Intravenous Product Packaging Market Outlook:

Intravenous Product Packaging Market size was valued at USD 6.4 billion in 2025 and is projected to reach USD 15.5 billion by the end of 2035, rising at a CAGR of 9.2% during the forecast period, i.e., 2026-2035. In 2026, the industry size of intravenous product packaging is assessed at USD 7.1 billion.

The demand for the intravenous product packaging market is closely related to the scale of injectable drug use, hospital admissions, and government-supported pharmaceutical manufacturing programs. According to the American Hospital Association, March 2025 data, nearly 36 million hospital admissions occur annually in the U.S., with a substantial portion of patients requiring IV fluids, antibiotics, or parenteral nutrition during inpatient treatment. Injectable therapies represent a major component of hospital drug utilization because they allow rapid systemic delivery and precise dosing in acute care settings. Further, the sterile injectable manufacturing and packaging infrastructure is a key component of supply chain security initiatives, mainly for essential medicines used in emergency and critical care. These policy priorities are reinforcing the investment in sterile packaging lines containers closure integrity systems, and high-quality IV bag production facilities across Europe and North America.

Besides, the government health expenditure growth and rising injectable medicine utilization in the public health programs are also expanding the demand for the IV packaging systems. As per the WHO January 2024 data, the global health expenditure reached USD 9.8 trillion, with hospitals accounting for the largest share of spending on medicines and medical supplies. Hospital procurement of infusion fluids, oncology injectables, anesthetics, and biologics requires sterile packaging formats capable of meeting the strict regulatory and stability requirements. Moreover, the regulatory agencies, including the FDA and EMA, continue to emphasize packaging integrity and sterility assurance via current good manufacturing practice requirements, reinforcing the importance of validated IV packaging materials and fill finish process in pharmaceutical supply chains.

Key Intravenous Product Packaging Market Insights Summary:

Regional Highlights:

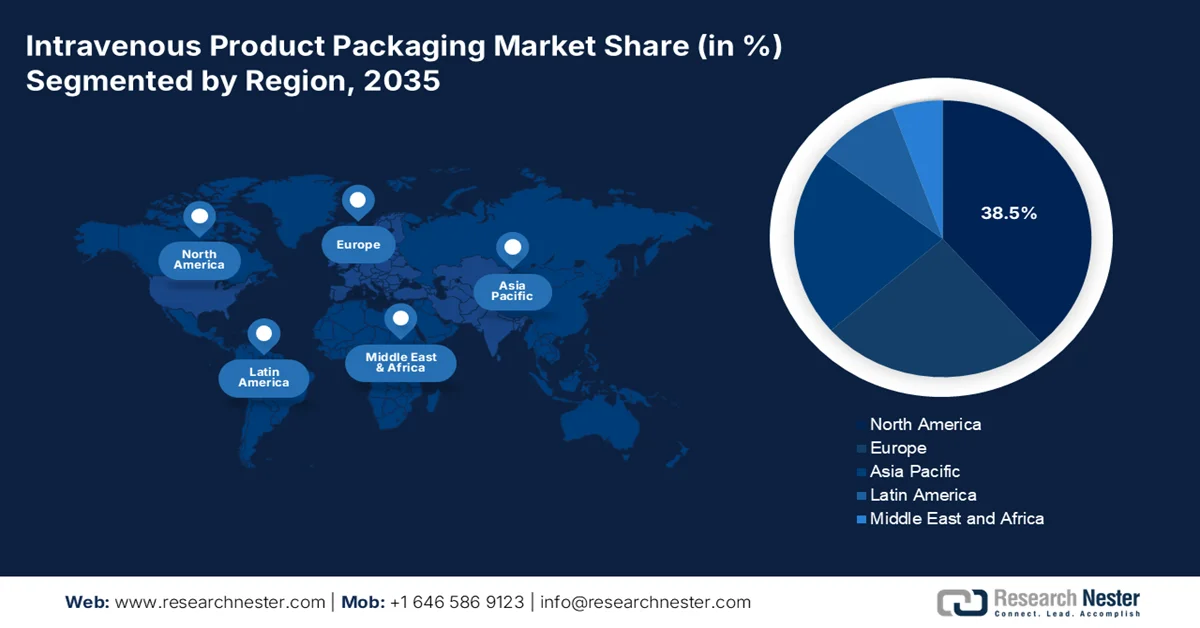

- The intravenous product packaging market in North America is anticipated to command a 38.5% share by 2035, attributed to the high volume of hospital-based acute care procedures and advanced healthcare infrastructure

- Asia Pacific is projected to witness the fastest growth at a CAGR of 6.8% during 2026–2035, fueled by rapid healthcare infrastructure expansion and rising government health expenditure

Segment Insights:

- In the intravenous product packaging market, the multi-port sub-segment under port type is expected to capture a 65.4% share by 2035, propelled by the clinical necessity for simultaneous or secondary drug infusions without compromising sterile pathways

- Under the packaging format segment, flexible packaging is set to dominate over the forecast period 2026–2035, impelled by improved patient safety and logistical advantages

Key Growth Trends:

- Aging population driving chronic disease management

- Increasing injectable drug approvals

Major Challenges:

- High cost of material transition

- Risk of quality failures

Key Players: Baxter International Inc. (U.S.), Becton, Dickinson and Company (U.S.), West Pharmaceutical Services, Inc. (U.S.), Berry Global Group, Inc. (U.S.), Pfizer Inc. (Hospira) (U.S.), Fresenius Kabi AG (Germany), Gerresheimer AG (Germany), SCHOTT AG (Germany), Sartorius AG (Germany), B. Braun Melsungen AG (Germany), Nipro Corporation (Japan), Terumo Corporation (Japan), Otsuka Pharmaceutical Factory, Inc. (Japan), DWK Life Sciences GmbH (UK).

Global Intravenous Product Packaging Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 6.4 billion

- 2026 Market Size: USD 7.1 billion

- Projected Market Size: USD 15.5 billion by 2035

- Growth Forecasts: 9.2% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (38.5% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, China, Japan, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Mexico, Indonesia

Last updated on : 25 March, 2026

Intravenous Product Packaging Market - Growth Drivers and Challenges

Growth Drivers

- Aging population driving chronic disease management: The global demographic shift toward an older population is the key demand driver for the intravenous product packaging market, as the elderly patients require more frequent hospitalizations and infusion therapies for chronic conditions. According to the NCOA June 2024 report, the number of U.S. people aged 65 and older is projected to reach 78.3 million by 2040. This population segment accounts for a certain percentage of all hospital stays involving IV therapy, driving a consistent demand for the IV bags, administration sets, and pre-filled syringes. Healthcare systems are responding by expanding geriatric care units and home health programs, both intensive users of IV products. Moreover, the manufacturers can target this demographic by developing user-friendly packaging designs suitable for elderly patients and home care settings.

- Increasing injectable drug approvals: Government regulators report a growing number of injectable drug approvals, mainly biologics and specialty therapies that require sterile packaging. The U.S. FDA notes that the biologics and injectable medicines represent a rapidly expanding portion of drug approvals, including the monoclonal antibody vaccines and oncology therapies that are delivered intravenously. Additionally, the FDA's March 2026 report states that biologic drugs account for 51% of the drug spending in the pharmaceutical development pipeline. These therapies require sterile packaging such as glass vials, IV bags, and polymer containers with validated container closure integrity systems. As regulatory agencies approve more parenteral medicines, pharmaceutical manufacturers expand sterile fill-finish capacity and packaging product lines.

- Healthcare workforce safety regulations: Occupational safety regulations governing healthcare worker protection from hazardous drug exposure are driving the demand for closed system IV packaging. The National Institute for Occupational Safety and Health publishes a list of hazardous drugs used in healthcare setting many of which are administered intravenously. OSHA enforcement activities under the General Duty Clause increasingly cite healthcare facilities for inadequate protection against antineoplastic drug exposure during the IV preparation and administration. This regulatory environment has surged the adoption of closed system transfer devices and is ready to administer IV packaging formats that minimize the manipulation. Manufacturers should develop integrated packaging solutions that reduce manipulation steps and incorporate engineering controls for exposure prevention.

Challenges

- High cost of material transition: The intravenous product packaging market is shifting away from traditional PVC due to environmental and safety concerns. The global non-PVC empty IV bags market is growing as the healthcare providers demand safer alternatives, such as polypropylene and ethylene vinyl acetate. However, transitioning to these advanced materials requires a significant R&D investment and process reengineering. For example, adopting cycling olefin polymers as a glass alternative reduces weight but necessitates new manufacturing protocols. While this creates a intravenous product packaging market opportunity, the high cost of innovation and the need for new regulatory approvals for material drug compatibility pose a formidable challenge for the smaller manufacturers with limited capital.

- Risk of quality failures: Packaging failures leading to contamination can result in costly recalls and reputational damage. For example, an FDA warning letter was issued to an India manufacturer regarding the visible contamination in polypropylene IV bags used for epidural ropivacaine. The FDA criticized the company for releasing batches despite known issues and for inadequately assessing the risk, which could lead to severe patient harm, such as meningitis or nerve damage. The company had to recall the batches and implement systemic CAPA programs. For new players in the intravenous product packaging market, these failures can be catastrophic, indicating the need for flawless quality control from day one.

Intravenous Product Packaging Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

9.2% |

|

Base Year Market Size (2025) |

USD 6.4 billion |

|

Forecast Year Market Size (2035) |

USD 15.5 billion |

|

Regional Scope |

|

Intravenous Product Packaging Market Segmentation:

Port Type Segment Analysis

Within the port type segment, the multi-port sub-segment is dominating and is poised to hold the share value of 65.4% by the end of 2035. The segment is driven by the clinical necessity for simultaneous or secondary drug infusions without compromising the sterile fluid pathway. These integrated ports allow healthcare providers to administer incompatible medications separately or deliver intermittent piggyback infusions, reducing the need for additional venipunctures and minimizing line disruptions. According to the NLM August 2021 study, nearly 62% of the patients who received IV therapy in U.S. hospitals required administration of two or more medications, a scenario optimally managed by the multiport bag systems. This design significantly lowers the risk of touch contamination at the injection site, a critical factor in reducing the central line associated with the bloodstream infections.

Packaging Format Segment Analysis

Under the packaging format segment, the flexible packaging, mainly plastic IV bags, is overtaking the rigid glass bottles due to patient safety and logistical advantages. The flexible containers are non-air dependent, eliminating the need for a vent tube and thereby reducing the risk of air embolism and airborne contamination during the administration. From a sustainability perspective, the EPA recognizes the shift towards source reduction, flexible plastic bags are lighter and take up less space in landfills and incinerators compared to glass. For healthcare providers, the ASHP notes that the flexible packaging is easier to store, transport, and dispose of, reducing the hospital costs and the physical burden on healthcare staff handling large volumes of IV fluids.

End user Segment Analysis

In the end user segment, the plastic polymer is leading in the intravenous product packaging market by 2035. The shift from glass and PVC to polypropylene and polyethylene is driven by the chemical compatibility and safety regulations. According to the NLM July 2025 study, nearly 26.2% of the produced polymer was polyethylene. The FDA’s Center for Drug Evaluation and Research has pushed for packaging materials that minimize leachables and extractables into sensitive IV drugs. Advanced multilayer plastic films using PP/PE provide superior barrier properties while being free from the plasticizers found in traditional PVC, which has flagged as potential endocrine disruptors. Further, the U.S. Department of Energy supports the development of bio-based plastics, promoting manufacturers to adopt polymers that reduce the carbon footprint of medical waste. These materials also offer better clarity for inspecting particulate matter in solutions, a key requirement for compliance with United States Pharmacopeia (USP) standards.

Our in-depth analysis of the intravenous product packaging market includes the following segments:

|

Segment |

Subsegments |

|

Product Type |

|

|

Material |

|

|

End user |

|

|

Drug Type |

|

|

Packaging Format |

|

|

Port Type |

|

|

Closure Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Intravenous Product Packaging Market - Regional Analysis

North America Market Insights

North America is dominating the intravenous product packaging market and is expected to hold the regional revenue share of 38.5% by the end of 2035. The region is defined by the presence of an advanced healthcare infrastructure and stringent regulatory standards that govern product quality and patient safety. The market demand in the region is mainly driven by the high volume of hospital-based acute care surgical procedures and critical care interventions that require intravenous therapy as a standard component of treatment. Moreover, a significant trend shaping the market is the ongoing transition from the rigid glass containers to flexible multi-layer plastic packaging, driven by the clinical advantages such as reduced risk of air embolism and improved handling efficiency for healthcare staff. Further, the presence of large, integrated healthcare systems and group purchasing organizations also influences packaging specifications, favoring standardized products that can be deployed across extensive hospital networks.

The increasing utilization of injectable medicines, strict regulatory oversight on pharmaceutical packaging, and rising healthcare expenditure are driving the intravenous product packaging market in U.S. According to the NLM June 2023 study the U.S. Food and Drug Administration regulates packaging inserts container labeling and safety requirements for prescription medicines reinforcing the need for validated sterile packaging formats such as vials ampoules and IV bags used in injectable therapies. The Centers for Medicare & Medicaid Services January 2026 data reported that U.S. national health expenditures reached approximately USD 5.3 trillion in 2024, with hospital services representing the largest spending category, increasing demand for infusion therapies and associated packaging systems. Furthermore, the medication packaging design has gained regulatory attention because medication errors and preventable adverse drug reactions have historically cost the U.S. healthcare system in preventable expenses. These data show an optimistic growth intravenous product packaging market in U.S.

The stringent regulatory oversight, increasing hospital use of the infusion therapies, and growing pharmaceutical manufacturing compliance requirements are shaping the intravenous product packaging market in Canada. According to the Zenodo April 2025 data, the Container Closure Systems, including IV bags and flexible drug delivery containers, play a critical role in preserving drug sterility and preventing chemical or microbiological contamination during storage and administration. Moreover, in Canada, Health Canada regulates pharmaceutical packaging under risk-based evaluation frameworks aligned with International Council for Harmonization standards, ensuring packaging materials and container systems maintain drug stability throughout their lifecycle. IV bags used in hospitals are commonly manufactured from polyvinyl chloride, ethylene vinyl acetate, polyolefins such as polyethylene and polypropylene, and multilayer polymer films, each selected based on compatibility with drugs, sterilization methods, and safety considerations, therefore driving the market expansion and growth.

APAC Market Insights

The Asia Pacific is projected to emerge as the fastest-growing region during the assessed period, 2026 to 2035, and is expected to grow at a CAGR of 6.8%. The region is driven by the rapid healthcare infrastructure expansion, aging population, and increasing government health expenditure across the major economies. The region’s growth trajectory is supported by the national health insurance expansions in China and India, which have increased hospital access for millions of citizens, directly correlating with high consumption of IV fluids and associated packaging. A significant trend shaping the intravenous product packaging market is the transition from glass containers to flexible plastic packaging, mainly in urban hospitals adopting western clinical practices. The region's medical device market, including IV packaging, is projected to grow at twice the rate of developed markets, attracting significant manufacturing investment from global and regional players.

The intravenous product packaging market in India is expanding alongside the growth of hospital infrastructure, intensive care services, and the increasing use of infusion-based drug delivery systems. The introduction of the advanced infusion technologies, such as Terumo India’s Terufusion Advanced Infusion Systems, in August 2025, is designed to enable connected drug administration in the intensive care units reflects the rising demand for safe and efficient intravenous therapy in the country. On the other hand, the PIB 2024 data indicate that there are nearly 8.39 crore hospital admissions, significantly increasing demand for inpatient treatments where intravenous fluids, antibiotics, and electrolyte solutions are commonly administered. Moreover, the requirement for compliant intravenous packaging systems and container closure technologies is expected to grow steadily across the country’s pharmaceutical manufacturing and healthcare sectors.

Expanding healthcare expenditure, rising hospital treatment volumes, and the large-scale use of injectable medicines in clinical care are fueling the intravenous product packaging market in China. According to the NLM November 2024 study, the country’s total healthcare expenditure reached approximately about USD 1.2 trillion in 2022, reflecting continued government investment in hospital services and pharmaceutical supply chains. China also maintains one of the world’s largest hospital networks. The People’s Republic of China, November 2024 data reported that the country had over 38,000 hospitals in 2023, with significant utilization of intravenous therapies for antibiotics, oncology drugs, electrolyte solutions, and parenteral nutrition in inpatient settings. As hospital infrastructure expands and demand for biologics and infusion therapies increases, China continues to strengthen domestic pharmaceutical manufacturing and sterile packaging capacity to support the growing clinical use of intravenous treatments.

Europe Market Insights

The intravenous product packaging market in Europe is expanding rapidly and is defined by the mature healthcare systems' stringent regulatory oversight from the EMA and increasing harmonization of packaging standards across the member states. The demand is driven by the high hospitalization rates across Western Europe, with the region performing millions of surgical procedures annually, requiring perioperative IV therapy. A significant trend shaping the market is the focus on reducing medical waste, with the European Commission’s Pharmaceutical Strategy pushing for more sustainable packaging materials, including the PVC free alternatives. The European Health Emergency Preparedness and Response Authority has established strategic stockpiles of medical supplies, including IV fluids, creating supplementary demand beyond routine consumption patterns.

The strong pharmaceutical manufacturing infrastructure and the increasing adoption of advanced inspection and quality assurance technologies for the sterile drug containers are driving the intravenous product packaging market in Germany. Growing demand for medicines packaged in IV bags has led the equipment manufacturers to develop specialized inspection solutions to maintain container integrity during high-volume production. For example, in April, Brevetti CEA launched a new inspection machine designed for IV bags, which can handle container sizes ranging from 50 ml to 1000 ml and perform particle inspection, cosmetic inspection, and leak detection, ensuring compliance with pharmaceutical quality standards and minimizing contamination risks. On the other hand, in May 2025, Sanner launched an optimized TabTec CR patient-friendly packaging prioritizing both consumer safety and convenience. These developments show a positive impact on intravenous product packaging market growth.

The rising hospital activity and sustained government healthcare expenditure, which directly increase the use of infusion therapies and sterile injectable medicines, are fueling the intravenous product packaging market in UK. According to the Government of the UK, May 2025 data, the hospitals in England recorded 22.1 million finished consultant episodes in 2024, reflecting the scale of inpatient and day case treatments where intravenous drugs and fluids are administered. On the other hand, the government healthcare spending continues to expand to support clinical services and pharmaceutical supply chains. The UK Office for National Statistics' May 2023 data reported that the total UK healthcare expenditure reached about USD 359 billion in 2022. Increased treatment volumes have raised demand for sterile injectable drugs and infusion therapies, which rely on validated container closure systems and high-integrity packaging materials to maintain sterility and drug stability. The data are fueling the intravenous product packaging market developments.

Key Intravenous Product Packaging Market Players:

- Baxter International Inc. (U.S.)

- Becton, Dickinson and Company (U.S.)

- West Pharmaceutical Services, Inc. (U.S.)

- Berry Global Group, Inc. (U.S.)

- Pfizer Inc. (Hospira) (U.S.)

- Fresenius Kabi AG (Germany)

- Gerresheimer AG (Germany)

- SCHOTT AG (Germany)

- Sartorius AG (Germany)

- B. Braun Melsungen AG (Germany)

- Nipro Corporation (Japan)

- Terumo Corporation (Japan)

- Otsuka Pharmaceutical Factory, Inc. (Japan)

- DWK Life Sciences GmbH (UK)

- Comar (U.S.)

- Omega Packaging (U.S.)

- AptarGroup, Inc., (U.S.)

- Sommaplast (Italy)

- the ALPLA Group (Austria)

- KM Packaging (UK)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Baxter International Inc. leverages its deep heritage in hospital care to drive innovation in intravenous product packaging market solutions. The company is a leading manufacturer of premixed IV drugs and irrigation solutions, necessitating advanced packaging systems such as flexible plastic containers and dual-chamber bags that ensure drug stability and ease of administration. According to the 2024 annual report, the company has made a net sale of USD 10.6 billion.

- Becton, Dickinson, and Company solidifies its position in the intravenous product packaging market by focusing on the medication delivery interface rather than just the primary fluid container. As a global medical technology giant, BD specializes in the critical components that connect IV bags to patient such as pre-filled saline syringes, IV catheters, and advanced administration sets. In 2025, the company made a cash flow of USD 3.430 billion.

- West Pharmaceutical Services Inc is an indispensable partner in the intravenous product packaging market, renowned for its expensive in containment and delivery components. Rather than manufacturing the entire IV bags, the company specializes in the high-precision elastomer components that seal them, such as stoppers, plungers, and needle-free injection ports. Their advancements focus on developing packaging components reduces the contamination.

- Berry Global Group, Inc plays a vital role in the intravenous product packaging market as a leading supplier of rigid plastic packaging and healthcare components. The company leverages its extensive material science capabilities to manufacture a wide array of products essential for IV delivery, including bottle closure twist-off caps for IV containers and specialized connectors.

- Pfizer Inc is a major end user and innovator within the intravenous product packaging market. As one of the world’s largest suppliers of injectable drugs and IV solutions, the company dictates packaging trends by demanding injectable drugs and IV solutions. Pfizer dictates packaging trends by demanding high-quality compatible systems for its vast portfolio. The company uses advanced flexible container packaging for its premix IV drugs, allowing for read-to-administer formats.

Here is a list of key players operating in the global intravenous product packaging market:

The global intravenous product packaging market is highly competitive and consolidated, dominated by a few multinational corporations alongside specialized regional players. The key strategic initiatives include a strong focus on technological innovation to enhance patient safety, such as the development of non-PVC and multi-layer film materials to reduce drug absorption and the risk of leaching. Moreover, mergers and acquisitions are prevalent as larger firms seek to expand their geographic footprint and product portfolios, primarily in emerging markets. For example, in December 2021, Comar expanded the packaging portfolio with the acquisition of Omega Packaging. Further, there is a significant push towards eco-friendly and sustainable packaging solutions in response to regulatory pressures and environmental concerns.

Corporate Landscape of the Intravenous Product Packaging Market:

Recent Developments

- In December 2025, AptarGroup, Inc., a global leader in drug and consumer product dosing, dispensing, and protection technologies, announced that it had acquired Sommaplast, a specialized provider of oral dosing pharma packaging solutions, such as closures, droppers, dispensers, and dosing cups, based in Brazil.

- In October 2025, Terumo Corporation announced the successful completion of its acquisition of a Drug Product Plant and associated Quality Control Laboratory operations from WuXi Biologics in Leverkusen, Germany with the transaction officially closing on September 30, 2025.

- In June 2025, the ALPLA Group is strengthening ALPLAinject, its injection-moulding division, with the acquisition of KM Packaging. This acquisition means the international plastic packaging specialist will now also manufacture high-quality closures for tubes, bottles and jars, including in clean rooms if desired, at six additional sites in Germany, Austria, Poland and the U.S.

- Report ID: 8473

- Published Date: Mar 25, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.