Luxury Wines and Spirits Market Outlook:

Luxury Wines and Spirits Market size was valued at over USD 297.8 billion in 2025 and is expected to reach USD 533.8 billion by the end of 2035, growing at a CAGR of 6.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of luxury wines and spirits is assessed at USD 317.7 billion.

The worldwide luxury wines and spirits market is readily shaped by evolving wealth distribution patterns, currency exchange volatility, demographic transitions, digital engagement, and sustainability credentials. According to official statistics published by the Oxfam Organization in January 2026, there has been a massive jump in billionaire wealth by more than 16% as of 2025, which is three times as rapid as the previous 5-year average to USD 18.3 trillion. In addition, this particular wealth category has been increasing by 81% over the past 6 years. Meanwhile, the collective wealth of different billionaires surged by USD 2.5 trillion, which is nearly equivalent to the overall wealth, which was held by the bottom 4.1 billion people. Therefore, with a continuous increase in this wealth category, there is a huge demand for wines and spirits, based on brand, which is positively impacting the luxury wines and spirits market growth.

Furthermore, the aspect of tokenized ownership, NFT-driven digital provenance, zero-alcohol ultra-premium and silent spirits formulations, and regenerative viticulture as a luxury differentiator are a few trends that are responsible for boosting the luxury wines and spirits market globally. As per an article published by NLM in March 2026, zero alcohol products generally mimic the appearance and taste of alcoholic beverages and comprise low alcohol content, usually less than 0.5% by volume. These products usually demonstrate small-scale proportions of overall alcohol sales, for instance, less than 3% in Australia, and 2% in the UK. Besides, these products are readily utilized as substitutes for alcoholic beverages and have the potential to diminish alcohol-based harms and alcohol consumption, thus denoting an optimistic outlook for the market exposure.

Key Luxury Wines and Spirits Market Insights Summary:

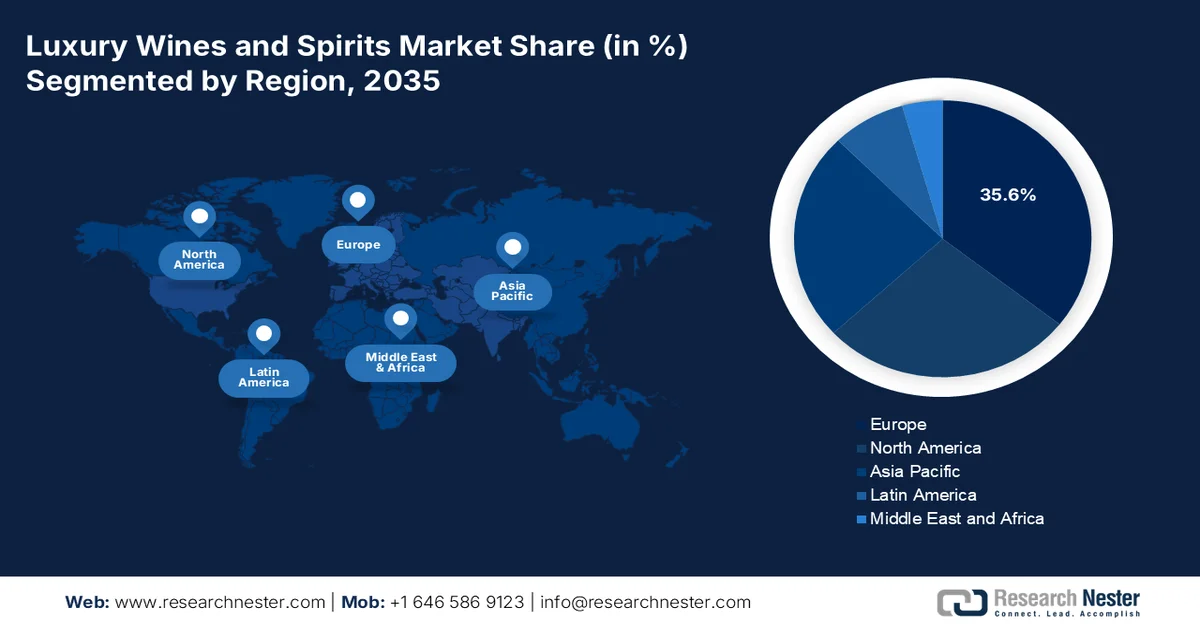

Regional Highlights:

- Europe in the luxury wines and spirits market is projected to command a 35.6% share by 2035, owing to its deep-rooted winemaking heritage, rising preference for artisanal premium products, and increasing demand for sustainable and organic offerings

- Asia Pacific is set to be the fastest-growing region over the 2026–2035 period, attributed to rising disposable incomes, expanding e-commerce penetration, and growing western cultural influence driving premiumization trends

Segment Insights:

- The individual consumers sub-segment under end user type in the luxury wines and spirits market is projected to account for a 40.7% share by 2035, propelled by moderate spirit consumption linked to psychosocial and health benefits enhancing mental and cardiovascular well-being

- The spirits segment within product type is expected to secure the second-highest share during the 2026–2035 period, impelled by its perceived role in fostering inner peace and facilitating deeper human consciousness connection

Key Growth Trends:

- Wealth transfer to the youth population with different expenditure priorities

- Expansion of travel retail across secondary airport facilities

Major Challenges:

- Supply chain fragility and raw material volatility

- Counterfeiting and brand integrity erosion

Key Players: Diageo Plc, Pernod Ricard, LVMH (Moët Hennessy), Brown-Forman Corporation, Bacardi Limited, Campari Group, Edrington Group, William Grant & Sons, ThaiBev, Sazerac Company, Heaven Hill Distilleries, Constellation Brands, The Wine Group, Suntory Holdings Limited, Asahi Group Holdings, Treasury Wine Estates, Accolade Wines, United Spirits Limited, Radico Khaitan, The Wine Shop, GALLO, TOPPAN Digital Inc., Piccadilly Distilleries, WX Brands.

Global Luxury Wines and Spirits Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 297.8 billion

- 2026 Market Size: USD 317.7 billion

- Projected Market Size: USD 533.8 billion by 2035

- Growth Forecasts: 6.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Europe (35.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, France, Italy, China, United Kingdom

- Emerging Countries: India, Japan, South Korea, Brazil, Mexico

Last updated on : 14 April, 2026

Luxury Wines and Spirits Market - Growth Drivers and Challenges

Growth Drivers

- Wealth transfer to the youth population with different expenditure priorities: The present youth have prioritized experimental consumption, digital-first discovery, and brand authenticity, in comparison to previous generations, viewing alcohol consumption as an appropriate display. According to official statistics published by the University of Michigan in April 2025, baby boomers in the U.S. significantly account for 51.8% of the nation’s overall wealth, which is worth USD 78.5 trillion. However, this particular population is continuously aging, with the youngest baby boomer aged 61 years and the oldest aged 79 years. Therefore, it has been estimated that USD 68 trillion to USD 84 trillion is projected to be under the ownership of spouses and descendants. Therefore, with this transfer, especially among the current generation, is positively driving the luxury wines and spirits market globally.

- Expansion of travel retail across secondary airport facilities: The aspect of primary airport facilities constitutes long-lasting luxury spirits duty-free sales; secondary airports across developing nations are continuously expanding, which is fueling the luxury wines and spirits market globally. Besides, as per a data report published by the USDA Government in December 2024, beverages comprising over 30% alcohol content are readily subject to 100% excise duty on the first USD 25 in payer’s pricing valuation and 10% later on, especially in Hong Kong. In addition, the same beverage category is effectively measured at a temperature of 20 degrees Celsius, which is subject to permit and license control, based on which import and export depend. Therefore, with such restrictions, the luxury wines and spirits market is continuously gaining increased exposure across different locations.

- Rise in private spirits and wine libraries for family offices: There has been an increase in the establishment of in-house spirits and wine libraries across private wealth management organizations. Unlike individual collectors, family offices usually purchase entire barrels, exclusive cuvées, and en primeur contracts directly from châteaux and distilleries, often at preferential pricing. These libraries are professionally stored in climate-controlled bonded warehouses, insured, and periodically rebalanced, such as investment portfolios. The particular library emerged in 2023 when fine wine indices outperformed gold and bonds. Based on this emergence, family offices currently allocate alternative asset portfolios to luxury spirits and wines, creating institutional-scale demand that was previously absent, thus proliferating the luxury wines and spirits market development.

Challenges

- Supply chain fragility and raw material volatility: Luxury wines and spirits depend on aging, climate-sensitive raw materials, including grapes, barley, rye, and oak. Besides, unpredictable weather patterns in key regions, such as Bordeaux, Champagne, Tuscany, and Scotland, reduce harvest yields and quality. Simultaneously, global logistics disruptions, such as container shortages, port delays, and rising freight costs, impact glass bottle, natural cork, and label supplies. Unlike mass-market beverages, luxury producers cannot easily substitute materials without devaluing brand heritage. Smaller luxury houses lack the bargaining power of giants, including LVMH or Pernod Ricard, making them vulnerable to supplier price hikes. Additionally, geopolitical tensions affect aluminum for capsules and wood for barrels from specific forests, which is negatively impacting the luxury wines and spirits market globally.

- Counterfeiting and brand integrity erosion: The luxury wines and spirits market counterfeit products, with fake premium Scotch, Cognac, and Champagne circulating through unverified online marketplaces and auction houses. Sophisticated forgery extends to holograms, serial numbers, and even bottle shapes. This erodes consumer trust, which is a critical asset for ultra-high-net-worth buyers who demand provenance. Besides, authentication technologies, including blockchain, NFC tags, and QR codes, exist, which many mid-tier luxury brands resist. Furthermore, cross-border enforcement is weak; counterfeiters operate from jurisdictions with lax intellectual property laws. For a sector built on heritage and storytelling, each fake bottle diminishes the perceived value of genuine products.

Luxury Wines and Spirits Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

6.7% |

|

Base Year Market Size (2025) |

USD 297.8 billion |

|

Forecast Year Market Size (2035) |

USD 533.8 billion |

|

Regional Scope |

|

Luxury Wines and Spirits Market Segmentation:

End user Segment Analysis

The individual consumers sub-segment, part of the end user type, is anticipated to garner the highest share of 40.7% in the luxury wines and spirits market by the end of 2035. The sub-segment’s upliftment is primarily attributed to moderate spirit consumption by individuals, which is associated with particular psychosocial, social, and health benefits, further centered around the mental and cardiovascular well-being of the consumers. According to official statistics published by the Penn State Extension in April 2024, 62% of individuals aged more than 18 years in the U.S., constituted a particular occasion to utilize alcoholic beverages, such as beer, wine, and liquor, as of 2023. Meanwhile, these individuals comprised 62% of men and women. In addition, 79% accounted for those with household incomes amounting to over USD 100,000, and 74% were categorized as college graduates. Therefore, with such consumption and categorization, the sub-segment is continuously growing across nations.

Product Type Segment Analysis

During the forecast period, the spirits segment, which is part of the product type, is projected to grab the second-highest share in the luxury wines and spirits market. The segment’s growth is highly driven by its importance for ensuring inner peace, enabling personal growth, and offering guidance for effectively connecting human consciousness with higher, eternal, and divine realms. Based on government estimates published by the USDA in 2026, the overall valuation of spirits export amounted to USD 3.5 billion, along with USD 3.7 billion as a 3-year average. Besides, as of 2025, the total valuation of spirits was USD 1.3 billion, which is followed by USD 300.7 million for the UK, USD 208.1 million for Canada, USD 167.0 million for Japan, USD 156.8 million for Mexico, USD 148.2 million Australia, USD 130.9 million in South Korea, USD 90.3 million for Brazil, USD 82.5 million in Honduras, and USD 70.8 million. Therefore, based on these export valuations, along with past exports in previous years, the sub-segment is eventually growing.

Global Spirits Export Valuation in Past Years (2022-2024)

|

Countries |

2022 (USD) |

2023 (USD) |

2024 (USD) |

|

Europe |

936.9 million |

1.0 billion |

1.3 billion |

|

UK |

337.3 million |

272.6 million |

300.7 million |

|

Canada |

861.4 million |

759.7 million |

208.1 million |

|

Japan |

231.4 million |

217.7 million |

167.0 million |

|

Mexico |

154.5 million |

173.9 million |

156.8 million |

|

Australia |

158.5 million |

148.3 million |

148.2 million |

|

South Korea |

152.0 million |

132.2 million |

130.9 million |

|

Brazil |

54.4 million |

50.8 million |

90.3 million |

|

Honduras |

52.0 million |

46.4 million |

82.5 million |

|

United Arab Emirates |

54.1 million |

72.0 million |

70.8 million |

Source: USDA

Alcohol Content Segment Analysis

Based on the alcohol content, the 40% to 60% segment in the luxury wines and spirits market is expected to account for the third-highest share by the end of the stipulated timeline. The segment’s development is highly propelled by demonstrating a distinctive transition towards increased consumption and high-strength spirits, especially across developing economies, frequently ranging between 40% and 60% in terms of volume. Based on an article published by the OECD in November 2025, the per capita yearly alcohol consumption effectively averaged 8.5 litres of pure alcohol across different countries. Besides, as of 2023, 27% of the global population, aged over 15 years, demonstrated strong episodic drinking almost monthly across 27 economies. Therefore, with this increase in alcohol consumption, this particular segment is continuously expanding across different countries.

Our in-depth analysis of the luxury wines and spirits market includes the following segments:

|

Segment |

Subsegments |

|

End user |

|

|

Product Type |

|

|

Alcohol Content |

|

|

Distribution Channel |

|

|

Packaging Type |

|

|

Occasion/Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Luxury Wines and Spirits Market - Regional Analysis

Europe Market Insights

Europe in the luxury wines and spirits market is anticipated to garner the largest share of 35.6% by the end of 2035. The market’s upliftment in the region is highly driven by an in-depth cultural heritage in winemaking and spirits production, an increase in the preference for artisanal and premium craft products, along with an upsurge in the need for sustainable, biodynamic, and organic spirits and wines. According to official statistics published by the Europe Parliament in July 2023, the region comprises 2.2 million vineyard holdings, with a variety in size ranging from an average of 0.2 hectares in Romania to 10.5 hectares in France. In addition, the region also effectively accounted for 48% of worldwide wine consumption, with the large-scale consumption in Germany, Italy, and France. Moreover, the overall area under vines in the region catered to 3.2 million hectares, accounting for 2% of the used agricultural area, along 45% of total vine-growing locations in the world, thus bolstering the luxury wines and spirits market growth.

Overall Area Analysis Under Vines in Europe (2023)

|

Countries |

Area (1,000 Hectare) |

|

Spain |

911 |

|

France |

793 |

|

Italy |

689 |

|

Romania |

181 |

|

Portugal |

173 |

|

Denmark |

104 |

|

Greece |

103 |

|

Others |

180 |

|

Hungary |

62 |

Source: Europe Parliament

The luxury wines and spirits market in Germany is growing significantly, owing to an increase in wine import volume, the presence of an affluent customer base prioritizing premiumization, a rise in the demand for high-quality luxury and sparkling spirits, the centralized logistics center for regional spirits and wine distribution, and the robust preference for organic and sustainability certifications. As stated in an article published by the ITA in August 2025, the country is regarded as the third-largest wine importer by valuation and volume, with imports worth USD 2.8 billion as of 2024. Additionally, Spain, France, and Italy are notable suppliers of wine to the nation, with a combined import industrial share of 79%. Besides, in the same year, the overall domestic valuation of the country’s U.S.-based wines was worth USD 55 million, thereby denoting an optimistic outlook for the luxury wines and spirits market growth.

Overall Wine Industry Size Analysis in Germany (2022-2025)

|

Component |

2022 |

2023 |

2024 |

2025 |

|

Total Exports |

1,236 million liters |

1,307 million liters |

1,266 million liters |

1,210 million liters |

|

Total Imports |

3,069 million liters |

3,070 million liters |

2,847 million liters |

2,860 million liters |

|

Imports from the U.S. |

73 million liters |

59 million liters |

55 million liters |

30 million liters |

|

Exchange Rates |

1.05 |

1.08 |

1.08 |

1.07 |

Source: ITA

The existence of fine wine auctions, spirits investment, private client cellars, an increase in export demand for scotch whisky, the aspect of consumers demonstrating the highest adoption rate of e-commerce for luxury beverages, and the sophisticated wine investment ecosystem are certain factors responsible for bolstering the luxury wines and spirits market in the UK. As per an article published by the Scotch Whisky Association in February 2025, the government in the country successfully mitigated growing domestic pressures on the scotch industry, including diminished excise duty, with 70% of the average priced bottle presently collected in tax. Besides, based on the UK-India FTA communication, the industry called for a trade deal that included a reduction of the 150% tariff on scotch imports to India, leading to suitable export growth, which is positively uplifting the luxury wines and spirits market in the country.

APAC Market Insights

The Asia Pacific in the luxury wines and spirits market is expected to emerge as the fastest-growing region during the forecast period. The market’s development in the region is highly propelled by the increasing west-form of cultural influence, especially in Japan and China, a rise in disposable incomes, a boom in the e-commerce industry, focus on the premiumization trend, and the foreign recovery for duty-free retail and travel. According to a data report published by the APISWA Organization in July 2023, the region constitutes a flagship drink approach that drives a digitalized public awareness campaign, known as the Power of No, which has reached 40 million young adults of legal age, particularly in Vietnam and Thailand. Besides, according to the World Health Organization (WHO), unrecorded alcohol, which is not taxed and is not part of the suitable governmental system control, accounted for nearly 32% of the overall alcohol consumption in the region, thus proliferating the market development.

The luxury wines and spirits market in China is gaining increased traction, owing to the rapid and massive expansion of a base of high-net-worth individuals, an escalation in premiumization among urban millennials, a cultural transition toward foreign drinking habits, and the continuously growing influence of luxury branding and social media. As per an article published by NLM in January 2026, the alcohol utilization among domestic individuals aged more than 15 years ranged from 20.3% to 27.6%, with higher rates witnessed among males and young to middle-aged adult individuals. Additionally, more than 40% of present drinkers in the country are significantly engaged in aggressive episodic drinking. Likewise, the male population in the country demonstrated 44.5%, and the female population catered to 34.3%, thereby making it suitable for the market’s demand.

The aspects of the young demographic profile, increased urbanization, a relatively underpenetrated luxury beverage industry, government budget allocations, and an increase in the exposure to worldwide whisky and wine culture through foreign travel, premium hospitality, and social media are certain trends that are responsible for driving the luxury wines and spirits market in India. According to official statistics published by the IBEF Organization in May 2025, the alcohol beverage industry in the country is expected to record an 8% to 10% revenue growth by the end of 2026 and successfully reach USD 61.9 billion. This is readily developed on a yearly growth rate of 13% in the past 3 financial years. Based on this growth, the operating profitability is projected to improve by 60 to 80 basic points, which is further supported by the absence of large-scale debt-based capital and premiumization spending, which is positively fueling the luxury wines and spirits market development.

North America Market Insights

North America in the luxury wines and spirits market is projected to witness considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by a rise in disposable incomes among high-net-worth households, the presence of an in-depth entrenched culture of premiumization, robust preference for craft-based and authentic spirits and wines, an increase in digital engagement, and affluent demographics. Based on government estimates published by the USDA in May 2022, the growing wine consumption, particularly in the U.S., has positively contributed to an upsurge in wine imports, which have increased from 127 million gallons to 456 million gallons, thereby almost reaching USD 7.5 billion in valuation. Besides, the majority of wine imports derive from Europe, accounting for 75% of the overall valuation and 50% by volume. Moreover, the ongoing supply of wines from and to different regional economies is uplifting the luxury wines and spirits market exposure.

2024 Wine Export and Analysis in North America

|

Countries |

Export (USD) |

Import (USD) |

|

U.S. |

1.4 billion |

6.7 billion |

|

Canada |

77.2 million |

1.9 billion |

|

Dominican Republic |

9.7 million |

84.7 million |

|

Mexico |

8.8 million |

334 million |

|

Jamaica |

6.4 million |

8.6 million |

|

Panama |

2.3 million |

35.9 million |

Source: OEC

The luxury wines and spirits market in the U.S. is gaining increased exposure, owing to the increased demand for authenticity and premium limited-edition offerings, a transition toward home consumption and off-trade retail, affluent consumers' needs despite mindful drinking habits, and a focus on technological and sustainability innovation. As per a data report published by the U.S. Department of the Treasury in February 2022, at present, there are more than 6,400 operating breweries in the country, denoting an increase from only 89, along with over 6,600 operating wineries and 1,900 operating distilleries. Besides, two breweries have readily dominated the domestic economy and currently cater to an approximate 65% of the global beer industry as measured in terms of revenue. Therefore, with the increased availability of such facilities, there is a huge demand for the market in the country.

The presence of robust premiumization trends as a cost-effective luxury, an increase in urban affluence and disposable incomes, a sudden transition toward experiential consumption and wine culture, along with e-commerce accessibility, and a young demographic impact are responsible for fueling the luxury wines and spirits market in Canada. As stated in an article published by the Statisque Canada in March 2026, provincial and federal governments significantly earned USD 15.5 billion from the sale and control of alcohol, which is worth USD 13.1 billion in March 2025. This effectively included net income from cannabis and provincial liquor authorities, retail sales taxes, excise taxes, and other specified taxes. Besides, liquor authorities and retail outlets sold USD 25.8 billion worth of alcoholic beverages, leading to a decrease in sales, despite the 1.6% increase in alcoholic beverage prices. Moreover, standard drinks based on the legal drinking age are also contributing to the luxury wines and spirits market growth in the country.

Standard Drinks Analysis based on Legal Drinking Age in Canada (2014-2024)

|

Year |

Beer |

Spirits |

Wines |

Ciders, Colers, and Other Rfreshment Beverages |

|

2014 |

4.4 |

2.4 |

2.4 |

0.3 |

|

2015 |

4.4 |

2.4 |

2.5 |

0.4 |

|

2016 |

4.3 |

2.5 |

2.5 |

0.4 |

|

2017 |

4.2 |

2.5 |

2.5 |

0.4 |

|

2018 |

4.1 |

2.5 |

2.4 |

0.5 |

|

2019 |

4.0 |

2.5 |

2.5 |

0.5 |

|

2020 |

3.9 |

2.6 |

2.5 |

0.7 |

|

2021 |

3.7 |

2.6 |

2.4 |

0.8 |

|

2022 |

3.6 |

2.6 |

2.2 |

0.8 |

|

2023 |

3.4 |

2.4 |

2.1 |

0.8 |

|

2024 |

3.1 |

2.2 |

1.9 |

0.8 |

Source: Government of Canada

Key Luxury Wines and Spirits Market Players:

- Diageo Plc (UK)

- Pernod Ricard (France)

- LVMH (Moët Hennessy) (France)

- Brown-Forman Corporation (UK)

- Bacardi Limited (UK)

- Campari Group (Italy)

- Edrington Group (UK)

- William Grant & Sons (UK)

- ThaiBev (Thailand)

- Sazerac Company (U.S.)

- Heaven Hill Distilleries (U.S.)

- Constellation Brands (U.S.)

- The Wine Group (U.S.)

- Suntory Holdings Limited (Japan)

- Asahi Group Holdings (Japan)

- Treasury Wine Estates (Australia)

- Accolade Wines (Australia)

- United Spirits Limited (India)

- Radico Khaitan (India)

- The Wine Shop (Malaysia)

- GALLO (U.S.)

- TOPPAN Digital Inc. (Japan)

- Piccadilly Distilleries (India)

- WX Brans (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- Diageo Plc commands a powerful portfolio of super-premium spirits brands that are staples in luxury bars and high-end gifting circuits globally. The company consistently leverages its scale to innovate with limited-edition releases and exclusive travel retail offerings that cater to affluent collectors.

- Pernod Ricard maintains a strong position in the luxury segment through its prestigious collection of heritage cognacs and single malts. The company focuses on immersive brand experiences and artisanal storytelling to deepen engagement with discerning high-net-worth consumers.

- LVMH (Moët Hennessy) benefits from an unmatched association with high fashion and exclusivity. The company integrates its wine and spirits offerings with its broader luxury ecosystem, including bespoke hotel and resort experiences.

- Brown-Forman Corporation excels in the premium America-based whiskey segment, leveraging its deep heritage to command loyalty among connoisseurs. The company drives desirability through meticulous barrel-selection programs and age-statement releases that appeal to serious investors.

- Bacardi Limited has cultivated a strong presence in the luxury rum and premium vodka categories through strategic acquisitions and family-led brand stewardship. The company prioritizes sustainability and craftsmanship in its super-premium lines to attract eco-conscious luxury buyers.

Here is a list of key players operating in the global luxury wines and spirits market:

The global luxury wines and spirits market remains highly concentrated, with Europe-headquartered players, particularly Diageo in the UK, along with Pernod Ricard and LVMH in France, dominating the premium and prestige segments. These leaders are pursuing strategic consolidation to defend market share amid softening U.S. and China demand. Recent merger discussions between Pernod Ricard and Brown-Forman from the U.S. signal a major shift toward creating a spirits colossus to better compete with Diageo. Besides, in January 2025, GALLO effectively entered into a deal with Spritz Society to extend the brand’s retail distribution for its line of products. This particular expanded distribution deal kicked off across Florida, Texas, Illinois, and South Carolina, which was followed by a nationwide expansion across different retail stores, thereby making it suitable for bolstering the luxury wines and spirits market worldwide.

Corporate Landscape of the Luxury Wines and Spirits Market:

Recent Developments

- In October 2025, TOPPAN Digital Inc. introduced secured NFC tags for opening detection and authenticity verification, along with ID authentication platforms as the latest IoT-based solutions to the luxury industry, especially in Europe.

- In September 2025, Piccadilly Distilleries introduced CASHMIR vodka, which significantly marked the newest chapter for the spirits industry in India by undergoing a 7x distillation for unparalleled purity, along with a 5x precision filtration through activated mango and carbon charcoal, as well as silver, gold, and platinum layers.

- In June 2025, WX Brans unveiled Here By Chance, which is the latest Paso Robles Cabernet Sauvignon that is focused on spontaneity, while significantly delivering outstanding quality.

- Report ID: 8513

- Published Date: Apr 14, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.