Legal Technology Market Outlook:

Legal Technology Market was valued at USD 34.4 billion in 2025 and is expected to grow to USD 83.8 billion by 2035, registering a CAGR of 10.4% over the forecast period, i.e., 2026-2035. In 2026, the industry size of legal technology is evaluated at USD 37.9 billion.

The legal technology market is poised for exceptional growth as law firms, corporate legal departments, and alternative legal service providers are embracing digital transformations. In this context, in March 2025, the American Bar Association’s Legal Technology Resource Center released its 2024 survey report, which found that 73% of firms now rely on cloud-based legal tools, whereas 67% of attorneys use fee-based online research services, and 55% turn to free platforms such as government databases. It also underscored that the adoption of AI-based discovery tools and electronic court filings has reached 85% among litigators, which reflects a structural shift toward efficiency and automation. In addition, 60% of firms have formal cybersecurity policies in place, wherein multifactor authentication is becoming more common, thereby positively impacting market growth.

Furthermore, the aspects of strategic partnerships, government-backed investments, and the expansion of legal tech startups are also strengthening the legal technology market. In this context, the UK Ministry of Justice in March 2025 announced a total of USD 1.8 million investment in the LawtechUK programme with a prime focus to accelerate digital transformation in the legal services sector. It also highlighted that since 2023, LawtechUK has supported more than 176 startups by fostering innovation in AI tools and legal software by connecting companies with investors and law firms. The initiative also underpins the UK’s USD 46.25 billion legal services industry, thereby driving economic growth, job creation, and access to technology-enabled legal solutions across the country. Therefore, from a strategic perspective, such instances are catalyzing the adoption of digital solutions across the legal ecosystem in different nations.

Key Legal Technology Market Insights Summary:

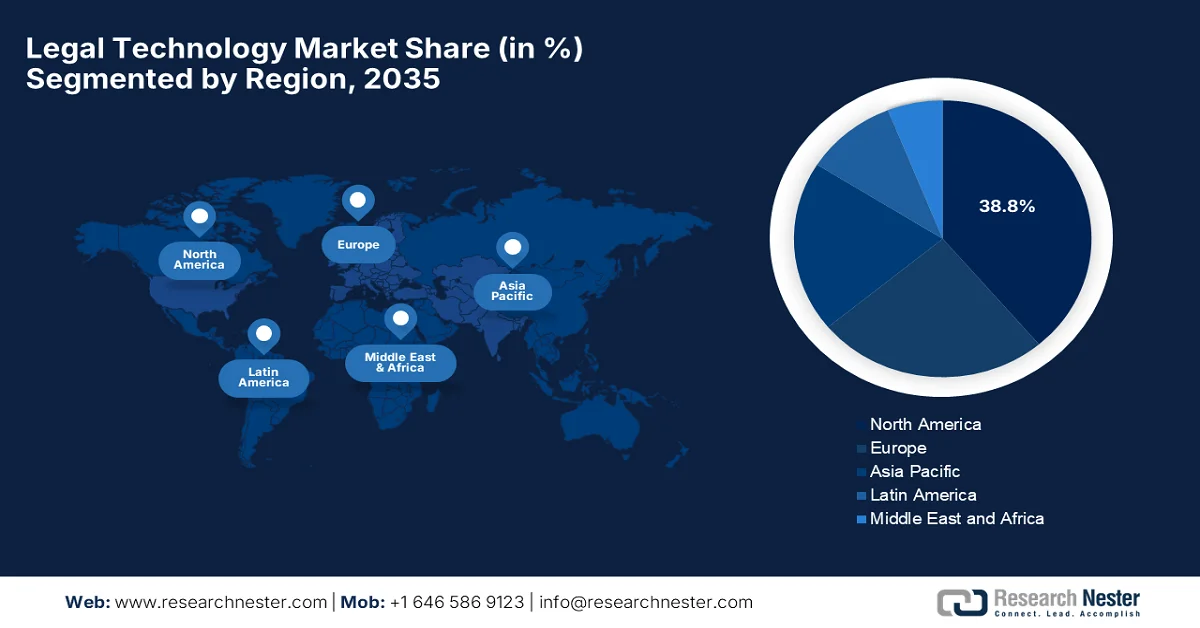

Regional Highlights:

- North America is anticipated to command a 38.8% share of the legal technology market by 2035, attributed to strong legal service expenditure, rising firm investments in legal technologies, and expanding technology-driven initiatives to enhance access to legal services.

- Asia Pacific is projected to witness the fastest growth in the forecast period 2026–2035, fueled by increasing demand for cost-efficient legal solutions and expanding adoption of AI-enabled compliance and analytics tools.

Segment Insights:

- Software in the legal technology market is projected to account for a 70.3% share by 2035, propelled by the growing adoption of workflow automation and AI-driven legal research platforms by law firms and legal departments.

- E-discovery is expected to secure a considerable share during 2026–2035, impelled by the surging volume of digital evidence and the need for faster and more efficient electronic document review in litigation and investigations.

Key Growth Trends:

- Adoption of AI

- Complex regulatory and compliance requirements

Major Challenges:

- Resistance to change and cultural barriers

- Regulatory and compliance complexity

Key Players: Thomson Reuters Corporation (U.S.), RELX plc - (LexisNexis Legal & Professional division) (UK), DocuSign, Inc. (U.S.), Themis Solutions Inc. (Clio) (Canada), CS Disco, Inc. (U.S.), HaystackID LLC (U.S.), Everlaw, Inc. (U.S.), iManage, LLC (U.S.), Ironclad, Inc. (U.S.), ContractPod Technologies Ltd. (UK), Luminance Technologies Ltd. (UK), LegalOn Technologies Co., Ltd. (Japan), SpotDraft Solutions Private Limited (India), Leegality (India), CaseMine (India), XMart Labs Sdn. Bhd (Malaysia), Bereev Sdn. Bhd. (Malaysia), Boss Boleh Sdn. Bhd. (Malaysia), Eudia, Inc. (U.S.), HighQ Solutions Limited (UK).

Global Legal Technology Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 34.4 billion

- 2026 Market Size: USD 37.9 billion

- Projected Market Size: USD 83.8 billion by 2035

- Growth Forecasts: 10.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.8% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, United Kingdom, Germany, China, Japan

- Emerging Countries: India, South Korea, Singapore, Australia, Canada

Last updated on : 11 March, 2026

Legal Technology Market - Growth Drivers and Challenges

Growth Drivers

- Adoption of AI: Artificial intelligence, along with generative AI, is the fundamental driver for the legal technology market since it helps automate tasks such as legal research, e-discovery, drafting, and case outcomes. This significantly increases efficiency and accuracy for legal professionals. In February 2025 Press Information Bureau (PIB) reported that India is utilizing AI to transform its judiciary and law enforcement by integrating AI in e-Courts Phase III, legal research, predictive policing, and AI-assisted language translation, with the main goal to enhance efficiency, accessibility, and decision-making. It also highlighted that these technologies streamline case management, reduce delays, and improve crime prevention, while ensuring administrative processes are faster and more transparent, hence suitable for bolstering the legal technology market’s expansion.

- Complex regulatory and compliance requirements: The continuous upgradations to laws and regulatory frameworks across different industries increase the need for technology that assists well with compliance management. This is the fundamental driving factor for the legal technology market. The EU Data Act, which came into force from September 2025, establishes proper rules for fair access to and use of data that is generated by connected devices, thereby strengthening both consumers and businesses while mitigating unfair contractual practices. Besides, this law also increases the legal certainty, thereby enabling public sector access and standardizing data-sharing processes, and it addresses the complexity of cross-sector regulations. Therefore, these measures reflect the rising demand for technological solutions that support compliance management in this continuously evolving regulatory landscape.

- Technology adoption: Cloud-based platforms are driving growth by providing scalability, remote accessibility, and secure data storage. This aspect prompts a profitable business environment for pioneers in the legal technology market. The article, which was published by the administrative office of the U.S. courts in January 2025, the country’s federal judiciary’s strategic plan prioritizes harnessing technology to improve public access to court services by ensuring the protection of the integrity of judicial information against cyber threats. The plan also leverages modernizing IT systems with automation, machine learning, and cloud solutions to enhance case management, electronic filing, and record-keeping. Therefore, achieving this requires developing staff skills and integrating flexible, technology systems in order to meet the Judiciary’s operational and security needs.

Challenges

- Resistance to change and cultural barriers: The legal profession is considered to be conservative and risk-averse, which sometimes prefers precedent and established workflows over rapid innovation. Most of the attorneys are skeptical about AI-based tools replacing or augmenting professional judgment. In this context, the concerns about reliability and ethical responsibility can slow down the technology adoption in this field. Besides, billable-hour models may also discourage efficiency-enhancing tools that reduce time spent on tasks. The existence of training gaps creates complications in implementation, as legal professionals may lack the technical knowledge to leverage improved analytics effectively. Therefore, overcoming cultural resistance in the legal technology market requires change management strategies that can be cost-intensive.

- Regulatory and compliance complexity: The providers in the legal technology market need to operate in a highly regulated environment where cross-border data transfer rules, AI governance laws, and professional responsibility standards keep changing. Emerging frameworks, such as AI-specific regulations and state-level automated decision-making laws, add compliance burdens for both vendors and the user. Therefore, ensuring that AI-generated outputs meet evidentiary and ethical standards is considered to be challenging in litigation contexts. Besides, vendors in the legal technology market need to design solutions that are transparent, auditable, and defensible under regulatory scrutiny. Furthermore, the constantly evolving legal requirements increase development costs and create uncertainty around long-term product roadmaps.

Legal Technology Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

10.4% |

|

Base Year Market Size (2025) |

USD 34.4 billion |

|

Forecast Year Market Size (2035) |

USD 83.8 billion |

|

Regional Scope |

|

Legal Technology Market Segmentation:

Component Segment Analysis

In the component segment, software is expected to garner the largest revenue share of 70.3% in the legal technology market over the forecasted years. The dominance is propelled by the adoption of software technologies by the leading law firms and departments with a primary focus on workflow automation. In August 2025, Thomson Reuters announced that it had launched CoCounsel Legal, which is a next-generation AI platform integrating legal research, workflow automation, intelligent document search, and AI-based assistance. The platform’s deep research feature consists of Westlaw and Practical Law content to generate multi-step research plans with transparent reasoning, enabling legal professionals to delegate complex tasks. Hence, with such constant developments from technology firms, the leading law firms and legal departments are adopting software technologies to transform legal operations.

Application Segment Analysis

In the legal technology market the e-discovery is anticipated to grow with a considerable revenue share over the stipulated time period. The growth of the sub-segment is highly propelled by the increasing volume of digital evidence and the need for faster, more efficient review of electronic documents in litigation and investigations. In July 2024, NiCE reported that the state attorney’s office for Florida’s eighth judicial circuit deployed the NiCE Justice, which is an AI-based digital evidence management solution, to automate intake, review, and organization of growing volumes of digital evidence. The cloud-based platform integrates with multiple systems by offering transcription, OCR, analytics, and automated case building, enabling prosecutors to focus on case preparation and meet discovery deadlines more efficiently. Therefore, from a strategic perspective adoption of AI-based e-discovery platforms enables legal institutions to manage growing volumes of digital evidence more efficiently.

End user Segment Analysis

The law firm subtype is projected to garner a significant share in the legal technology market by the conclusion of 2035. The proactive adoption of technically advanced solutions to enhance operational efficiency is the main fueling factor behind this leadership. Increasing caseloads, complex regulatory requirements, and the need for rapid, accurate legal research are encouraging firms across different nations to invest in AI, workflow automation, and document management tools. In addition, the competitive pressures push firms to leverage technology for client service, cost reduction, and faster turnaround times. Also, the integration of digital platforms allows law firms to optimize internal collaboration, streamline billing and compliance processes, and improve case strategy. Therefore, the presence of all of these factors underscores the segment’s prominence in reshaping the overall growth trajectory of the legal technology industry.

Our in-depth analysis of the legal technology market includes the following segments:

|

Segment |

Subsegments |

|

Component |

|

|

Application |

|

|

Software Type |

|

|

End user |

|

|

Deployment Mode |

|

|

Organization Size |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Legal Technology Market - Regional Analysis

North America Market Insights

The North America legal technology market is expected to hold the largest revenue share of 38.8% during the forecast period. The region’s leadership is mainly driven by strong legacy legal service expenditure, funding grants, and rising firm budgeting for legal technologies. The mature legal services ecosystem with extensive innovation infrastructure and nonprofit projects that expand access to legal data also drives the region’s market. In December 2025, the Legal Services Corporation reported that it had awarded 32 technology initiative grants totaling USD 4.2 million to legal services organizations across 22 U.S. states to enhance technology use in delivering legal services. The funded projects are AI-based search assistants, automated administrative tools, and digital resources to improve access to justice for low-income citizens in the country, hence denoting a positive legal technology market outlook.

The focus on solutions that reduce manual work with improved speed and accuracy is the main factor boosting the growth of the legal technology market in the U.S. The presence of leading market pioneers and their strategic activities also positions the U.S. at the forefront of revenue generation in the region. This environment creates a highly competitive landscape wherein both established and newer entrants collaborate through partnerships, funding, acquisitions, and venture funding with the main goal of addressing evolving legal demands. In December 2025, BriefCatch, which is a secure AI-assisted legal writing platform for law firms and courts, reported that it had closed a USD 6 million Series A funding round, which was led by Full In to accelerate platform development and expand market presence. It also notes that the platform combines expert-guided editing with some optional AI-based features, thereby helping legal professionals to improve clarity, while maintaining full control and security over their work.

The emergence of software suitable for practice management, billing automation, and cloud collaboration drives the legal technology market in Canada. The country’s supportive technology ecosystem and successful financing rounds for legaltech companies reflect the country’s rising influence on the global stage. As of the October 2025 data from the country’s government, Canada’s Courts Administration Service (CAS) advanced digital courts in 2024-25, by modernizing legacy systems, expanding e-courtroom capabilities, and implementing AI and robotic process automation to improve access, efficiency, and bilingual service delivery. In addition, court facilities were upgraded and newly constructed across the country, integrating modern courtroom technologies, hybrid hearing capabilities, and accessibility features, creating secure and future-ready environments, hence suitable for bolstering the market’s growth in the country.

APAC Market Insights

The Asia Pacific legal technology market is poised for the fastest growth, mainly influenced by the demand for cost-efficient solutions. The central countries, such as China, India, South Korea, and Japan, adopt AI-enabled tools to manage compliance and analytics, driven by rising enterprise IT investment. The regional market growth is also heightened by mobile technology penetration and the rise of cross-border legal service needs. Based on the July 2025 data from the Hong Kong Department of Justice, it actively promoted law tech and AI in the legal sector, which also includes pilot trials of locally developed large language models such as HKGAI V1 and legal AI tools such as HKPilot and LexiHK. The DoJ established a Consultation Group on Lawtech Development to guide policy, support small and medium-sized law firms, and enhance technology adoption through awareness programs, exhibitions, and phased implementation strategies.

China legal technology market is navigating unique regulatory and data governance frameworks. The domestic service providers in the country are strengthening R & D, incorporating improved algorithms and machine learning to tackle the complexity of domestic legal workflows. In November 2024, the Supreme People’s Court of China released the results of the Faxin Legal Foundation Model, which is a national-level AI infrastructure for the legal industry. It was built on Tsinghua University’s research and trained with 320 million legal documents and 3.67 trillion words, and it provides capabilities in legal semantic understanding, reasoning, and intelligent search. The government report also notes that it has already applied in Shenzhen’s AI-assisted trial system and intelligent retrieval platforms, and the model enhances judicial efficiency and consistency, hence positioning China as a key growth contributor for the regional industry.

The strong government support and a focus on accessible legal assistance that addresses local procedural nuances are the main factors responsible for uplifting the legal technology market in India. The country is witnessing an increased adoption across law firms and legal departments, which is encouraged by digital transformation initiatives. Based on the PIB February 2026 data, the Ministry of Law and Justice reported progress under Phase III of the e-Courts Mission Mode Project, which is aimed at transforming courts in the country into digital and paperless institutions. It states that 6.37 billion pages of records have been digitized, virtual courts and video conferencing have been expanded nationwide, and e-filing and e-payments have been widely adopted. With AI-enabled applications such as Digital Courts 2.1 and integration of cloud-based repositories, the initiative strengthens efficiency and accessibility, marking a significant leap in the country’s legal technology market.

India Court Records Digitization: High Court & District Court Pages Digitized According to Official Government Data (As of December 2025)

|

High Court |

Total Pages Digitized in High Court |

Total Pages Digitized in District Courts |

|

Allahabad |

57,74,41,007 |

1,68,69,63,743 |

|

Andhra Pradesh |

3,41,11,865 |

17,28,50,732 |

|

Bombay |

8,90,63,956 |

22,07,485 |

|

Calcutta |

5,95,17,135 |

0 |

|

Chhattisgarh |

24,26,800 |

1,91,84,603 |

|

Delhi |

23,46,18,073 |

10,48,83,922 |

|

Gauhati - Arunachal Pradesh |

5,06,407 |

1,26,322 |

|

Gauhati - Assam |

2,97,53,593 |

15,58,31,203 |

|

Gauhati - Mizoram |

12,31,287 |

20,97,820 |

|

Gujarat |

16,98,629 |

11,64,409 |

|

Himachal Pradesh |

79,15,775 |

11,81,757 |

|

Jammu & Kashmir and Ladakh |

4,11,76,756 |

2,50,11,814 |

|

Jharkhand |

3,01,84,408 |

96,24,854 |

|

Karnataka |

5,14,20,668 |

4,63,47,270 |

|

Kerala |

8,17,95,531 |

1,71,13,720 |

|

Madhya Pradesh |

24,62,88,505 |

66,68,95,995 |

|

Madras |

20,76,93,848 |

13,16,62,142 |

|

Manipur |

58,56,075 |

57,36,785 |

|

Meghalaya |

11,56,596 |

38,20,961 |

|

Orissa |

5,33,13,761 |

17,36,02,357 |

|

Patna |

2,40,49,339 |

2,39,56,123 |

|

Punjab & Haryana |

29,46,04,020 |

62,82,06,241 |

|

Rajasthan |

13,44,36,567 |

3,50,10,815 |

|

Sikkim |

11,73,135 |

54,15,378 |

|

Telangana |

12,85,86,477 |

7,61,42,250 |

|

Tripura |

54,39,454 |

5,62,558 |

|

Uttarakhand |

2,41,91,236 |

1,33,14,115 |

|

Total |

2,36,96,50,903 |

4,00,89,15,374 |

Source: PIB

Europe Market Insights

Europe legal technology market has adopted a prominent position across the global dynamics propelled by the stringent data protection frameworks, which compel law firms and companies to adopt advanced compliance tools and secure digital workflows. The region’s market includes a blend of established technology-based firms and innovative startups that are leveraging AI and multilingual capabilities to serve cross-border legal requirements. In November 2025, the European Commission reported that it had adopted the DigitalJustice2030 strategy by aiming to accelerate the digitalization of justice systems across the region. The plan is mainly focused on efficiency, resilience, and competitiveness by promoting AI in judicial processes, creating a Europe Legal Data Space, and developing an IT toolbox for Member States, hence making it suitable for standard market growth.

The public and private enterprise adoption of analytics systems to support cross-border legal work drives the growth of the legal technology market in Germany. The country’s market benefits from robust engineering capabilities and collaboration among technology firms, legal practitioners, and academic institutions that are exploring emerging modalities such as AI‑assistance for legal reasoning. Based on the government data, which was published in January 2026, the Hessian judiciary achieved a major milestone by fully implementing electronic files (e-files) across all 83 courts and public prosecutor’s offices, meeting the requirements of Germany’s eJustice Act. Furthermore, it also mentioned that around 10,000 workstations and 450 courtrooms were equipped, enabling digital handling of legal proceedings and investigations, thus denoting a positive market outlook.

The UK legal technology market is solidifying its position in the region on account of substantial government funding grants and legal innovation pilots, which are fostering a favorable ecosystem for AI experimentation and automated legal services. Developers in the country are mainly focused on solutions that streamline document automation, assist legal research with AI, and facilitate efficient case management. In this context, the UK Ministry of Justice, in July 2025, published the AI Action Plan for Justice, which outlines the significance of artificial intelligence that will be responsibly integrated across courts, tribunals, prisons, probation, and related services. The plan aims to make the justice system in England and Wales faster and more accessible, which includes efforts to reduce court backlogs and improve rehabilitation outcomes. Furthermore, it focuses on strengthening governance and infrastructure, embedding AI in high-impact use cases, and investing in workforce capability and partnerships.

Key Legal Technology Market Players:

- Thomson Reuters Corporation (U.S.)

- RELX plc - (LexisNexis Legal & Professional division) (UK)

- DocuSign, Inc. (U.S.)

- Themis Solutions Inc. (Clio) (Canada)

- CS Disco, Inc. (U.S.)

- HaystackID LLC (U.S.)

- Everlaw, Inc. (U.S.)

- iManage, LLC (U.S.)

- Ironclad, Inc. (U.S.)

- ContractPod Technologies Ltd. (UK)

- Luminance Technologies Ltd. (UK)

- LegalOn Technologies Co., Ltd. (Japan)

- SpotDraft Solutions Private Limited (India)

- Leegality (India)

- CaseMine (India)

- XMart Labs Sdn. Bhd (Malaysia)

- Bereev Sdn. Bhd. (Malaysia)

- Boss Boleh Sdn. Bhd. (Malaysia)

- Eudia, Inc. (U.S.)

- HighQ Solutions Limited (UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Thomson Reuters is one of the most prominent players that operates in legal information and software solutions. The company is providing a suite of legal research, compliance, and practice management tools. Besides, Thomson makes heavy investments in AI-based solutions, contract management, and regulatory compliance tools, which are allowing it to maintain leadership through continuous innovation and acquisitions.

- LexisNexis, which is part of RELX Group, is a provider of legal, regulatory, and business information services and focuses on legal research, analytics, and e-discovery. The company’s platforms provide improved search capabilities, AI-based understandings, and document automation for law firms, corporations, and government agencies.

- DocuSign is yet another prominent player in this field that provides e-signature and digital transaction management solutions, revolutionizing contract execution and workflow automation for legal and business environments. The company’s cloud-based platform makes sure there is a secure, legally binding electronic signature, document tracking, and contract lifecycle management.

- Clio is a specialist player in terms of cloud-based management software for law firms, providing tools for case management, billing, client collaboration, and document automation. The company’s strategy is mainly focused on accessibility for small and mid-sized law firms by expanding into enterprise-grade solutions through acquisitions and partnerships.

- DISCO is focused on litigation technology and e-discovery solutions, and it is offering AI-powered tools for document review, case management, and legal research. The company makes investments in AI, cloud deployment, and cybersecurity to maintain defensibility in large-scale, complex litigation.

Below is the list of some prominent players operating in the global market:

The global legal technology market is intensely competitive, which is dominated by U.S. and UK-based firms with strong product portfolios. Companies such as Thomson Reuters, RELX Group, DocuSign, and Ironclad lead in terms of legal research, analytics, and contract lifecycle management, whereas Clio serves law firms with cloud-based practice solutions. AI integration, cloud deployment, mergers & acquisitions, and global expansion are considered to be central to sustaining competitive advantage in this field. For instance, in February 2026, BriefCatch reported that it had acquired WordRake’s core product and patented technology assets, including twelve U.S. patents and its in-line editing algorithms, in a transaction which is aimed at strengthening workflow-embedded legal writing tools, hence positively impacting the market’s growth and exposure.

Corporate Landscape of the Legal Technology Market:

Recent Developments

- In February 2026, HaystackID announced that it had launched AI Governance Services, which is a new portfolio designed to help organizations operationalize responsible and defensible AI oversight by embedding governance, validation, and audit-ready evidence into enterprise workflows.

- In February 2026, DISCO announced the launch of the industry’s first scaled agentic AI tool for fact investigation and eDiscovery, thereby enhancing its Cecilia Q&A platform with autonomous, multi-step reasoning to deliver deeper, faster analysis on large and complex datasets.

- Report ID: 6215

- Published Date: Mar 11, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.