronic Transistor Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.8 billion

- 2026 Market Size: USD 1.9 billion

- Projected Market Size: USD 3.9 billion by 2035

- Growth Forecasts: 8.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (47.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, Germany, South Korea

- Emerging Countries: India, Vietnam, Thailand, Mexico, Indonesia

Last updated on : 14 May, 2026

Optoelectronic Transistor Market - Growth Drivers and Challenges

Growth Drivers

- Semiconductor and photonics integration funding: The U.S. CHIPS and Science Act is a primary demand driver for optoelectronic transistor market development via large-scale federal semiconductor investment. According to the Congress.gov September 2023 data, the Act authorizes USD 52.7 billion in funding for semiconductor manufacturing R&D and workforce development, with additional tax incentives for fabrication expansion. A portion of this funding is directed toward advanced semiconductor architectures, including heterogeneous integration of photonic and electronic systems, which directly supports optoelectronic transistor research for high-speed switching and low-energy data transmission. The demand impact is concentrated in the U.S. expansion and federal lab collaboration, particularly for applications in AI hardware and defense-grade computing systems.

- NASA optical communications and space grade photonic systems: NASA is contributing to the optoelectronic transistor market demand via its optical communications and deep space network modernization programs. NASA’s Laser Communication Relay Demonstration represents a shift toward optical data transmission systems capable of achieving higher bandwidth than traditional RF systems. These systems require radiation-tolerant photonic-electronic switching components suitable for deep-space environments. Optoelectronic transistors are relevant in reducing payload power consumption while increasing data throughput for Earth observation and interplanetary missions. The demand is emerging from satellite manufacturers and subcontracted aerospace electronics suppliers aligned with NASA procurement frameworks, particularly for next-generation low-Earth orbit satellite constellations.

- Exascale computing programs: The U.S. Department of Energy is driving the demand for optoelectronic transistor market technologies via its exascale computing initiative and national laboratory infrastructure investments. According to the Exascale Project, September 2023, USD 1.8 billion in funding for exascale systems focusing on reducing data movement bottlenecks in high-performance computing. National laboratories such as Oak Ridge, Argonne, and Lawrence Livermore are evaluating photonic interconnects and hybrid optical electronic switching architectures to improve energy efficiency in supercomputing workloads. The demand signal is concentrated in defense modeling, climate simulation, and materials science applications. DOE programs also support integrated photonics testbeds that validate device-level performance under extreme computational loads, creating a structured procurement pipeline for advanced transistor-level photonic components.

Challenges

- Heterogeneous material integration complexity: The optoelectronic transistor market faces a key challenge as it requires integration of incompatible material systems. Silicon cannot emit light efficiently due to its indirect bandgap, forcing manufacturers to combine III-IV compound semiconductors such as indium phosphide and gallium arsenide with silicon substrates. This doubles the technical complexity and supply chain risk. Top companies address this by using both CMOS for volume scale performance and SiGe for ultra-high speed applications

- Skilled talent shortage: The optoelectronics transistors market barely existed as a commercial discipline a decade ago, creating a critical leadership and engineering gap. There are many vacancies with companies needing expertise across silicon photonics III-IV materials and thin film lithium niobate domains that traditionally required separate specializations. Top companies manage it by integrating lasers by leveraging deep internal expertise, yet most of the firms cannot replicate its capability.

Optoelectronic Transistor Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.1% |

|

Base Year Market Size (2025) |

USD 1.8 billion |

|

Forecast Year Market Size (2035) |

USD 3.9 billion |

|

Regional Scope |

|

Optoelectronic Transistor Market Segmentation:

End user Segment Analysis

Under the end user segment, the OEM sub-segment is leading and is poised to hold the largest share value of 61.5% by 2035. The segment is driven by the automotive, industrial automation, and medical device manufacturers integrating phototransistors and optocouplers directly into new equipment designs. According to the PIB March 2026 data, the Ministry of Electronics and Information Technology (MeitY) approved 29 new proposals with USD 856 million investment and projected production of USD 10.2 billion, adding to 46 earlier approvals. These initiatives directly target domestic manufacturing of components, including optoelectronic transistors traditionally imported by OEMs. By enabling local fabs to supply the automotive industry and medical device assemblers, ECMS reduces OEM lead times from 26 weeks to under 12 weeks. The projected 14,246 direct jobs further strengthen OEM supply chain resilience.

Mounting/Style Segment Analysis

Surface-mount technology is the predominant mounting style for the optoelectronic transistor market due to its compatibility with high-speed automated assembly processes. Unlike through-hole components that require manual insertion or dedicated wave soldering, SMD devices are placed directly onto printed circuit boards using pick and place machines and secured via reflow soldering. This approach significantly reduces manufacturing time, lowers production costs, and minimizes the physical footprint of each component. For optoelectronic transistors, SMD packaging also improves high-frequency performance by reducing parasitic inductance and capacitance caused by long leads. Additionally, SMD enables double-sided board population, allowing designers to create more compact and feature-rich electronic systems. These advantages make SMD the default choice for high-volume applications such as consumer electronics, automotive sensor clusters, industrial controls, and portable medical monitors.

Material Segment Analysis

Silicon (Si) is fueling the material segment in the optoelectronic transistor market owing to its ongoing innovations that enhance performance. As per the 2024 Optica Publishing Group study, the Si/Ge waveguide phototransistor achieves exceptional responsivity of 606 A/W at 1V bias and 1032 A/W at 2.8V bias with low dark current of just 4 µA and 42 µA. This high gain is accomplished by engineering the electric field distribution, placing two p+-doped regions in the silicon slab beneath a thin germanium epitaxial layer. The device also delivers a measured bandwidth of 1.5 GHz with stable phase noise response. This design leverages standard CMOS-compatible silicon fabrication processes, proving that silicon can compete with compound semiconductors in sensitivity while maintaining its cost and scalability advantages. Such innovations reinforce silicon's dominance across industrial automation, EV charging, and consumer sensor applications.

Our in-depth analysis of the optoelectronic transistor market includes the following segments:

|

Segment |

Subsegments |

|

Type |

|

|

Material |

|

|

Spectral Response |

|

|

Mounting/Style |

|

|

Application |

|

|

Output Configuration |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Optoelectronic Transistor Market - Regional Analysis

APAC Market Insights

Asia Pacific is dominating the optoelectronic transistor market and is poised to hold the regional revenue share of 47.5% by 2035. The market is driven by the concentration of semiconductor assembly, consumer electronics manufacturing, and automotive production. China operates the world’s largest mature node wafer fabs producing high volumes of standard optocouplers for industrial and consumer applications. Japan focuses on high-reliability phototransistors for automotive and other applications. Japan focuses on high-reliability phototransistors for automotive and medical devices using precision manufacturing and long-term customer relationships. Government initiatives across the region support domestic production through subsidies, tax incentives, and R&D funding for the localization of optoelectronic components. The shift toward electric vehicles and the renewable energy inverters further stimulates the regional demand for the isolation components.

The strong policy backing and ecosystem development in semiconductor and electronics manufacturing are driving the optoelectronic transistor market in India. According to the PIB February 2026 data, the India Semiconductor Mission, with an outlay of USD 9.3 billion, provides up to 50% fiscal support for fabs, compound semiconductor facilities, and advanced packaging, directly enabling the production of optoelectronic components. As of December 2025, 10 projects worth USD 19.5 billion have been approved across six states, strengthening domestic manufacturing capacity. Additionally, India permits 100% FDI in electronics manufacturing under the automatic route, encouraging global investment and technology transfer. The sector’s momentum is further reflected in production CAGR exceeding 17% and export CAGR above 20%, indicating strong demand expansion. Together, these factors are positioning India as a growing hub for optoelectronic transistor manufacturing and innovation.

Semiconductor Market Projections, 2026

|

Year |

USD billion |

|

2023 |

38 |

|

2024 |

45 |

|

2030 |

100-110 |

Source: PIB February 2026

Japan optoelectronic transistor market is expanding rapidly and is set to reach USD 392.8 million in 2025 and is expected to reach USD 1,047.6 million by the end of 2035. The market is projected to expand at a CAGR of 8.5% in the assessed period. In 2026, the market is estimated to reach USD 453.9 million. The market is driven by the strong demand across telecommunications and automotive electronics. OECD October 2025 data indicates that Japan reached 210 mobile broadband connections per 100 people in 2025, reflecting a highly advanced digital infrastructure that is accelerating the deployment of fiber optic networks and high-speed data systems. This directly increases the demand for optoelectronic components used in optical switching and signal processing. On the other hand, the automotive sector remains a key growth area, with the MLIT June 2021 data reporting that over 90% of passenger vehicles were equipped with Level 1 ADAS features, supporting widespread use of LiDAR and infrared sensing technologies. These trends, combined with Japan’s strong semiconductor base, are reinforcing sustained demand for the optoelectronic transistor applications.

North America Market Insights

The North America is projected to emerge as the fastest-growing region in the optoelectronic transistor market and is expected to expand at a CAGR of 8.2% during the assessed period, 2026 to 2035. The region is driven by the strong demand from industrial automation, defense electronics, and electric vehicle infrastructure. The U.S. leads in the development of radiation-hardened phototransistors for military and aerospace applications, where reliability under extreme conditions is paramount. Canada complements this with a focus on the renewable energy integration using the optocouplers and phototransistors for grid-tied solar inverters and wind turbine controls. Reshoring initiatives have supported the domestic production of mature node optoelectronic components, reducing reliance on Asia assembly while maintaining cost competitiveness via automated surface mount manufacturing lines.

The expansion in the broader semiconductor manufacturing ecosystem and sustained innovation funding are driving the optoelectronic transistor market in the U.S. According to the U.S. Census Bureau, October 2024 data, the number of semiconductor establishments increased from 1,876 to 2,545 by Q1 2024, alongside workforce growth to 202,029 employees, indicating the rising production capacity and industry scale. Capital investment is also stimulating, with total equipment expenditures rising from USD 14.4 billion to USD 30.3 billion in 2022, reflecting the upgrades in the fabrication technologies compatible with the advanced optoelectronic devices. On the other hand, U.S. R&D spending reached USD 885.6 billion in 2022, as per the NCSES May 2024 data, supporting next-generation technologies such as neuromorphic optoelectronic transistors. Moreover, the innovations such as ORNT remain at the research stage; they align with AI and photonics priorities, reinforcing long-term commercialization potential and contributing to sustained market expansion across high-performance computing and sensing applications.

The rising business-led R&D investment and targeted semiconductor initiatives, is driving the optoelectronic transistor market in Canada. According to the Government of Canada, September 2024 data, the businesses in the nation reported USD 30.4 billion in in-house R&D spending in 2022, marking a 9.4% increase, with projections reaching USD 31.4 billion in 2023, indicating sustained innovation activity and commercialization potential. This funding environment supports the development of advanced photonic and semiconductor technologies, including optoelectronic components. On the other hand, the strategic investments such as the USD 226.5 million allocated to quantum technologies and semiconductor packaging projects in Quebec are strengthening domestic manufacturing capabilities and supply chain resilience, as per the Prime Minister of Canada's April 2024 article. These projects are also expected to generate over 280 skilled jobs, reinforcing technical capacity. Collectively, expanding R&D expenditure and focused industrial investments are driving steady growth in Canada’s optoelectronic transistor market.

Europe Market Insights

The optoelectronic transistor market in Europe is shaped by industrial automation, renewable energy integration, and stringent medical safety regulations. Germany leads in the industrial applications with the variable frequency drives and robotics requiring optocoupler-based isolation for motor control systems. France focuses on solar inverter production utilizing phototransistors for grid-tied isolation in residential and utility-scale installations. The Medical Device Regulation mandates optical isolation for patient-connected equipment, sustaining demand across France and Germany medical device manufacturers. Regulatory harmonization under the IEC standards ensures cross border component qualification with the extended certification cycles targeting industrial and medical end-markets.

The substantial semiconductor investments and strong industrial R&D intensity are shaping the optoelectronic transistor market in Germany. According to the European Commission's December 2025 data, the government has approved semiconductor projects totaling over USD 34.5 billion in public and private investment, supporting first-of-a-kind fabrication facilities and strengthening regional supply chains. Germany’s firm-level investment performance remains well above the EU average, reaching 143.4% in 2025, with R&D expenditure at 143.4% and innovation spending at 145% of the EU average, reflecting a sustained commitment to advanced electronics and photonics development. This investment environment is further reinforced by Germany’s industrial model, contributing nearly half of the EU’s top R&D investors. Collectively, these factors are accelerating demand for high-performance semiconductor components, supporting steady growth in optoelectronic transistor applications.

The domestic photonics and semiconductor ecosystem, supported by both industry performance and government investment, is driving the optoelectronic transistor market in the UK. According to the Government of the UK, May 2023, the UK photonics sector had a USD 23.5 billion turnover in 2024, growing 20% over two years, and contributes USD 10.9 billion to the economy, indicating an expanding demand for the optoelectronic components across high-value applications. Long-term projections suggest that over 60% of the UK economy will depend on photonics by 2035, particularly in AI, quantum technologies, defense, and healthcare, all of which rely on the optoelectronic switching and sensing devices. To support this growth, the UK government is investing up to USD 254 million and USD 1.27 billion over the next decade in semiconductor infrastructure. These combined factors are driving sustained demand and positioning the UK as a key innovation hub for optoelectronic transistor technologies.

Key Optoelectronic Transistor Market Players:

- Broadcom Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

- ON Semiconductor (U.S.)

- Vishay Intertechnology, Inc. (U.S.)

- Analog Devices, Inc. (U.S.)

- ams-OSRAM AG (Austria)

- Infineon Technologies AG (Germany)

- STMicroelectronics N.V. (Switzerland)

- NXP Semiconductors N.V. (Netherlands)

- Sony Semiconductor Solutions Corporation (Japan)

- Toshiba Electronic Devices & Storage Corporation (Japan)

- Renesas Electronics Corporation (Japan)

- Rohm Co., Ltd. (Japan)

- Sharp Corporation (Japan)

- Seoul Semiconductor Co., Ltd. (South Korea)

- Samsung Electronics Co., Ltd. (South Korea)

- LG Innotek (South Korea)

- Ayar Labs (U.S.)

- Comptek Solutions (Finland)

- Merck (Germany)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Broadcom Inc. is a dominant player in the optoelectronic transistor market, using its extensive portfolio of fiber optic components, isolation sensors, and industrial optocouplers. The company integrates high-speed optoelectronic transistors into data center infrastructure, telecommunications, and automotive systems. Strategic initiatives include infrastructure, telecommunications, and automotive systems.

- Texas Instruments Incorporated strengthens its position in the optoelectronic transistor market by embedding these devices into the precision analog and embedded processing systems for industrial and automotive applications. Their optoelectronic transistors are critical in motor drives, grid protection, and isolated data acquisition. The company focuses on miniaturization and extended temperature range operation.

- ON Semiconductor is a key innovator in the optoelectronic transistor market, offering a wide range of photoreceivers, optocouplers, and ambient light sensors. Their devices are widely deployed in medical electronics, renewable energy inverters, and smart home systems. Strategic moves include shifting toward silicon carbide-based optoelectronic transistors for high voltage efficiency.

- Vishay Intertechnology, Inc maintains a strong foothold in the optoelectronic transistor market via its broad catalog of optocouplers, reflective optical sensors, and IR receivers. These components are essential for industrial controls, power supplies, and consumer electronics. Vishay’s strategy centers on cost-competitive mass production, rapid design in support, and developing surface mount optoelectronic production. In the 2025 fourth quarter, the company earned net revenue of USD 172,584.

- Analog Devices, Inc addresses the high-performance segment of the optoelectronic transistor market by integrating these devices into precision measurement, healthcare monitoring, and industrial isolation modules. Their optoelectronic transistors enable ultra-low leakage current and high linearity for applications such as continuous patient monitoring and seismic data acquisition. In 2025, the company spent USD 1,766,001 in R&D.

Here is a list of key players operating in the global optoelectronic transistor market:

The optoelectronic transistor market is highly competitive, driven by the rapid advancements in the fiber optic communications Li Fi and sensor technologies. The key players from the U.S., Europe, and Japan dominate the high-end R&D, focusing on miniaturization and energy efficiency. Strategic initiatives include vertical integration partnerships with telecom giants and expanding production of GaN and SiC-based devices. Asia manufacturers, mainly from South Korea and Malaysia, use cost-effective mass production and government-backed semiconductor initiatives. Mergers and acquisitions are common to consolidate intellectual property, while investments in automotive and medical sensing applications are intensifying rivalry across all regions.

Corporate Landscape of the Optoelectronic Transistor Market:

Recent Developments

- In December 2024, Ayar Labs, a startup optical chip design company, announced the completion of a USD 155 million Series D financing round. The list of investors in this round is truly impressive: in addition to the lead investors, Advent Global Opportunities and Light Street Capital, it also includes industry giants such as NVIDIA, AMD, Intel, GlobalFoundries, VentureTech Alliance (a partner of TSMC), and 3M.

- In October 2024, Comptek Solutions, a leader in advanced passivation technology for the semiconductor industry, proudly announces the successful design and installation of its pilot line, funded by the European Innovation Council (EIC). This state-of-the-art pilot line integrates Comptek's proprietary Kontrox™ passivation technology with other widely used industry techniques such as Atomic Layer Deposition (ALD), delivering a proven, scalable solution for industrial manufacturing specifically targeting power electronics and optoelectronic applications.

- In October 2024, Merck, a leading science and technology company, intensifies the strategic focus of its Electronics business on solutions for the semiconductor industry. This is ensured by the strategic convergence of the display and semiconductor business units, as well as by the expansion of the portfolio through the now completed acquisition of Unity-SC for €155 million plus additional milestone-based payments.

- Report ID: 4013

- Published Date: May 14, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Optoelectronic Transistor Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.