Machine Learning Market Outlook:

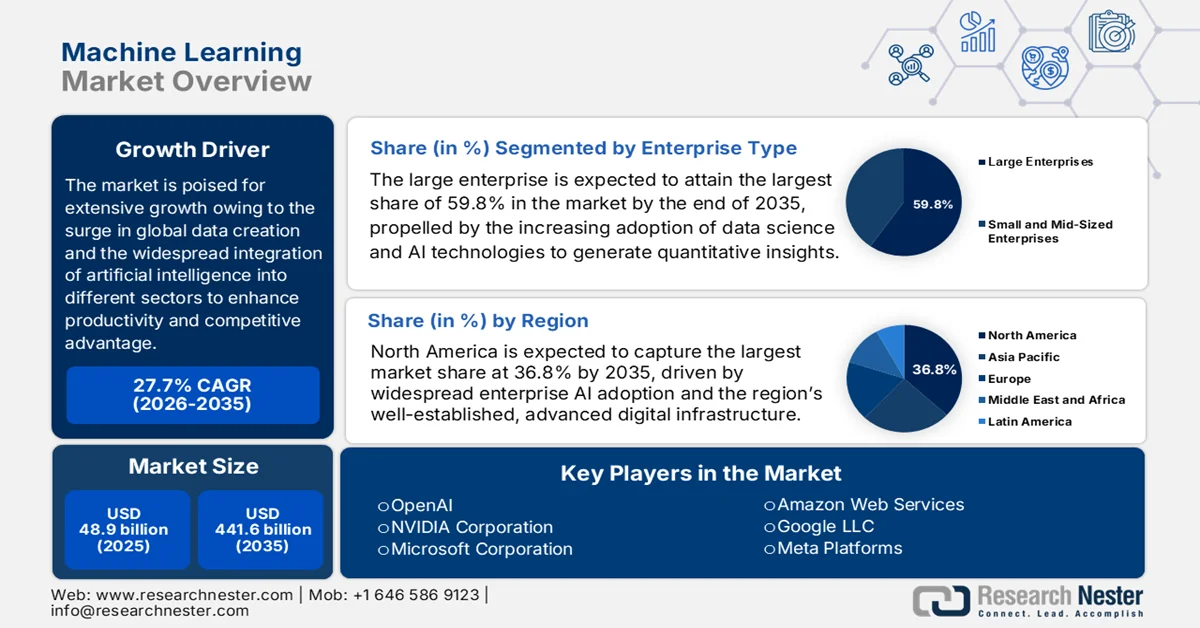

Machine Learning Market was valued at USD 48.9 billion in 2025 and is expected to grow significantly, reaching USD 441.6 billion by 2035, representing a CAGR of 27.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of machine learning is estimated at USD 62.4 billion.

The machine learning market is poised for extensive growth in the upcoming years, owing to the exponential surge in global data creation and the widespread integration of artificial intelligence into different sectors to enhance productivity and competitive advantage. In this context, governments across different nations are making generous investments to expand their applications in various fields. In December 2025, the U.S. Department of Agriculture (USDA) stated that the ARS Artificial Intelligence Center of Excellence (AI-COE) will fund 4 to 6 projects in the financial year 2026 at up to USD 100,000 each, supporting the development or adaptation of AI and ML methods to address agricultural research challenges or create prototype digital tools for producers. The funded projects must demonstrate real-world applicability, leverage SCINet’s high-performance computing clusters, including GPU and high-memory nodes, and focus on AI, ML-driven scientific research, hence positively impacting the market’s growth and exposure in the agricultural sector.

Furthermore, the industry-specific demand in sectors such as healthcare and finance, influenced by the need for predictive maintenance, fraud detection, and personalized diagnostics, also fosters innovation and large-scale deployment in the market. The Library of Congress in March 2024 revealed that the financial industry is adopting artificial intelligence and machine learning with a prime focus on enhancing efficiency, decision-making, risk management, and customer service. The U.S. investment in AI is expected to reach a substantial amount of USD 100 billion in 2025, and global investment is nearly USD 200 billion. Meanwhile, the advances in computing power, big data analytics, and access to alternative and unstructured data allow AI and ML systems to analyze complex datasets, automate processes, and deliver more accurate insights when compared to traditional methods.

Key Machine Learning Market Insights Summary:

Regional Highlights:

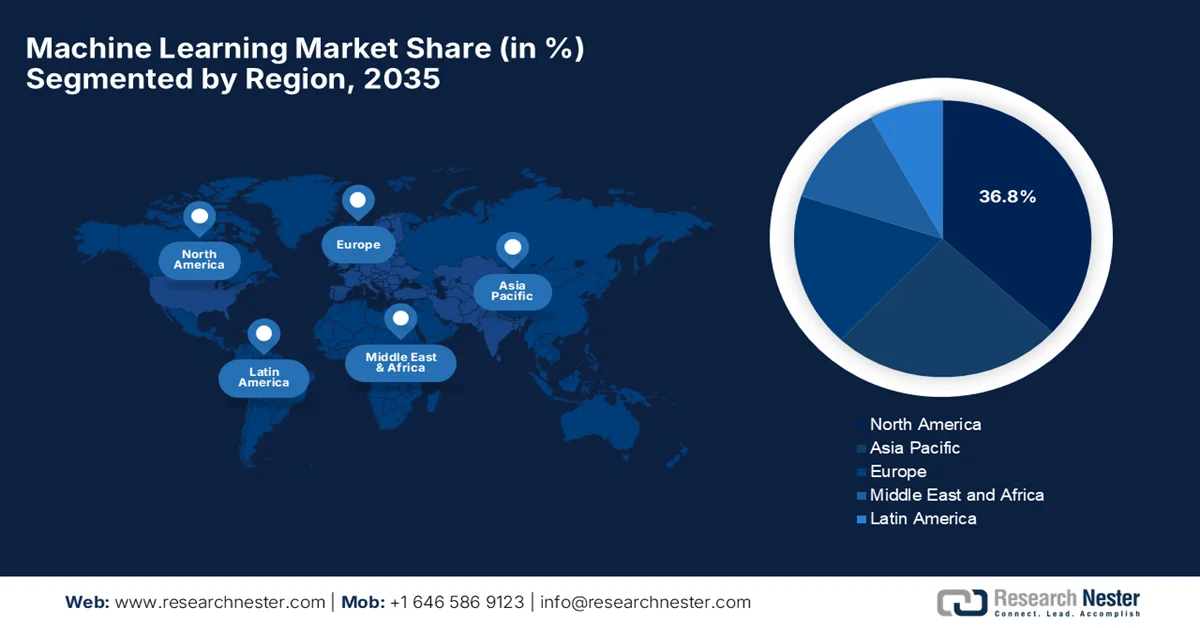

- The North America region is projected to command a 36.8% share of the machine learning market by 2035, stimulated by strong enterprise AI adoption and advanced digital infrastructure.

- Asia Pacific is anticipated to witness rapid expansion in the forecast period 2026–2035, fueled by government-backed AI initiatives and expanding machine learning integration across industries.

Segment Insights:

- In the machine learning market, the large enterprise segment is forecast to account for 59.8% share by 2035, propelled by increasing adoption of data science and AI technologies to generate quantitative insights.

- The cloud-based segment is expected to lead the market by 2035, catalyzed by scalable cloud infrastructure enabling broader enterprise-level AI and deployment.

Key Growth Trends:

- Explosion of data and digital transformation initiatives

- Rising adoption of cloud-based ML platforms

Major Challenges:

- Data quality and availability

- Talent shortage and skill gaps

Key Players: OpenAI (U.S.), NVIDIA Corporation (U.S.), Microsoft Corporation (U.S.), Amazon Web Services (U.S.), Google LLC (U.S.), Meta Platforms (U.S.), IBM Corporation (U.S.), Intel Corporation (U.S.), Salesforce (U.S.), SAP SE (Germany), Seldon.io (UK), Mind Foundry (UK), Sony Corporation (Japan), Fujitsu Limited (Japan), Samsung SDS (South Korea), Upstage Co. Ltd. (South Korea), Tata Consultancy Services (India), Axiata Group (Malaysia), Siemens AG (Germany), Xanadu Quantum Technologies Inc. (Canada), Lockheed Martin Corporation (U.S.), RADCOM Ltd. (Israel), Fractal Analytics Limited (India)

Global Machine Learning Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 48.9 billion

- 2026 Market Size: USD 62.4 billion

- Projected Market Size: USD 441.6 billion by 2035

- Growth Forecasts: 27.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (36.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: India, South Korea, Canada, Singapore, Australia

Last updated on : 10 March, 2026

Machine Learning Market - Growth Drivers and Challenges

Growth Drivers

- Explosion of data and digital transformation initiatives: The increase in digital data from IoT devices, online transactions, and customer interactions efficiently fuels the demand for ML solutions that can extract insights and automate analytics. In this context, machine learning plays a pivotal role in processing huge amounts of structured and unstructured data sets more efficiently. The government of India, in December 2024, announced a series of initiatives that are mainly focused on strengthening the country’s digital infrastructure and public services, building on platforms such as Aadhaar, UPI, DigiLocker, and DIKSHA, along with advanced data centers and AI-driven technologies. Besides, these efforts included expanding citizen-centric services through UMANG, MeriPehchaan, API Setu, and CSCs, improving rural connectivity, financial inclusion, and digital access, hence benefiting the overall market.

- Rising adoption of cloud-based ML platforms: The aspects of cloud infrastructure make ML more accessible, scalable, and cost-effective. Therefore, organizations across most nations prefer cloud deployments due to reduced infrastructure costs, flexibility, and quicker deployment cycles, which allow even small and mid-sized businesses to adopt ML. The article, which was published by the National Institute of Health (NIH) in March 2024, states that a clinical trial developed a cloud-based machine learning platform using wearable devices to monitor physical activity in patients discharged with cardiovascular conditions. By analyzing more than 17,000 person-day data points with an XGBoost algorithm, the system accurately predicted clinical outcomes with 85% overall accuracy, 87% sensitivity, and 79% specificity. Therefore, such studies reflect the potential of cloud-based ML tools to support precision home health monitoring and reduce hospital readmissions, thus suitable for bolstering the machine learning market globally.

- Demand for predictive analytics and real-time insights: Businesses across different sectors, such as finance and healthcare, retail, and manufacturing, are depending on ML for predictive analytics in order to forecast trends and make data-driven decisions. In this context, the World Bank in June 2025 reported that governments in Latin America and the Caribbean collect huge amounts of administrative data, wherein 96% of management information system data is being used for descriptive analytics, of that 50% applied for diagnostic or predictive purposes. Besides, predictive analytics, such as early warning systems in health and education needs to be improved, and 8% of Health MIS is fully digitalized. Moreover, strengthening analytical capabilities, investments in analytics units, and improving data infrastructure are highly essential to turn data into actionable insights for evidence-based governance, hence driving the overall market.

U.S. Hospital Adoption of Predictive AI by Size, Ownership, and Location: 2023-2024

|

Category |

Metric |

2023 |

2024 |

|

Overall adoption |

Hospitals using predictive AI (integrated with EHR) |

66% |

71% |

|

By hospital size |

Small (<100 beds) |

53% |

59% |

|

Medium (100-399 beds) |

75% |

80% |

|

|

Large (>400 beds) |

90% |

96% |

|

|

By ownership |

Government |

39% |

44% |

|

Non-profit |

75% |

80% |

|

|

For-profit |

60% |

69% |

|

|

By location |

Rural |

48% |

56% |

|

Urban |

77% |

81% |

Source: ASTP

Challenges

- Data quality and availability: One of the biggest challenges in the machine learning market is making sure that there is access to high-quality and well-labeled data. The models in machine learning rely mostly on large datasets for training, validation, and testing, but most of the organizations struggle with fragmented, inconsistent, or biased data sources. Therefore, the aspect of poor data quality is known to negatively affect model accuracy, reliability, and fairness, which can lead to flawed predictions and operational risks. In regulated sectors such as healthcare and finance, data privacy laws impose restrictions on access to usable datasets. In addition, labeling data is time-consuming and expensive, especially for specialized domains, making it challenging for firms from price-sensitive regions.

- Talent shortage and skill gaps: The shortage of skilled workforce is identified as a major barrier, causing hindrance to market growth. Meanwhile, the process of developing, deploying, and maintaining ML systems necessitates proper knowledge in data science, statistics, programming, domain knowledge, and MLOps practices. In this context, the demand for experienced ML engineers and AI researchers outpaces supply, thereby adding burgeoning hiring costs and intensifying competition for talent. In addition, smaller enterprises and emerging markets struggle to attract or retain qualified professionals. Furthermore, the continued advancements in ML and tools in turn necessitate continuous upskilling, making workforce development a critical challenge in this field.

Machine Learning Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

27.7% |

|

Base Year Market Size (2025) |

USD 48.9 billion |

|

Forecast Year Market Size (2035) |

USD 441.6 billion |

|

Regional Scope |

|

Machine Learning Market Segmentation:

Enterprise Type Segment Analysis

In the enterprise type segment, large enterprise is expected to attain the largest share of 59.8% in the machine learning market by the end of 2035. The subtype’s dominance in this field is mainly propelled by the increasing adoption of data science and AI technologies to generate quantitative insights. The large enterprises are also leveraging deep learning and advanced AI techniques to improve service quality and operational efficiency. In May 2025, IBM reported that it introduced new hybrid AI technologies at its THINK event, thereby allowing enterprises to build and deploy AI agents quickly using their own enterprise data through watsonx Orchestrate. These solutions integrate with over 80 enterprise applications and provide pre-built domain agents, agent orchestration, and observability, helping businesses automate workflows and optimize operations, hence denoting a wider segment scope.

Europe Enterprises Considering AI Adoption by Size Class: Official Government-Reported Statistics for 2024 and 2025

Source: Eurostat

Deployment Type Segment Analysis

By the conclusion of 2035, the cloud-based sub-segment is anticipated to lead the machine learning market with a considerable share. The increase in firm-level adoption of AI technologies, which is supported by scalable cloud infrastructure, indicates that cloud adoption is a key enabler for broad ML deployment. For instance, Salesforce in June 2023 reported that it has launched AI Cloud, which is a cloud-native platform that incorporates generative AI, analytics, and automation across enterprise workflows with the main goal to enhance productivity and customer experiences. The company also notes that this cloud is powered by the Einstein GPT Trust Layer, which ensures data security and compliance by enabling organizations such as AAA, Gucci, and RBC US Wealth Management to leverage AI at scale. Hence, this platform demonstrates the prominence of cloud infrastructure in enabling the broad adoption of machine learning and AI technologies across enterprises.

End use Industry Segment Analysis

The IT and telecommunications sub-type is predicted to hold a significant portion of the market during the forecast period. This growth is primarily driven by the reliance of IT and telecom companies on advanced analytics and automation to improve network performance. The adoption of AI-based chatbots, recommendation systems, and intelligent routing in telecom operations also fuels ML deployment. Companies are using ML algorithms for traffic management and to detect anomalies, thereby enhancing service reliability. Besides, the rise of 5G networks and edge computing is efficiently accelerating ML adoption by providing the infrastructure that is needed for low-latency, data-intensive applications. Furthermore, IT and telecom providers are leveraging ML-driven insights to improve retention and develop innovative digital services, solidifying the segment’s strategic importance in the overall machine learning industry over the years ahead.

Our in-depth analysis of the machine learning market includes the following segments:

|

Segment |

Subsegments |

|

Organization Size |

|

|

Deployment Type |

|

|

End use Industry |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Machine Learning Market - Regional Analysis

North America Market Insights

The North America machine learning market is expected to lead the industry with a total of 36.8% revenue share by 2035, highly propelled enterprise AI adoption and advanced digital infrastructure. The region also benefits from a well-established innovation landscape, which is supported by public research institutions, industry collaboration, and federal initiatives that are proactively promoting trustworthy AI standards. In July 2025, the U.S. National Science Foundation announced a total investment of USD 100 million to support five National Artificial Intelligence Research Institutes with the main goal to advance AI research, workforce development, and public benefit. These institutes are focused on materials discovery, generative AI, STEM education, molecule creation, and AI assistants, leveraging cloud-based platforms and machine learning to accelerate innovation, hence denoting a positive market outlook.

The rising investments in AI research and technical standards are certain factors that are responsible for uplifting the U.S. machine learning market. The research organizations in the country are leading the way in guiding the prominence of machine learning is used across public services, industry, and critical supply chains. At the same time, their initiatives create a supportive environment that encourages businesses confidently adopt machine learning by meeting high standards for performance and reliability. In October 2024, the U.S. National Artificial Intelligence Research Resource (NAIRR) pilot, which was launched by the NSF in January 2024, is providing researchers and educators across the nation with access to advanced AI and machine learning infrastructure, including high-performance computing, cloud resources, and LLMs. This particular pilot partners with federal agencies, industry leaders such as Microsoft, NVIDIA, and OpenAI, and nonprofit organizations, and it enables projects in materials discovery, AI-augmented learning, and accessibility for deaf learners, hence suitable for standard market growth.

The massive, ongoing federal funding for research and infrastructure is the key growth catalyst boosting the market in Canada. The presence of a robust talent pool, rapid adoption of AI for automation, and investments in cloud computing are also propelling the growth of the country’s market. Based on the officially reported data, which was published in November 2025, the country’s federal government made a total investment of USD 42.5 million in AI compute infrastructure at the University of Toronto through the Canadian Sovereign AI Compute Strategy to support researchers across health care, science, engineering, and humanities. Besides, this initiative aims to boost national AI leadership, provide access to advanced machine learning capabilities, and strengthen research collaboration across universities, Indigenous communities, and industry partners.

APAC Market Insights

The Asia Pacific machine learning market is predicted to experience robust growth supported by its central countries, which are advancing machine learning technologies both in industry and public service delivery. These administrative programmes in this region reflect a push towards embedding machine learning across diverse sectors, from agriculture to healthcare, with support from government-backed initiatives and ecosystem development platforms. In January 2026, South Korea’s AI Basic Act came into effect, which forms a legal and governance framework to advance the nation’s AI and machine learning capabilities. The government data states that this Act supports research and development, the creation of AI training datasets, infrastructure such as AI data centers, and the ethical, safe deployment of AI across industries and public services, hence supporting the overall market’s growth and exposure.

The rapid deployment of machine learning and autonomous systems as a competitive economic and technological priority is driving the market in China. The country’s government-backed initiatives are designed to strengthen innovation capacity and integration in both public and commercial domains. In January 2026, the country’s government released an action plan to secure a reliable domestic supply of core AI technologies by 2027, with a strong focus on integrating artificial intelligence into manufacturing. Besides, this plan targets the deployment of three to five general-purpose large AI models, the development of industry-specific models, and the creation of 100 high-quality industrial datasets to accelerate intelligent production. Therefore, from a strategic perspective, such plans efficiently boost market growth by accelerating industrial adoption of machine learning, strengthening domestic AI capabilities, and stimulating innovation across major sectors.

The machine learning market in India is being propelled by the government-backed missions that provide centralized resources for AI and machine learning developments. These initiatives support startups, public institutions, and educational programmes to foster the adoption of ML technologies. In March 2025, according to the article published by the Press Information Bureau (PIB), the country’s Ministry of Electronics & IT outlined a national AI roadmap under the USD 1.24 billion IndiaAI Mission, focused on expanding AI, machine learning infrastructure, indigenous model development, and affordable access to high-performance GPUs. The initiative includes 18,693 GPUs, open compute access at subsidized rates, Centres of Excellence across sectors, and support for foundational models such as BharatGen and Sarvam-1 hence suitable for bolstering market growth in the country.

Europe Market Insights

Europe market is growing at a significant rate, primarily propelled by coordinated continental strategies that promote adoption with a strong emphasis on ethical, secure, and socially responsible AI. The government initiatives, regulatory frameworks, and the shift toward cloud-based deployment also drive the region’s market. In August 2024, as stated by the European Union’s article, its AI Act entered into force, which forms a harmonized, risk-based regulatory framework for artificial intelligence across all member states. The Act sets clear obligations for high-risk AI systems, such as those used in healthcare, recruitment, and critical infrastructure, by promoting transparency and banning unacceptable uses such as social scoring. Furthermore, it creates uniform compliance standards and encourages responsible innovation to strengthen reliable machine learning deployment and position Europe as a predominant leader in safe and human-centric AI.

Europe Enterprises Using Artificial Intelligence in 2025: Adoption by Country and Sector

|

Category |

Metric |

Value (2025) |

|

By country (highest & lowest) |

Denmark |

42.03% |

|

Finland |

37.82% |

|

|

Sweden |

35.04% |

|

|

Romania |

5.21% |

|

|

Poland |

8.36% |

|

|

Bulgaria |

8.55% |

|

|

By sector (highest adoption) |

Information & communication |

62.52% |

|

Professional, scientific & technical services |

40.43% |

|

|

Real estate |

24.82% |

|

|

Construction |

10.79% |

Source: Eurostat

Government AI strategies that aim to close gaps with global leaders by enhancing research infrastructures are the primary catalyst for the market in Germany. The focus on enabling innovative machine learning applications in strategic industries such as manufacturing and quantum technologies. In February 2025, the Deutsche Forschungsgemeinschaft (DFG) announced the continuation of its funding initiative in artificial intelligence by supporting up to 15 Emmy Noether Groups that are highly focused on AI methods. This program concentrates on providing early-career researchers with optimal conditions to conduct advanced AI research and cultivate the next generation of leading AI experts in the country. The initiative includes additional calls to identify AI-specific research needs, ensuring that funding aligns with emerging priorities across disciplines, hence solidifying the country’s position in the machine learning industry.

The growth of the UK machine learning market can be attributed to the formation of safety institutes and a focus on collaborative AI evaluation, which reflects a national commitment to balancing innovation with responsible deployment. These factors are contributing to a robust environment for machine learning adoption and governance. As per the data which was kept forward by the country’s government in January 2026, its AI Opportunities Action Plan underscores the AI initiatives, including AI-assisted NHS diagnostics for 2.4 million chest X-rays, AI tutoring pilots in schools, and the launch of Isambard-AI supercomputer and 5 AI Growth Zones to expand public compute capacity. It also backs the Sovereign AI Unit with up to USD 610 million to support domestic AI companies, along with more than USD 122 million for the National Data Library to unlock public datasets for AI research and applications, hence denoting a positive outlook for the market’s upliftment in the country.

Key Machine Learning Market Players:

- OpenAI (U.S.)

- NVIDIA Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Amazon Web Services (U.S.)

- Google LLC (U.S.)

- Meta Platforms (U.S.)

- IBM Corporation (U.S.)

- Intel Corporation (U.S.)

- Salesforce (U.S.)

- SAP SE (Germany)

- Seldon.io (UK)

- Mind Foundry (UK)

- Sony Corporation (Japan)

- Fujitsu Limited (Japan)

- Samsung SDS (South Korea)

- Upstage Co. Ltd. (South Korea)

- Tata Consultancy Services (India)

- Axiata Group (Malaysia)

- Siemens AG (Germany)

- Xanadu Quantum Technologies Inc. (Canada)

- Lockheed Martin Corporation (U.S.)

- RADCOM Ltd. (Israel)

- Fractal Analytics Limited (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- OpenAI is a pioneer in terms of generative machine learning models and large language models such as GPT-4 and beyond. The company has secured significant strategic investments to scale compute infrastructure and research, which also includes massive funding that has allowed it to push frontier AI technologies and fuel adoption across enterprise and consumer applications.

- NVIDIA Corporation is also a prominent player in this field that benefits from foundational GPU and AI compute capabilities that power the majority of modern ML training and inference workloads. The firm’s hardware platforms and software ecosystem readily accelerate deep learning across data centers, cloud, and edge environments.

- Microsoft Corporation is a central player that deliberately boosts machine learning incorporation through Azure AI and its enterprise ecosystem by embedding models into productivity software and cloud services. The company actively partners with AI innovators to strengthen its enterprise AI leadership and expand cloud-based ML adoption.

- Google LLC is a specialist that combines advanced ML research, custom TPU hardware, and scalable cloud services under Google Cloud AI and its DeepMind division. The company is mainly focused on end-to-end ML tools and research in multimodal models and optimization, thereby serving both developers and enterprises with flexible ML platforms.

- IBM Corporation has a long history in enterprise AI with its Watson platform, which provides machine learning, natural language processing, and automation. The company’s solutions are suitable for healthcare, finance, and large-scale digital transformation, and it emphasizes explainable ML deployment in complex business environments.

Below is the list of some prominent players operating in the global market:

The global machine learning market is dominated by large U.S.-based firms such as OpenAI, NVIDIA, Microsoft, AWS, Google, Meta, IBM, and Intel that lead in terms of AI platforms, cloud ML services, and hardware acceleration. Europe-specific innovators such as SAP, Dataiku, Seldon.io, Owkin, and Mind Foundry complement the market competency with strong enterprise ML tools, platforms, and industry-specific solutions. On the other hand, players from the Asia Pacific are efficiently expanding ML applications in consumer technology and enterprise AI. In February 2026, Siemens AG announced that it had acquired Canopus AI to integrate AI-based computational metrology and inspection into semiconductor manufacturing. The deal enhances Siemens’ EDA portfolio by combining Canopus AI’s machine learning-based wafer and mask inspection technology with Siemens’ Calibre platform to improve edge placement error measurement, yield ramp, and time-to-volume for technically improved nodes.

Corporate Landscape of the Machine Learning Market:

Recent Developments

- In February 2026, Xanadu and Lockheed Martin announced they entered a joint research initiative to advance the foundations of quantum machine learning by focusing on generative models and novel quantum approaches to data representation for applications in defense, finance, and pharmaceuticals.

- In February 2026, RADCOM Ltd. reported that it had launched RADCOM Neura, which is an AI agent suite especially designed for integration into agentic AI ecosystems to transform service assurance into an enabler of autonomous, intent-driven networks. The product is powered by customer data from RADCOM ACE and advanced AI and ML tools.

- In February 2026, Fractal reported that it had launched PiEvolve, which is an evolutionary, agentic engine for autonomous machine learning and scientific discovery, achieving top-tier performance on OpenAI’s MLE-Bench with more than 60% overall medal rate and 80% MLE-Bench-Lite performance.

- In January 2026, Siemens and NVIDIA expanded their strategic partnership to develop an Industrial AI operating system by integrating AI across the full industrial lifecycle from design and simulation to adaptive manufacturing and supply chains.

- Report ID: 5169

- Published Date: Mar 10, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.