Optical Sorter Market Outlook:

Optical Sorter Market size was valued at USD 3.8 billion in 2025 and is projected to reach USD 9.4 billion by 2035, rising at a CAGR of 9.6% during the forecast period, 2026-2035. In 2026, the industry size of optical sorter is assessed at USD 4.1 billion.

The optical sorter market is shaped by the rising throughput requirements and quality compliance mandates across food processing, recycling, and mining operations, supported by measurable production and waste management trends from public agencies. According to the FAO December 2024 data, the global primary crop production surpassed 9.9 billion metric tons in recent years across supply chains, driving the demand for automated sorting systems that reduce reject rates and improve the grading accuracy. Additionally, the NLM April 2022 study indicates that nearly 931 million tons of food waste is generated, reinforcing the need for optical sorting in waste stream separation and recovery operations. These data underline consistent capital investment by processors seeking yield optimization, regulatory compliance, and reduced manual labor dependency.

Besides, the recycling and resource recovery sector is expanding the optical sorting adoption due to the policy-driven waste segregation targets. As per the EPA December 2025 data, the recycling rate in the U.S. is 32.1%, with the municipal solid waste generation being 292.4 million tons, creating a sustained demand for automated material recovery facilities. On the other hand, the mineral production continues to grow with copper output alone exceeding 22 million metric tons, as per the SME 2026 data, supporting the ore sorting to improve the grade efficiency and reduce the energy consumption. These publicly reported production volumes and policy targets are directly influencing the procurement cycles, with enterprises prioritizing systems that deliver measurable throughput gains, traceability, and compliance with environmental and export regulations.

Key Optical Sorter Market Insights Summary:

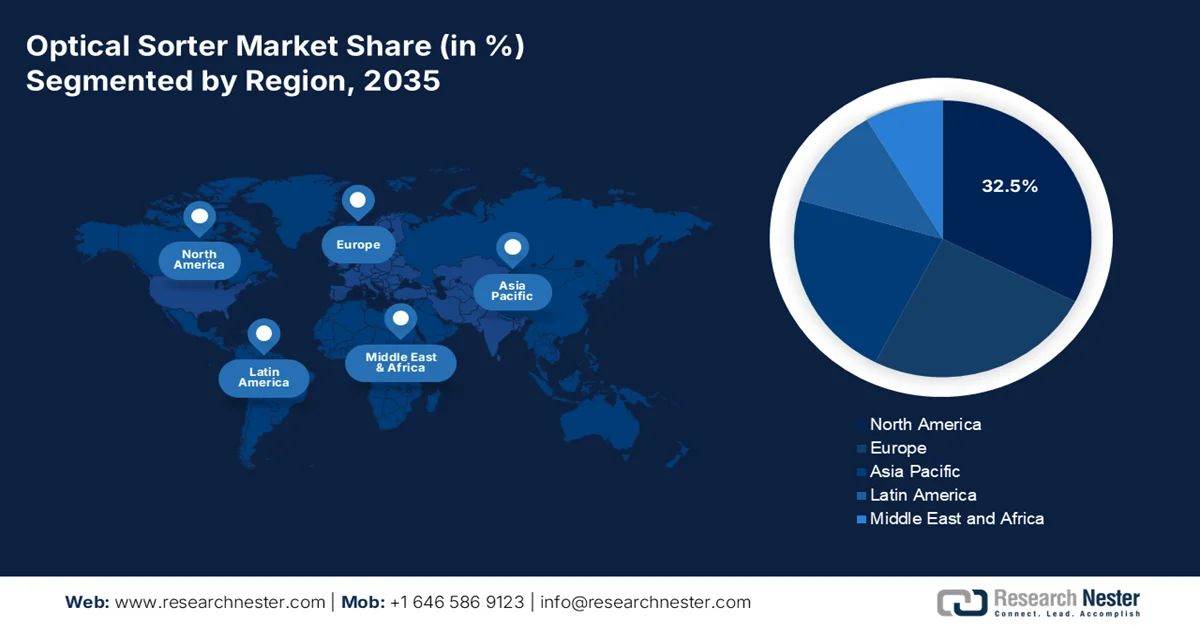

Regional Highlights:

- The optical sorter market in North America is projected to hold a leading share of 32.5% by 2035, supported by stringent recycling regulations, labor dynamics, and increasing waste stream complexity

- Asia Pacific is expected to register the fastest growth through 2026–2035, stimulated by rising domestic recycling mandates and expanding automation adoption across waste management systems

Segment Insights:

- The fully automatic sorters segment in the optical sorter market is anticipated to capture a 78.3% share by 2035, driven by speed consistency and continuous 24/7 operation without human intervention

- The food sorters segment is forecasted to maintain a leading share by 2035, fueled by rising demand for contaminant-free food products and stringent quality standards

Key Growth Trends:

- Growth in circular economy investment

- Climate and sustainability policies

Major Challenges:

- Low defect detection accuracy issues

- Disrupted supply chains and component sourcing

Key Players: Tomra Systems, Bühler Group, Key Technology, Satake Corporation, CP Manufacturing, Pellenc ST, Steinert, Sesotec, Newtec, Raytec Vision, Greefa, Hefei Meyer Optoelectronic Technology, Anzai Manufacturing, Redwave, National Recovery Technologies, Hefei Taihe Optoelectronic Technology, MSort, Daewon GSI, ProSort, MSS, Inc. .

Global Optical Sorter Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.8 billion

- 2026 Market Size: USD 4.1 billion

- Projected Market Size: USD 9.4 billion by 2035

- Growth Forecasts: 9.6% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (32.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Indonesia, Vietnam

Last updated on : 1 May, 2026

Optical Sorter Market - Growth Drivers and Challenges

Growth Drivers

- Growth in circular economy investment: Circular economy initiatives backed by the governments are stimulating the adoption of the market. The European Commission’s Economy Action Plan allocates substantial funding under programs such as Horizon Europe, with billions of euros directed toward waste reduction and recycling innovation. Similarly, the METI 2025 data indicated that Japan is set to invest USD 13.8 billion over the next ten years in the resource recycling sector. These programs highlight the automated sorting for plastics, e-waste, and packaging streams. These programs highlight the automated sorting for plastics, e-waste, and packaging streams with optical sorters positioned as the primary technology for achieving the high purity output required to meet recycled content mandates across both regions.

- Climate and sustainability policies: The climate policies are driving the optical sorter demand for prioritizing waste reduction and resource efficiency. According to the United Nations Climate Change September 2024 data, food waste accounts for 8% to 10% of the global greenhouse gas emissions, prompting national strategies to reduce the losses. Programs funded under climate action plans push the adoption of technologies that improve the sorting accuracy and recovery rates. For example, the optical sorters deployed in food processing lines reduce the landfill-bound organic waste by identifying and redirecting the imperfect but edible produce to the secondary market, while the NIR-based system in municipal facilities lowers methane emissions from decomposing plastics, and certain percentage diversion rates for recyclable packaging materials.

- Public investment in agricultural exports: Export-oriented agricultural policies are increasing the demand for high-precision sorting systems. government fund certification, grading, and export infrastructure to meet the international standards. For instance, the USDA export programs and inspection services support large-scale agricultural shipments, while India’s APEDA promotes quality compliance for global markets. These initiatives require consistent sorting accuracy to meet the buyer's specifications. Manufacturers should integrate the export-grade quality parameters and certification compatibility into their systems. According to the World Trade Organization 2026 data, the global export of agricultural products reached USD 1,493.91 billion in 2024, reinforcing the need for standardized sorting technologies to maintain competitiveness.

Global Agricultural Products Trade Flow, 2020 to 2024

|

Year |

Import |

Export |

|

2020 |

1,199.24 |

1,158.66 |

|

2021 |

1,419.72 |

1,354.37 |

|

2022 |

1,586.72 |

1,496.74 |

|

2023 |

1,534.4 |

1,470.56 |

|

2024 |

1,559.68 |

1,493.91 |

Source: World Trade Organization 2026

Challenges

- Low defect detection accuracy issues: New players in the market face the technical challenge of achieving high detection accuracy, as optical sorters are prone to false negatives and false positives. These errors significantly impact overall system performance and customer trust. The limitation is mainly pronounced with infrared sorting technologies, which struggle with plastics containing carbon black pigment. Carbon black absorbs IR light, preventing reflection to sensors and making accurate detection difficult.

- Disrupted supply chains and component sourcing: Supply chain disruptions have emerged as a critical challenge for optical sorter manufacturers, affecting both production timelines and cost structures. The market is facing issues sourcing high-quality components such as hyperspectral cameras, NIR sensors, lasers, and specialized lighting systems. These disruptions in prices for alternative suppliers will compress already thin margins. Global consumer health concerns have amplified the need for validated component quality, making it harder for new manufacturers to prove their supply chain reliability to skeptical buyers.

Optical Sorter Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.6% |

|

Base Year Market Size (2025) |

USD 3.8 billion |

|

Forecast Year Market Size (2035) |

USD 9.4 billion |

|

Regional Scope |

|

Optical Sorter Market Segmentation:

Operation Segment Analysis

Under the operation segment, the fully automatic sorters are expected to hold the largest share value of 78.3% by the end of 2035 in the optical sorter market. The segment is driven by their speed consistency and ability to operate 24/7 without human intervention. Fully automatic sorters integrate AI, real-time sensors, and high-speed ejection systems, making them indispensable for the large-scale recycling facilities and food processing lines. According to the My Meyer April 2026 data, the automatic optical sorting systems reported a 70% to 80% reduction in labor costs and a 15% to 20% increase in throughput capacity compared to semi-automatic alternatives. The trend toward lights-out manufacturing and rising wage pressures in developed economies further accelerate adoption. Fully automatic sorters also reduce human exposure to hazardous waste and improve sorting accuracy. As Industry 4.0 principles spread, investment in fully automated optical sorters will continue to outpace semi-automatic models globally.

Product Type Segment Analysis

Within the product type segment, the food sorters sub-segment is leading in the market. These systems are used for nuts, grains, fruits, vegetables, seafood, and meat to remove the foreign material defects and contaminants. According to the NLM January 2024 study, the optical sorter in the food sector has provided a 100% correct classification rate of the contaminants. Rising consumer demand for premium blemish-free produce, along with strict zero-tolerance policies for allergens and foreign objects, drives this growth. Additionally, labor shortages in agricultural processing have pushed packers to invest in high-speed food sorters that can handle delicate products without damage. Additionally, labor shortages in agricultural processing have pushed packers to invest in high-speed food sorters that can handle delicate products without damage, while real-time AI-driven quality grading further reduces waste and maximizes throughput across sorting lines.

End user Industry Segment Analysis

The food and beverage processing is the leading sub-segment in the end-user industry segment in the market. The optical sorter in this industry ensures product safety, quality grading, and regulatory compliance. The food processing facilities that implemented optical sorting for nuts, grains, and frozen vegetables have experienced a reduction in the detected foreign object contamination incidents. Further, the need to comply with the FDA Food Safety Modernization Act (FSMA) and similar global regulations drives continuous investment. Optical sorters now detect not only color defects but also hidden biological hazards using hyperspectral imaging. As automation becomes standard in food plants, the food & beverage industry will remain the largest end user of optical sorting technology through 2035.

Our in-depth analysis of the optical sorter market includes the following segments:

|

Segment |

Subsegments |

|

Platform |

|

|

Technology |

|

|

Application |

|

|

Product Type |

|

|

Operation |

|

|

End user Industry |

|

|

Component |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Optical Sorter Market - Regional Analysis

North America Market Insights

North America is projected to dominate the optical sorter market and is poised to hold the regional revenue share of 32.5% by the end of 2035. The region is defined by a mature evolving landscape where the regulatory pressure, labor dynamics, and waste stream complexity drive technology adoption. In the U.S., the shift from voluntary to mandatory recycling obligations at the state level has pushed the material recovery facilities to replace manual sorting lines with automated optical systems capable of meeting stricter contamination limits. The market also reflects regional specialization, such as U.S. buyers prioritizing high-throughput systems for mixed plastics and e-waste, and Canada operators emphasizing multi-material flexibility to handle diverse packaging formats generated under national zero-plastic-waste timelines.

The sustained public investment in waste management, food quality systems, and mining efficiency, with measurable output volumes reinforcing equipment demand for the optical sorter market in the U.S. The U.S. Environmental Protection Agency's March 2026 data reported that plastic generation reached 35.7 million tons, requiring advanced sorting systems to improve recovery rates within material recovery facilities. On the other hand, the International Nut & Dried Fruit December 2024 data indicated that the U.S. leads in tree nut production, with 39% of the global production in the U.S., driving demand for high-throughput grading and defect-detection technologies across processing lines. Additionally, the U.S. Geological Survey's January 2024 data noted that crushed stone production totaled 1.5 billion metric tons, reflecting strong mining output where sensor-based ore sorting is increasingly deployed to enhance material quality and reduce downstream processing costs. These sector-specific volumes backed by federal reporting are directly influencing procurement strategies for automated sorting systems.

Crushed Stone Statistics, 2019 to 2023

|

|

2019 |

2020 |

2021 |

2022 |

2023 |

|

Sold or used by producers |

1,470 |

1,460 |

1,510 |

1,550 |

1,500 |

|

Recycled material |

32 |

31 |

33 |

33 |

33 |

|

Imports for consumption |

24 |

20 |

19 |

16 |

13 |

|

Consumption, apparent |

1,530 |

1,510 |

1,560 |

1,600 |

1,600 |

|

Price, average unit value, dollars per metric ton |

12.36 |

12.69 |

13.19 |

14.23 |

15.60 |

|

Employment, quarry and mill, number |

69,000 |

68,000 |

68,900 |

70,400 |

70,000 |

|

Net import reliance as a percentage of apparent consumption |

2 |

1 |

1 |

1 |

1 |

Source: the U.S. Geological Survey January 2024

The growth across waste management, agri-food processing, and mining output is driving the market in Canada, all of which require efficient material separation systems. Government of Canada November 2024 data reported that total solid waste generated reached 36.5 million tons, reinforcing demand for advanced sorting in recycling and recovery facilities. In January 2026, the grain production totaled 35.4 million tons, driving the adoption of optical sorting to meet export quality standards. Moreover, February 2026 data highlighted that the total value of mineral production surpassed USD 64.3 billion in 2024, reflecting strong mining activity where ore sorting technologies are increasingly deployed to enhance grade efficiency. These government-backed production and waste volumes are directly contributing to steady capital investment in automated optical sorting systems across Canada.

APAC Market Insights

The North America is projected to emerge as the fastest-growing region in the optical sorter market and is expected to expand at a CAGR of 9.4% during the assessed period, 2026 to 2035. The region is driven by China’s domestic recycling mandates following the National Sword, Japan’s Plastic Resource Circulation Act, and emerging regulations across India and Southeast Asia. China leads with the ban on imported waste and domestic targets to reduce plastic recycling, forcing the MRF modernization. Japan’s METI allocated a budget for optical sorter deployment, targeting collection efficiency. Labor shortages across Japan and South Korea accelerate automation, and China's aging manual sorting workforce drives replacement demand. Food sorting applications grow across all countries, driven by export quality requirements.

The rising plastic waste volumes and the need for efficient segregation infrastructure are driving the market in India. According to the CEEW January 2025 data, the country generates approximately 4 to 9 million tons of plastic waste annually, with recycling rates ranging between 13% and 60%, indicating gaps in sorting efficiency and material recovery. Packaging accounts for around 59% of total plastic consumption, creating a high-volume waste stream that requires precise identification and separation technologies. Moreover, the improvements in processing capability are evident with Odisha achieving a 65% recycling rate in 2022 to 2023, reflecting the impact of better infrastructure and compliance mechanisms. These dynamics highlight increasing demand for the automated optical sorting systems to handle mixed plastic streams, improve recovery yields, and support policy objectives aimed at reducing dependence on virgin materials and strengthening circular economy practices across India.

The optical sorter market in China is expanding steadily, supported by large-scale grain production and increasing focus on post-harvest quality improvement. As the world’s leading rice producer, the country relies heavily on efficient paddy processing, where optical color sorting technologies are proving critical. According to the IJAFP 2024 study, in terms of physical quantity, the optical sorters can reduce immature seeds from 5.64% to 0.16%, weedy grains from 16.83% to 0.47%, and chalky grains from 1.20% to 0.45%, significantly improving final product quality without altering moisture content. These measurable gains align with China’s emphasis on food safety, yield optimization, and minimizing losses across agricultural value chains. With increasing mechanization and modernization of milling infrastructure, demand for high-precision sorting systems is rising. As processors prioritize consistency and export-grade standards, optical sorting technologies are becoming a key component in upgrading China’s grain handling and processing ecosystem.

Europe Market Insights

The optical sorter market in Europe is driven by the binding EU recycling targets, extended producer responsibility harmonization, and the circular economy action plan. The plastic packaging recycling rate is directly requiring optical sorter deployment of optical sorters across all member states. Germany leads in the strictest packaging regulations, followed by France’s Anti-Waste Law. Southern parts of the region are catching up via recovery and resilience facility funding for waste management modernization. The key trends include AI-integrated near-infrared sorters for black plastics, hyperspectral imaging for e-waste separation, and mobile optical units for construction and demolition debris. Food sorting remains strong, driven by EFSA contamination zero-tolerance policies for nuts, grains, and dried fruits.

Large recycling operations and early adoption of advanced sorting technologies are fueling the market in Germany. Industrial deployments, such as in November 2025, the partnership of Vogt Plastic and Cimbria is propelling excellence in plastic recycling. Vogt Plastic’s facility, which processes around 200 tons of plastic per day using 19 optical sorters across dedicated HDPE and PP lines, highlights the scale at which automated sorting is being integrated to achieve high-purity outputs. On the other hand, the innovation-led installations are strengthening market expansion, for instance, in July 2025, the Recycleye STADLER project in Aulendorf introduced AI-only optical sorting for construction and demolition waste, enabling precise separation of mineral fractions such as brick and concrete. These developments indicate increasing capital investment in both capacity expansion and technology upgrades, driving the market growth and expansion.

The public funding programs and private sector investments aimed at improving recycling infrastructure and material recovery are driving the optical sorter market in the UK. Government-backed initiatives such as the Scottish Recycling Improvement Fund are directly enabling technology adoption; for example, Fife Council secured USD 592,200 to install a Tomra optical sorter as per the Fife Council's February 2022 data for flexible plastic segregation, supporting Scotland’s first dedicated facility for film recycling. This reflects a broader shift toward the handling of complex waste streams that require advanced sorting capabilities. On the other hand, industry-led upgrades are reinforcing growth, as seen in Tetra Pak’s September 2025 deployment of AI-powered optical sorting technology in Scotland, marking a first for carton sorting applications in the region. These developments strengthen the demand for optical sorting systems in the UK.

Key Optical Sorter Market Players:

- Tomra Systems (Norway)

- Bühler Group (Switzerland)

- Key Technology (U.S.)

- Satake Corporation (Japan)

- CP Manufacturing (U.S.)

- Pellenc ST (France)

- Steinert (Germany)

- Sesotec (Germany)

- Newtec (Denmark)

- Raytec Vision (Italy)

- Greefa (Netherlands)

- Hefei Meyer Optoelectronic Technology (China)

- Anzai Manufacturing (Japan)

- Redwave (Austria)

- National Recovery Technologies (U.S.)

- Hefei Taihe Optoelectronic Technology (China)

- MSort (China)

- Daewon GSI (South Korea)

- ProSort (India)

- MSS, Inc. (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Tomra Systems is a top global player in the optical sorter market, leveraging decades of expertise in sensor-based sorting for recycling food and mining. The company has strategically integrated deep learning and near-infrared technology to enhance the material identification accuracy. The company has made revenue of USD 1.46 billion in 2024 as per the company’s annual report.

- Buhler Group excels in food safety and grain processing, mainly via its SORTEX series, and leads in the market. The company’s strategic initiatives center on AI-driven platforms such as Sortex H SpectraVis, which use hyperspectral imaging to detect subtle defects invisible to human eyes. The company has made a net profit of 5.9% rise in 2024 compared to the previous year.

- Key Technology is renowned for its VERYX and Optyx systems, which deploy high-resolution cameras and laser sensors for fresh-cut produce and frozen foods. The key strategic initiatives include integrating artificial intelligence with object recognition algorithms to sort by shape, size, and biological properties. The company has also focused on a user-friendly touch interface and remote service capabilities.

- Satake Corporation holds a strong position in the optical sorter market, mainly for rice, cereals, and legumes. The company’s strategic initiatives involve multispectral cameras and near-infrared technologies to remove discolored foreign or contaminated kernels. Satake has advanced its SORTEX range and developed AI-based solutions for recycling.

- CP Manufacturing via its MSS division is a key player in the optical sorter market in heavy-duty recycling. The company’s strategic initiatives center on deploying optical sorters for single-stream recycling, e-waste, and construction debris. The company has championed the use of near-infrared and color cameras combined with pneumatic ejection.

Here is a list of key players operating in the global market:

The global optical sorter market is highly competitive, dominated by established players from Europe, Japan, and the U.S., and on the other hand, the emerging economies such as China and India are gaining traction. The key strategic initiatives include AI-integrated sorting solutions, hyperspectral imaging for complex waste streams, and strategic partnerships with recycling firms. Companies are also expanding via acquisitions to enhance their regional presence and product portfolios. For example, in May 2024, STEINERT acquires the MSort product line. Sustainability pressures and food safety regulations are driving innovation with a focus on multi-sensor sorters and cloud-based data analytics to improve sorting accuracy and operational efficiency for recyclables and food products.

Corporate Landscape of the Market:

Recent Developments

- In April 2026, Satake announced the global expansion of the SLASH modular range of compact optical sorters after the successful launch in Japan. The Slash series of optical sorters showcases Satake's latest technological innovations and customer-centered design.

- In December 2025, Key Technology (Key), a member of Duravant’s Food Sorting and Handling Group, introduces its COMPASS® optical sorter for leafy greens. Designed to inspect fresh-cut product straight from the field, this belt-fed system combines high-performance foreign material (FM) detection and removal with gentle, hygienic product handling.

- In May 2025, Bühler launched the groundbreaking SORTEX AI700 optical sorter in London, transforming impurity detection in food processing. Its first application specializes in removing gluten-containing grains from oats, a critical step in ensuring gluten-free product integrity.

- Report ID: 8551

- Published Date: May 01, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.