Battery Management System Market Outlook:

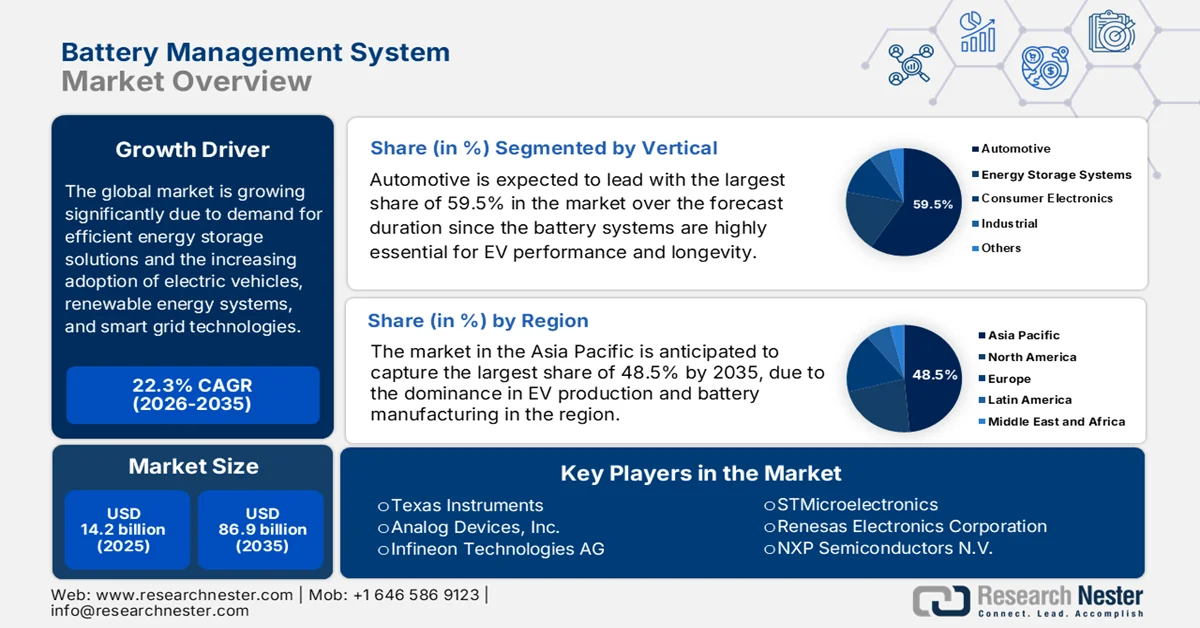

Battery Management System Market size was valued at USD 14.2 billion in 2025 and is anticipated to grow significantly, reaching USD 86.9 billion by 2035, driven by a CAGR of 22.3% during the forecast period of 2026-2035. In 2026, the industry size of battery management system is estimated at USD 17.3 billion.

The demand for efficient energy storage solutions across various sectors is the main factor behind the exceptional growth of the battery management system (BMS) market. The increasing adoption of electric vehicles, renewable energy systems, and smart grid technologies has resulted in a higher necessity for BMS solutions to optimize battery performance and extend battery life. In this context, the International Energy Agency (IEA) in 2025 reported that global electric car sales exceeded 17 million units in 2024, which denotes more than 20% of new car sales worldwide, and growth driven primarily by China, where sales surpassed 11 million, nearly two-thirds of global EV sales. It also stated that in the U.S., EV sales grew to 1.6 million, representing over 10% of new car sales, supported by the Clean Vehicle Tax Credit and additional state-level incentives, hence denoting a lucrative growth opportunity for battery management systems.

Global Electric Vehicle Sector 2024: Sales, Fleet, and Regional Growth Analysis Based on Official Statistics

|

Metric |

Global |

China |

U.S. |

Europe |

|

EV Sales (million units) |

17 |

11 |

1.6 |

3 |

|

EV Share of New Car Sales |

20% |

50% |

>10% |

20% |

|

Fleet Size (million units) |

58 |

- |

- |

- |

|

Annual Growth (2024 vs 2023) |

+25% |

+40% |

+10% |

Stagnant |

|

PHEV Share of EV Sales |

- |

~30% |

- |

- |

|

EREV Share of EV Sales |

- |

>10% |

- |

- |

|

Government Incentives |

Global varies |

trade-in USD 2,750) |

USD 7,500 Clean Vehicle Tax Credit + state incentives |

Regional subsidies phased out, CO₂ targets unchanged |

|

Top OEM Market Share Change |

- |

- |

Tesla: 60% → 38% |

- |

Source: IEA

The long-term outlook for the battery management system (BMS) market is robust, which is supported by considerable investment in terms of R&D for next-generation battery chemistries and the increasing necessity for grid-scale energy storage. For instance, in September 2024, the U.S. Department of Energy (DOE) reported that it allocated almost USD 125 million to two Energy Innovation Hub teams, which are led by Argonne National Laboratory and Stanford University, to advance next-generation battery and energy storage research. These teams will focus on developing scientific foundations for safer, longer-lasting, and more versatile rechargeable batteries by highly focusing on earth-abundant materials to reduce supply chain risks. It stated that Argonne’s Energy Storage Research Alliance is set to target compact batteries for heavy-duty transport and grid storage, whereas Stanford’s Aqueous Battery Consortium will explore aqueous batteries for long-duration grid applications, hence denoting a positive BMS market outlook.

Key Battery Management System Market Insights Summary:

Regional Highlights:

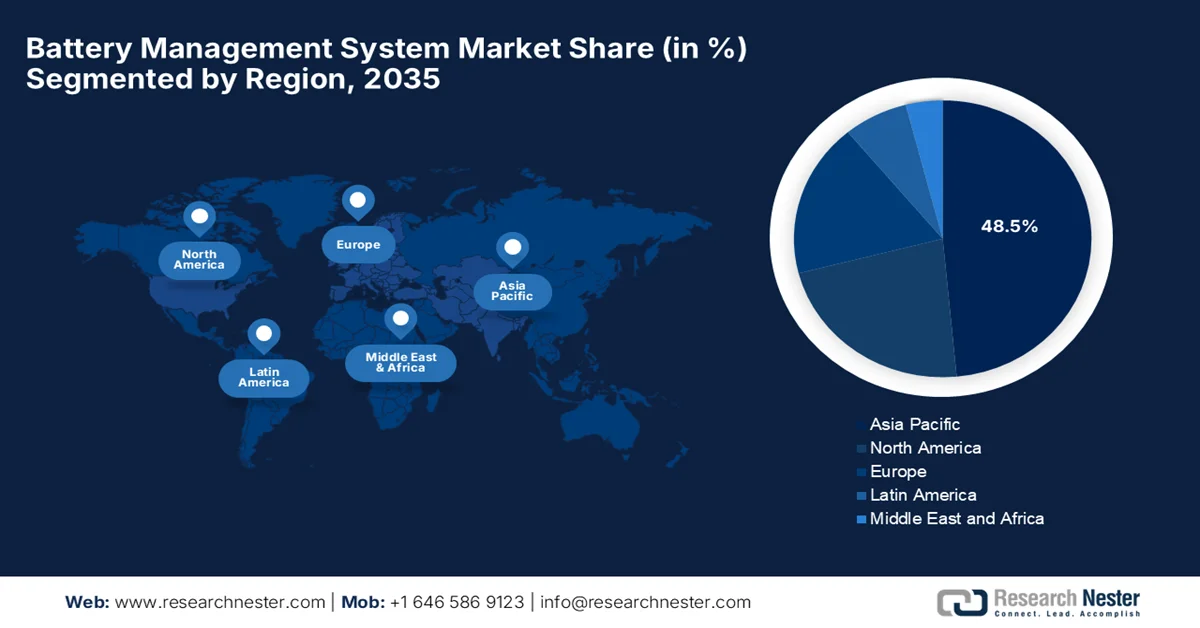

- Asia Pacific region is anticipated to dominate the battery management system market with a 48.5% share, propelled by strong EV production, battery manufacturing leadership, and robust supply chain ecosystems

- North America is poised to witness notable expansion in the forecast period 2026–2035, impelled by rapid transportation electrification and rising lithium-ion battery trade flows

Segment Insights:

- By 2035, the automotive segment in the battery management system market is projected to command a 59.5% share, driven by accelerating EV adoption and increasing demand for enhanced battery performance and longevity

- By 2035, the lithium-ion battery segment is expected to secure a considerable share, fueled by its high energy density and efficiency

Key Growth Trends:

- Expansion of renewable energy & energy storage systems

- Technological advancements

Major Challenges:

- Limited interoperability and standardization

- Thermal management

Key Players: Texas Instruments, Analog Devices, Inc., Infineon Technologies AG, STMicroelectronics, Renesas Electronics Corporation, NXP Semiconductors N.V., Eberspaecher Vecture Inc., Elithion Inc., Nuvation Engineering, LLC, Lithium Balance A/S, LG Energy Solution, Samsung SDI, Panasonic Corporation, BorgWarner Inc., Marelli Holdings Co., Ltd., BYD Company Ltd., Sensata Technologies, Inc., Schneider Electric, ABB Ltd., Johnson Matthey PLC, Denso Corporation

Global Battery Management System Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 14.2 billion

- 2026 Market Size: USD 17.3 billion

- Projected Market Size: USD 86.9 billion by 2035

- Growth Forecasts: 22.3% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (48.5% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Brazil, Mexico, Indonesia, Vietnam

Last updated on : 20 March, 2026

Battery Management System Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of renewable energy & energy storage systems: Solar, wind, and other renewables are growing, resulting in the need for grid‑scale and distributed energy storage, which rely on BMS to manage battery banks efficiently and safely. These BMS technologies are best known to balance power supply, stabilizing the grid, and optimizing charge and discharge cycles in energy storage systems. In this context, the official statistics, which were kept forward by IEA in October 2024, stated that global renewable energy capacity is projected to grow by 5,500 GW between 2024 and 2030, which is roughly equal to the current combined power capacity of China, Europe, India, and the U.S., and with solar PV contributing 80% of this growth. It also stated that by 2030, renewables are expected to meet 50% of global electricity demand, and their share in final energy consumption will rise to around 20%, which was 13% in 2023, hence benefiting the overall battery management system market.

- Technological advancements: Integration of AI, predictive analytics, and IoT capabilities is making BMS even smarter, which allows anomaly detection and predictive maintenance. New battery chemistries, such as solid‑state batteries and high‑voltage systems, require more advanced BMS configurations for optimal performance and safety, thereby fostering a favorable environment for boosting the overall battery management system (BMS) market. In November 2025, LG Energy Solution reported that its integrated battery life management solution, better. Re won the CES 2026 Innovation Award in the Vehicle Tech & Advanced Mobility category, which marks the first time a battery company was recognized solely for software technology. It is an AI-powered solution that uses machine learning and AI-driven analytics for battery health diagnostics, anomaly detection, making it suitable for standard market growth.

- Increasing use in consumer electronics: There has been an incremental demand for laptops, smartphones, wearables, and portable devices, all of which use rechargeable batteries. This factor fuels growth in the battery management system market since it enhances device performance and safety. In November 2025, the report from Voxdev stated that there is a rapid expansion of mobile phone and internet access across developing economies, showing that 84% of adults own a mobile phone, wherein smartphones are considered to be the primary device for internet access. It also mentioned that of the 67% of adults who used the internet in the past three months, 90% accessed it through smartphones, underscoring their critical role in education, financial services, and digital inclusion. Overall, the data indicate a strong demand positively impacting the BMS market’s growth and exposure.

Challenges

- Limited interoperability and standardization: This is the major obstacle that is hindering the expansion of the battery management system (BMS) market since it currently lacks universal standards for communication protocols, data formats, and system interfaces across different battery types, OEMs, and applications. Most BMS solutions use proprietary protocols, making it difficult to integrate with third‑party control systems or energy management platforms. This factor reduces cross‑vendor compatibility and ultimately slows down growth, as developers must build custom interfaces for each deployment. On the other hand, the absence of interoperability also complicates upgrades and maintenance throughout the battery’s lifecycle and imposes restrictions on data exchange needed for analytics or diagnostics, thus negatively impacting adoption in this sector.

- Thermal management: The aspects of battery performance and longevity are highly sensitive to temperature variations. Therefore, effective thermal management is highly essential to prevent overheating and maintain optimal operation. In this context, designing compact and low‑cost thermal solutions that work well with BMS is considered to be complex, especially in high‑power applications such as EVs or grid storage. In addition, the aspect of inadequate thermal control can lead to accelerated wear and lower overall system efficiency, limiting adoption in the battery management system market. Furthermore, integrating temperature sensors and cooling systems increases design complexity and unit cost, requiring a careful balance between performance, safety, and economics.

Battery Management System Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

22.3% |

|

Base Year Market Size (2025) |

USD 14.2 billion |

|

Forecast Year Market Size (2035) |

USD 86.9 billion |

|

Regional Scope |

|

Battery Management System Market Segmentation:

Vertical Segment Analysis

In the vertical segment, automotive is expected to lead with the largest share of 59.5% in the battery management system (BMS) market over the forecast timeline. The battery systems are highly essential for EV performance and longevity. On the other hand, EV adoption is at a surge, which is due to emissions reduction goals and infrastructure investments. For instance, in August 2025, FORVIA HELLA announced the start of the world’s first series production of its 12V lithium battery management system in China for use in new energy vehicles. The firm notes that the system enables precise monitoring and intelligent control of lithium batteries, ensuring optimal battery performance. Hence, from a strategic perspective, this will boost the segment’s dominance by accelerating the integration of advanced battery management technologies in electric vehicles, thus boosting automotive growth.

Battery Type Segment Analysis

By the end of 2035, the lithium-ion battery, which is based on battery type, is anticipated to grow with a considerable share in the battery management system market. The segment is largely driven by its high energy density and efficiency. The private sector innovations and government-funded research are solidifying the subsegment’s prominent position in this field. In June 2025, the U.S. Department of Energy reported that researchers at Argonne National Laboratory and Illinois Institute of Technology had developed a lithium-air battery with four times the energy density of conventional lithium-ion cells. Besides, this design uses a solid ceramic-polymer composite embedded with lithium-rich nanoparticles, enabling a stable four-electron reaction at room temperature, hence denoting a wider scope for the segment’s growth and exposure.

Topology Segment Analysis

The centralized system is predicted to grow at a significant rate in the battery management system (BMS) market during the discussed timeframe. This centralized BMS is mostly used in larger battery packs such as EVs and grid storage since it can simplify monitoring and control across many cells. In this context, in January 2023, Texas Instruments introduced new high-precision battery cell and pack monitors, which can enable automakers to maximize EV range and safety. The company also notes that these BQ79718-Q1 and BQ79731-Q1 devices deliver industry-leading accuracy in voltage, current, and temperature measurements, allowing precise state-of-charge and state-of-health estimations. Hence, such technological developments from major semiconductor manufacturers are expected to accelerate the adoption of centralized BMS architectures in high-capacity battery systems such as electric vehicles in the years ahead.

Our in-depth analysis of the battery management system market includes the following segments:

|

Segment |

Subsegments |

|

Vertical |

|

|

Battery Type |

|

|

Topology |

|

|

System Integration |

|

|

End user |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Battery Management System Market - Regional Analysis

APAC Market Insights

The Asia Pacific battery management system market is projected to be the largest market, capturing a revenue share of 48.5% during the forecast period. The region’s leadership is effectively attributable to the dominance in EV production, battery manufacturing, and renewable energy. The region benefits from suitable government subsidies, localized production of lithium-ion cells, and a robust supply chain centered in China, South Korea, and Japan. In this context, the IEA in 2023 revealed that battery demand and supply are heavily concentrated in China, which is dominating global lithium-ion production. Besides, China alone accounts for nearly 85% of global battery cell manufacturing capacity. The report also stated that the extraction and processing of critical minerals is similarly concentrated, with China at the forefront of producing the most essential materials, hence positively impacting BMS market growth.

China battery management system market is one of the largest and most influential landscapes, which is efficiently fueled by the country’s global leadership in electric vehicle manufacturing and the rapid expansion of large-scale energy storage projects. The country is witnessing a transition to renewable energy, due to which the BMS market is evolving from simple monitoring tools into integrated smart systems, which are essential for both the automotive and industrial sectors. As per the article published by IEA in 2025, China is the leader in the global EV battery supply chain, which has accounted for 80% of global battery cell production in 2024. It also supplies nearly 85% of cathode active materials and over 90% of anode active materials, giving it a near monopoly in component manufacturing. In addition, China refined about 65% of global lithium and three-quarters of cobalt, while dominating graphite mining and refining, in turn, denoting a lucrative growth opportunity for battery management systems.

The national push toward electric mobility and the inclusion of renewable energy into the power grid are driving the battery management system (BMS) market in India. Local manufacturing is gaining momentum as the government implements self-reliance initiatives and production incentives, which are providing encouraging opportunities for domestic firms to develop proprietary hardware and software solutions. In June 2025, the Press Information Bureau (PIB) reported that the Ministry of Power, Government of India, has launched a 30 GWh viability gap funding scheme to expand battery energy storage systems, aiming to attract USD 3.96 billion in investment and meet India’s storage needs by the end of 2028. The government also extended the ISTS waiver for storage projects until mid-2028 and added historic renewable capacity of 29.5 GW in 2024-25, contributing to a total installed capacity of 472.5 GW, hence making it suitable for exponential market growth in the years ahead.

North America Market Insights

The rapid electrification of the transportation sector and significant lithium-ion trade flows are certain drivers responsible for uplifting the battery management system market in North America. The region's extensive focus on high-performance electric vehicles and stringent safety regulations encourages manufacturers to opt for advanced diagnostics and thermal management technologies. In this context, the November 2025 data from the Congress government disclosed that the U.S. lithium-ion battery manufacturing has grown sharply from 2020 to 2024, wherein the output rose 359%, and domestic assembly capacity also expanded. Besides, in the import aspect, China supplied 69% of finished batteries and 33% of non-lead-acid battery parts in 2024. On the other hand, exports surged, notably to Mexico, reflecting both growing production and cross-border trade, hence denoting a positive BMS market outlook.

The U.S. market is all set to witness extensive growth due to the presence of major automotive and technology firms, which fosters a competitive environment for innovation. The BMS market dynamics are also reshaped by government initiatives, which are aimed at strengthening domestic supply chains and manufacturing independence, and have accelerated the development of localized hardware and specialized battery control technologies. In July 2024, the IEA stated that under the U.S. Infrastructure Investment and Jobs Act, USD 7.5 billion has been allocated to establish a network of 500,000 electric vehicle chargers in the country. It stated that these funds are administered through the National Electric Vehicle Formula Program, thereby enabling states to deploy publicly accessible charging and fueling infrastructure. Moreover, this initiative aims to support the expansion of EV adoption by ensuring reliable charging access, hence denoting a huge growth opportunity for battery management systems.

Canada’s abundant critical mineral resources and a focus on building a domestic end-to-end electric vehicle supply chain are responsible for uplifting the battery management system market in Canada. Growth in the country’s market is efficiently propelled by significant federal and provincial investments in large-scale battery manufacturing plants and cross-border integration with the region’s automotive industry. The government of Canada, in October 2025, announced more than USD 22 million in funding for eight projects with the main goal of accelerating battery innovation and production capacity. Besides, these investments aim to enhance battery performance, reduce costs, strengthen Canada’s supply chains, and reduce the overall environmental impacts. Therefore, with scaling domestic production, the country is positioning itself as a predominant leader in clean energy and battery innovation.

Europe Market Insights

The primary emphasis on sustainability and circular economy principles boosts the battery management system market in Europe. Growth in this region is largely propelled by the carbon neutrality goals and the rapid transition of its established automotive industry toward full electrification. The European Commission in December 2025 reported that it has launched the battery booster facility to strengthen Europe’s battery manufacturing ecosystem as part of its clean energy transition. The report states that this facility will mobilize up to USD 1.6 billion from the Innovation Fund, financed through EU ETS revenues, to support battery cell producers during their ramp-up phase. In addition, as the continent expands its domestic battery cell production, the market is evolving toward intelligent systems that support second-life applications and integration with renewable energy networks.

The battery management system market in Germany is growing at a noteworthy pace due to the large automotive engineering expertise and the integration of smart software and cloud-based diagnostics. The country is highly focused on decentralized energy storage and grid stabilization, which is pushing the boundaries of BMS functionality, ensuring these systems are essential for both transport and the transition to renewable power. As per an article published by the National Institute of Health (NIH) in July 2025 in Germany, BMS requirements are largely shaped by national, regional, and international standards, which cover both hardware and software components. It also stated that these requirements are classified as functional i.e,., state of charge and energy management, and non-functional, such as reliability and robustness, and into qualitative and quantitative criteria. Furthermore, the report highlighted the urgent need for updated, consistent standards to enhance safety, interoperability, and performance.

UK’s net-zero targets and the mandatory transition toward zero-emission vehicles are accelerating the UK market growth. The country’s market is also driven by government-backed initiatives and substantial funding, which support moving battery technologies from research to production. Based on the government data, which was published in November 2023, the UK battery strategy outlined the government’s vision to build a competitive battery supply chain in the global landscape by the end of 2030. It is focused on designing and developing future batteries, strengthening domestic manufacturing resilience, and enabling a sustainable battery industry. The approach is built around design-build-sustain, ensuring innovation, supply chain security, and sustainability, hence making it suitable for standard market growth.

Key Battery Management System Market Players:

- Texas Instruments (U.S.)

- Analog Devices, Inc. (U.S.)

- Infineon Technologies AG (Germany)

- STMicroelectronics (Switzerland)

- Renesas Electronics Corporation (Japan)

- NXP Semiconductors N.V. (Netherlands)

- Eberspaecher Vecture Inc. (Canada)

- Elithion Inc. (U.S.)

- Nuvation Engineering, LLC (U.S.)

- Lithium Balance A/S (Denmark)

- LG Energy Solution (South Korea)

- Samsung SDI (South Korea)

- Panasonic Corporation (Japan)

- BorgWarner Inc. (U.S.)

- Marelli Holdings Co., Ltd. (Japan)

- BYD Company Ltd. (China)

- Sensata Technologies, Inc. (U.S.)

- Schneider Electric (France)

- ABB Ltd. (Switzerland)

- Johnson Matthey PLC (UK)

- Denso Corporation (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Texas Instruments is identified as one of the leading providers of battery management ICs and integrated BMS solutions. The company has its strengths lying in precision analog and embedded processing technologies that enhance cell monitoring, charge balancing, and safety control, which are highly essential features for high‑performance lithium‑ion systems.

- Analog Devices, Inc. is a prominent player that is recognized for its high‑accuracy measurement and signal processing capabilities crucial to advanced BMS platforms. The firm is highly focused on integration, flexibility, and performance, enabling OEMs to tailor BMS solutions for diverse battery chemistries and system sizes.

- Infineon Technologies AG is offering power semiconductor and BMS technologies that are optimized for EV, renewable energy storage, and industrial energy applications. The firm’s solutions are highly focused on high‑efficiency power conversion, thermal management, and safety features, which are integrated with battery control systems.

- LG Energy Solution is yet another prominent supplier of lithium‑ion battery cells and integrated BMS systems for EVs and stationary storage. The company is deliberately expanding global production capacity and strategic partnerships with major automakers to advance wireless BMS and real‑time diagnostics technologies.

- Panasonic Corporation has spent years in battery production and BMS integration, supplying BMS solutions for EVs, consumer electronics, and energy storage systems. Its BMS solutions are extensively focused on robust safety protocols, reliability, and long-life cycles, supported by extensive deployment in automotive platforms.

Below is the list of some prominent players operating in the global BMS market:

The battery management system market consists of established semiconductor companies along with energy and automotive system integrators. OEM battery manufacturers such as LG Energy Solution, Panasonic, Samsung SDI, and BYD integrate improved BMS technologies for EV and ESS applications, whereas the specialized developers such as Elithion and Nuvation Engineering are focused on high‑voltage and grid storage solutions. AI‑enabled diagnostics, thermal safety enhancement, cloud connectivity, and OEM partnerships to scale adoption are the tactical strategies adopted by the leading pioneers to strengthen their market positions. In December 2025, Delta, in partnership with NXP Semiconductors, reported that it had unveiled an 800V BMS platform and vehicle computing and zonal controller systems at CES 2026 by combining Delta’s system integration expertise with NXP’s advanced automotive semiconductors.

Corporate Landscape of the Battery Management System Market:

Recent Developments

- In February 2026, BorgWarner reported that it is expanding its battery management system program with a global OEM, building on production that began in 2023. The scalable, modular system will support new BEV and PHEV passenger cars and light commercial vehicles, offering compatibility up to 800 volts.

- In October 2025, NXP introduced the industry’s first battery management chipset with built-in electrochemical impedance spectroscopy, which allows lab-grade diagnostics directly in vehicles. The solution synchronizes cell measurements at nanosecond precision, providing an understanding of battery health, safety, and fast charging performance.

- In December 2024, Marelli introduced the EIS-based BMS for automotive batteries by combining AI and cloud tracking to optimize SoC, SoP, and remaining battery life, enhancing safety, longevity, and driving range.

- Report ID: 3475

- Published Date: Mar 20, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.