Mobile Wallet Market Outlook:

Mobile Wallet Market size was valued at over USD 13.6 billion in 2025 and is expected to reach USD 115.2 billion by the end of 2035, growing at a CAGR of 26.8% during the forecast period, i.e., 2026-2035. In 2026, the industry size of mobile wallet is estimated at USD 17.2 billion.

The worldwide mobile wallet market is presently undergoing a profound transformation, rapidly evolving from a suitable payment alternative into the centralized pillar of digital financial infrastructure. According to official statistics published by the ORF America in January 2026, Pix and Unified Payment Interface (UPI) have emerged as the world’s most used real-time payment systems, accounting for 15% and 48% of global transactions, respectively. Besides, digital public infrastructure (DPI) has been readily adopted, with the economic value added projected to reach India from 2.95 to 4.2% of the gross domestic product (GDP). Regarding this, Aadhar provides a biometric-based ID for more than 1.4 billion citizens that support payments bridge, a suitable payment system, eSign, and electronic Know Your Customer (eKYC), thus driving the mobile wallet market exposure.

Global UPI and Pix Transaction Analysis (2017-2025)

|

Year |

UPI (Billion) |

Pix (Billion) |

|

2017 |

0.01 |

- |

|

2018 |

0.27 |

- |

|

2019 |

0.82 |

- |

|

2020 |

1.50 |

- |

|

2021 |

3.25 |

- |

|

2022 |

6.29 |

- |

|

2023 |

9.97 |

3.83 |

|

2024 |

14.44 |

March: 4.88 September: 5.51 |

|

2025 |

19.47 |

March: 6.25 September: 6.85 |

Source: ORF America

Furthermore, an expansion in super-app ecosystem, the proliferation of QR code payments, acceleration in contactless payment, enhanced biometric and security authentication, demographic adoption and segmentation patterns, and government-specific real-time payment infrastructure are certain trends that are responsible for bolstering the mobile wallet market globally. As stated in an article published by the Consumer Financial Protection Bureau in September 2023, there has been a continuous rise in point-of-sale purchases, especially in the U.S., and this particular growth is expected to continue, with the valuation of digital wallet tap-to-pay transactions growing by more than 150% by the end of 2028. This technological growth results in 16% of citizens in America holding a credit card, followed by an increase by 43%, thereby making it suitable for bolstering the market expansion.

Key Mobile Wallet Market Insights Summary:

Regional Highlights:

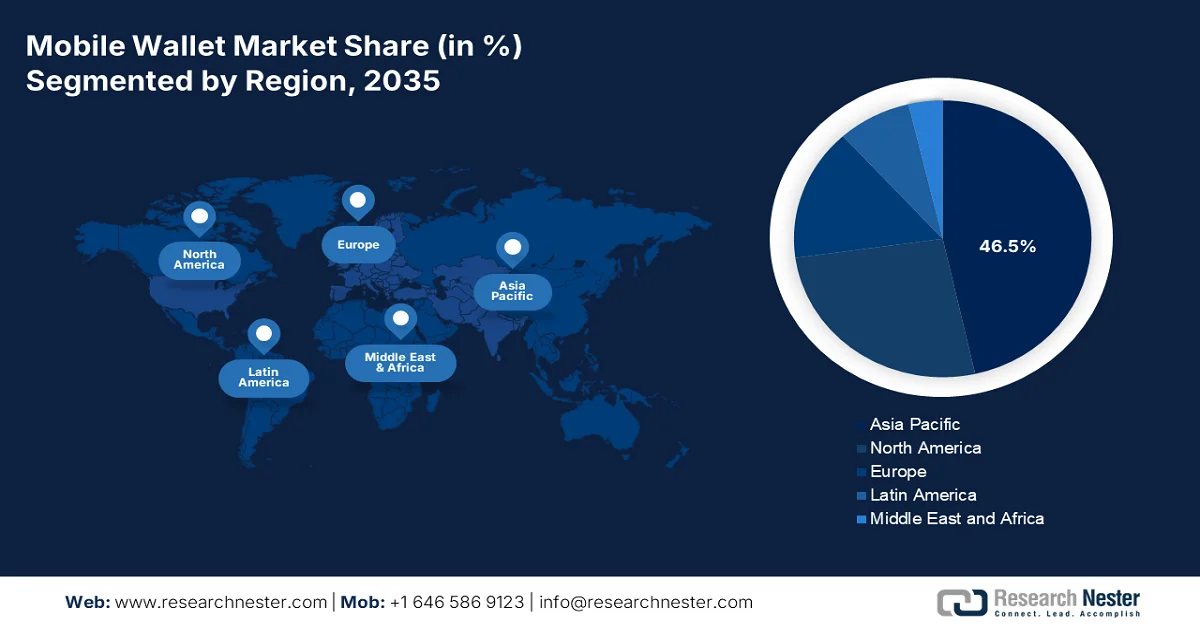

- Asia Pacific mobile wallet market is projected to hold a dominant 46.5% share by 2035, propelled by rapid smartphone penetration and expansion of real-time payment infrastructures

- Europe is anticipated to witness the fastest growth in the forecast period, impelled by rising e-commerce adoption and increasing consumer preference for contactless payments

Segment Insights:

- Individual consumers sub-segment in the mobile wallet market is expected to capture a leading 68.4% share by 2035, driven by widespread smartphone usage and growing preference for seamless digital payment experiences

- Proximity payments segment is projected to secure the second-highest share over the forecast period, fueled by enhanced transaction speed, security, and convenience

Key Growth Trends:

- Increase in mobile internet accessibility

- Expansion in digital retail transformation

Major Challenges:

- Merchant resistance and fee structure tensions

- Infrastructure gaps in emerging and rural economies

Key Players: Apple Inc. (U.S.), Google LLC (U.S.), Samsung Electronics Co. Ltd. (South Korea), Alibaba Group Holding Limited (China), Tencent Holdings Limited (China), PayPal Holdings Inc. (U.S.), Amazon.com Inc. (U.S.), Visa Inc. (U.S.), Mastercard Incorporated (U.S.), Kakao Pay (South Korea), PayPay Corporation (Japan), Rakuten Pay (Japan), PhonePe Private Limited (India), Paytm (India), Commonwealth Bank (Australia), NAB (Australia), Touch 'n Go Group (Malaysia), Boost (Malaysia), Barclays PLC (UK), Vodafone Group Plc (UK), Thunes (Singapore).

Global Mobile Wallet Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 13.6 billion

- 2026 Market Size: USD 17.2 billion

- Projected Market Size: USD 115.2 billion by 2035

- Growth Forecasts: 26.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (46.5% Share by 2035)

- Fastest Growing Region: Europe

- Dominating Countries: United States, China, India, United Kingdom, Germany

- Emerging Countries: Japan, South Korea, Brazil, Indonesia, Mexico

Last updated on : 19 March, 2026

Mobile Wallet Market - Growth Drivers and Challenges

Growth Drivers

- Increase in mobile internet accessibility: The foundational driver for the mobile wallet market caters to the unprecedented worldwide proliferation of mobile internet and smartphone accessibility. According to official statistics published by the VoxDev Organization in November 2025, mobile services and technologies significantly contributed USD 6.5 trillion to the worldwide GDP as of 2024. Besides, the Global Findex Digital Connectivity Tracker has demonstrated that 84% of adults in developing nations own a mobile phone. Moreover, 90% of adults across all regions significantly utilize smartphones. Meanwhile, device passwords are utilized by 60% mobile phone owners globally. Therefore, with such internet services, there is a huge growth opportunity for the market.

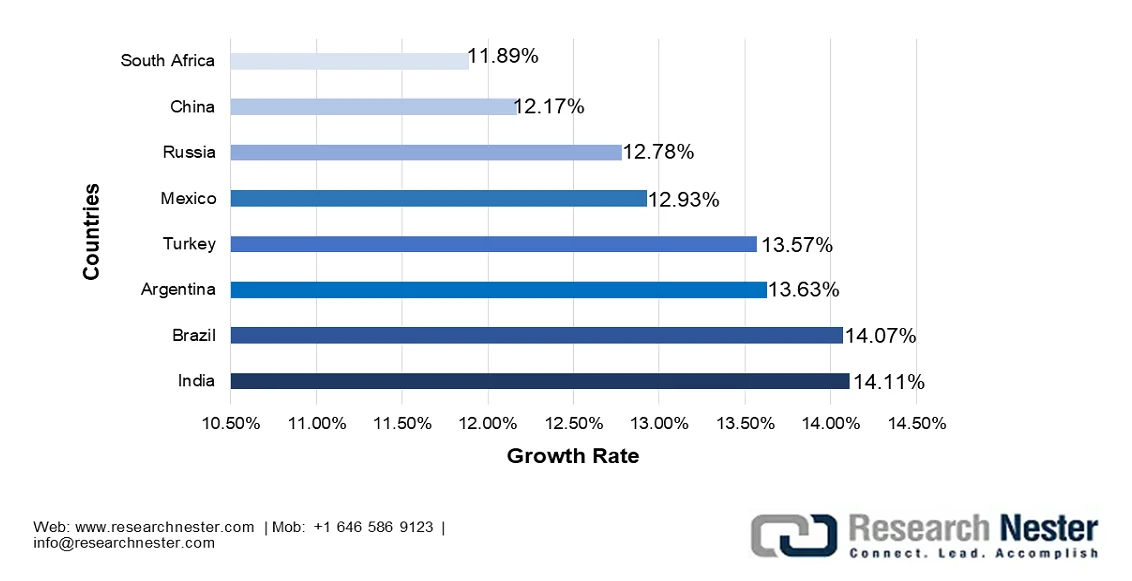

- Expansion in digital retail transformation: The transition towards online shopping and rise in e-commerce have effectively contributed to mobile wallet market growth and expansion. Based on government estimates published by the ITA in 2025, more than 90% of B2B organization has currently shifted to a virtual sales model, owing to improved managing software and process efficiencies. Additionally, the adoption rate of digitalized selling methods accounts for 13% in South Korea and 15% in Japan. Besides, the international B2C e-commerce revenue is projected to grow to USD 5.5 trillion by the end of 2027, with a steady 14.4% growth rate. Based on this growth, India is ranked among 20 nations globally in retail e-commerce development, with a 14.1% growth rate, thus positively impacting the market development.

Country-Wise B2C E-Commerce Forecast Analysis (2025)

Source: ITA

- Consumer demand for speed and convenience: The fundamental consumer preference for rapid and convenient transaction methods is continuing to drive the mobile wallet market adoption globally. As stated in an article published by the Department of Financial Services in July 2024, there has been an increase in overall digital payment transactions from 20.7 billion to 185.9 billion between 2023 and 2024, along with a 44% growth rate. In addition, these particular transactions have grown from 2.2 billion to 185.9 billion during the same duration, with transaction values increasing from USD 1.1 trillion to USD 36.5 trillion. Therefore, with such an increase in volume and value, mobile transaction services are gaining speed and convenience, thereby denoting an optimistic outlook for the market’s upliftment.

Challenges

- Merchant resistance and fee structure tensions: Providers in the mobile wallet market face persistent resistance from merchants concerned about transaction fees, data ownership, and the disintermediation of direct customer relationships. Payment processing fees associated with mobile wallets, typically passed through from card networks and acquiring banks, represent high costs for merchants operating on thin margins, particularly in retail, food service, and small business segments. These fee structures have become increasingly contentious, with merchants in multiple jurisdictions challenging interchange fees and seeking regulatory intervention. Beyond direct costs, merchants express concern about losing direct access to customer transaction data, which mobile wallet providers increasingly control and monetize.

- Infrastructure gaps in emerging and rural economies: The mobile wallet market adoption faces fundamental infrastructure barriers in emerging economies and rural regions where the digital payments ecosystem remains underdeveloped. Reliable internet connectivity remains inconsistent across large geographic areas, making real-time transaction processing and authentication unreliable. Smartphone penetration, while increasing globally, still excludes significant populations relying on feature phones incompatible with advanced wallet applications. Even where devices and connectivity exist, the absence of a robust digital identity verification infrastructure complicates onboarding and compliance with know-your-customer regulations.

Mobile Wallet Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

26.8% |

|

Base Year Market Size (2025) |

USD 13.6 billion |

|

Forecast Year Market Size (2035) |

USD 115.2 billion |

|

Regional Scope |

|

Mobile Wallet Market Segmentation:

End user Segment Analysis

The individual consumers sub-segment, which is part of the end user segment, is anticipated to garner the highest share of 68.4% in the mobile wallet market by the end of 2035. The sub-segment’s upliftment is highly driven by the fundamental transformation in how individuals conduct daily financial transactions across both developed and emerging economies. The segment's dominance is driven by the universal applicability of mobile wallets to consumer payment needs, from retail purchases and bill payments to peer-to-peer transfers and transportation fares. Besides, millennial and Gen Z consumers have grown up with smartphones as their primary computing devices, demonstrating a particular preference for mobile wallet adoption, valuing the convenience of contactless payments, loyalty program integration, and seamless e-commerce checkout experiences.

Mode of Payment Segment Analysis

The proximity payments segment in the mobile wallet market is projected to account for the second-highest share during the forecast period. The segment’s growth is highly fueled by its importance for enhancing consumer convenience, security, and transaction speed. According to official statistics published by the Communications of the IIMA in 2022, the mobile payment utilization surpassed the revenue of USD 930 billion internationally and successfully reached 1.3 billion users by the end of 2023. Regarding this growth, 30% consumers utilize mobile devices for contactless payment, and 75% prefer using debit or credit cards for contactless payments. Moreover, almost 45% of customers frequently utilize mobile wallets to make payments, denoting an increase from 23%, thus effectively driving the segment’s growth globally.

Type Segment Analysis

By the end of the stipulated timeline, the open wallets sub-segment, which is part of the type segment, is expected to hold the third-highest share in the mobile wallet market. The sub-segment’s development is highly propelled by the aspect of permitting users to transact and store various payment methods across different businesses. Additionally, this provides significant benefits in interoperability, security, and convenience. As per an article published by OECD in September 2025, there has been an increase in consumers initiating and receiving digital payments from 55% to 62% between 2021 and 2024, and overall, it accounts for 96% across OECD-based nations. This demonstrates that consumers are increasingly relying on digitalized payment modes to effectively transfer money and purchase required goods and services, which in turn is positively impacting the sub-segment’s expansion globally.

Our in-depth analysis of the mobile wallet market includes the following segments:

|

Segment |

Subsegments |

|

End user |

|

|

Mode of Payment |

|

|

Type |

|

|

Technology |

|

|

Application |

|

|

Ownership |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Mobile Wallet Market - Regional Analysis

APAC Market Insights

The Asia Pacific in the mobile wallet market is anticipated to garner the highest share of 46.5% by the end of 2035. The market’s upliftment in the region is primarily attributed to unprecedented smartphone penetration, government-funded real-time payment infrastructures, the proliferation of super-app ecosystems, and the focus on absolute transaction volume. According to official statistics published by the PCI Security Standards Council Organization in 2023, there has been an expected growth in digitalized payments by 19.8% in the region by the end of 2027. Besides, the volume of non-cash transactions significantly reached the 1.3 trillion mark as of 2023, while real-time payment transaction volumes are projected to increase at a 14.1% growth by 2027. Moreover, B2B payments revenue effectively doubled to USD 1.4 trillion as of 2025 at a 10.5% growth rate, thus driving the market growth in the overall region.

The mobile wallet market in China is growing significantly, owing to increased penetration through super-app ecosystems, embedded payments through social media, lifestyle, and e-commerce services, digital infrastructure development, and expansion in mobile payment adoption. As per an article published by the State Council in March 2026, the overall number of cross-border transactions processed by the domestic UnionPay and NetsUnion Clearing Corporation increased by 124.5%, and the overall transaction valuation surged by 90.4%. This particular growth in payment activity significantly reflects the growing appeal of the country as the ultimate travel destination, as well as the seamless integration of mobile payment systems for international visitors. Therefore, with such growth in payment services, the mobile wallet market is gradually expanding in the overall country.

The revolution in digital payments through UPI, the government’s Digital India Initiative, the presence of a supportive regulatory framework encouraging advancements and maintaining consumer protection, and financial inclusion strategies are factors uplifting the market in India. As stated in an article published by the Department of Financial Services in November 2024, there has been an increase in the overall digital payment transactions in the country from 20.7 billion to 187.3 billion between 2023 and 2024, along with a 44% growth rate. Meanwhile, UPI has significantly revolutionized digital payments in the nation, with growth accounting for 920 million to 131.1 billion between the same duration, with 129% growth rate. Therefore, nearly 46% of the worldwide real-time payment transactions are taking place in India, which is positively impacting the mobile wallet market.

Monthly India-Based Digital Payment Transactions in Value and Volume (2024)

|

Months |

Transaction Value (USD) |

Transaction Volume |

|

April |

25.7 million |

16.8 billion |

|

May |

51.5 million |

17.6 billion |

|

June |

26.2 million |

17.3 billion |

|

July |

47.9 million |

17.8 billion |

|

August |

31.0 million |

17.6 billion |

|

September |

27.1 million |

17.6 billion |

Source: Department of Financial Services

Europe Market Insights

Europe in the mobile wallet market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the presence of mobile payment technologies, robust consumer preference for mobile wallets, significant increase in contactless payment incorporation, and expansion in the e-commerce industry. According to official statistics published by the Consilium Europe in December 2025, 77% of internet users in the region purchased services or goods online in 2024. In addition, the share of e-shoppers surged from 57% to 77% in the same year, denoting an increase of 20% points. Besides, young and middle-aged adults in the region comprehensively embraced online shopping, with 89% of internet users aged 25 to 34 years engaged in online shopping, which is closely followed by 86% aged between 35 and 44 years, thus proliferating the market development.

Internet Users Initiating Online Purchases in Europe: Comparative Analysis (2010 versus 2024)

|

Countries |

2010 |

2024 |

|

Ireland |

52% |

96% |

|

Netherlands |

74% |

94% |

|

Denmark |

76% |

91% |

|

Sweden |

71% |

90% |

|

Czechia |

40% |

86% |

|

Slovakia |

42% |

85% |

|

France |

70% |

84% |

|

Germany |

73% |

83% |

Source: Consilium Europe

The mobile wallet market in Germany is gaining increased traction, owing to its robust economy, high consumer purchasing power, digital payment solutions, the existence of supportive regulatory frameworks, digital transformation across different industries, and expansion in buy-now-pay-later services. Based on government estimates published by the ITA in August 2025, it has been demonstrated that 51% of overall payments in the country are conducted with physical currency. Besides, the federal government unveiled the Research and Innovation for Technical Sovereignty 2030 (FITS2020) strategy in January 2025 and focused on allocating USD 1.7 billion yearly for strengthening the country’s position in industrial and digitalized technologies. Moreover, the AI scene in the country increased by 43% to USD 2.5 billion, thus driving the mobile wallet market expansion.

The aspects of an increase in the retail acceptance of contactless payment, consumer behavior trends effectively favoring mobile payments, and enhanced safeguarding expectations through regulatory frameworks are certain trends fueling the market in the UK. As stated in an article published by the UK Government in July 2025, nearly 50 billion payments have been made in the UK as of 2024 by businesses and consumers, accounting for almost 1,500 transactions every second. Besides, the ability to initiate and achieve payments is crucial to regular lives that underpin trade, economic activities, and commerce, with 48.1 billion transactions in the country. Meanwhile, there has been an increase in domestic contactless payments from 3% of overall transactions to 38% in 2023, accounting for 18.3 billion transactions, thereby making it suitable for the market development.

North America Market Insights

North America in the mobile wallet market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by regulatory catalysts, tactical shift toward control, and consumer adoption trends. According to official statistics published by the Federal Reserve Organization in June 2025, regional households earning less than USD 25,000 every year, and adults aged more than 55 years, depend more on cash and other payment methods. Besides, adults aged between 18 and 24 years are more likely to ensure payment through a mobile phone and readily utilize phones for 45% of overall payments. Moreover, consumers tend to initiate an average of 48 monthly payments as of 2024. Additionally, in the same year, cash accounted for 14% of all consumer payments, and meanwhile, debit and credit cards catered to 30% and 35% of payments, thus driving the market expansion.

Average Number of Payments in North America (2016-2024)

|

Year |

Cash |

Credit |

Debit |

ACH |

Other |

|

2016 |

14 |

8 |

12 |

4 |

45 |

|

2017 |

12 |

9 |

11 |

4 |

41 |

|

2018 |

11 |

10 |

12 |

5 |

43 |

|

2019 |

10 |

9 |

12 |

4 |

38 |

|

2020 |

6 |

9 |

10 |

4 |

35 |

|

2021 |

7 |

10 |

10 |

4 |

36 |

|

2022 |

7 |

12 |

11 |

5 |

39 |

|

2023 |

7 |

15 |

14 |

6 |

46 |

|

2024 |

7 |

17 |

14 |

6 |

48 |

Source: Federal Reserve Organization

The mobile wallet market in the U.S. is gaining increased exposure, owing to large-scale consumer adoption, a push towards differentiation beyond basic payments, integration of high-value and new use cases, and digital ID integration as a notable catalyst. As per an article published by the Information Technology and Innovation Foundation Organization in September 2024, 90% of consumers in the country owned a smartphone as of 2023, which includes 97% of consumers under 50 years of age. Therefore, with an increase in digital ID and digital payments, there is no longer a need to carry a physical wallet. Besides, digital ID tends to save 110 billion hours internationally, leading to fraud reduction and cost savings amounting to USD 1.6 trillion. Furthermore, complete digital ID coverage in the country can significantly unlock economic valuation which is equivalent to 4% of GDP by the end of 2030, thus fueling the market growth.

The comprehensive adoption of smartphones and technology integration, a supportive regulatory environment and financial ecosystem, the push for accessibility and competition, and the transition to embedded and digital-first finance are factors boosting the mobile wallet market in Canada. As stated in an article published by the Canada Telecommunications Association in January 2023, 95% of the adult population significantly utilizes the internet, either on a smartphone or computer. Besides, the country’s internet utilization is ahead of countries such as the U.S., France, UK, Germany, Japan, and Italy, denoting an increase of 27% points from the 68% of the population. Besides, 98% of consumers aged between 18 and 29 years, as well as 95% of those aged between 30 and 49 years, own a smartphone, thereby making it suitable for fueling the market demand.

Key Mobile Wallet Market Players:

- Apple Inc. (U.S.)

- Google LLC (U.S.)

- Samsung Electronics Co. Ltd. (South Korea)

- Alibaba Group Holding Limited (China)

- Tencent Holdings Limited (China)

- PayPal Holdings Inc. (U.S.)

- Amazon.com Inc. (U.S.)

- Visa Inc. (U.S.)

- Mastercard Incorporated (U.S.)

- Kakao Pay (South Korea)

- PayPay Corporation (Japan)

- Rakuten Pay (Japan)

- PhonePe Private Limited (India)

- Paytm (India)

- Commonwealth Bank (Australia)

- NAB (Australia)

- Touch 'n Go Group (Malaysia)

- Boost (Malaysia)

- Barclays PLC (UK)

- Vodafone Group Plc (UK)

- Thunes (Singapore)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Apple Inc. leverages its deeply integrated hardware-software ecosystem, with Apple Pay pre-installed on iPhones and Apple Watches, to drive seamless adoption among its substantial and loyal user base. The company's strategic focus on privacy and security, emphasizing features such as tokenization and biometric authentication, positions its wallet as a trusted interface for transactions.

- Google LLC benefits from the ubiquitous reach of the Android operating system, allowing it to be pre-loaded on a vast array of device models from numerous manufacturers. Its strategy is evolving to transform the wallet into a comprehensive digital hub, integrating not just payments but also passes, transit tickets, and digital IDs.

- Samsung Electronics Co. Ltd. distinguishes itself through its strategic acquisition of LoopPay technology, which enabled Magnetic Secure Transmission (MST) to ensure compatibility with traditional magnetic stripe terminals, broadening its acceptance at launch. The company integrates its wallet deeply within its device ecosystem, offering synergy with other Samsung services and products to enhance user convenience.

- Alibaba Group Holding Limited has transcended its function as a mere payment tool to become the central pillar of a comprehensive super-app, offering a vast suite of financial and lifestyle services within a single platform. Its market dominance is fortified by its symbiotic relationship with Alibaba's e-commerce ecosystem, facilitating seamless transactions for millions of merchants and consumers.

- Tencent Holdings Limited is inextricably linked to the ubiquitous WeChat social messaging app, turning peer-to-peer transfers and merchant payments into a native, frictionless part of daily social interaction and communication. The company's strategy successfully embeds financial transactions within a broader context of social networking, content, and mini-programs, creating an indispensable, all-encompassing user experience.

Here is a list of key players operating in the global market:

The mobile wallet market is characterized by intense competition between technology giants, financial institutions, and fintech innovators across global regions. Technology companies from the U.S. and China collectively dominate the market, leveraging their extensive user bases and integrated ecosystems to drive adoption. Apple, Google, and Samsung maintain leadership through hardware integration and seamless user experiences, while Asia-based players such as Alibaba's Alipay and Tencent's WeChat Pay have achieved dominance through super-app ecosystems that embed payments within broader lifestyle services. Besides, in October 2024, Thunes significantly expanded its Direct Global Network into Egypt. This expansion brought bank account payments and mobile wallet solution capabilities to the organization’s pay strategies, thus enhancing cross-border payment services in both North Africa and the Middle East dynamic economies, thereby boosting the mobile wallet industry globally.

Corporate Landscape of the Mobile Wallet Market:

Recent Developments

- In December 2025, Visa successfully enabled the unveiling of three brand new digital wallets in Europe by partnering with Vipps MobilePay, Klarna, and BBVA, and also collaborating with BANCOMAT based on a planned pilot as of early 2026.

- In April 2024, Mastercard introduced the latest mobile virtual card application that readily enables virtual commercial cards to be added seamlessly to digitalized wallets and also offers financial institutions with suitable choices for delivering sustainable and secure contactless payment solutions.

- In January 2023, Samsung Electronics unveiled the availability of Samsung Wallet across 8 economies, including Taiwan, Singapore, Malaysia, India, Hong Kong, Canada, Brazil, and Australia. This particular service is a go-everywhere and secure application to conveniently utilize and organize regular essentials.

- Report ID: 8449

- Published Date: Mar 19, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.