Low GWP Refrigerants Market Outlook:

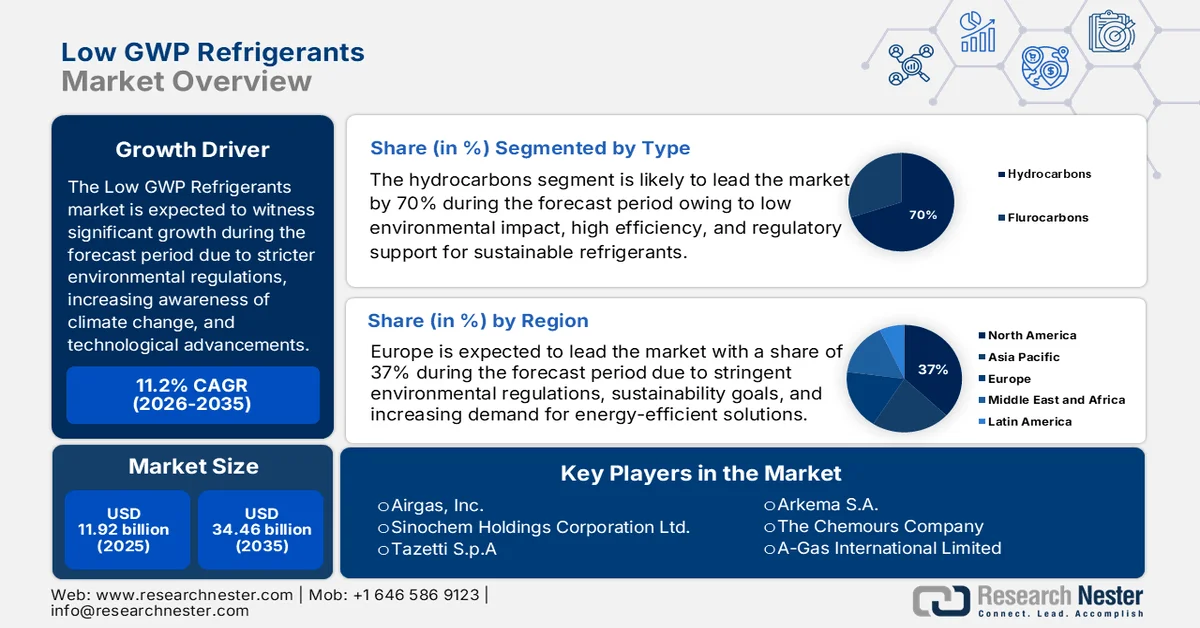

Low GWP Refrigerants Market size was over USD 11.92 billion in 2025 and is anticipated to cross USD 34.46 billion by 2035, witnessing more than 11.2% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of low GWP refrigerants is estimated at USD 13.12 billion.

The reason behind the growth is impelled by the rising demand for air conditioners for homes and workplaces. The change in climate during summer increases the temperature of the climate and to reduce this heat people buy air conditioners, and cooling fans as air conditioners reduce the heat inside the room by circulating cool air. Even companies buy air conditioners to maintain the temperature of the rooms and the systems i.e. computers and CPUs.

According to statistics, there are more than 1 billion heating, ventilation, and air conditioning (HVAC) units worldwide, and this number will increase by over 5 million by 2030.

The rising concern about global warming is believed to fuel the market growth. Hydrochlorofluorocarbon (HCFC) and chlorofluorocarbons (CFC) are two substances with high GWPs that can trap heat in the lower temperature resulting in climate change and global warming. As a result, there has been a shift in consumer preference for appliances with low GWP refrigerants such as carbon dioxide, ammonia, hydrocarbons, and HFOs as they are more environmentally friendly and have lower global warming potential. For instance, wealthy countries have produced the majority of the world's HFC emissions, which are anticipated to increase threefold by 2030.

Key Low GWP Refrigerants Market Insights Summary:

Regional Highlights:

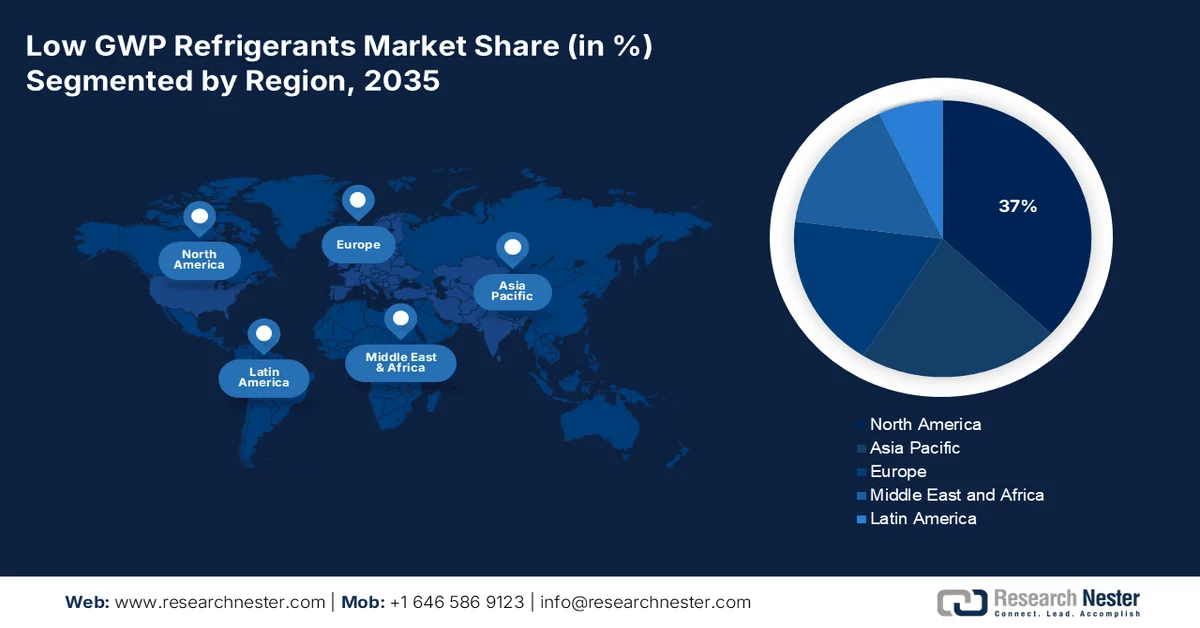

- Europe in the low GWP refrigerants market is projected to command the largest share of 37% by 2035, driven by growing government initiatives to eliminate the utilization of HFC refrigerants.

- Asia Pacific is anticipated to emerge as the second largest region by 2035, fueled by international commitments to reduce greenhouse gas emissions.

Segment Insights:

- The hydrocarbons segment of the low GWP refrigerants market is projected to account for approximately 70% share by 2035, propelled by the growing demand from the industrial sector.

- The commercial refrigeration segment is anticipated to secure a notable share by 2035, stimulated by the increasing production of cold storage food items across the world.

Key Growth Trends:

- Higher Utilization in the A/C System of Vehicles

- Developing Cold Chain Logistics System

Major Challenges:

- Harmful Effects of Low GWP Refrigerants

- Lack of Awareness about the Benefits of Low GWP Refrigerants

Key Players: Pfizer Inc., Cardinal Health Inc., NxThera, Inc., Veru, Inc., Teleflex Incorporated, Eli Lily & Company, Sanofi S.A., GSK plc, Mylan N.V., AbbVie Inc.

Global Low GWP Refrigerants Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 11.92 billion

- 2026 Market Size: USD 13.12 billion

- Projected Market Size: USD 34.46 billion by 2035

- Growth Forecasts: 11.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Europe (37% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, France

- Emerging Countries: China, India, Japan, South Korea, Thailand

Last updated on : 25 February, 2026

Low GWP Refrigerants Market - Growth Drivers and Challenges

Growth Drivers

- Higher Utilization in the A/C System of Vehicles– Luxury cars are highly in demand Y-O-Y in the modern world and the air conditioning system is becoming mandatory in cars to regulate the temperature, humidity, and airflow.

A refrigerant used in vehicles' air conditioning systems makes a significant contribution to the greenhouse effect and to reduce this effect low-GWP refrigerants such as HFO-1234yf are used in the air conditioning systems which could greatly lessen the total equivalent warming impact.

According to data, over 70% of hydrofluorocarbon (HFCs) released globally come from the motor vehicle air conditioning, AC, and refrigeration industries.

- Developing Cold Chain Logistics System- The cold chain depends on refrigerants, and the adoption of low-carbon refrigeration technology is expected to be the main factor in creating a greener cold chain sector by reducing carbon dioxide (CO2) emissions.

Challenges

-

Harmful Effects of Low GWP Refrigerants– Low GWP refrigerants are estimated to cause harmful effects on the environment therefore, people are choosing refrigerants with less toxicity, high performance, battery efficiency, low volumetric capacity, and ecofriendly product. This, as a result, is anticipated to hinder the growth of the market.

- Lack of Awareness about the Benefits of Low GWP Refrigerants

- Complex Transformation Procedure from High to Low GWP Refrigerants

Low GWP Refrigerants Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.2% |

|

Base Year Market Size (2025) |

USD 11.92 billion |

|

Forecast Year Market Size (2035) |

USD 34.46 billion |

|

Regional Scope |

|

Low GWP Refrigerants Market Segmentation:

Type (Fluorocarbons, Hydrocarbons)

The hydrocarbons segment in the low GWP refrigerants market is estimated to gain a robust revenue share of about 70% in the coming years owing to the growing demand from the industrial sector. Hydrocarbons such as propane and isobutane are affordable, simple to acquire, and are frequently utilized as refrigerants in the industrial sector.

These refrigerants can be used for cooling industrial spaces since they provide efficient cooling performance and reduce the carbon footprint of the cooling systems. In addition, owing to their high-efficiency performance they have applications in chemical manufacturing and pharmaceutical processing.

Application (Commercial, Domestic, Industrial Refrigeration)

The commercial refrigeration segment in the low GWP refrigerants market is set to garner a notable share shortly owing to the increasing production of cold storage food items across the world. The commercial usage of refrigerators includes usage for storage of food, dairy products, juices, and frozen food, among others is necessary for preserving and distributing food while maintaining food nutrients. In many retail food refrigeration applications, refrigerants provide the best combination of efficiency, environmental friendliness, and safety, also help in maintaining near-zero downtime of the store applications, and reduce food losses by maintaining the precise temperature.

Moreover, international food companies encourage the use of propane refrigerant systems, and commercial refrigerators use the more recent hydrocarbon refrigerant R290 since it is becoming a favored refrigerant. For instance, switching to low GWP alternatives can significantly slow the rate of global warming as huge refrigeration systems can retain thousands of pounds of HFCs and frequently leak at a rate of over 18% per year. According to estimates, in 2022, frozen food sales in the United States reached over USD 70 billion.

Our in-depth analysis of the global market includes the following segments:

|

Type |

|

|

Application |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Low GWP Refrigerants Market - Regional Analysis

European Market Forecast

Europe industry is estimated to hold largest revenue share of 37% by 2035. impelled by the growing government initiatives to eliminate the utilization of HFC refrigerant. The European Parliament has set regulations such as fluorinated greenhouse gases (F-Gas) Regulation to prohibit the use of refrigerants with a global warming potential of more than 2500.

Under this regulation users of refrigeration and air conditioning equipment are subject to legal obligations and to primarily focus on preventing system leaks to reduce emissions. Further, the F-Gas regulation in Europe promotes the adoption of low GWP refrigerants and aims to reduce the EU's F-gas emissions by two-thirds in 2030.

Besides this, The EU's "Green Deal" is a European Commission's strategy to promote a circular economy, to make the EU carbon-neutral by 2050.

APAC Market Statistics

The Asia Pacific low GWP refrigerants market is estimated to be the second largest, during the forecast timeframe led by its international commitments to reduce greenhouse gas emissions. India joined the Kigali Agreement, to eliminate hydrofluorocarbons (HFCs), dangerous greenhouse gases used in air conditioning and refrigeration, and the country is expected to reduce its usage of HFCs by more than 80% by 2047.

In addition, in 2022 the Kigali Amendment (KA) to the Montreal Protocol has been ratified by Singapore, making it the 134th nation to reduce its HFC consumption by 80% over the following 20 years.

Low GWP Refrigerants Market Players:

- Linde Plc

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Airgas, Inc.

- Sinochem Holdings Corporation Ltd.

- Tazetti S.p.A

- Arkema S.A.

- The Chemours Company

- A-Gas International Limited

- Shandong Yuan Chemical Industry Co., Ltd.

- Harp International Ltd.

- Honeywell International Inc.

Recent Developments

- Honeywell International Inc. launched New Low-Global-Warming-Potential Refrigerant Solstice N71 (R-471A) a refrigerant for commercial and industrial refrigeration to provide a quick lifeline to supermarkets, and to become carbon neutral while accelerating efforts to address climate change.

- Linde Plc to announce a significant event of a long-term agreement for the supply of industrial gases with Mims, which is constantly working for the expansion of production capacity by 50%.

- Report ID: 4167

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.