Ophthalmic Devices Market Outlook:

Ophthalmic Devices Market size was over USD 48.8 billion in 2025 and is expected to cross USD 80.2 billion by the end of 2035, growing at more than 5.1% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of ophthalmic devices is assessed at USD 51.2 billion.

The globally aging population and the rising prevalence of vision disorders are rearranging the growth dynamics of the ophthalmic devices market. The technological advancements, especially the integration of artificial intelligence and digital health platforms into diagnostic and surgical equipment, are readily transforming patient care by streamlining workflows. According to an article published by the World Health Organization (WHO) in February 2026, globally, at least 2.2 billion people live with near or distance vision impairment, and in 1 billion cases, it could have been prevented or remains unaddressed. The report also mentioned the leading causes, which include cataracts, 94 million cases; refractive errors, 88.4 million; age-related macular degeneration, 8 million; glaucoma, 7.7 million; and diabetic retinopathy, 3.9 million, whereas presbyopia affects 826 million people. Vision impairment is four times more prevalent in low- and middle-income regions compared to high-income ones, elevating the growth potential for the ophthalmic devices industry.

Furthermore, the ophthalmic devices market is influenced by both the increasing cost burden of eye diseases, which supports demand growth, and reimbursement and affordability pressures that affect purchasing decisions and technology deployment rates. Apart from this, higher treatment costs and growing patient volumes encourage healthcare providers and governments to make investments in terms of diagnostic and surgical equipment to improve efficiency and reduce avoidable vision loss. The U.S. Centers for Disease Control and Prevention in May 2024 reported that the economic burden of vision loss and blindness in the U.S. has been staggering, which was USD 134.2 billion in a year, including USD 98.7 billion in direct medical, nursing home, and supportive services, and USD 35.5 billion in indirect costs such as absenteeism and lost productivity. Medicare alone paid USD 10.2 billion for major eye diseases such as AMD, cataracts, diabetic retinopathy, and glaucoma by covering 41% of beneficiaries.

Key Ophthalmic Devices Market Insights Summary:

Regional Highlights:

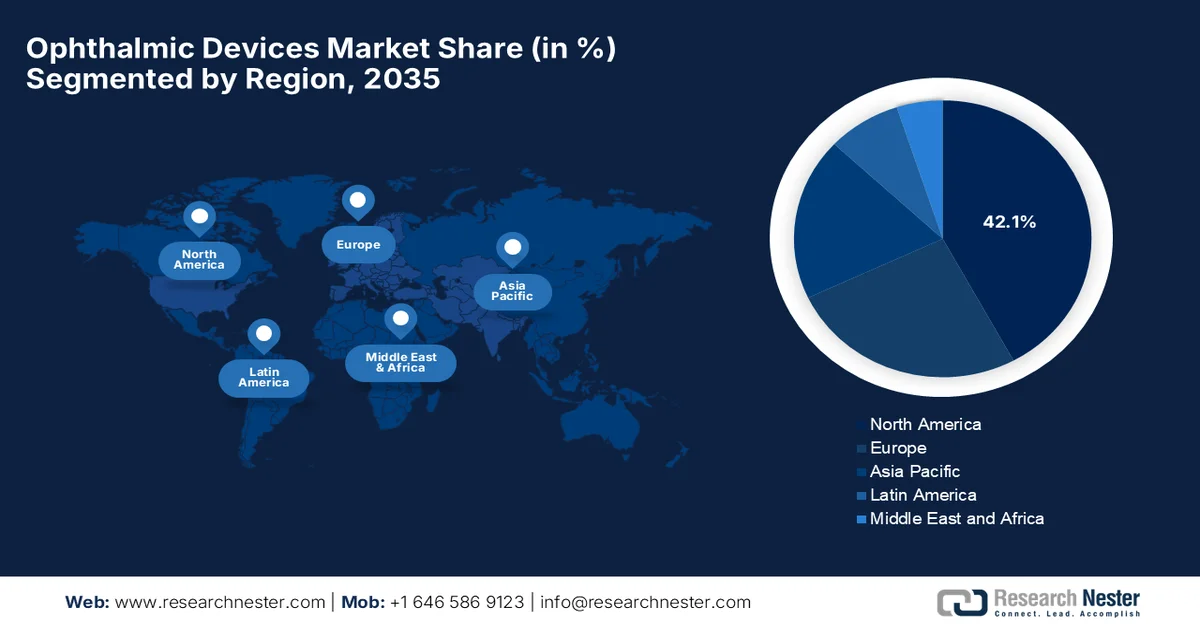

- In the ophthalmic devices market, North America is projected to capture 42.1% of the global share by 2035, bolstered by rapid adoption of artificial intelligence, cloud-based telehealth networks, advanced surgical robotics, strong professional training infrastructure, and early product approvals by regional regulatory bodies

- Asia Pacific is anticipated to expand at a rapid pace during 2026-2035, fueled by the acceleration of domestic manufacturing and local medical equipment industrialization, government-led healthcare subsidization programs, and rural wellness missions aimed at eradicating preventable blindness

Segment Insights:

- In the ophthalmic devices market, the hospitals & eye clinics segment is projected to account for 80.5% share by 2035, reinforced by the high volume of ophthalmic surgeries and diagnostic procedures, availability of advanced imaging and surgical technologies, presence of skilled ophthalmologists, and increasing patient preference for specialized eye care services

- The Cataract segment is anticipated to secure a considerable share by 2035, stimulated by the rising global prevalence of age-related cataracts, increasing access to cataract screening and surgical services, and continuous advancements in intraocular lenses and phacoemulsification technologies

Key Growth Trends:

- Increasing awareness and early diagnosis

- Expansion of healthcare infrastructure

Major Challenges:

- Stringent regulatory approvals

- Limited access in rural and emerging regions

Key Players: Alcon, Johnson & Johnson Vision, Bausch + Lomb, Carl Zeiss Meditec, EssilorLuxottica, Hoya Corporation, Topcon Healthcare, NIDEK Co., Ltd., Halma plc, Heidelberg Engineering, Haag-Streit Group.

Global Ophthalmic Devices Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 48.8 billion

- 2026 Market Size: USD 51.2 billion

- Projected Market Size: USD 80.2 billion by 2035

- Growth Forecasts: 5.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.1% share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: U.S., Germany, Japan, China, France

- Emerging Countries: India, South Korea, Singapore, Brazil, Saudi Arabia

Last updated on : 23 June, 2026

Ophthalmic Devices Market - Growth Drivers and Challenges

Growth Drivers

- Increasing awareness and early diagnosis: The expanding public health campaigns, regular vision screening programs, and awareness of preventive eye care are encouraging early diagnosis of eye conditions. This aspect of early detection requires advanced diagnostic technologies, which increases demand in the ophthalmic devices market. In June 2022, the article published by NIH revealed that a survey over 46 countries revealed that childhood vision screening programs vary considerably in terms of screening age, tests used, personnel involved, and frequency of examinations. It mentions that all countries provide some form of vision screening between the ages of 3 and 7 years, but the number of screenings per child ranges widely. The study found that infant screening is available in all participating countries, and at least one childhood vision screening program exists nationwide, positively contributing to the ophthalmic devices market’s expansion.

- Expansion of healthcare infrastructure: The burgeoning investments in terms of specialty eye clinics, ambulatory surgical centers, and diagnostic facilities are increasing access to ophthalmic care. Also, emerging economies are witnessing medical infrastructure growth, supported by government initiatives and private investments, which in turn drives the procurement of ophthalmic devices. For instance, in May 2026, Adani Foundation announced the launch of a substantial USD 18 million rural vision care initiative in Bihar to establish the Adani Centre for Eye and Adani Training in Ophthalmic Medicine with a total capacity for 330,000 surgeries annually and training for 1,000 professionals each year. This particular plan also includes a 200-bed hospital in Pirpainti to expand healthcare access in eastern Bihar. In addition, Adani announced a USD 60 million expansion to extend affordable vision care across underserved regions of India, benefiting the overall ophthalmic devices market.

Global Contact Lens Export Rankings by Country 2023- Shipment Value and Volume

|

Country |

Export Value (000 USD) |

Quantity (Items) |

|

Europe |

1,907,251.26 |

5,695,370,000 |

|

Ireland |

1,300,074.82 |

4,760,650,000 |

|

Germany |

1,197,634.71 |

2,453,120,000 |

|

U.S. |

1,076,005.56 |

641,508,000 |

|

Singapore |

552,983.93 |

349,655,000 |

|

Other Asia, nes |

518,357.03 |

1,967,070,000 |

|

Netherlands |

191,390.98 |

67,544,000 |

|

Malaysia |

191,267.83 |

312,628,000 |

|

Hungary |

108,359.15 |

428,374,000 |

|

Czech Republic |

85,465.31 |

109,681,000 |

Source: WITS

Challenges

- Stringent regulatory approvals: The ophthalmic devices market faces considerable challenges imposed by the administrative bodies for approvals and product commercialization. The authorities necessitate extensive clinical trials, safety validation, and documentation before devices can enter the market. Therefore, this results in long approval timelines and increased development costs for manufacturers. In addition, the regulatory standards keep changing across different nations, and they create complexities for global product launches. In this context, companies need to adapt to compliance requirements, quality standards, and post-market surveillance obligations. These regulatory hurdles can cause delays to innovation cycles and restrict the speed at which new technologies reach healthcare providers and patients, ultimately impacting overall ophthalmic devices market growth.

- Limited access in rural and emerging regions: Access inequality is also a major burdening factor for the ophthalmic devices market, especially in case of rural and emerging nations. Besides, advanced eye care infrastructure is often concentrated in urban centers, which leaves rural populations underserved. Apart from these high equipment costs, inadequate healthcare infrastructure and shortage of trained professionals create restrictions to accessibility. Therefore, early diagnosis and treatment of eye disorders are frequently delayed, leading to preventable vision impairment. Even when devices are available, logistical challenges such as maintenance support and supply chain constraints hinder consistent usage, thereby negatively impacting the market’s expansion.

Ophthalmic Devices Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.1% |

|

Base Year Market Size (2025) |

USD 48.8 billion |

|

Forecast Year Market Size (2035) |

USD 80.2 billion |

|

Regional Scope |

|

Ophthalmic Devices Market Segmentation:

End user Segment Analysis

Under the end user segment, hospitals & eye clinics are expected to attain the largest share of 80.5% in the ophthalmic devices market during the discussed timeframe. The segment’s dominant position is effectively propelled by the high volume of ophthalmic surgeries and diagnostic procedures performed in these facilities. In addition to the availability of advanced imaging and surgical technologies, the presence of skilled ophthalmologists, and increasing patient preference for specialized eye care services position the segment for extensive growth. In August 2024, Alcon and Aravind Eye Care System announced the launch of India’s first-ever Global Centre of Excellence for Cataract Surgery Training in Chennai. The center is equipped with Alcon’s advanced technologies, such as the CENTURION® Vision System and NGENUITY® 3D visualization system, and it will train residents in modern procedures such as phacoemulsification.

Application Segment Analysis

Cataract, which is a part of the application segment in the ophthalmic devices market, is poised to hold a considerable share by the end of 2035. The segment’s growth is largely propelled by rising global prevalence of age-related cataracts, increasing access to cataract screening and surgical services, and continuous advancements in intraocular lenses and phacoemulsification technologies. In April 2025, ZEISS Medical Technology celebrated more than 2 million digitally planned cataract cases in the U.S. using its VERACITY Surgery Planner. The company also showcased new refractive solutions, which include the VISUMAX® 800 with SMILE® pro and MEL® 90, broadening treatment options for myopia, hyperopia, and astigmatism, thus denoting a wider segment scope.

Product Segment Analysis

On the basis of product, optical coherence tomography scanners are predicted to grow with a notable revenue share in the ophthalmic devices market over the forecasted years. The segment’s growth is being fueled by the increasing adoption of non-invasive, high-resolution retinal imaging for the early detection and monitoring of retinal and optic nerve disorders. The integration of artificial intelligence into OCT platforms, rising demand for precise disease progression tracking, and the shift toward data-driven clinical decision-making are also accelerating the deployment of OCT scanners across eye care settings. In September 2025, Topcon Healthcare introduced the Triton2 multimodal Swept-Source OCT and IMAGEnet®7 to the Europe’s market at EURETINA 2025 in Paris and ESCRS 2025 in Copenhagen. The company also mentioned that Triton2 enhances clinical efficiency with high-density scans, wide-field OCT angiography, and true colour fundus imaging.

Our in-depth analysis of the ophthalmic devices market includes the following segments:

|

Segment |

Subsegments |

|

End user |

|

|

Application |

|

|

Product |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Ophthalmic Devices Market - Regional Analysis

North America Market Insights

The North America ophthalmic devices market is anticipated to garner the highest share of 42.1% during the forecast period. The region’s market benefits from technological innovation, where the rapid adoption of artificial intelligence, cloud-based telehealth networks, and advanced surgical robotics continuously transforms clinical workflows. The strong professional training infrastructure and early product approvals by regional regulatory bodies solidify the leading position in the global eye care landscape. In February 2025, the Jeffrey and Patricia Cole Pavilion at the Cleveland Clinic’s Cole Eye Institute was inaugurated as part of a USD 172 million expansion project. This new 150,000-square-foot outpatient building is linked by a three-story glass atrium to the renovated 130,000-square-foot original institute, which more than doubles the footprint of the facility, and hence, such instances heighten the demand for ophthalmic devices.

The structural migration of surgical procedures from centralized hospital networks to distributed, high-efficiency ambulatory surgical centers is responsibly boosting the overall U.S. ophthalmic devices market. The country’s market also benefits from favorable public and private healthcare insurance reimbursement modifications that incentivize these outpatient facilities, forcing a nationwide surge in the procurement of operating equipment. In November 2023, the Centers for Medicare & Medicaid Services (CMS) reported that it finalized the CY 2024 Medicare hospital outpatient prospective payment system and ambulatory surgical center payment system rule by updating payment rates by 3.1% for hospitals and ASCs meeting quality reporting requirements. This particular rule extends the hospital market basket update for ASC rates through CY 2025, allowing more data collection post-COVID-19. These policies affect about 3,500 hospitals, 6,000 ASCs, and over 7,000 licensed hospitals, thereby advancing health equity, transparency, and patient-centered care.

The Canada ophthalmic devices market has gained immense exposure owing to the strategic emphasis on provincial public health procurement programs and community-centered care initiatives. The expansion is also being propelled by federal initiatives, which are aimed at extending specialized diagnostic services to remote and indigenous communities, creating a unique demand. Based on the government data published in June 2026, Canada tabled its first-ever National Strategy for Eye Care, which was led by the health minister. The strategy aims to improve access to eye care, prevent vision loss, and strengthen supports for people who are blind or partially sighted, developed in consultation with provinces, territories, Indigenous partners, and health professionals, thus suitable for bolstering the market’s expansion.

APAC Market Insights

The Asia Pacific ophthalmic devices market is expected to progress at a rapid pace from 2026 to 2035. The region’s upliftment is mainly propelled by the acceleration of domestic manufacturing and local medical equipment industrialization, which lowers production costs and increases regional self-sufficiency. This growth is being supported by government-led healthcare subsidization programs and rural wellness missions, which are aimed at eradicating preventable blindness, prompting a public sector influx of entry-level and mid-tier diagnostic machinery. In March 2026, researchers at Tohoku University, Japan, developed a portable AI-powered slit lamp for anterior segment imaging, which was built at a material cost of under USD 500. In a clinical study of 170 participants, the device showcased excellent agreement with optical coherence tomography, consistently producing high-contrast images of ocular structures and pathologies.

The sweeping centralized government procurement policies force manufacturing efficiencies and restructure how medical devices are selected for public hospitals, thereby supporting the growth of China ophthalmic devices market. In addition, the fast-tracked implementation of digital medical networks allows secondary community health centers to connect with top-tier tier-3 metropolitan hospitals for real-time collaborative eye diagnostic reviews. In November 2024, the article published by NIH's nationwide survey covering over 13,000 hospitals found that the country had 48,652 ophthalmologists, 64,495 ophthalmic nurses, and 14,320 optometrists. This translates to densities of 1.7 ophthalmologists, 2.25 nurses, and 0.47 optometrists per 50,000 people, meeting the global average for ophthalmologists but falling short for optometrists.

In India, the ophthalmic devices market has gained immense exposure owing to the proliferation of non-profit charitable eye care models and high-volume, cost-efficient community eye hospitals that maximize equipment utilization through non-stop surgical throughput. Market growth is stimulated by the National Programme for Control of Blindness and Visual Impairment, which fosters extensive public-private partnerships to distribute basic screening tools and cataract surgical kits into deep rural pockets. As per an article published by Press Information Bureau (PIB) in June 2026 under Operation DRISHTI, the country’s Army and Air Force launched a Mega Advanced Surgical Eye Camp at Military Hospital Namkum, Ranchi, which offered 200 free advanced eye surgeries. The team also performed procedures such as phacoemulsification for cataracts, MIGS for glaucoma, and anti-VEGF injections for retinal diseases.

India Optical Devices Import by Country 2023 - Shipment Value & Volume Breakdown

|

Country |

Import Value (000 USD) |

Quantity (Items) |

|

China |

6,390.28 |

3,736,230 |

|

U.S. |

1,970.83 |

9,500 |

|

Germany |

1,302.75 |

151,160 |

|

Japan |

678.71 |

30,967 |

|

Canada |

617.22 |

1,007 |

|

New Zealand |

484.19 |

7,725 |

|

France |

213.95 |

48 |

|

Korea, Rep. |

211.35 |

104 |

|

Hong Kong, China |

167.38 |

89,603 |

Source: WITS

Europe Market Insights

The Europe ophthalmic devices market is predicted to witness considerable growth during the discussed timeframe. The region is witnessing such growth under the influence of strict regional clinical standardization frameworks and a high concentration of cross-border medical academic research clusters. The region stands as a pioneer in opting for sustainable, eco-designed surgical instruments, where hospital procurement processes favor energy-efficient laser equipment. In this context, NIH in January 2023 stated that the European Union has established a structured regulatory framework under the Medical Device Regulation (EU) 2017/745, which classifies ophthalmic AI and diagnostic software based on risk levels and requires CE marking for market approval. It also mentioned that this system enables the commercialization of AI-based ophthalmic tools, which include diagnostic and imaging software used in eye care, thus supporting their rapid integration into clinical practice across Europe.

The highly integrated cluster of precision optics manufacturers, specialized engineering institutes, and university research hospitals is uplifting the ophthalmic devices market in Germany. Market expansion is also being fueled by the country's statutory health insurance system, which rapidly incorporates innovative diagnostic methodologies into standard outpatient reimbursement catalogs. In December 2024, NIH revealed that the EyeMatics project, which is a part of Germany’s Medical Informatics Initiative 2024-2028, integrates ophthalmic data across multiple university hospitals to study real-world treatment outcomes, particularly for intravitreal injection therapies used in retinal diseases. This initiative reflects the large-scale deployment of digital health systems in ophthalmology, which enables data-driven evaluation of disease progression and treatment effectiveness in conditions.

In the UK, the ophthalmic devices market is positioned for sustained growth in the upcoming years, owing to the restructuring of the National Health Service (NHS) that shifts routine eye management to community-based clinical pathways. This transition is heavily supported by the suitable schemes, which provide fast-tracked pathways for the trial and implementation of non-invasive, high-speed automated testing equipment within high-street optometry chains. Based on the government data published in June 2026, the government announced a USD 25 million investment to digitize eye care referrals, which enables community optometrists to directly access NHS systems. This rollout will give every optical practice with an NHS contract access to the NHS e-Referral service and the National Care Records Service by 2028, reducing unnecessary hospital visits and easing GP workloads, thus heightening the demand for home-based ophthalmic devices.

Key Ophthalmic Devices Market Players:

- Alcon (Switzerland)

- Johnson & Johnson Vision (U.S.)

- Bausch + Lomb (U.S.)

- Carl Zeiss Meditec (Germany)

- EssilorLuxottica (France)

- Hoya Corporation (Japan)

- Topcon Healthcare (Japan)

- NIDEK Co., Ltd. (Japan)

- Halma plc (UK)

- Heidelberg Engineering (Germany)

- Haag-Streit Group (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Alcon positions itself as a global leader in eye care, which is focused exclusively on surgical and vision care solutions. The company has a high priority towards innovation in minimally invasive cataract surgery technologies and digital surgery platforms, allowing it to maintain a competitive position in this field.

- Johnson & Johnson Vision, which is a part of Johnson & Johnson’s MedTech segment, is focused on contact lenses and refractive surgery solutions. The company’s product portfolio includes ACUVUE® contact lenses and advanced LASIK and cataract surgery technologies.

- Bausch + Lomb is a foundational player that operates across an ophthalmic portfolio covering pharmaceuticals, surgical devices, and vision care products. The firm is highly focused on cataract and vitreoretinal surgical equipment, intraocular lenses, and a huge range of contact lenses and lens care products.

- Carl Zeiss Meditec is yet another dominant force in this sector, which is focused on ophthalmic diagnostic and surgical solutions. In addition, the company’s strategy is strongly structured on innovation, particularly in digital ophthalmology, AI-assisted diagnostics, and integrated surgical workflows.

- EssilorLuxottica has been operating as a global leader in vision care and eyewear by combining lens manufacturing with retail and brand distribution. Besides, the company deliberately integrates corrective lenses, frames, and advanced vision care solutions across a vertically integrated model.

Here is a list of key players operating in the global ophthalmic devices market:

The ophthalmic devices market hosts both multinational corporations and specialized manufacturers. Alcon, Johnson & Johnson Vision, Carl Zeiss Meditec, and EssilorLuxottica are the leading players with a focus on expanding their product portfolios across diagnostic, surgical, and vision care segments. Companies are also making R&D investments to develop advanced imaging systems, laser-based surgical equipment, and AI-enabled diagnostic tools. Mergers and acquisitions, geographic expansion in emerging markets, and partnerships with eye care providers and research institutions are being preferred by leading pioneers to secure their market positions. For instance, in July 2025, Topcon Healthcare announced the acquisition of Intelligent Retinal Imaging Systems to expand its connected care strategy across primary and eye care. The integration of IRIS’s AI-assisted diagnostics and EMR-compatible platform strengthens early detection of retinal diseases in routine clinical settings.

Corporate Landscape of the Ophthalmic Devices Market:

Recent Developments

- In April 2026, Halma plc announced the acquisition of Surgistar, Inc., which is a maker of surgical instruments, as a bolt-on for its healthcare sector company MicroSurgical Technology. The move strengthens MST’s capabilities in cataract and ophthalmic surgery, adding complementary products and enhancing in-house manufacturing.

- In March 2026, ZEISS Vision Care acquired key assets of Vivior AG to strengthen its capabilities in personalized eye care. Vivior’s experience in monitoring and analyzing visual behavior will help ZEISS deliver hyper-personalized lens solutions and support proactive eye health management.

- Report ID: 8623

- Published Date: Jun 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.