Global Next-Generation Biometric Authentication Market

- An Outline of the Global Next-Generation Biometric Authentication Market

- Market Definition and Segmentation

- Study Assumptions and Abbreviations

- Research Methodology & Approach

- Primary Research

- Secondary Research

- Data Triangulation

- SPSS Methodology

- Executive Summary

- Growth Drivers

- Major Roadblocks

- Opportunities

- Prevalent Trends

- Government Regulation

- Growth Outlook

- Competitive White Space Analysis – Identifying Untapped Market Gaps

- Risk Overview

- SWOT

- Technological Advancement

- Technology Maturity Matrix for Next-Generation Biometric Authentication Market Recent News

- Regional Demand

- Global Next-Generation Biometric Authentication by Geography – Strategic Comparative Analysis

- Strategic Segment Analysis: Next-Generation Biometric Authentication Demand Landscape

- Next-Generation Biometric Authentication Demand Trends Driven by national security needs, fraud prevention in finance, healthcare demands from aging populations, rising consumer acceptance, and regulatory frameworks that emphasize privacy and responsible use (2026-2036)

- Root Cause Analysis (RCA) for discovering problems of the Next-Generation Biometric Authentication Market

- Porter Five Forces

- PESTLE

- Comparative Positioning

- Global Next-Generation Biometric Authentication – Key Player Analysis (2036)

- Competitive Landscape: Key Suppliers/Players

- Competitive Model: A Detailed Inside View for Investors

- Company Market Share, 2036 (%)

- Amazon Web Services, Inc.

- Fingerprint Cards AB

- Fujitsu

- HID Global Corporation, part of ASSA ABLOY

- Hitachi, Ltd.

- IDEMIA

- Microsoft

- NEC Corporation

- Suprema Inc.

- Synaptics Incorporated

- Thales

- Global Next-Generation Biometric Authentication Market Outlook

- Market Overview

- Market Revenue by Value (USD Million), Volume (Million Tons), and Compound Annual Growth Rate (CAGR)

- Next-Generation Biometric Authentication Market Segmentation Analysis (2026-2036)

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Sensors, Market Value (USD Million), and CAGR, 2026-2036F

- Cameras, Market Value (USD Million), and CAGR, 2026-2036F

- Readers & Scanners, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- On-device SDKs, Market Value (USD Million), and CAGR, 2026-2036F

- Server/Cloud, Market Value (USD Million), and CAGR, 2026-2036F

- Analytics & AI/ML, Market Value (USD Million), and CAGR, 2026-2036F

- Services, Market Value (USD Million), and CAGR, 2026-2036F

- System Integration, Market Value (USD Million), and CAGR, 2026-2036F

- Managed/Hosted, Market Value (USD Million), and CAGR, 2026-2036F

- Consulting & Testing, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Fingerprint, Market Value (USD Million), and CAGR, 2026-2036F

- Facial, Market Value (USD Million), and CAGR, 2026-2036F

- Iris, Market Value (USD Million), and CAGR, 2026-2036F

- Palm & Vein, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Behavioral & Soft Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Voice, Market Value (USD Million), and CAGR, 2026-2036F

- Signature & Keystroke, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Access Control & Physical Security, Market Value (USD Million), and CAGR, 2026- 2036F

- Logical Access & Digital Identity, Market Value (USD Million), and CAGR, 2026- 2036F

- Payments & Financial Transactions, Market Value (USD Million), and CAGR, 2026- 2036F

- Workforce / Enterprise IAM, Market Value (USD Million), and CAGR, 2026- 2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026- 2036F

- Travel & Immigration, Market Value (USD Million), and CAGR, 2026- 2036F

- Consumer Electronics & IoT, Market Value (USD Million), and CAGR, 2026- 2036F

- Law Enforcement & Public Safety, Market Value (USD Million), and CAGR, 2026- 2036F

- Others, Market Value (USD Million), and CAGR, 2026- 2036F

- By Authentication Type

- Single-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- Multi-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- By End user Vertical

- Government & Public Sector, Market Value (USD Million), and CAGR, 2026-2036F

- BFSI, Market Value (USD Million), and CAGR, 2026-2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026-2036F

- Education, Market Value (USD Million), and CAGR, 2026-2036F

- Logistics, Market Value (USD Million), and CAGR, 2026-2036F

- Retail, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Mode

- On-Premise, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud-Based/SaaS, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- Regional Synopsis, Value (USD Million), 2026-2036

- North America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Asia Pacific Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Middle East and Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- By Component

- Market Overview

- North America Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036, By

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Sensors, Market Value (USD Million), and CAGR, 2026-2036F

- Cameras, Market Value (USD Million), and CAGR, 2026-2036F

- Readers & Scanners, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- On-device SDKs, Market Value (USD Million), and CAGR, 2026-2036F

- Server/Cloud, Market Value (USD Million), and CAGR, 2026-2036F

- Analytics & AI/ML, Market Value (USD Million), and CAGR, 2026-2036F

- Services, Market Value (USD Million), and CAGR, 2026-2036F

- System Integration, Market Value (USD Million), and CAGR, 2026-2036F

- Managed/Hosted, Market Value (USD Million), and CAGR, 2026-2036F

- Consulting & Testing, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Fingerprint, Market Value (USD Million), and CAGR, 2026-2036F

- Facial, Market Value (USD Million), and CAGR, 2026-2036F

- Iris, Market Value (USD Million), and CAGR, 2026-2036F

- Palm & Vein, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Behavioral & Soft Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Voice, Market Value (USD Million), and CAGR, 2026-2036F

- Signature & Keystroke, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Access Control & Physical Security, Market Value (USD Million), and CAGR, 2026- 2036F

- Logical Access & Digital Identity, Market Value (USD Million), and CAGR, 2026- 2036F

- Payments & Financial Transactions, Market Value (USD Million), and CAGR, 2026- 2036F

- Workforce / Enterprise IAM, Market Value (USD Million), and CAGR, 2026- 2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026- 2036F

- Travel & Immigration, Market Value (USD Million), and CAGR, 2026- 2036F

- Consumer Electronics & IoT, Market Value (USD Million), and CAGR, 2026- 2036F

- Law Enforcement & Public Safety, Market Value (USD Million), and CAGR, 2026- 2036F

- Others, Market Value (USD Million), and CAGR, 2026- 2036F

- By Authentication Type

- Single-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- Multi-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- By End user Vertical

- Government & Public Sector, Market Value (USD Million), and CAGR, 2026-2036F

- BFSI, Market Value (USD Million), and CAGR, 2026-2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026-2036F

- Education, Market Value (USD Million), and CAGR, 2026-2036F

- Logistics, Market Value (USD Million), and CAGR, 2026-2036F

- Retail, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Mode

- On-Premise, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud-Based/SaaS, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- S. Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Canada Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- By Component

- Overview

- Europe Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036, By

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Sensors, Market Value (USD Million), and CAGR, 2026-2036F

- Cameras, Market Value (USD Million), and CAGR, 2026-2036F

- Readers & Scanners, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- On-device SDKs, Market Value (USD Million), and CAGR, 2026-2036F

- Server/Cloud, Market Value (USD Million), and CAGR, 2026-2036F

- Analytics & AI/ML, Market Value (USD Million), and CAGR, 2026-2036F

- Services, Market Value (USD Million), and CAGR, 2026-2036F

- System Integration, Market Value (USD Million), and CAGR, 2026-2036F

- Managed/Hosted, Market Value (USD Million), and CAGR, 2026-2036F

- Consulting & Testing, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Fingerprint, Market Value (USD Million), and CAGR, 2026-2036F

- Facial, Market Value (USD Million), and CAGR, 2026-2036F

- Iris, Market Value (USD Million), and CAGR, 2026-2036F

- Palm & Vein, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Behavioral & Soft Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Voice, Market Value (USD Million), and CAGR, 2026-2036F

- Signature & Keystroke, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Access Control & Physical Security, Market Value (USD Million), and CAGR, 2026- 2036F

- Logical Access & Digital Identity, Market Value (USD Million), and CAGR, 2026- 2036F

- Payments & Financial Transactions, Market Value (USD Million), and CAGR, 2026- 2036F

- Workforce / Enterprise IAM, Market Value (USD Million), and CAGR, 2026- 2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026- 2036F

- Travel & Immigration, Market Value (USD Million), and CAGR, 2026- 2036F

- Consumer Electronics & IoT, Market Value (USD Million), and CAGR, 2026- 2036F

- Law Enforcement & Public Safety, Market Value (USD Million), and CAGR, 2026- 2036F

- Others, Market Value (USD Million), and CAGR, 2026- 2036F

- By Authentication Type

- Single-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- Multi-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- By End user Vertical

- Government & Public Sector, Market Value (USD Million), and CAGR, 2026-2036F

- BFSI, Market Value (USD Million), and CAGR, 2026-2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026-2036F

- Education, Market Value (USD Million), and CAGR, 2026-2036F

- Logistics, Market Value (USD Million), and CAGR, 2026-2036F

- Retail, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Mode

- On-Premise, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud-Based/SaaS, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- UK Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Germany Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- France Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Italy Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Spain Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Netherlands Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Russia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Switzerland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Poland Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Belgium Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Europe Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- By Component

- Overview

- Asia Pacific, Excluding Japan Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Segmentation (USD Million), 2026-2036, By

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Sensors, Market Value (USD Million), and CAGR, 2026-2036F

- Cameras, Market Value (USD Million), and CAGR, 2026-2036F

- Readers & Scanners, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- On-device SDKs, Market Value (USD Million), and CAGR, 2026-2036F

- Server/Cloud, Market Value (USD Million), and CAGR, 2026-2036F

- Analytics & AI/ML, Market Value (USD Million), and CAGR, 2026-2036F

- Services, Market Value (USD Million), and CAGR, 2026-2036F

- System Integration, Market Value (USD Million), and CAGR, 2026-2036F

- Managed/Hosted, Market Value (USD Million), and CAGR, 2026-2036F

- Consulting & Testing, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Fingerprint, Market Value (USD Million), and CAGR, 2026-2036F

- Facial, Market Value (USD Million), and CAGR, 2026-2036F

- Iris, Market Value (USD Million), and CAGR, 2026-2036F

- Palm & Vein, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Behavioral & Soft Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Voice, Market Value (USD Million), and CAGR, 2026-2036F

- Signature & Keystroke, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Access Control & Physical Security, Market Value (USD Million), and CAGR, 2026- 2036F

- Logical Access & Digital Identity, Market Value (USD Million), and CAGR, 2026- 2036F

- Payments & Financial Transactions, Market Value (USD Million), and CAGR, 2026- 2036F

- Workforce / Enterprise IAM, Market Value (USD Million), and CAGR, 2026- 2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026- 2036F

- Travel & Immigration, Market Value (USD Million), and CAGR, 2026- 2036F

- Consumer Electronics & IoT, Market Value (USD Million), and CAGR, 2026- 2036F

- Law Enforcement & Public Safety, Market Value (USD Million), and CAGR, 2026- 2036F

- Others, Market Value (USD Million), and CAGR, 2026- 2036F

- By Authentication Type

- Single-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- Multi-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- By End user Vertical

- Government & Public Sector, Market Value (USD Million), and CAGR, 2026-2036F

- BFSI, Market Value (USD Million), and CAGR, 2026-2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026-2036F

- Education, Market Value (USD Million), and CAGR, 2026-2036F

- Logistics, Market Value (USD Million), and CAGR, 2026-2036F

- Retail, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Mode

- On-Premise, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud-Based/SaaS, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- China Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Japan Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- India Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Korea Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Australia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Indonesia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Malaysia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Vietnam Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Thailand Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Singapore Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- New Zealand Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Asia Pacific Excluding Japan Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- By Component

- Overview

- Latin America Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

- Segmentation (USD Million), 2026-2036, By

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Sensors, Market Value (USD Million), and CAGR, 2026-2036F

- Cameras, Market Value (USD Million), and CAGR, 2026-2036F

- Readers & Scanners, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- On-device SDKs, Market Value (USD Million), and CAGR, 2026-2036F

- Server/Cloud, Market Value (USD Million), and CAGR, 2026-2036F

- Analytics & AI/ML, Market Value (USD Million), and CAGR, 2026-2036F

- Services, Market Value (USD Million), and CAGR, 2026-2036F

- System Integration, Market Value (USD Million), and CAGR, 2026-2036F

- Managed/Hosted, Market Value (USD Million), and CAGR, 2026-2036F

- Consulting & Testing, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Fingerprint, Market Value (USD Million), and CAGR, 2026-2036F

- Facial, Market Value (USD Million), and CAGR, 2026-2036F

- Iris, Market Value (USD Million), and CAGR, 2026-2036F

- Palm & Vein, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Behavioral & Soft Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Voice, Market Value (USD Million), and CAGR, 2026-2036F

- Signature & Keystroke, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Access Control & Physical Security, Market Value (USD Million), and CAGR, 2026- 2036F

- Logical Access & Digital Identity, Market Value (USD Million), and CAGR, 2026- 2036F

- Payments & Financial Transactions, Market Value (USD Million), and CAGR, 2026- 2036F

- Workforce / Enterprise IAM, Market Value (USD Million), and CAGR, 2026- 2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026- 2036F

- Travel & Immigration, Market Value (USD Million), and CAGR, 2026- 2036F

- Consumer Electronics & IoT, Market Value (USD Million), and CAGR, 2026- 2036F

- Law Enforcement & Public Safety, Market Value (USD Million), and CAGR, 2026- 2036F

- Others, Market Value (USD Million), and CAGR, 2026- 2036F

- By Authentication Type

- Single-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- Multi-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- By End user Vertical

- Government & Public Sector, Market Value (USD Million), and CAGR, 2026-2036F

- BFSI, Market Value (USD Million), and CAGR, 2026-2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026-2036F

- Education, Market Value (USD Million), and CAGR, 2026-2036F

- Logistics, Market Value (USD Million), and CAGR, 2026-2036F

- Retail, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Mode

- On-Premise, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud-Based/SaaS, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- Brazil Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Argentina Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Mexico Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Latin America Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- By Component

- Overview

- Middle East & Africa Market

- Overview

- Market Value (USD Million), Current and Future Projections, 2026-2036

- Increment $ Opportunity Assessment, 2026-2036

- Year-on-Year Growth Forecast (%)

- Segmentation (USD Million), 2026-2036, By

- By Component

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- Sensors, Market Value (USD Million), and CAGR, 2026-2036F

- Cameras, Market Value (USD Million), and CAGR, 2026-2036F

- Readers & Scanners, Market Value (USD Million), and CAGR, 2026-2036F

- Software, Market Value (USD Million), and CAGR, 2026-2036F

- On-device SDKs, Market Value (USD Million), and CAGR, 2026-2036F

- Server/Cloud, Market Value (USD Million), and CAGR, 2026-2036F

- Analytics & AI/ML, Market Value (USD Million), and CAGR, 2026-2036F

- Services, Market Value (USD Million), and CAGR, 2026-2036F

- System Integration, Market Value (USD Million), and CAGR, 2026-2036F

- Managed/Hosted, Market Value (USD Million), and CAGR, 2026-2036F

- Consulting & Testing, Market Value (USD Million), and CAGR, 2026-2036F

- By Technology

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Fingerprint, Market Value (USD Million), and CAGR, 2026-2036F

- Facial, Market Value (USD Million), and CAGR, 2026-2036F

- Iris, Market Value (USD Million), and CAGR, 2026-2036F

- Palm & Vein, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- Behavioral & Soft Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Voice, Market Value (USD Million), and CAGR, 2026-2036F

- Signature & Keystroke, Market Value (USD Million), and CAGR, 2026-2036F

- Others, Market Value (USD Million), and CAGR, 2026-2036F

- By Application

- Access Control & Physical Security, Market Value (USD Million), and CAGR, 2026- 2036F

- Logical Access & Digital Identity, Market Value (USD Million), and CAGR, 2026- 2036F

- Payments & Financial Transactions, Market Value (USD Million), and CAGR, 2026- 2036F

- Workforce / Enterprise IAM, Market Value (USD Million), and CAGR, 2026- 2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026- 2036F

- Travel & Immigration, Market Value (USD Million), and CAGR, 2026- 2036F

- Consumer Electronics & IoT, Market Value (USD Million), and CAGR, 2026- 2036F

- Law Enforcement & Public Safety, Market Value (USD Million), and CAGR, 2026- 2036F

- Others, Market Value (USD Million), and CAGR, 2026- 2036F

- By Authentication Type

- Single-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- Multi-Factor, Market Value (USD Million), and CAGR, 2026- 2036F

- By End user Vertical

- Government & Public Sector, Market Value (USD Million), and CAGR, 2026-2036F

- BFSI, Market Value (USD Million), and CAGR, 2026-2036F

- Healthcare & Life Sciences, Market Value (USD Million), and CAGR, 2026-2036F

- Education, Market Value (USD Million), and CAGR, 2026-2036F

- Logistics, Market Value (USD Million), and CAGR, 2026-2036F

- Retail, Market Value (USD Million), and CAGR, 2026-2036F

- By Deployment Mode

- On-Premise, Market Value (USD Million), and CAGR, 2026-2036F

- Cloud-Based/SaaS, Market Value (USD Million), and CAGR, 2026-2036F

- Hybrid, Market Value (USD Million), and CAGR, 2026-2036F

- Country Level Analysis, Value (USD Million)

- Saudi Arabia Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- UAE Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Israel Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Qatar Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Kuwait Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Oman Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- South Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Rest of Middle East & Africa Market Value (USD Million) and CAGR & Y-o-Y Growth Trend, 2026-2036F

- Physiological Biometrics, Market Value (USD Million), and CAGR, 2026- 2036F

- Hardware, Market Value (USD Million), and CAGR, 2026-2036F

- By Component

- Overview

- Global Economic Scenario

- World Economic Outlook

- About Research Nester

- Our Global Clientele

- We Serve Clients Across World

Next-Generation Biometric Authentication Market Outlook:

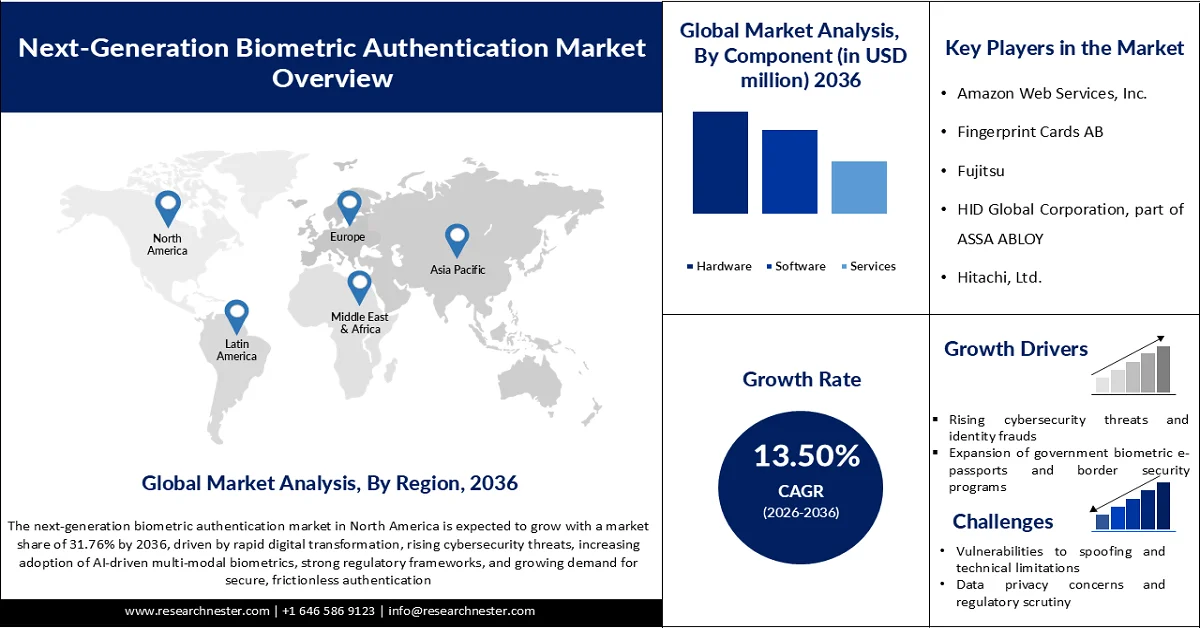

Next-Generation Biometric Authentication Market is valued at USD 65.34 billion in 2025 and is projected to reach USD 287.04 billion by 2036, growing at a CAGR of 13.50% during the forecast period, i.e., 2026-2036. In 2026, the industry size of next-generation biometric authentication is evaluated at USD 80.90 billion.

The global next-generation biometric authentication market is witnessing strong growth, driven primarily by the need for highly secure, scalable, and user-friendly identity verification systems across digital and physical platforms. A key growth factor is the increasing use of biometrics in government-led identity and border security programs, which is accelerating large-scale adoption worldwide. According to a 2025 report by the U.S. Department of Homeland Security, its biometric system stores over 320 million unique identities and processes more than 400,000 biometric transactions per day, demonstrating the massive scale and operational reliance on biometric authentication. Additionally, government-backed infrastructure and interoperability efforts, supported by organizations such as the National Institute of Standards and Technology, are enhancing accuracy, standardization, and cross-agency data sharing, thereby further boosting adoption. The next-generation biometric authentication market is also benefiting from rising cyber threats and the shift toward passwordless authentication, particularly in sectors such as banking, healthcare, and travel. Advances in AI-driven facial recognition, multimodal biometrics, and cloud-based identity platforms are improving both security and user experience. Overall, strong government investment, proven scalability, and increasing digital transformation are positioning biometric authentication as a foundational component of next-generation identity ecosystems globally.

Key Next-Generation Biometric Authentication Market Insights Summary:

Regional Insights:

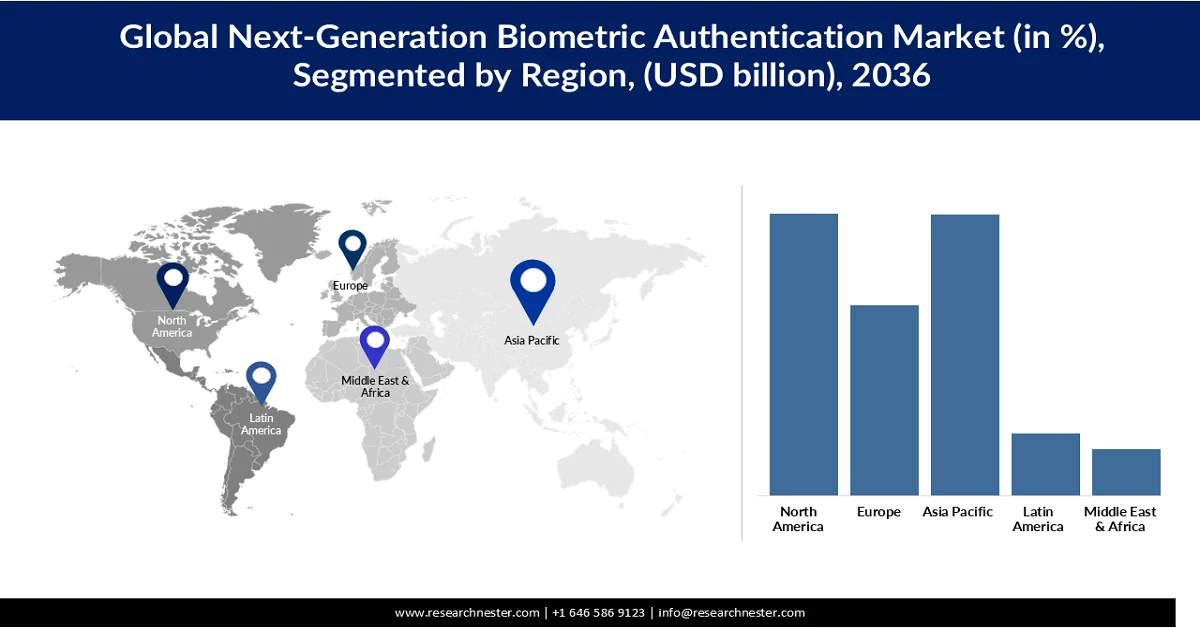

- The North America next-generation biometric authentication market is projected to capture a 31.76% share by 2036, fueled by rapid digital transformation, rising cybersecurity threats, and increasing adoption of AI-driven multi-modal biometrics

- Asia Pacific is anticipated to witness notable expansion in the forecast period 2026-2036, stimulated by large-scale digital transformation and rising demand for secure authentication across mobile payments, banking, and government services

Segment Insights:

- In the next-generation biometric authentication market, the hardware segment is expected to account for a 42.58% share by 2036, propelled by its critical function in capturing and processing physical identity traits such as fingerprints, facial features, and iris patterns

- The physiological biometrics segment is forecasted to dominate with a 73.3% share by 2036, impelled by its high accuracy and widespread adoption across government identification systems

Key Growth Trends:

- Rising cybersecurity threats and identity fraud

- Expansion of government biometric e–passports and border security programs

Major Challenges:

- Vulnerabilities to spoofing and technical limitations

- Data privacy concerns and regulatory scrutiny

Key Players: Amazon Web Services, Inc. (U.S.), Fingerprint Cards AB (Sweden), Fujitsu (Japan), HID Global Corporation, part of ASSA ABLOY (U.S.), Hitachi, Ltd. (Japan), IDEMIA (France), Microsoft (U.S.), NEC Corporation (Japan), Suprema Inc. (South Korea), Synaptics Incorporated (U.S.), Thales (France).

Global Next-Generation Biometric Authentication Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 65.34 billion

- 2026 Market Size: USD 80.90 billion

- Projected Market Size: USD 287.04 billion by 2036

- Growth Forecasts:13.50% CAGR (2026-2036)

Key Regional Dynamics:

- Largest Region: North America (31.76% Share by 2036)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, United Kingdom, Japan

- Emerging Countries: India, South Korea, Singapore, Brazil, Indonesia

Last updated on : 24 April, 2026

Next-Generation Biometric Authentication Market - Growth Drivers and Challenges

Growth Drivers

- Rising cybersecurity threats and identity fraud: The rapid digitization of financial, healthcare, and government services has significantly increased exposure to cyber threats and identity fraud. According to the 2021 U.S. Bureau of Justice Statistics, approximately 23.9 million people (9% of U.S. residents aged 16 and older) experienced identity theft in a single year, underscoring the magnitude of the issue. The FBI reports that identity misuse often involves bank fraud, credit card fraud, and tax-related scams, making personal data highly valuable to criminals. Increasing data breaches and phishing attacks are primary methods used to steal sensitive information. Cybercriminals also use stolen identities for account takeover and financial fraud. Growing dependence on digital platforms has expanded the attack surface, increasing vulnerability. As a result, demand for advanced cybersecurity and identity verification systems is rising rapidly.

- Expansion of government biometric e–passports and border security programs: Governments worldwide are increasingly adopting biometric-enabled identity systems to enhance border security and reduce fraud in travel documents. The U.S. National Institute of Standards and Technology (NIST) has highlighted that biometric systems such as fingerprint recognition significantly improve identity verification accuracy in passport and border control applications. Biometric e-passports store encrypted facial and fingerprint data, allowing automated verification at immigration checkpoints. This reduces dependence on manual document checks and lowers the risk of forgery or impersonation. Government agencies also integrate these systems with international security databases to flag suspicious travelers. Rising global travel volumes and security threats are accelerating adoption. These initiatives strengthen national security while improving efficiency at borders.

- Integration with financial services and digital payments ecosystems: The integration of identity verification systems with financial services is accelerating due to the rapid growth of digital payments and online banking. The FBI’s Internet Crime Complaint Center (IC3) reports that cyber-enabled fraud causes billions in annual losses, with identity-related crimes forming a major component of financial fraud cases. Financial institutions now rely heavily on digital identity verification to prevent account takeover, loan fraud, and unauthorized transactions. Government-backed identity systems and authentication frameworks help reduce fraud risks in digital onboarding processes. As cashless transactions expand, secure identity verification becomes essential for trust in financial ecosystems. Regulatory bodies also encourage stronger customer authentication standards. This convergence is driving widespread adoption of biometric and digital identity solutions in fintech.

Challenges

- Vulnerabilities to spoofing and technical limitations: Biometric and digital identity systems face significant restraints due to spoofing attacks and technical limitations. Attackers can sometimes bypass systems using fake fingerprints, facial masks, or high-resolution images, reducing overall reliability. According to the U.S. National Institute of Standards and Technology, even advanced facial recognition systems can show performance variations depending on lighting, camera quality, and user conditions such as aging or injuries. These inconsistencies create false acceptance or rejection errors, impacting trust in authentication systems. Additionally, large-scale deployment challenges, such as hardware dependency and integration complexity, further limit seamless adoption. As a result, continuous upgrades and anti-spoofing technologies are required to maintain system accuracy and security.

- Data privacy concerns and regulatory scrutiny: The use of biometric and identity data raises serious privacy concerns, as such information is highly sensitive and irreversible if compromised. Governments and regulatory bodies have increased scrutiny on how organizations collect, store, and process biometric data. The U.S. Government Accountability Office (GAO) has emphasized the need for strong safeguards to prevent unauthorized access and misuse of personal identity information in federal systems. Public concern over surveillance and data tracking also limits widespread acceptance of biometric solutions. Strict regulations, such as data minimization requirements and consent frameworks, add compliance burdens for companies. Additionally, cross-border data sharing restrictions complicate global deployment. These factors collectively slow down adoption despite growing demand for secure identity solutions.

Next-Generation Biometric Authentication Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2036 |

|

CAGR |

13.50% |

|

Base Year Market Size (2025) |

USD 65.34 billion |

|

Forecast Year Market Size (2036) |

USD 287.04 billion |

|

Regional Scope |

|

Next-Generation Biometric Authentication Market Segmentation:

Component Segment Analysis

The hardware segment is expected to hold a share of 42.58% by 2036, due to its critical function in capturing and processing physical identity traits such as fingerprints, facial features, and iris patterns. According to NIST, fingerprint and face recognition systems are widely deployed across federal agencies, including DHS, FBI, and the Department of State, for identity verification and border security applications, requiring large-scale biometric sensors and scanners for data capture and processing at entry points and security systems. NIST also highlights that biometric systems are essential for securing facilities, screening individuals at borders, and preventing fraud, all of which rely heavily on dedicated hardware infrastructure such as fingerprint scanners, cameras, and iris recognition devices. The expansion of government identity programs like PIV (Personal Identity Verification) mandates the use of physical biometric capture devices for authentication and access control in federal systems. Hardware accuracy improvements have also strengthened adoption, as multi-finger and high-resolution scanning significantly enhance identification reliability in large databases. Additionally, the increasing deployment of biometric-enabled border control systems and e-passports is further boosting demand for robust sensing and imaging devices. Overall, hardware remains the backbone of biometric authentication because it enables real-time, high-precision identity capture required for secure government and commercial applications.

Technology Segment Analysis

The physiological biometrics segment is expected to hold a share of 73.3% by 2036. Physiological biometrics, such as fingerprint, facial, and iris recognition, drive strong segment growth due to their accuracy and widespread U.S. government adoption. According to a 2020 report published by Incubator for Media Education and Development (IMEDD), top facial recognition algorithms achieved false match rates below 0.1% under controlled conditions. The Department of Homeland Security noted in 2023 that its biometric systems handle hundreds of millions of identity transactions annually, reflecting large-scale deployment. Additionally, the Federal Bureau of Investigation stated in 2021 that its Next Generation Identification System, or NGI, contains over 161 million fingerprint records. This proven reliability and extensive institutional use continue to accelerate growth in the physiological biometrics segment.

Application Segment Analysis

The local access & digital identity segment is a major driver of application growth, as governments and enterprises increasingly deploy biometrics for secure authentication and identity verification. Agencies like the NIST have emphasized passwordless authentication frameworks that rely on biometric credentials, accelerating adoption in both public and private systems. Additionally, the Department of Homeland Security uses biometric-based digital identity platforms for border control and access management, processing large volumes of identity verifications annually. The Social Security Administration and other agencies are also expanding secure digital identity services, reinforcing demand for reliable authentication. This widespread institutional use drives continuous growth in local access control and digital identity applications.

Our in-depth analysis of the next-generation biometric authentication market includes the following segments:

|

Segments |

Subsegments |

|

Component |

|

|

Technology |

|

|

Application |

|

|

Authentic Type |

|

|

End user Vertical |

|

|

Deployment Mode |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Next-Generation Biometric Authentication Market - Regional Analysis

North America Market Insights

The North America next-generation biometric authentication market is expected to hold the largest market share of 31.76% by 2036, driven by rapid digital transformation, rising cybersecurity threats, increasing adoption of AI-driven multi-modal biometrics, strong regulatory frameworks, and growing demand for secure, frictionless authentication. Agencies such as the Department of Homeland Security and the Federal Bureau of Investigation continue to scale biometric databases and authentication systems, driving widespread adoption across border security, law enforcement, and public services. At the same time, enterprise demand is rising due to increasing cybersecurity threats and the shift toward passwordless authentication frameworks guided by the NIST, further accelerating regional next-generation biometric authentication market growth.

The U.S. is seeing rapid expansion in next-generation biometric authentication market, driven by federal adoption and private sector demand. The Department of Homeland Security (DHS) reports that biometrics are now central to identity verification programs, with fingerprints and facial recognition used across immigration, border security, and law enforcement. Consumer acceptance is also strong: surveys show 67% of locals are already comfortable using biometrics, and 87% expect to be comfortable soon. States such as Illinois, Texas, and Washington have enacted biometric privacy laws, while California and Virginia include biometric provisions in broader consumer privacy legislation. Litigation under the Biometric Information Privacy Act (BIPA) has surged, reflecting both the growth of the industry and heightened compliance risks. Together, these trends indicate a U.S. next-generation biometric authentication market that is expanding rapidly, but under close regulatory scrutiny to balance innovation with privacy.

In Canada, the biometrics market is expanding steadily due to government-led digital identity and immigration programs. The Immigration, Refugees and Citizenship Canada reported that between 2020 and 2023, it collected millions of biometric records annually (fingerprints and photos) as part of visa and permit processing, reflecting sustained post-pandemic recovery and adoption. The Canada Border Services Agency has also increased the use of biometric verification at ports of entry since 2021, strengthening border security and traveler identification. Additionally, Canada continues biometric data-sharing initiatives with the Department of Homeland Security under updated agreements to enhance cross-border screening. These post-2020 expansions in enrolment volumes and operational use are driving consistent growth in biometric applications across the country.

Asia Pacific Market Insights

The Asia Pacific next-generation biometric authentication market is witnessing rapid growth in the biometrics market due to large-scale digital transformation and rising demand for secure authentication across mobile payments, banking, and government services. Countries such as China, India, Japan, and Southeast Asian economies are increasingly integrating fingerprint and facial recognition into digital identity and e-governance systems, strengthening adoption across both public and private sectors. The expansion of smartphone penetration and digital wallets is further accelerating the usage of biometric authentication in everyday transactions. Additionally, regulatory pushes for stronger cybersecurity and identity verification frameworks are encouraging organizations to replace traditional password-based systems with biometric solutions.

China has built one of the world’s largest biometric ecosystems, with hundreds of millions of facial recognition-enabled cameras deployed nationwide for public security and surveillance. The Cyberspace Administration of China has introduced draft rules to regulate biometric data use, but public security organs retain broad powers to collect fingerprints, iris scans, gait, and DNA data, creating the world’s largest police-run DNA database. While this scale demonstrates rapid adoption, organizations like the Biometrics Institute caution that China’s expansion raises privacy and ethical concerns, particularly around mass surveillance and data storage. Nonetheless, China continues to lead globally in AI-powered biometric systems, embedding them into everyday life from transportation hubs to e-government services, making biometrics a cornerstone of its digital identity ecosystem.

Japan’s next-generation biometric authentication market is growing steadily, driven by government modernization and demographic realities. Japan’s Ministry of Justice has introduced the Japan Electronic Travel Authorization (JESTA) system, which will apply to travelers from visa-exempt countries to strengthen pre-arrival screening and identity verification. In 2025, Japan recorded over 39 million international visitors, with a significant proportion entering under visa-free arrangements, underscoring the need for streamlined, secure authentication systems.

Moreover, Japan’s aging population is a key driver for next-generation biometric authentication market adoption, particularly in healthcare and eldercare services. According to the Cabinet Office Japan’s Annual Report on the Aging Society FY2024, the population aged 65 and over reached 36.23 million in 2023, and projections indicate that by 2070, roughly one in every 2.6 people will be aged 65+, while one in four will be 75 or older. This demographic shift is accelerating demand for secure, easy-to-use authentication methods that reduce reliance on passwords and physical documentation. Biometrics enables seamless patient identification, remote care access, and automated service delivery in elderly care environments. Additionally, the Biometrics Institute emphasizes Japan’s strong focus on transparency and accountability in biometric deployment. This combination of demographic need and responsible governance is positioning Japan as a leader in advanced and ethical biometric adoption.

Europe Market Insights

The next-generation biometric authentication market in Europe is growing steadily, driven by strong regulatory frameworks and the integration of biometrics into unified digital identity systems. Initiatives such as the EU Digital Identity Wallet and updated eIDAS 2.0 regulation are enabling secure cross-border authentication using facial and fingerprint recognition across member states. Airports, border control systems, and public services are increasingly adopting contactless biometric technologies to improve security and operational efficiency. At the same time, strict data privacy laws like GDPR are shaping the next-generation biometric authentication market toward secure, consent-based, and privacy-preserving biometric solutions. This balance of regulation and innovation is steadily expanding biometrics adoption across both government and enterprise applications.

Germany is steadily advancing next-generation biometric authentication market as part of its national digitalization strategy. The Federal Ministry of the Interior and Community (BMI) has integrated biometrics into national ID cards and residence permits, requiring fingerprints and facial images for secure identity verification. Facial recognition is also being piloted in airports and train stations to streamline passenger flows, while law enforcement agencies use biometrics for forensic investigations. The OECD highlights that Germany’s demographic challenges, particularly an aging population, are accelerating adoption in healthcare and eldercare, where secure identity verification is critical.

At the same time, Germany is aligning with the EU AI Act, which places restrictions on high-risk biometric applications such as emotion detection. The Biometrics Institute stresses the importance of transparency and accountability in biometric deployment, warning against over-reliance on surveillance technologies. This dual emphasis on innovation and regulation positions Germany as a leader in responsible biometric adoption, balancing technological progress with privacy protections.

The UK is also seeing strong growth in next-generation biometric authentication market, particularly in border security, policing, and financial services. The UK Home Office has expanded biometric use in immigration and asylum processes, requiring fingerprints and facial images for visa applicants and asylum seekers. Airports across the UK have adopted biometric e-gates, with millions of passengers using facial recognition to speed up entry. The Biometrics and Surveillance Camera Commissioner emphasizes the need for ethical oversight, ensuring biometrics are deployed responsibly and in line with public trust. Nonprofit organizations such as the Biometrics Institute report that facial recognition remains the dominant modality, but behavioral biometrics are increasingly used in banking to combat fraud. The Identity Management Institute notes that public acceptance is high, with a majority of UK citizens expressing comfort with biometric use. This combination of government-led adoption, consumer readiness, and nonprofit oversight is driving steady growth while ensuring that privacy and accountability remain central to the UK’s biometric strategy.

Key Next-Generation Biometric Authentication Market Players:

- Amazon Web Services, Inc. (U.S.)

- Fingerprint Cards AB (Sweden)

- Fujitsu (Japan)

- HID Global Corporation, part of ASSA ABLOY (U.S.)

- Hitachi, Ltd. (Japan)

- IDEMIA (France)

- Microsoft (U.S.)

- NEC Corporation (Japan)

- Suprema Inc. (South Korea)

- Synaptics Incorporated (U.S.)

- Thales (France)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- NEC is a global leader in AI-driven facial recognition and multimodal biometric systems used in border control, law enforcement, and smart city projects. Its advanced algorithms consistently rank among the most accurate in global benchmarks, driving large-scale government adoption. The company focuses on integrating biometrics with digital identity platforms for seamless authentication. NEC’s solutions are widely deployed across airports, public safety systems, and national ID programs.

- Thales plays a major role in secure digital identity and biometric authentication for governments and enterprises worldwide. It provides solutions for e-passports, national IDs, and border management systems using facial and fingerprint recognition. The company is also advancing cloud-based biometric authentication and cybersecurity integration. Its strong presence in defense and aviation further strengthens biometric adoption in high-security environments.

- IDEMIA specializes in augmented identity solutions, combining biometrics with AI and cryptography for secure authentication. It is a key provider of biometric systems for passports, driver’s licenses, and financial services. The company focuses on contactless and mobile-based biometric verification to enhance user convenience. IDEMIA’s technologies are widely used in both public sector identity programs and private sector applications.

- Microsoft is driving next-generation biometric authentication market through its passwordless ecosystem, including Windows Hello facial and fingerprint recognition. The company integrates biometrics with cloud identity platforms like Azure Active Directory for enterprise security. Its focus on zero-trust architecture and seamless authentication is accelerating adoption across organizations. Microsoft’s solutions are widely used in enterprise IT environments and consumer devices.

- Synaptics is a key player in biometric hardware, particularly fingerprint sensors and AI-enabled edge processing solutions. Its technologies are embedded in smartphones, laptops, and IoT devices, enabling secure and fast authentication. The company is advancing under-display and touchless biometric solutions to support next-generation user interfaces. Synaptics’ innovations are helping expand biometric adoption across consumer electronics and connected devices.

Below is the list of the key players operating in the global next-generation biometric authentication market:

Key players in the next-generation biometric authentication market are driving growth through continuous innovation in AI-powered, multimodal, and contactless authentication technologies. Companies like NEC Corporation, Thales, and IDEMIA are expanding secure digital identity platforms for government and enterprise use. Firms such as Microsoft and Amazon Web Services are integrating biometrics into cloud and passwordless authentication ecosystems, accelerating enterprise adoption. Additionally, advancements in fingerprint sensors and mobile biometrics by companies like Synaptics Incorporated and Fingerprint Cards AB are strengthening deployment across consumer electronics, further fueling next-generation biometric authentication market expansion.

Corporate Landscape of the Global Next-Generation Biometric Authentication Market:

Recent Developments

- In March 2025, Amazon Web Services expanded the capabilities of its AWS Console Mobile App by adding support for 24 additional services. This update allows users to access services such as Service Quotas, CloudFront, Amazon SES, AWS Cloud9, and AWS Batch through an integrated mobile web browser within the app. The enhancement improves accessibility and enables customers to manage a broader range of AWS services seamlessly on mobile devices.

- In July 2024, IDEMIA announced the delivery of an upgraded Multibiometric Identification System (MBIS) to INTERPOL, incorporating advanced fingerprint and facial recognition technologies. The system enables all 196 member countries to more efficiently access and query biometric databases for criminal investigations. It features algorithms ranked number one in NIST benchmark evaluations, demonstrating significant improvements in accuracy and forensic performance. This development underscores IDEMIA’s role in advancing large-scale, AI-driven biometric solutions for global security applications.

- Report ID: 7978

- Published Date: Apr 24, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2036

Copyright @ 2026 Research Nester. All Rights Reserved.