Lidocaine Market Outlook:

Lidocaine Market size was valued at USD 2.7 billion in 2025 and is anticipated to surpass a value of USD 4.3 billion by 2035, expanding at a CAGR of 5.4% during the forecast period from 2026 to 2035. In 2026, the industry size of lidocaine is assessed at USD 2.8 billion.

The global lidocaine market is experiencing steady expansion owing to the rising demand for efficient and rapid-acting local anesthetics across various medical applications. The market is benefitting from increased surgical volumes and a shift towards minimally invasive interventions. According to the article published by the International Society of Aesthetic Plastic Surgery (ISAPS) in June 2024, 34.9 million aesthetic procedures were performed globally in 2023, with total surgical and non-surgical procedures increasing 3.4%. Besides, surgical procedures rose 5.5% to over 15.8 million, whereas liposuction was the most common surgical procedure, and all face and head procedures also witnessed notable growth. The U.S. and Brazil led in total procedures, with surgeries primarily conducted in hospitals and office facilities, reflecting a huge necessity for lidocaine.

Furthermore, the expanding geriatric population requiring chronic pain management and the surge in adoption of non-opioid pain protocols stimulate consistent growth in the lidocaine market. According to the article published by the World Health Organization (WHO) in October 2025, global population ageing is growing at a rapid pace, with the number of people aged 60 and older projected to rise from 1 billion in 2020 to 2.1 billion by 2050, and 80% of older adults will be living in low- and middle-income nations. Moreover, the article highlighted that ageing involves complex biological, social, and environmental factors, which in turn can lead to increased prevalence of chronic diseases, geriatric syndromes, and multi-morbidity. Therefore, from a strategic perspective, the rising aging demographics create a sustained demand base for local anesthetics such as lidocaine, particularly in terms of outpatient and long-term care settings where non-opioid pain management is prioritized.

Key Lidocaine Market Insights Summary:

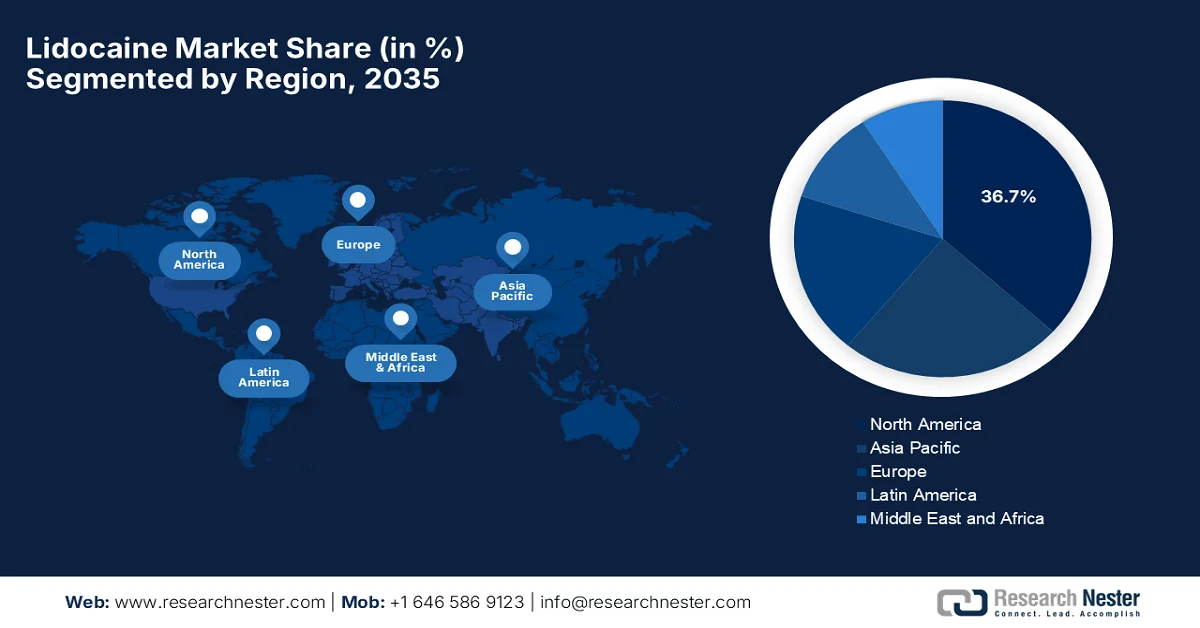

Regional Highlights:

- North America lidocaine market is projected to capture 36.7% share by 2035, supported by advanced healthcare systems and rising outpatient procedures alongside innovations in delivery systems

- Asia Pacific is anticipated to witness the fastest expansion in the market over 2026–2035, propelled by increasing healthcare investments and growing medical tourism demand

Segment Insights:

- In the lidocaine market, the injectable formulation segment is estimated to secure a 42.6% share by 2035, attributed to its extensive utilization across surgical, dental, and emergency care settings requiring rapid anesthesia

- Dentistry application segment is expected to attain a notable share during 2026–2035, fueled by the widespread reliance on lidocaine for routine and surgical dental procedures

Key Growth Trends:

- Expanding pain management needs

- Technological advancements in delivery systems

Major Challenges:

- Safety concerns and side effects

- Supply chain and raw material constraints

Key Players: Pfizer Inc. (U.S.), Baxter International Inc. (U.S.), Endo International plc (Dublin), Amneal Pharmaceuticals LLC (U.S.), Viatris Inc. (U.S.), SCILEX Holding Company (U.S.), Sorrento Therapeutics, Inc. (U.S.), Medline Industries, Inc. (U.S.), Teva Pharmaceutical Industries Ltd. (Israel), Fresenius SE & Co. KGaA (Germany), AstraZeneca plc (UK), China Medical System Holdings Limited (China), Hikma Pharmaceuticals PLC (UK), Sandoz International GmbH (Switzerland), Shandong Chenghui Pharmaceutical Group Co., Ltd (China), Boehringer Ingelheim GmbH (Germany), Hisamitsu Pharmaceutical Co., Inc. (Japan), Teikoku Pharma Co., Ltd. (Japan), Avenacy (U.S.), Zydus Lifesciences (India), Huons Global (South Korea), Aspen Pharmacare Holdings Limited (South Africa), Sun Pharmaceutical Industries Ltd. (India), Teikoku Pharma USA, Inc. (U.S.), Glenmark Pharmaceuticals Ltd. (India), Kotra Pharma (M) Sdn Bhd (Malaysia).

Global Lidocaine Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 2.7 billion

- 2026 Market Size: USD 2.8 billion

- Projected Market Size: USD 4.3 billion by 2035

- Growth Forecasts: 5.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (36.7% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, China, Japan, India

- Emerging Countries: South Korea, Brazil, Mexico, Thailand, Indonesia

Last updated on : 26 March, 2026

Lidocaine Market - Growth Drivers and Challenges

Growth Drivers

- Expanding pain management needs: The increasing burden of chronic and acute pain conditions, such as arthritis, neuropathy, and back pain, is effectively driving therapeutic use of lidocaine for nerve pain and chronic pain relief. In this context, the June 2023 WHO article revealed that approximately 18 million people worldwide were living with rheumatoid arthritis in a year, about 70% are women, and 55% are aged above 55. Besides, the report also underscored that around 13 million individuals experience moderate to severe symptoms that could benefit from rehabilitation. The disease most commonly affects the joints of the hands, wrists, feet, ankles, knees, shoulders, and elbows, contributing to chronic pain, denoting a huge potential for the overall lidocaine market in the years ahead.

- Technological advancements in delivery systems: The continued innovations in terms of sustained-release formulations, liposomal technology, and microneedle patches enhance therapeutic efficiency and ease of use. These advancements contribute to the expansion of the overall lidocaine market. In September 2025, the U.S. Food and Drug Administration (FDA) approved Bondlido (lidocaine topical system) 10% under NDA 215029 for the relief of pain associated with post-herpetic neuralgia in adults. Besides this, the particular approval was followed by a complete response submission by MEDRx U.S., Inc., reflecting innovations in topical delivery systems that improve adhesion, localized drug release, and patient comfort. Hence, the regulatory support, coupled with continued technological advancements in lidocaine delivery, is readily enhancing therapeutic efficiency and expanding its clinical applications.

- Growth in cardiac care applications: Lidocaine serves as an effective anti-arrhythmic agent. Therefore, its use in hospital settings for cardiac care contributes significantly to the lidocaine market growth. In October 2023, a National Institute of Health (NIH) study found that lidocaine, which is a class Ib anti-arrhythmic, is primarily effective for ventricular arrhythmias by blocking sodium channels, shortening action potential duration, and increasing the refractory period, particularly in ischemic tissue. It has regained focus for acute, sustained ventricular tachyarrhythmias, whereas clinical studies show lidocaine can terminate refractory ventricular arrhythmias, often in combination with amiodarone. Current international guidelines position lidocaine as a second-line therapy for shock-refractory ventricular tachycardia and for acute coronary syndrome-related arrhythmias.

Challenges

- Safety concerns and side effects: Lidocaine is associated with side effects such as allergic reactions, cardiovascular complications, and neurological symptoms if used improperly. Therefore, the rising awareness of the side effects can impact the prescription rates among healthcare professionals and patient acceptance. On the other hand, the aspects of reported safety incidents can affect regulatory scrutiny, thereby creating financial and reputational risks for manufacturers who are operating in the lidocaine market. In this context, companies need to make heavy investments in clinical testing and patient education to ensure safe usage. These safety concerns also limit the scope for over-the-counter availability in some regions, further constraining market expansion.

- Supply chain and raw material constraints: The lidocaine market is mainly dependent on continued supply chains for active pharmaceutical ingredients as well as excipients. Therefore, any disruptions due to geopolitical tensions or pandemic-related restrictions can cause delays to production along with distribution. The aspect of fluctuations in raw material costs, especially in terms of pharmaceutical-grade chemicals, can negatively affect pricing and profitability. Manufacturers face pressure to maintain consistent quality while managing these supply concerns. Dependency on a low number of API suppliers increases vulnerability to shortages. Therefore, companies in this field need to implement supply chain management, diversify sourcing, and maintain buffer inventories to mitigate supply risks.

Lidocaine Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

5.4% |

|

Base Year Market Size (2025) |

USD 2.7 billion |

|

Forecast Year Market Size (2035) |

USD 4.3 billion |

|

Regional Scope |

|

Lidocaine Market Segmentation:

Formulation Segment Analysis

The injectable, which is under the formulation segment, is anticipated to gain the largest share of 42.6% in the lidocaine market during the forecast period. The dominance of the segment is largely attributable to its extensive use in surgical procedures, dental applications, and emergency settings requiring rapid local anesthesia. For instance, in February 2026, Galderma announced that regulatory authorities in the EU, U.S., and Canada approved its next-generation Restylane syringe for use with NASHA lidocaine-based injectable products across multiple facial and hand indications. The company also notes that this redesigned syringe is developed with aesthetic practitioners, enhances precision, control, and comfort through ergonomic features, thereby supporting consistent and high-quality injection outcomes, hence denoting a wider segment scope.

Application Segment Analysis

In the application segment, dentistry is expected to grow with a considerable share in the lidocaine market over the forecasted years. The segment’s growth is largely driven by widespread use of lidocaine as a local anesthetic in dental procedures such as surgeries, cavity treatments, and routine oral care. In March 2025, the study published by the American Journal of Emergency Medicine provided proven recommendations for managing acute dental pain in emergency departments, hospitals, and urgent care settings where definitive dental treatment is not immediately available. Besides, this study emphasized the use of short-acting local anesthetics, including lidocaine, along with NSAIDs and acetaminophen for post-operative pain after simple or surgical tooth extractions. Thus, such evidence-based studies are solidifying lidocaine’s role as a safe, effective, and standard pharmacological option for managing acute dental pain.

Distribution Channel Segment Analysis

By the conclusion of the forecast period, hospital pharmacies in the distribution channel segment are predicted to account for a significant revenue share in the lidocaine market. The high volumes of surgical procedures, emergency care, and specialized interventions are the key factors that are responsible for uplifting the overall subtype’s growth and exposure. Lidocaine is extensively used and purchased from hospital pharmacies for rapid local anesthesia during minor and major surgeries, dental procedures, and catheter-based interventions. In addition, its proven efficacy in managing cardiac arrhythmias, particularly ventricular tachycardia, underscores its critical presence in inpatient care. Furthermore, hospital pharmacies ensure reliable availability of lidocaine, thereby supporting both scheduled procedures and urgent, emergency applications, which makes them the foundation for the global lidocaine supply chain.

Our in-depth analysis of the lidocaine market includes the following segments:

|

Segment |

Subsegments |

|

Formulation |

|

|

Application |

|

|

Distribution Channel |

|

|

Type |

|

|

Route of Administration |

|

|

End user |

|

|

Strength |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Lidocaine Market - Regional Analysis

North America Market Insights

The North America lidocaine market is forecasted to emerge as the largest landscape with a share of 36.7% during the discussed timeframe. The region’s dominance is effectively fueled by its advanced healthcare system and high outpatient procedures. Growth is also bolstered by the rising regulatory support and innovations in delivery systems, such as advanced transdermal patches and long-acting injectables. For instance, in May 2023, the U.S. Food and Drug Administration (FDA) approved Restylane Eyelight (P040024/S135), which is a hyaluronic acid–based dermal filler containing 0.3% lidocaine to reduce injection-related pain. The approval allows its use for improving the appearance of sunken or hollow areas under the eyes, i.e., infraorbital hollowing in adults aged 21 and older, hence making it suitable for standard lidocaine market growth.

A rise in dental procedures and wider adoption of cosmetic treatments is boosting the U.S. lidocaine market. Robust research and development efforts and the presence of major pharmaceutical players are also the key factors supporting market expansion. In addition, the growing availability of over-the-counter lidocaine products and generic formulations is enhancing accessibility for consumers, efficiently contributing to the country’s leading market position in the region. In this context, Armas Pharmaceuticals in April 2025 announced the reintroduction of Lidocaine Jelly 2% 30mL to the U.S. lidocaine market after more than two years of unavailability, thereby addressing a supply gap for healthcare providers. Besides, the company notes that the topical anesthetic is used in urological and endoscopic procedures to provide localized pain relief, thus highlighting its importance in clinical practice.

The lidocaine market in Canada is propelled by the rising number of ambulatory surgery centers (ASCs), which offer cost-effective alternatives for minor outpatient procedures where local anesthetics are essential. The competitive environment in the country is reshaped by the presence of both global pharmaceutical giants and domestic players, with recent regulatory approvals that are helping to address supply shortages. In April 2025, NIH analyzed the safety of outpatient ASCs in the country by reviewing 2,596 aesthetic surgery patients at a single ASC in Ontario. In this context, results showed a very low complication rate of 2.4%, with only 0.4% requiring hospital resources postoperatively, demonstrating that same-day discharge procedures in the country’s ASCs are safe. Therefore, this study highlights the prominence of ASCs in Canada, supporting increased utilization of local anesthetics such as lidocaine for outpatient procedures.

APAC Market Insights

The Asia Pacific lidocaine market is expected to register the fastest growth from 2026 to 2035. The region’s growth is mainly propelled by significant investments in healthcare infrastructure across emerging economies. There has been a rising popularity of medical tourism and aesthetic dermatology treatments, which is boosting the consumption of topical and injectable anesthetics in this region. According to the official statistics by the World Bank in January 2025, Thailand leads in terms of cosmetic surgery, dental care, and cardiac treatments, which attracted more than 3 million medical tourists and USD 600 million in a year. Besides, the report also noted that India emphasizes complex surgeries such as transplants and orthopedics, supported by its e-Medical Visa and Heal in India campaign, thereby attracting 476,000 foreign patients in 2023, hence denoting a huge growth potential for lidocaine in the region.

The China lidocaine market is emerging as the strongest market in this region due to the insatiable demand for surgical and dental anesthesia. The fundamental growth drivers for the country’s market are regulatory support, significant government investment in healthcare infrastructure, and the rising popularity of dermal fillers and laser treatments, which utilize topical lidocaine for pain management. In May 2024, Teikoku Pharma USA received the NMPA approval for Lidoderm, which is a 5% lidocaine hydrogel patch, for treating post-herpetic neuralgia. The product, licensed to Link Healthcare Group, and it provides a topical, non-systemic pain relief option with a 12-hour on/off schedule, allowing up to three patches at once. Hence, from a strategic perspective, such instances in the country highlight encouraging opportunities for pharmaceutical companies to introduce innovative lidocaine-based products and expand lidocaine market penetration in both surgical and cosmetic segments.

The huge volume of dental, ophthalmic, and minor surgical procedures is responsible for uplifting the lidocaine market in India. As the country expands its healthcare infrastructure and increases access to medical services in both urban and rural areas, the demand for cost-effective local anesthetics also rises at a notable pace. According to the article, which was published by Press Information Bureau (PIB) in August 2023 under the National Programme for Control of Blindness and Visual Impairment in the country, the mission-mode cataract surgery campaign conducted a total of 8,344,824 cataract surgeries in the financial year 2022‑23, which rapidly exceeded the target of 7,500,000 surgeries. The article underscores that this initiative aimed to reduce avoidable blindness to 0.25% by 2025 and was supported by state-level funding. Hence, the growing ophthalmic surgical procedures are efficiently driving the increased utilization of lidocaine in India.

Europe Market Insights

A primary emphasis on patient safety and the widespread adoption of non-opioid pain management strategies are driving the overall lidocaine market in Europe. Market’s development is sustained by strategic partnerships between leading players, an aging population requiring frequent chronic pain interventions, and a focus on high-purity formulations. For instance, in June 2024, Aspen Pharma Ireland entered into a licensing agreement with Wooshin Labottach for Lidocaine 700mg medicated plasters in selected markets of Europe. These plasters provide symptomatic relief of neuropathic pain linked to post-herpetic neuralgia in adults, whereas this partnership strengthens the company’s position in Europe and the Middle East. Hence, with such tactical strategies, the region is positioned to enhance patient access to effective topical anesthetics and solidify the regulatory-backed growth of lidocaine-based products.

The lidocaine market in Germany is positioned for sustained growth in the upcoming years, owing to rising surgical volumes, continuously upgrading healthcare infrastructure, and a strategic clinical shift toward regional anesthesia to reduce reliance on systemic opioids. Domestic manufacturers in the country continue to lead in developing advanced delivery systems, such as extended-release injectables and high-adhesion transdermal patches. The Federal Statistical Office of Germany stated that in 2023, hospitals in the country reported the 20 most frequent full inpatient surgeries based on diagnosis-related groups statistics, covering all hospitals billing under the DRG system in accordance with the Hospital Compensation Act (KHEntgG). Among the top twenty procedures, other surgeries on the intestine accounted for 386,048 procedures, access to the lumbar spine for 346,903, and reconstruction of female genitalia post-partum for 339,263. Additional common procedures included endoscopic bile duct surgery 290,454, and Caesarean sections 252,209. This data reflects the high surgical volume that drives demand for anesthetics such as lidocaine in Germany.

Frequent Inpatient Surgeries in Germany 2023 - OPS Code Statistics & Procedure Volumes

|

OPS Code |

Surgery |

Number of Surgeries |

|

|

Total surgeries |

16,531,491 |

||

|

5-469 |

Intestine surgery |

386,048 |

|

|

5-032 |

Lumbar spine access |

346,903 |

|

|

5-758 |

Female genital reconstruction |

339,263 |

|

|

5-513 |

Bile duct endoscopic surgery |

290,454 |

|

|

5-820 |

Hip joint prosthesis |

273,737 |

|

|

5-749 |

Caesarean section |

252,209 |

|

|

5-794 |

Fracture repositioning with osteosynthesis |

241,174 |

|

|

5-822 |

Knee joint prosthesis |

229,551 |

|

|

5-839 |

Spine surgery |

220,696 |

|

|

5-896 |

Skin tissue debridement |

216,854 |

|

|

5-452 |

Large intestine excision |

212,465 |

|

|

5-511 |

Cholecystectomy |

201,602 |

|

|

5-916 |

Soft tissue covering |

190,743 |

|

|

5-790 |

Fracture/epiphysiolysis reposition |

171,251 |

|

|

5-900 |

Skin surface restoration |

170,724 |

|

|

5-800 |

Joint revision |

167,933 |

|

|

5-530 |

Inguinal hernia repair |

158,895 |

|

|

5-83b |

Spine osteosynthesis |

155,883 |

|

|

5-895 |

Skin tissue excision |

152,010 |

|

|

5-831 |

Disc tissue excision |

146,149 |

|

A highly centralized procurement strategy of the National Health Service (NHS) accelerates growth in the UK lidocaine market as it prioritizes large-scale availability of essential local anaesthetics. The market also sees a distinct rise in the use of medicated plasters specifically for post-viral nerve pain, reflecting a clinical preference for targeted, non-systemic treatments in the country's aging demographic. In June 2024, NHS Somerset ICB issued a Patient Group Direction, which authorizes HCPC-registered physiotherapists to administer lidocaine hydrochloride 1% and 2% injections for intra-articular or extra-articular musculoskeletal lesions across GP practices and commissioned services. These guidelines will be valid until November 2026, and it includes measures for record-keeping, adverse event reporting, and patient consent, hence making it suitable for standard market growth.

Key Lidocaine Market Players:

- Pfizer Inc. (U.S.)

- Baxter International Inc. (U.S.)

- Endo International plc (Dublin)

- Amneal Pharmaceuticals LLC (U.S.)

- Viatris Inc. (U.S.)

- SCILEX Holding Company (U.S.)

- Sorrento Therapeutics, Inc. (U.S.)

- Medline Industries, Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Fresenius SE & Co. KGaA (Germany)

- AstraZeneca plc (UK)

- China Medical System Holdings Limited (China)

- Hikma Pharmaceuticals PLC (UK)

- Sandoz International GmbH (Switzerland)

- Shandong Chenghui Pharmaceutical Group Co., Ltd (China)

- Boehringer Ingelheim GmbH (Germany)

- Hisamitsu Pharmaceutical Co., Inc. (Japan)

- Teikoku Pharma Co., Ltd. (Japan)

- Avenacy (U.S.)

- Zydus Lifesciences (India)

- Huons Global (South Korea)

- Aspen Pharmacare Holdings Limited (South Africa)

- Sun Pharmaceutical Industries Ltd. (India)

- Teikoku Pharma USA, Inc. (U.S.)

- Glenmark Pharmaceuticals Ltd. (India)

- Kotra Pharma (M) Sdn Bhd (Malaysia)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Pfizer Inc is identified as the leading player in this field, which leverages a strong global footprint and diversified portfolio of injectable and hospital-use anesthetics. The company is highly focused on maintaining a strong position through consistent supply and lifecycle management of essential drugs, which includes local anesthetics.

- Teva Pharmaceutical Industries Ltd is considered to be a dominant force in the generics sector of the market with its cost-efficient production and extensive global distribution network. The firm concentrates mostly on affordability and accessibility, particularly in emerging markets.

- Fresenius SE & Co. KGaA is a prominent player that specializes in injectable formulations, including lidocaine, and benefits from strong integration with hospital supply chains. Besides, the firm’s growth strategy includes expanding sterile injectables production and strengthening its presence in critical care and anesthesia.

- Hisamitsu Pharmaceutical Co., Inc. leads in terms of transdermal drug delivery systems, including lidocaine patches. The company differentiates itself through innovation in topical formulations and strong R&D capabilities, allowing it to maintain a leading position in the lidocaine market.

- Sun Pharmaceutical Industries Ltd. is a major contributor to the market, i.e., through its extensive generics portfolio and cost-effective manufacturing. The company has a strong presence in emerging economies, and it continues to expand in regulated markets.

Below is the list of some prominent players operating in the global lidocaine market:

The lidocaine market hosts both pharmaceutical giants and regional generics manufacturers who are intensely competing in terms of pricing, continued innovations, and distribution reach. The leading pioneers, such as Pfizer, Teva, and Fresenius, benefit from their strong product portfolios and global supply chains, whereas players from the Asia Pacific are focused on cost-efficient production. Distribution partnerships and capacity expansion to enhance geographic presence are a few tactical strategies pursued by players in this field. Companies are also investing in advanced drug delivery systems and high-purity APIs to differentiate offerings. In February 2026, China Medical System Holdings Limited signed an agreement with Teikoku Pharma USA, Inc. for the distribution of Lidoderm lidocaine cataplasms in mainland China. This is a 10-year agreement, and it enables CMS to leverage its marketing network and expand into out-of-hospital and new retail channels.

Corporate Landscape of the Lidocaine Market:

Recent Developments

- In November 2025, Shandong Chenghui Pharmaceutical Group Co., Ltd obtained CEP certification for its lidocaine hydrochloride API from the EDQM, which is the fifth CEP approval for the company that year and supports ongoing international registrations in Europe and the U.S.

- In August 2025, Avenacy announced the launch of its first lidocaine hydrochloride injection, USP in the U.S., which is a generic equivalent of XYLOCAINE, for local and regional anesthesia across surgical, dental, diagnostic, and obstetrical procedures.

- In May 2025, Huons announced the U.S. FDA approvals for its 1% and 2% multi-dose vials of lidocaine hydrochloride injection, with added preservatives that allow repeated use after opening and are therapeutically equivalent to the reference drug Xylocaine.

- In December 2024, Zydus Lifesciences received final U.S. FDA approval to manufacture lidocaine and prilocaine cream USP 2.5%/2.5% at its Ahmedabad site. The cream is indicated for local analgesia on intact skin and genital mucous membranes for minor surgery and pre-infiltration anesthesia.

- Report ID: 3577

- Published Date: Mar 26, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.