LiDAR Market TOC

- An Introduction to the Research Study

- Preface

- Market Taxonomy

- Definition of the Market and the Segment

- Acronyms and Assumptions

- The Research Procedure

- Sources of Data

- Secondary

- Primary

- Manufacturer Front

- End User Front

- Supplier/Distributor Front

- Calculation and Derivation of Market Size

- Top-down Approach

- Bottom-up Approach

- Sources of Data

- Recommendation by Analyst for C-Level Executives

- An Abstract of the Report

- Evaluation of Market Fluctuations and Outlook

- Market Growth drivers

- Market Growth Deflation

- Market Trends

- End User Based

- Product/Service Based

- Fundamental Market Prospects

- Strategic competitive opportunities

- Geographic opportunities

- Application centric opportunities

- Pricing Analysis

- Regional Demand Analysis

- Analysis on Recent Development/Market Trends in Japan

- Analysis on Market Trends

- Global LiDAR Market Outlook & Projections, Opportunities Assessment, 2022 to 2035

- Market Summary

- Market Value (USD Million) Current and Future Projections, 2023-2036

- Market Increment $ Opportunity Assessment, 2023-2036

- Year on Year Growth Forecast (%)

- By Product

- Airborne LiDAR Market Value (USD Million0 Current and Future Projections, 2023-2036

- Terrain Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Bathymetric Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Mobile Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Still Image Ground LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- UAV LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Solid State LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Airborne LiDAR Market Value (USD Million0 Current and Future Projections, 2023-2036

- By Technology

- 2D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 3D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 4D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Product

- By Application

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- Roads Market Value (USD Million) Current and Future Projections, 2023-2036

- Rails Market Value (USD Million) Current and Future Projections, 2023-2036

- Pipelines Market Value (USD Million) Current and Future Projections, 2023-2036

- Engineering Market Value (USD Million) Current and Future Projections, 2023-2036

- Environment Market Value (USD Million) Current and Future Projections, 2023-2036

- Forest Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Coastline Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Pollution Models Chemicals Market Value (USD Million) Current and Future Projections, 2023-2036

- Agriculture Market Value (USD Million) Current and Future Projections, 2023-2036

- Wind Farm Market Value (USD Million) Current and Future Projections, 2023-2036

- Precision Forestry Market Value (USD Million) Current and Future Projections, 2023-2036

- ADA and Unnamed Vehicles Market Value (USD Million) Current and Future Projections, 2023-2036

- Exploration Market Value (USD Million) Current and Future Projections, 2023-2036

- Oil and Gas Market Value (USD Million) Current and Future Projections, 2023-2036

- Mining Market Value (USD Million) Current and Future Projections, 2023-2036

- Urban Planning Market Value (USD Million) Current and Future Projections, 2023-2036

- Maps Production Market Value (USD Million) Current and Future Projections, 2023-2036

- Meteorology Market Value (USD Million) Current and Future Projections, 2023-2036

- Military & Defense Market Value (USD Million) Current and Future Projections, 2023-2036

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- By Geography

- North America Market Value (USD Million) Current and Future Projections, 2023-2036

- Latin America Market Value (USD Million) Current and Future Projections, 2023-2036

- Europe Market Value (USD Million) Current and Future Projections, 2023-2036

- Asia Pacific Excluding Japan (APEJ) Market Value (USD Million) Current and Future Projections, 2023-2036

- Japan Market Value (USD Million) Current and Future Projections, 2023-2036

- Middle East & Africa Market Value (USD Million) Current and Future Projections, 2023-2036

- North America Lidar Market Valuation, Business Viewpoint, and Forecast by region, 2023-2036

- Outline of the Segment

- Detailed Overview

- Trends in the Market

- By Product

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Terrain Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Bathymetric Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Mobile Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Still Image Ground LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- UAV LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Solid State LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- BY Technology

- 2D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 3D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 4D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Application

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- Roads Market Value (USD Million) Current and Future Projections, 2023-2036

- Rails Market Value (USD Million) Current and Future Projections, 2023-2036

- Pipelines Market Value (USD Million) Current and Future Projections, 2023-2036

- Engineering Market Value (USD Million) Current and Future Projections, 2023-2036

- Environment Market Value (USD Million) Current and Future Projections, 2023-2036

- Forest Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Coastline Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Pollution Models Chemicals Market Value (USD Million) Current and Future Projections, 2023-2036

- Agriculture Market Value (USD Million) Current and Future Projections, 2023-2036

- Wind Farm Market Value (USD Million) Current and Future Projections, 2023-2036

- Precision Forestry Market Value (USD Million) Current and Future Projections, 2023-2036

- ADA and Unmanned Vehicles Market Value (USD Million) Current and Future Projections, 2023-2036

- Exploration Market Value (USD Million) Current and Future Projections, 2023-2036

- Oil and Gas Market Value (USD Million) Current and Future Projections, 2023-2036

- Mining Market Value (USD Million) Current and Future Projections, 2023-2036

- Urban Planning Market Value (USD Million) Current and Future Projections, 2023-2036

- Maps Production Market Value (USD Million) Current and Future Projections, 2023-2036

- Meteorology Market Value (USD Million) Current and Future Projections, 2023-2036

- Military & Defense Market Value (USD Million) Current and Future Projections, 2023-2036

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- By Country

- US Market Value (USD Million) Current and Future Projections, 2023-2036

- Canada Market Value (USD Million) Current and Future Projections, 2023-2036

- By Product

- Latin America LiDAR Market Valuation, Business Viewpoint, and Forecast by Region, 2023-2036

- Outline of the Segment

- Detailed Overview

- Trends in the market

- By Product

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Terrain Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Bathymetric Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Mobile Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Still Image Ground LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- UAV LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Solid State LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Technology

- 2D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 3D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 4D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Application

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- Roads Market Value (USD Million) Current and Future Projections, 2023-2036

- Rails Market Value (USD Million) Current and Future Projections, 2023-2036

- Pipelines Market Value (USD Million) Current and Future Projections, 2023-2036

- Engineering Market Value (USD Million) Current and Future Projections, 2023-2036

- Environment Market Value (USD Million) Current and Future Projections, 2023-2036

- Forest Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Coastline Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Pollution Models Chemicals Market Value (USD Million) Current and Future Projections, 2023-2036

- Agriculture Market Value (USD Million) Current and Future Projections, 2023-2036

- Wind Farm Market Value (USD Million) Current and Future Projections, 2023-2036

- Precision Forestry Market Value (USD Million) Current and Future Projections, 2023-2036

- Forest Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Coastline Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Pollution Models Chemicals Market Value (USD Million) Current and Future Projections, 2023-2036

- Agriculture Market Value (USD Million) Current and Future Projections, 2023-2036

- Wind Farm Market Value (USD Million) Current and Future Projections, 2023-2036

- Precision Forestry Market Value (USD Million) Current and Future Projections, 2023-2036

- Oil and Gas Market Value (USD Million) Current and Future Projections, 2023-2036

- Mining Market Value (USD Million) Current and Future Projections, 2023-2036

- Urban Planning Market Value (USD Million) Current and Future Projections, 2023-2036

- Maps Production Market Value (USD Million) Current and Future Projections, 2023-2036

- Meteorology Market Value (USD Million) Current and Future Projections, 2023-2036

- Military & Defense Market Value (USD Million) Current and Future Projections, 2023-2036

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- By Country

- Brazil, Market Value (USD Million) Current and Future Projections, 2023-2036

- Mexico, Market Value (USD Million) Current and Future Projections, 2023-2036

- Argentina, Market Value (USD Million) Current and Future Projections, 2023-2036

- Rest of Latin America, Market Value (USD Million) Current and Future Projections, 2023-2036

- By Product

- Europe LiDAR Market Valuation, Business Viewpoint, and Forecast by Region, 2023-2036

- Outline of the Segment

- Detailed Overview

- Trends in the market

- By Product

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Terrain Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Bathymetric Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Mobile Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Still Image Ground LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- UAV LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Solid State LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Technology

- 2D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 3D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 4D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Application

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- Roads Market Value (USD Million) Current and Future Projections, 2023-2036

- Rails Market Value (USD Million) Current and Future Projections, 2023-2036

- Pipelines Market Value (USD Million) Current and Future Projections, 2023-2036

- Engineering Market Value (USD Million) Current and Future Projections, 2023-2036

- Environment Market Value (USD Million) Current and Future Projections, 2023-2036

- Forest Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Coastline Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Pollution Models Chemicals Market Value (USD Million) Current and Future Projections, 2023-2036

- Agriculture Market Value (USD Million) Current and Future Projections, 2023-2036

- Wind Farm Market Value (USD Million) Current and Future Projections, 2023-2036

- Precision Forestry Market Value (USD Million) Current and Future Projections, 2023-2036

- ADA and Unmanned Vehicles Market Value (USD Million) Current and Future Projections, 2023-2036

- Exploration Market Value (USD Million) Current and Future Projections, 2023-2036

- Oil and Gas Market Value (USD Million) Current and Future Projections, 2023-2036

- Mining Market Value (USD Million) Current and Future Projections, 2023-2036

- Urban Planning Market Value (USD Million) Current and Future Projections, 2023-2036

- Maps Production Market Value (USD Million) Current and Future Projections, 2023-2036

- Meteorology Market Value (USD Million) Current and Future Projections, 2023-2036

- Military & Defense Market Value (USD Million) Current and Future Projections, 2023-2036

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- By Country

- Germany Market Value (USD Million) Current and Future Projections, 2023-2036

- UK Market Value (USD Million) Current and Future Projections, 2023-2036

- Italy Market Value (USD Million) Current and Future Projections, 2023-2036

- France Market Value (USD Million) Current and Future Projections, 2023-2036

- Spain Market Value (USD Million) Current and Future Projections, 2023-2036

- BENELUX Market Value (USD Million) Current and Future Projections, 2023-2036

- Russia Market Value (USD Million) Current and Future Projections, 2023-2036

- Poland Market Value (USD Million) Current and Future Projections, 2023-2036

- Rest of Europe Market Value (USD Million) Current and Future Projections, 2023-2036

- By Product

- Asia Pacific Excluding Japan (APEJ) LiDAR Market Valuation, Business Viewpoint and Forecast by Region, 2023-2036

- Outline of the Segment

- Detailed Overview

- Trends in the market

- By Product

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Terrain Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Bathymetric Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Mobile Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Still Image Ground LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- UAV LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Solid State LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Technology

- 2D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 3D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 4D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Application

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- Roads Market Value (USD Million) Current and Future Projections, 2023-2036

- Rails Market Value (USD Million) Current and Future Projections, 2023-2036

- Pipelines Market Value (USD Million) Current and Future Projections, 2023-2036

- Engineering Market Value (USD Million) Current and Future Projections, 2023-2036

- Environment Market Value (USD Million) Current and Future Projections, 2023-2036

- Forest Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Coastline Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Pollution Models Chemicals Market Value (USD Million) Current and Future Projections, 2023-2036

- Agriculture Market Value (USD Million) Current and Future Projections, 2023-2036

- Wind Farm Market Value (USD Million) Current and Future Projections, 2023-2036

- Precision Forestry Market Value (USD Million) Current and Future Projections, 2023-2036

- ADA and Unmanned Vehicles Market Value (USD Million) Current and Future Projections, 2023-2036

- Exploration Market Value (USD Million) Current and Future Projections, 2023-2036

- Oil and Gas Market Value (USD Million) Current and Future Projections, 2023-2036

- Mining Market Value (USD Million) Current and Future Projections, 2023-2036

- Urban Planning Market Value (USD Million) Current and Future Projections, 2023-2036

- Maps Production Market Value (USD Million) Current and Future Projections, 2023-2036

- Meteorology Market Value (USD Million) Current and Future Projections, 2023-2036

- Military & Defense Market Value (USD Million) Current and Future Projections, 2023-2036

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- By Country

- China, Market Value (USD Million) Current and Future Projections, 2023-2036

- India, Market Value (USD Million) Current and Future Projections, 2023-2036

- Indonesia, Market Value (USD Million) Current and Future Projections, 2023-2036

- South Korea, Market Value (USD Million) Current and Future Projections, 2023-2036

- Australia, Market Value (USD Million) Current and Future Projections, 2023-2036

- Singapore, Market Value (USD Million) Current and Future Projections, 2023-2036

- Malaysia, Market Value (USD Million) Current and Future Projections, 2023-2036

- New Zealand, Market Value (USD Million) Current and Future Projections, 2023-2036

- Rest of Asia Pacific Excluding Japan (APEJ), Market Value (USD Million) Current and Future Projections, 2023-2036

- By Product

- Japan LiDAR Market Valuation, Business Viewpoint and Forecast, 2023-2036

- Outline of the Segment

- Detailed Overview

- Trends in the market

- By Product

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Terrain Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Bathymetric Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Mobile Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Still Image Ground LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- UAV LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Solid State LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Technology

- 2D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 3D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 4D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Application

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- Roads Market Value (USD Million) Current and Future Projections, 2023-2036

- Rails Market Value (USD Million) Current and Future Projections, 2023-2036

- Pipelines Market Value (USD Million) Current and Future Projections, 2023-2036

- Engineering Market Value (USD Million) Current and Future Projections, 2023-2036

- Environment Market Value (USD Million) Current and Future Projections, 2023-2036

- Forest Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Coastline Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Pollution Models Chemicals Market Value (USD Million) Current and Future Projections, 2023-2036

- Agriculture Market Value (USD Million) Current and Future Projections, 2023-2036

- Wind Farm Market Value (USD Million) Current and Future Projections, 2023-2036

- Precision Forestry Market Value (USD Million) Current and Future Projections, 2023-2036

- ADA and Unmanned Vehicles Market Value (USD Million) Current and Future Projections, 2023-2036

- Exploration Market Value (USD Million) Current and Future Projections, 2023-2036

- Oil and Gas Market Value (USD Million) Current and Future Projections, 2023-2036

- Mining Market Value (USD Million) Current and Future Projections, 2023-2036

- Urban Planning Market Value (USD Million) Current and Future Projections, 2023-2036

- Maps Production Market Value (USD Million) Current and Future Projections, 2023-2036

- Meteorology Market Value (USD Million) Current and Future Projections, 2023-2036

- Military & Defense Market Value (USD Million) Current and Future Projections, 2023-2036

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- By Product

- Middle East & Africa LiDAR Market Valuation, Business Viewpoint and Forecast by Region, 2023-2036

- Outline of the Segment

- Detailed Overview

- Trends in the market

- By Product

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Terrain Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Bathymetric Air LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Mobile Ground-Based LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Still Image Ground LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- UAV LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Solid State LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- Airborne LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Technology

- 2D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 3D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- 4D LiDAR Market Value (USD Million) Current and Future Projections, 2023-2036

- By Application

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- Roads Market Value (USD Million) Current and Future Projections, 2023-2036

- Rails Market Value (USD Million) Current and Future Projections, 2023-2036

- Pipelines Market Value (USD Million) Current and Future Projections, 2023-2036

- Engineering Market Value (USD Million) Current and Future Projections, 2023-2036

- Environment Market Value (USD Million) Current and Future Projections, 2023-2036

- Forest Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Coastline Management Market Value (USD Million) Current and Future Projections, 2023-2036

- Pollution Models Chemicals Market Value (USD Million) Current and Future Projections, 2023-2036

- Agriculture Market Value (USD Million) Current and Future Projections, 2023-2036

- Wind Farm Market Value (USD Million) Current and Future Projections, 2023-2036

- Precision Forestry Market Value (USD Million) Current and Future Projections, 2023-2036

- ADA and Unmanned Vehicles Market Value (USD Million) Current and Future Projections, 2023-2036

- Exploration Market Value (USD Million) Current and Future Projections, 2023-2036

- Oil and Gas Market Value (USD Million) Current and Future Projections, 2023-2036

- Mining Market Value (USD Million) Current and Future Projections, 2023-2036

- Urban Planning Market Value (USD Million) Current and Future Projections, 2023-2036

- Maps Production Market Value (USD Million) Current and Future Projections, 2023-2036

- Meteorology Market Value (USD Million) Current and Future Projections, 2023-2036

- Military & Defense Market Value (USD Million) Current and Future Projections, 2023-2036

- Corridor Mapping Market Value (USD Million) Current and Future Projections, 2023-2036

- By Country

- Combined Gulf Countries Market Value (USD Million) Current and Future Projections, 2023-2036

- Israel Market Value (USD Million) Current and Future Projections, 2023-2036

- South Africa Market Value (USD Million) Current and Future Projections, 2023-2036

- Rest of Middle East & Africa Market Value (USD Million) Current and Future Projections, 2023-2036

- By Product

LiDAR Market Outlook:

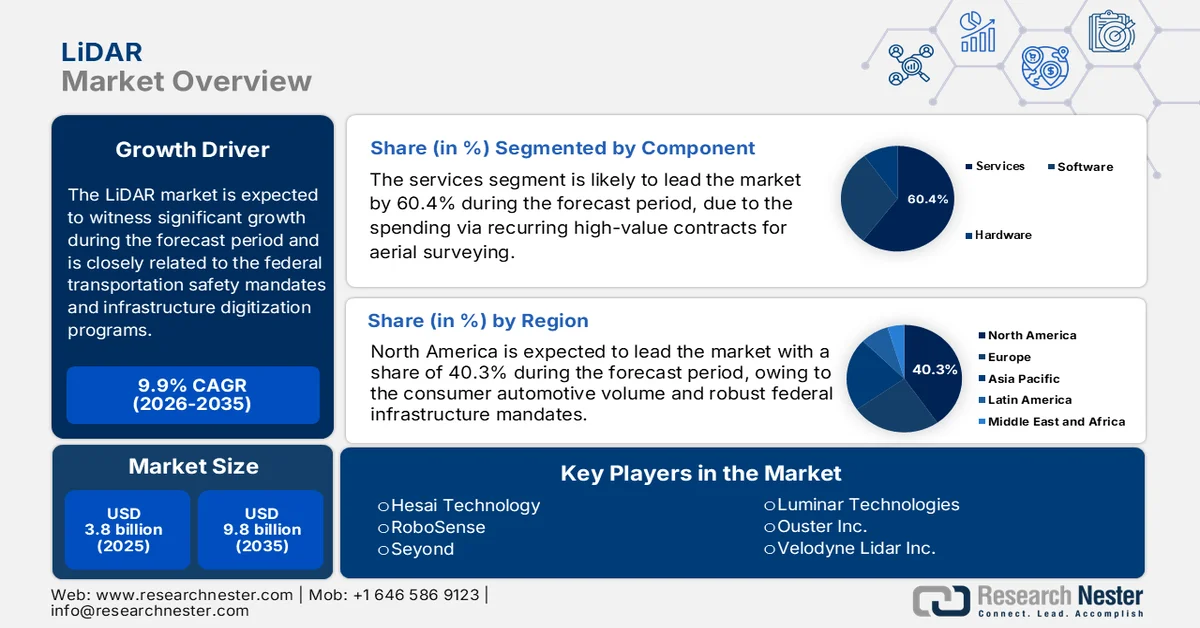

LiDAR Market size was valued at USD 3.8 billion in 2025 and is projected to reach USD 9.8 billion by the end of 2035, rising at a CAGR of 9.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of LIDAR is assessed at USD 4.2 billion.

The LiDAR market trends are being shaped by the federal transportation safety mandates, infrastructure development and digitization programs, and investments in environmental monitoring. According to the Cambridge University Press August 2022 study, the U.S. Department of Transportation reported allocating over USD 110 billion in 2023 under the Bipartisan Infrastructure Law for roads, bridges, and major projects, many of which integrate geospatial mapping and 3D surveying technologies for planning and asset management. The Federal Highway Administration continues to advance the 3D Elevation Program data acquisition in coordination with the USGS, July 2024 data, which noted that high-resolution elevation data can generate USD 690 million in annual conservative benefits nationwide, supporting flood risk mitigation, construction planning, and precision agriculture.

Besides, the National Oceanic and Atmospheric Administration's December 2024 data has expanded the coastal mapping activities supported by federal funding of USD 100 million annually for coastal resilience and hydrographic surveys, where airborne and bathymetric LiDAR systems are routinely deployed. Moreover, on the defense and public safety side, the U.S. Department of War March 2023 data depicts that the Department of Defense has proposed a budget of USD 842 billion, reinforcing the investments in autonomous systems surveillance and terrain intelligence applications. Furthermore, the Federal Aviation Administration is also progressing unmanned aircraft system integration, expanding the commercial drone-based mapping activity. Overall, the public-sector capital expenditure, geospatial modernization initiatives, and national security programs are sustaining procurement pipelines for airborne, terrestrial, and mobile LiDAR platforms across transportation, utilities, environmental management, and defense verticals.

Key LiDAR Market Insights Summary:

Regional Highlights:

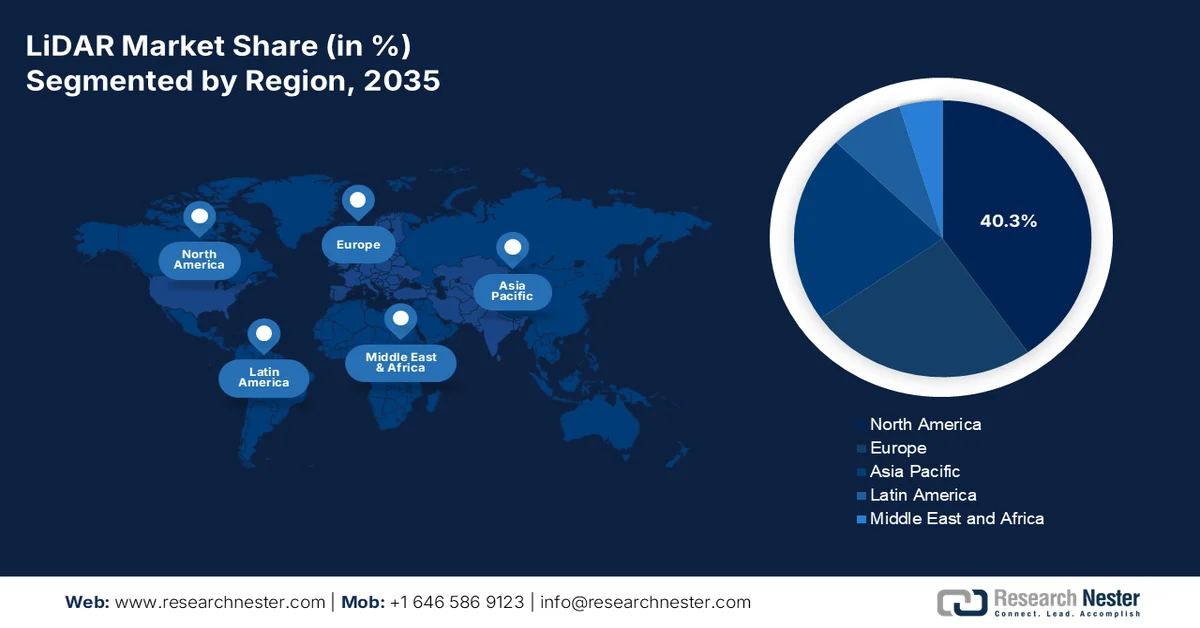

- North America in the LiDAR market is projected to hold a 40.3% share by 2035, owing to high adoption in defense, civilian infrastructure, and automotive applications.

- Asia Pacific is expected to be the fastest-growing region during 2026–2035, driven by technological innovations in traffic management and urban planning.

Segment Insights:

- The services sub-segment in the LiDAR market is projected to account for 60.4% share by 2035, impelled by the demand for 3D geospatial intelligence, climate adaptation mapping, and BIM integration.

- The short-range sub-segment is expected to maintain revenue leadership during 2026–2035, fueled by its adoption in automobile security systems, robotics, and factory automation.

Key Growth Trends:

- Flood risk management and climate resilience spending

- Renewable energy and grid expansion program

Major Challenges:

- Tariffs Trade war, and supply chain reconfiguration

- Threat towards low-cost photogrammetry and 4D radar

Key Players: Hesai Technology, RoboSense, Seyond, Luminar Technologies, Ouster Inc., Velodyne Lidar Inc., Innoviz Technologies, Aeva Technologies, Cepton, Trimble Inc., FARO Technologies, Hexagon AB, Sick AG, Valeo SA, Continental AG, Topcon Corporation, Mitsubishi Electric, DENSO Corporation, Teledyne Optech, RIEGL, Orbbec, Kyocera Corporation, Voyant Photonics

Global LiDAR Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 3.8 billion

- 2026 Market Size: USD 2.89 billion

- Projected Market Size: USD 9.8 billion by 2035

- Growth Forecasts: 9.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region:North America (40.3% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Canada, Germany, Japan, France

- Emerging Countries: China, South Korea, India, Brazil, Singapore

Last updated on : 25 February, 2026

LiDAR Market - Growth Drivers and Challenges

Growth Drivers

- Flood risk management and climate resilience spending: Climate adaptation funding is directly driving the LiDAR market, supporting flood modeling and coastal risk assessment. As per the NOAA 2024 report, USD 6.8 billion is allocated for coastal resilience mapping and hydrographic surveys. Moreover, the USGS reports that the high-resolution elevation data support floodplain mapping across all the U.S. states, reducing the disaster losses. Besides the federal emergency management agency, which funds billions on the hazard mitigation grant program, which relies on updated topographic data for risk modeling. Further, as the climate risk reporting becomes mandatory in multiple jurisdictions, high-resolution terrain datasets will increasingly be embedded into regulatory compliance workflows.

- Renewable energy and grid expansion program: Energy transition spending is creating a demand for terrain modeling and transmission corridor analysis. As stated in the U.S. Department of Energy report in February 2022, an investment of USD 62 billion was allocated towards clean energy under the recent federal legislation. Utility-scale solar and wind installations require precise site assessment and vegetation management datasets. Moreover, the International Renewable Energy Agency data in March 2024 depicts that the renewable capacity additions reached 473 GW globally in 2023, signaling the rapid grid expansion needs. This sustained capital deployment toward renewable generation and transmission infrastructure is expected to structurally increase demand for high-resolution geospatial datasets to support permitting environmental compliance and long-term grid asset management across both developed and emerging LiDAR markets.

- Research and advanced sensor innovation funding: The public R&D funding sustains long-term LiDAR market innovation. As per the U.S. National Science Foundation 2024 report, USD 9.06 billion is funded to support photonics sensing systems and robotic research. These programs fund the next generation of solid-state sensors, miniaturization, and advanced manufacturing processes. Sustained federal R&D allocations also reduce commercialization risk by enabling early-stage prototyping, field validation, and technology transfer partnerships between academia and industry. Moreover, this structured funding pipeline strengthens domestic supply chains and accelerates the integration of advanced sensing systems into defense, transportation, energy, and environmental monitoring programs.

U.S. National Science Foundation FY 2024 Budget Allocation

|

|

FY 2024 Budget Request ($) |

FY 2024 Current Plan ($) |

|

Computer and Information Science and Engineering |

1,172.14 |

989.35 |

|

Engineering |

970.00 |

740.80 |

|

Geosciences |

1,801.98 |

1,577.08 |

|

GEO: Polar Programs |

463.60 |

559.76 |

|

[GEO: Polar Programs: U.S. Antarctic Logistical Support Activities] |

[102.00] |

[109.31] |

|

Mathematical and Physical Sciences |

1,835.79 |

1,554.21 |

|

Social, Behavioral and Economic Sciences |

360.60 |

290.29 |

|

Technology, Innovation and Partnerships |

1,185.63 |

617.90 |

|

International Science and Engineering |

71.21 |

63.70 |

|

Integrative Activities |

646.37 |

551.83 |

Source: NSF 2024

Challenges

- Tariffs Trade war, and supply chain reconfiguration: Geopolitics have created sudden cost inflation for cross-border suppliers. The U.S. tariff policies have introduced profound uncertainty, increasing the costs for imported laser scanners and optical components. This disrupts the cost structures of new companies reliant on specific regional manufacturing hubs. While this forces the development of regional sourcing, it creates a dual supply chain burden that is prohibitively expensive for startups in the LiDAR market to establish simultaneously compared to giant players.

- Threat towards low-cost photogrammetry and 4D radar: LiDAR does not operate in a technological vacuum; it competes with cheaper, good enough substitutes. The high costs are suppressed by the easy availability of low-cost photogrammetry systems. These 2D/3D cartographic models use standard cameras, avoiding the expensive laser and MEMS components required for LiDAR. For surveying agriculture and basic ADAS customers, choose photogrammetry drones, which are significantly lighter and cheaper to fly than heavy LiDAR systems, capping the total addressable LiDAR market volume.

LiDAR Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

9.9% |

|

Base Year Market Size (2025) |

USD 3.8 billion |

|

Forecast Year Market Size (2035) |

USD 9.8 billion |

|

Regional Scope |

|

LiDAR Market Segmentation:

Component Segment Analysis

The services sub-segment is dominating and is poised to hold the share value of 60.4% by the end of 2035 in the LiDAR market. This dominance is due to the spending via recurring high-value contracts for aerial surveying, GIS data processing, asset management, and digital twin maintenance. The segment is driven by the dominance due to the demand for 3D geospatial intelligence, climate adaptation mapping, and Building Information Modeling integration. Moreover, the services generate multi-year high-margin income streams from government mapping agencies, engineering consultancies, and defense contractors. Additionally, the growing adoption of LiDAR-as-a-Service (LaaS) models and cloud-based data analytics platforms is further accelerating recurring revenue generation and strengthening long-term client retention across infrastructure, smart city, and environmental monitoring projects.

Range Segment Analysis

The short range sub segment is projected to maintain its revenue leadership in the range segment during the assessment period. The segment is driven by the segment’s widespread adoption in automobile security systems, robotics, and factory automation. These sensors typically operate under 100 meters and provide precise object detection and collision avoidance in compact, densely populated environments, vital for ADAS functions such as emergency braking and for warehouse robotics navigating narrow aisles. Short-range systems benefit from lower component costs, simpler solid-state architecture, and easier regulatory approval compared to long-range airborne counterparts. According to the NLM April 2025 study, it is recorded that over 400 drone-related near-miss incidents near U.S. airports, with various cases requiring pilots to take evasive action, underscoring the urgent need for short-range LiDAR deployment in ground-based security perimeters and drone detection networks to prevent catastrophic collisions in sensitive airspace.

Technology Segment Analysis

The mechanical LiDAR is leading and is estimated to garner a noteworthy revenue share in the market during the forecast timeline. The leadership stems from its unparalleled 360-degree view, long-range capabilities extending several kilometers, and proven reliability in corridor mapping, military surveillance, volumetric engineering, and large-scale topographic surveys. The mechanical systems remain the gold standard, where the maximum point density and extreme accuracy come at a cost. As per the NLM April 2025 study, the mechanical LiDAR sensors mostly use physically moving components, such as the rotating mirrors, oscillating prisms, entire sensor heads, etc., to steer the laser beam across the environment and measure the distance to provide an accurate 3D map. Furthermore, their established deployment across national mapping programs and defense-grade reconnaissance missions continues to reinforce mechanical LiDAR’s dominance in mission-critical, high-precision geospatial applications.

Our in-depth analysis of the LiDAR market includes the following segments:

|

Segment |

Subsegments |

|

Installation Platform |

|

|

Technology |

|

|

Component |

|

|

Application |

|

|

Range |

|

|

Data Processing Method |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

LiDAR Market - Regional Analysis

North America Market Insights

The North America LiDAR market is dominating and is expected to hold the regional revenue share of 40.3% by 2035. The market is a mature dual pillar structure where defense and civilian infrastructure applications command equal strategic priority. The region functions as the primary proving ground for high cost high performance sensor integration, mainly in aerospace, autonomous defense platforms, and long-range topographic mapping. The adoption is further propelled by consumer automotive volume, robust federal infrastructure mandates, and environmental monitoring programs that treat LiDAR as a non-discretionary utility. Moreover, the regulatory harmonization between Canada and the U.S. enables cross-border supply chains and service corridors thought the market remains sensitive to export controls on high specification components. The region’s competitive focus centers on engineering resilience, data accuracy standards, and sovereign capability retention in critical mapping and defense supply chains.

Sustained federal infrastructure climate resilience and R&D investments are accelerating the growth of the LiDAR market in the U.S. In March 2023, the USGS recommended 20 proposals across 13 states under its 3D Elevation Program, expected to add approximately 82,000 square miles of new public-domain LiDAR point cloud data and derived elevation products to national holdings. Moreover, the USGS October 2024 data states that the total 3DEP data acquisition investments reached USD 93.8 million, including USD 70.9 million in Federal funds and USD 22.9 million in non-Federal partner contributions, reflecting sustained multi-stakeholder funding participation. Besides, the structured cost-sharing model provides predictable procurement pipelines for airborne survey operators and geospatial analytics firms while expanding standardized elevation coverage nationwide. Overall, these data reinforce a long-term demand visibility within the U.S. LiDAR ecosystem.

U.S. 3D Elevation Program (3DEP) Annual LiDAR Funding

|

Fiscal Year |

Federal Funds (USD Million) |

Non-Federal Funds (USD Million) |

|

FY15 |

35.7 |

11.0 |

|

FY16 |

42.9 |

16.0 |

|

FY17 |

73.1 |

13.1 |

|

FY18 |

108.3 |

13.4 |

|

FY19 |

103.3 |

33.5 |

|

FY20 |

90.5 |

18.3 |

|

FY21 |

52.6 |

13.5 |

|

FY22 |

70.5 |

17.1 |

|

FY23 |

93.2 |

12.7 |

|

FY24 |

70.9 |

22.9 |

Source: USGS October 2024

The escalating disaster losses and national elevation data deployment are driving the LiDAR market in Canada. According to the IBC January 2024 report, severe weather events in 2023 caused over USD 3.1 billion in insured damage, and floods remain the most frequent and costly disaster, generating more than USD 2 billion in annual damages, reinforcing the need for high-resolution floodplain mapping and terrain intelligence. On the other hand, the Government of Canada's October 2025 data depicts that the National Elevation Data Strategy has significantly expanded coverage, with 709,000 km² of new LiDAR-derived elevation data added to the High-Resolution Digital Elevation Model, increasing national coverage by 54% and now serving 244 of Canada’s 250 largest cities, covering over 95% of the population. Additionally, LiDAR point cloud datasets expanded by more than 200,000 km², totaling nearly 364,000 km² nationwide. These federal upgrades are generating consistent demand for airborne data acquisition processing services and analytics platforms, particularly across flood mitigation infrastructure planning, Arctic monitoring, and urban development sectors.

APAC Market Insights

The Asia Pacific LiDAR market is the fastest-growing and is expected to register a CAGR of 12.3% between 2026 and 2035. The market growth is factored by technological inventions for traffic management and urban planning. Asia Pacific has a massive urban population, rapid infrastructure build-out, and aggressive government digitalization timelines, which create immediate large-scale use cases. China functions as the region’s manufacturing engine and volume driver, integrating LiDAR into mass-market electric vehicles. On the other hand, South Korea contributes precision robotics integration and sensor miniaturization, embedding LiDAR into elder care assistive devices, construction ICT, and autonomous mobile logistics. The region is set to have an active growth in the LiDAR market.

The LiDAR market in India is strengthening via increasing domestic engineering capacity, infrastructure digitization, and participation in global sensor innovation networks. The launch of Velodyne Lidar’s India Design Center in Bengaluru in June 2021 signals a strategic shift toward localized development of LiDAR sensor and software solutions, reinforcing India’s role in advanced mobility and smart infrastructure ecosystems. Additionally, the PRS Legislative Research in February 2023 reported that the Ministry of Road Transport and Highways allocated over USD 0.33 million (FY2023–24) toward road transport and highway development, supporting large-scale corridor mapping and asset monitoring requirements. This indicates a long-term demand visibility for LiDAR hardware integration, mapping services, and analytics platforms across transportation, urban planning, and industrial automation sectors in India.

The formalized national standards and large-scale automotive deployment are expanding the LiDAR market in China. The implementation of GB/T 45500-2025 Performance Requirements and Test Methods for Automotive LiDAR establishes the unified national benchmarks for the ranging accuracy, angular resolution, interference resistance, and environmental durability, reinforcing regulatory clarity for ADAS and autonomous vehicle integration. According to the HESAI May 2025 data, China’s annual LiDAR installations have exceeded 1.5 million units, with penetration reaching 25% in new energy vehicles priced above RMB 150,000 and projected to double by 2025. As China formalizes testing protocols while expanding NEV production, the market is positioning itself as a global volume leader in automotive LiDAR integration and performance benchmarking.

Europe Market Insights

The LiDAR market in Europe is expanding significantly and is undergoing a transformative shift, moving from early adopter pilot programs toward systematic cross-border industrial deployment. The demand is diversifying across national mapping agencies, rail infrastructure operators, wind energy developers, and precision agriculture cooperatives. The regional characteristic is the strong interplay between the public sector environmental mandates and private sector engineering capability. The countries lacking domestic sensor fabrication lead in application layer integration, embedding LiDAR into digital twin platforms and heritage preservation workflows. The market is a maturing ecosystem where value is captured less by hardware margins and more by software workflows, calibration services, and multi-sensor fusion expertise.

Federally funded digital infrastructure, climate adaptation, and geospatial modernization programs are fueling the LiDAR market in Germany. The market is further strengthened via a combination of European institutional financing and advanced domestic sensor development. According to the European Investment Bank's July 2022 report, the bank has approvedUSD 16.35 million in venture debt financing to Munich-based Blickfeld GmbH under the European Fund for Strategic Investments, supporting the scale of smart LiDAR hardware and software solutions. On the other hand, recent advancements in Germany, such as the Ulm-based Scantinel Photonics, announced in July 2024 the launch of its next-generation FMCW photonic scanner detector chip based on standard CMOS technology, advancing integration and scalability in high-performance sensing systems. These data are positioning Germany as a key hub for next-generation sensing technologies across mobility robotics and industrial LiDAR markets.

The LiDAR market in UK is expanding in alignment with offshore renewable energy scaling and long-term flood resilience investment. In October 2024, Venterra Group announced a USD 12.7 millioninvestment to launch the Venterra V-LiDAR fleet, described as the first UK-designed and manufactured dual LiDAR buoy fleet, strengthening domestic offshore wind measurement capacity and reinforcing the UK’s position in offshore wind infrastructure. Offshore wind development requires precise wind resource assessment and site validation, creating sustained demand for floating LiDAR systems and marine data services. Besides, the Government of the UK data in July 2021 depicts that USD 6.6 billioninvestment in flood and coastal defenses is accelerating high-resolution terrain mapping and coastal monitoring programs to mitigate climate-related risks. These data show a positive impact on the UK LiDAR market’s growth.

Key LiDAR Market Players:

- Hesai Technology (China)

- RoboSense (China)

- Seyond (China)

- Luminar Technologies (U.S.)

- Ouster Inc. (U.S.)

- Velodyne Lidar Inc. (U.S.)

- Innoviz Technologies (Israel)

- Aeva Technologies (U.S.)

- Cepton (backed by Koito) (U.S.)

- Trimble Inc. (U.S.)

- FARO Technologies (U.S.)

- Hexagon AB (Sweden)

- Sick AG (Germany)

- Valeo SA (France)

- Continental AG (Germany)

- Topcon Corporation (Japan)

- Mitsubishi Electric (Japan)

- DENSO Corporation (Japan)

- Teledyne Optech (Canada)

- RIEGL (Austria)

- Orbbec (China)

- Kyocera Corporation (Japan)

- Voyant Photonics (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Hesai Technology has solidified its leadership in the global LiDAR market via aggressive capacity expansion and strategic ecosystem integration. The company announced the plans double its annual production capacity, a move directly tied to its selection as a LiDAR partner for NVIDIA’s DRIVE Hyperion platform. According to the 2024 annual report, the company has made a revenue of USD 284,569 thousand.

- RoboSense has captured the top position in the global passenger car LiDAR market, securing a market share in both annual and cumulative ADAS LiDAR sales. The company has shipped certain units, becoming the world’s first LiDAR firm to surpass millions in cumulative shipments. Its strategic dominance is underpinned by full-stack chip self-development capabilities covering transcribing, scanning, and data processing. In 2024, the company made a revenue of RMB 1,648,902 thousand.

- Seyond is executing a deliberate pivot from single customer concentration toward diversified global commercialization in the LiDAR market. The company has secured fixed point nominations from OEMs and ADAS companies, including a landmark partnership with GAC Group, scheduled for mass production.

- Luminar Technologies is redefining competitive strategy in the automotive LiDAR market by shifting from custom-engineered solutions to a unified product architecture. Collaborating with multiple global OEMs, the company has developed the Limunar Halo platform, designed to establish a collective industry standard covering all use cases from advanced safety to full autonomy.

- Ouster Inc. is executing a consolidation-driven strategy to become the definitive end-to-end perception platform for the Physical AI era. The company’s strategic thesis holds that customers no longer wish to act as system integrators; Ouster now delivers seamlessly synchronized, calibrated LiDAR-camera data ready for immediate deployment across industrial automation, smart infrastructure, and robotics.

Below is the list of some prominent players operating in the global LiDAR market:

The global LiDAR market is defined by a fierce two-front battle: cost-driven volume leadership versus technology-driven premium differentiation. Further, China players are actively pursuing price compression strategies within domestic supply chains to slash automotive sensors prices and capture mass market EV design wins. In January 2026, MicroVision, Inc. announced that it had agreed to acquire certain assets from Luminar Technologies, Inc. Moreover, U.S. specialists are pivoting toward next-generation architecture and balance sheet discipline, prioritizing the standardized platforms to secure long term OEM integration. Further, the European industrial stalwarts are fortifying their dominance in surveying and factory automation via precision instrumentation, while Japanese players leverage automotive supply chain incumbency to con develop an integrated sensing solution.

Corporate Landscape of the LiDAR Market:

Recent Developments

- In August 2025, Orbbec unveiled the Pulsar ME450, the industry’s first dToF 3D LiDAR using a combination of a MEMS mirror and a motor to offer configurable scanning patterns and adjustable vertical field of view.

- In January 2025, Kyocera Corporation announced the development of its unique Camera-LIDAR Fusion Sensor, the world's first LIDAR that aligns the optical axes of the camera and LIDAR into a single sensor.

- In December 2024, Voyant Photonics, a lidar startup based in the heart of New York City and announced the launch of sub-USD 1500 FMCW lidar at CES 2025

- Report ID: 5264

- Published Date: Feb 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.