Industrial Demand Response Management Systems Market Outlook:

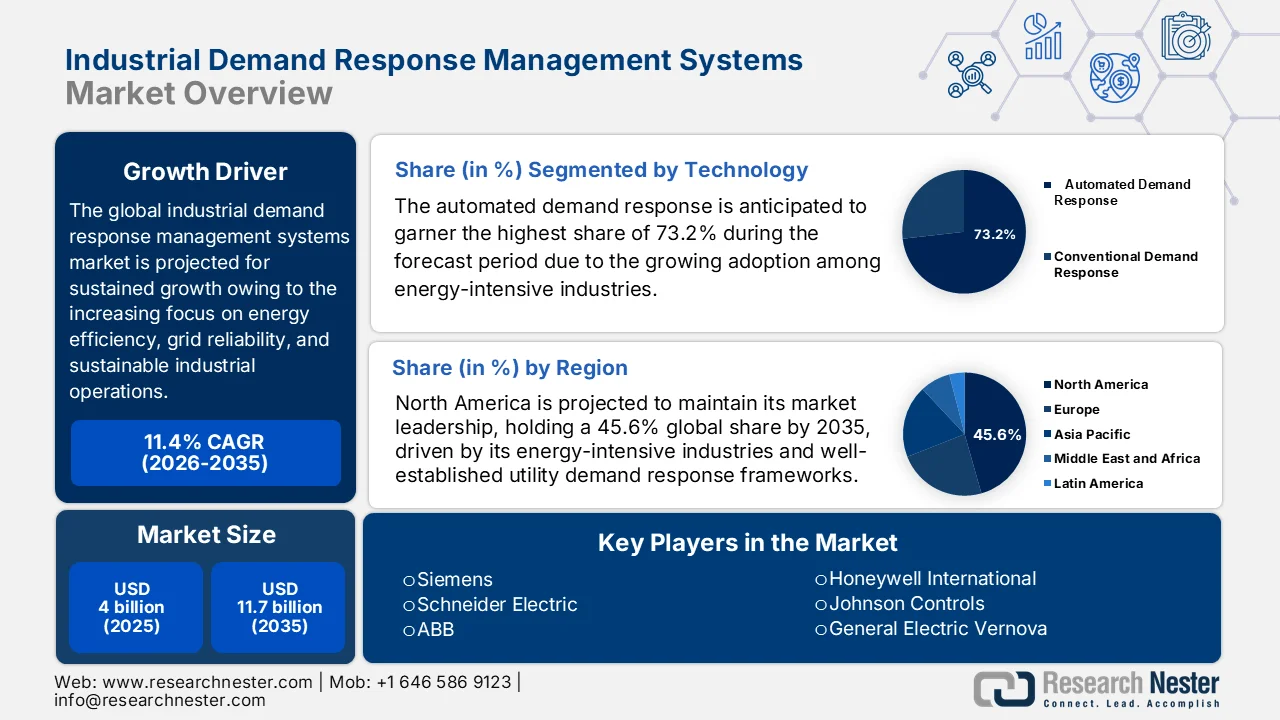

Industrial Demand Response Management Systems Market size was over USD 4 billion in 2025 and is expected to reach USD 11.7 billion by the end of 2035, growing at around 11.4% CAGR during the forecast period, i.e., 2026-2035. In 2026, the industry size of industrial demand response management systems is assessed at USD 4.4 billion.

The industrial demand response management systems market is projected to experience solid growth in the next decade, owing to the increasing focus on energy efficiency, grid reliability, and sustainable industrial operations. Industries are opting for demand response management systems to optimize electricity consumption, reduce peak load demand, and support participation in smart grid programs. According to the article published by the International Energy Agency in July 2023, demand response has become a highly critical tool for balancing grids, which are dominated by variable renewables such as wind and solar, yet deployment still lags behind Net Zero targets. Countries such as Australia, Europe, and Korea are advancing with new regulations and pilot programs, whereas global efforts need to be accelerated to reach 500 GW of DR capacity by 2030. International initiatives such as IEA’s 3DEN, ISGAN, and mission innovation green-powered future mission are fostering collaboration, innovation, and digitalization to expand demand‑side flexibility worldwide.

Furthermore, integrating technologies such as artificial intelligence, Internet of Things, and cloud-based analytics is enhancing the effectiveness of demand response strategies. Growing investments in smart grid infrastructure and rising adoption of renewable energy sources are also contributing to the industrial demand response management systems market’s expansion. In this context, the Energy Information Administration revealed that industrial participation remains a significant component of demand response programs, with enrolled industrial customers increasing from 39,808 in 2023 to 43,608 in 2024, indicating renewed engagement from energy-intensive facilities. Meanwhile, the reported industrial energy savings declined after 2022, but the EIA notes that the reduction in 2023 and 2024 reflects a reclassification in annual filings rather than a proportional decrease in demand response activity. Overall, the data indicate continued reliance on industrial load flexibility to support grid reliability and peak-load management.

U.S. Industrial Demand Response Market Performance and Demand Savings Trends 2022 - 2024

|

Metric (Industrial Sector) |

2022 |

2023 |

2024 |

YoY Change (2023-2024) |

|

Number of Customers Enrolled |

39,365 |

39,808 |

43,608 |

+9.5% |

|

Energy Savings (MWh) |

162,081 |

69,649 |

73,367 |

+5.3% |

|

Potential Peak Demand Savings (MW) |

14,864 |

13,840 |

14,439 |

+4.3% |

|

Actual Peak Demand Savings (MW) |

6,613 |

4,009 |

5,080 |

+26.7% |

Source: EIA

Key Industrial Demand Response Management Systems Market Insights Summary:

Regional Highlights:

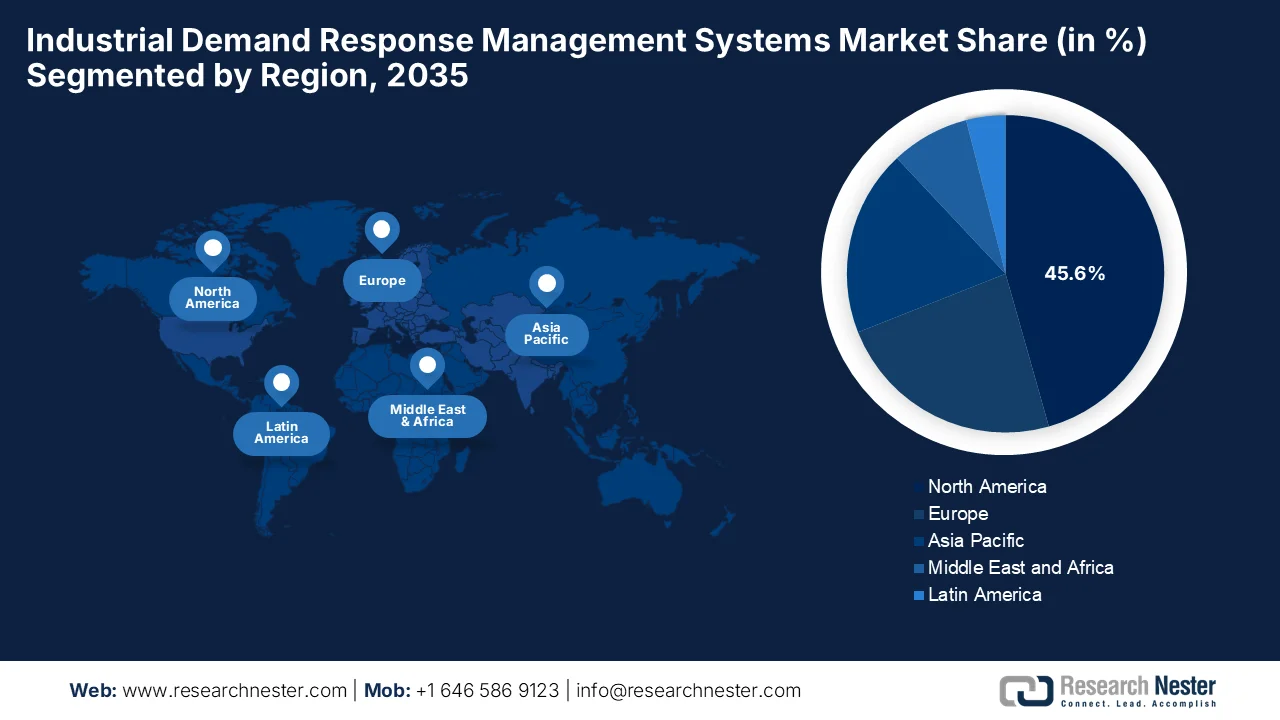

- By 2035, North America is projected to capture a 45.6% share of the industrial demand response management systems market, reinforced by energy-intensive industries, mature utility demand response frameworks, and advanced grid infrastructure

- Asia Pacific is anticipated to witness considerable expansion in the 2026-2035 period, stimulated by rapid industrialization, increasing smart grid investments, and national decarbonization policies across manufacturing hubs

Segment Insights:

- The automated demand response segment is expected to account for 73.2% share by 2035 in the industrial demand response management systems market, supported by rising adoption among energy-intensive industries seeking efficient and automated energy management solutions

- By 2035, the manufacturing sector is forecast to secure a considerable revenue share, fueled by high and continuous electricity consumption that creates opportunities for demand shifting and energy optimization without compromising production efficiency

Key Growth Trends:

- Rising energy costs

- Expansion of smart grid infrastructure

Major Challenges:

- Operational complexity and production constraints

- Limited awareness and skills gap

Key Players: Siemens (Germany), Schneider Electric (France), ABB (Switzerland), Honeywell International (U.S.), Johnson Controls (Ireland), General Electric Vernova (U.S.), Enel X (Italy),AutoGrid Systems (U.S.), EnergyHub (U.S.), CPower Energy Management (U.S.), Generac (U.S.),CPower (U.S.), Fujitsu (Japan).

Global Industrial Demand Response Management Systems Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 4 billion

- 2026 Market Size: USD 4.4 billion

- Projected Market Size: USD 11.7 billion by 2035

- Growth Forecasts: 11.4% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (45.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, South Korea

- Emerging Countries: India, Australia, France, United Kingdom, Canada

Last updated on : 23 June, 2026

Industrial Demand Response Management Systems Market - Growth Drivers and Challenges

Growth Drivers

- Rising energy costs: This is the main boosting factor for the industrial demand response management systems market. The solution enables facilities to shift or curtail energy consumption during peak pricing periods, which also helps to lower operational costs. Growing volatility in energy markets encourages businesses to optimize consumption and improve overall energy efficiency. In May 2023, the IEA reported that rising energy prices initially reduce firms’ productivity by lowering capacity utilization, with estimates showing a 5% price increase cutting productivity by 0.4% after one year. The same report also stated that, however, in the medium term, firms often adapt through investment and efficiency gains, with a 10% price shock linked to a 0.9 p.p. rise in productivity growth after four years, thereby encouraging industries to opt for demand response management systems.

- Expansion of smart grid infrastructure: The deployment of smart grids is creating lucrative opportunities for pioneers operating in the industrial demand response management systems market. Advanced metering and automated communication technologies allow industries to participate effectively in demand response programs with the main goal of improving grid reliability and thereby generating financial incentives for energy consumption adjustments. In March 2026, the article published by UNSDSN revealed that smart grids are emerging as the backbone of a resilient energy future wherein the modernization of aging infrastructure meets rising demand, climate pressures, and the need for a very reliable digital-age power. It is integrating advanced monitoring, automation, distributed energy resources, and two‑way communication to enable flexible and sustainable operations, thereby supporting renewables and electrification.

Challenges

- Operational complexity and production constraints: Industrial facilities across different nations have an increased priority towards operational continuity and production efficiency, which makes participation in demand response programs a major challenge. Most of the manufacturing processes, chemical operations, and energy-intensive industrial activities necessitate continuous power supply and cannot easily reduce or shift loads without showing any effect on productivity, product quality, or equipment performance. Apart from this, demand response scenarios might conflict with production schedules, thereby creating concerns about operational disruptions and financial losses. Furthermore, accurately identifying flexible loads and implementing automated control strategies requires detailed process analysis and advanced system coordination, thereby negatively impacting the growth of the industrial demand response management systems market.

- Limited awareness and skills gap: There has been a growing interest in terms of energy efficiency and grid flexibility, but still, most of the industrial organizations do not have sufficient awareness of the operational and financial benefits offered by these systems. In this context, decision makers see DRMS as an energy-saving tool rather than a strategic asset that is capable of generating revenue, enhancing sustainability, and improving grid participation. In addition, successful implementation necessitates knowledge in terms of energy markets, automation systems, data analytics, and grid operations. Therefore, most of the industrial facilities are witnessing a shortage of personnel with the necessary technical skills to manage sophisticated demand response programs effectively, hindering the expansion of the industrial demand response management systems market.

Industrial Demand Response Management Systems Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

11.4% |

|

Base Year Market Size (2025) |

USD 4 billion |

|

Forecast Year Market Size (2035) |

USD 11.7 billion |

|

Regional Scope |

|

Industrial Demand Response Management Systems Market Segmentation:

Technology Segment Analysis

The automated demand response, which is under the technology segment, is anticipated to garner the highest share of 73.2% during the forecast period. The segment’s dominating position is mainly driven by the growing adoption among energy-intensive industries that are looking for efficient and automated energy management solutions. ADR systems enable immediate, rule-based load adjustments in response to utility signals, dynamic pricing, or grid conditions, eliminating the need for manual intervention, thus benefiting the overall industrial demand response management systems market. For instance, in February 2023, Tata Power announced a partnership with AutoGrid to roll out an AI‑enabled smart energy management system in Mumbai, which engages 55,000 residential and 6,000 large C&I customers. The program combines behavioral demand response with automated demand response through its EZ Home platform.

End use Segment Analysis

By the end of 2035, the manufacturing sector, which is a part of the end use category, is expected to grow with a considerable revenue share in the industrial demand response management systems market. The growth of the sub-segment is attributed to its high and continuous electricity consumption, which makes it well-suited for demand response programs. Energy-intensive operations such as metal processing, chemical production, food processing, and automotive manufacturing provide viable opportunities for load shifting and demand optimization without any compromise on production efficiency or output quality. In April 2026, Schneider Electric, in collaboration with Microsoft, introduced agentic manufacturing capabilities at Hannover Messe 2026, which was powered by Azure AI and EcoStruxure automation expert. The company also mentions that their unified platform collapses traditional automation phases into a single traceable workflow, with the industrial copilot.

Services Segment Analysis

Managed services are predicted to hold a notable share in the industrial demand response management systems market during the forecast period. The segment’s growth is effectively propelled by growing reliance on third-party expertise to manage complex energy optimization activities. Most of the industrial organizations do not have dedicated in-house teams to monitor energy markets, coordinate with utilities, or optimize demand response participation. Therefore, these managed service providers take responsibility for system setup, event execution, compliance management, and performance reporting, which in turn allows industries to minimize operational burden, thereby maximizing financial benefits from demand response programs. In addition, these services help industries quickly scale demand response participation across multiple facilities without significant capital investment in internal infrastructure, hence positively contributing to the segment’s expansion.

Our in-depth analysis of the industrial demand response management systems market includes the following segments:

|

Segment |

Subsegments |

|

Technology |

|

|

End use |

|

|

Services |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Industrial Demand Response Management Systems Market - Regional Analysis

North America Market Insights

The North America industrial demand response management systems market is projected to dominate with a total share of 45.6% by the end of 2035. The region’s leadership is mainly propelled by the presence of energy-intensive industries, well-established utility demand response frameworks, and advanced grid infrastructure. The region’s high level of industrial automation and strong focus on peak-load cost optimization also drive adoption. In May 2024, the Irvine Ranch Water District Load Shifting and demand response pilot project tested a novel technology platform to automate load shifting and demand response at water treatment and pumping facilities, with a main goal to cut peak demand, reduce energy bills, and lower emissions. This project demonstrated benefits through battery energy storage systems, thus making it suitable for standard market growth.

The nation accelerates its transition toward a modernized, highly electrified smart grid, driving expansion of the U.S. industrial demand response management systems market. The country’s market also benefits from supportive federal policies under the Inflation Reduction Act, regional grid modernizations, and the ongoing rollout of advanced metering infrastructure by major utility companies. As per the June 2022 reports by OSTI, the DOE Better Buildings, Better Plants Program provides industrial facilities with guidance on managing peak electricity demand through demand response initiatives. It also explains how manufacturers and water utilities can leverage time‑varying rates, smart technologies, and demand response programs to reduce energy bills and improve efficiency. It resulted in a substantial 25% reduction in energy intensity over ten years, and it gained access to DOE resources, technical support, and recognition for leadership in energy efficiency, hence supporting the market’s expansion.

In Canada, the industrial demand response management systems market has gained immense exposure owing to the country’s extensive clean energy grid goals and provincial initiatives to optimize regional power transmission. Growth is also supported by provincial utilities and independent system operators, which actively deploy demand response programs to integrate growing intermittent renewable capacity and manage peak winter heating strains. Based on the government data published in May 2026, the country is laying the foundation for a clean, reliable, and affordable electricity grid to meet rising demand as households and industries shift from fossil fuels to electrification. In addition, it also mentions the Clean Electricity Regulations, which were finalized in 2024, and it sets limits on fossil fuel generation, which is set to begin in 2035, ensuring a net‑zero electricity system by 2050, thereby maintaining affordability and reliability.

APAC Market Insights

The Asia Pacific industrial demand response management systems market is expected to grow at a considerable rate from 2026 to 2035. The region’s upliftment is mainly driven by massive industrialization, expanding smart grid investments, and national decarbonization policies across major manufacturing hubs. Governments in countries such as Japan, South Korea, China, and Australia are proactively reshaping their energy frameworks to support grid modernization, integrating advanced telemetry and digital communication networks to handle the influx of variable renewable energy sources. For instance, Tokyo Electric Power Company Energy Partner, Inc. began a demand response demonstration in February 2024 along with Shizen Connect Co., Ltd. by using its energy management system to remotely control home battery storage systems. The company also notes that this project tested both economic benefits, such as reduced procurement costs, and technical feasibility, along with battery responsiveness to remote commands.

The state-led initiatives are deploying provincial demand response frameworks to handle the massive influx of variable solar and wind energy, driving the growth of the industrial demand response management systems market in China. The country’s market is also supported by its vast, energy-dense industrial manufacturing base, which consists of steel production, chemical processing, automotive manufacturing, and tech fabrication hubs integrating automated energy management systems. Based on the government data published in June 2026, China launched a three‑year action plan to cut energy use and carbon emissions across nine high‑consumption industries, including steel, cement, aluminum, and coal‑fired power. This particular initiative sets targets through 2028 by focusing on efficiency upgrades, funding support, and stricter standards to drive industrial modernization, thus denoting a huge opportunity for the industrial demand response management systems market to grow.

In India, the industrial demand response management systems market is being driven by the aggressive modernization of its power infrastructure to integrate its influx of utility-scale solar and wind energy. The market is also supported by the energy-intensive manufacturing sector, along with a booming network of hyperscale data centers, which are proactively deploying automated energy management platforms. In April 2026, the article published by FSR Global revealed that India’s electricity system faces a flexibility challenge as installed renewable capacity surpasses 50%, but actual generation lags due to variability. Meanwhile, the peak demand is already hitting 250 GW, and rising cooling loads, EV adoption, and industrial growth are straining the grid. In this context, demand response offers a rapid, cost‑effective solution by shifting consumption, such as pre‑cooling buildings, adjusting AC loads, or midday EV charging, to better align demand with renewable supply.

Europe Market Insights

In Europe, the industrial demand response management systems market is poised for extensive growth owing to the region’s strong focus on energy efficiency, decarbonization goals, and increasing penetration of renewable energy sources into the power mix. Industries across major economies such as Germany, France, and the UK are actively adopting demand-side flexibility solutions. In addition, utilities and system operators are collaborating with manufacturing and process industries to integrate automated load control systems that enhance operational efficiency. For instance, in March 2025, ACER submitted its proposal for a new EU‑wide network code on demand response to the European Commission with the main goal of strengthening flexibility in electricity markets. This code ensures that consumers, storage providers, and distributed generation can fully participate, lowering supply costs and supporting renewable integration, hence supporting the market’s expansion.

The need for rapid demand-side flexibility to balance a power grid increasingly reliant on volatile domestic wind and solar assets is boosting Germany industrial demand response management systems market. The country’s market is undergoing a structural shift driven by recent regulatory overhauls from the federal network agency, which is called Bundesnetzagentur. Specifically, the phasing out of traditional grid fee privileges for rigid, constant baseload consumption is actively forcing the country’s manufacturers to adopt automated energy management solutions. Apart from this, to mitigate exceptionally high national electricity tariffs, energy-intensive sectors such as automotive manufacturing, heavy chemical complexes, and steel mills are implementing advanced, cloud-based IDRMS. These plants leverage Internet of Things infrastructure to pool their flexible manufacturing loads, industrial batteries, and on-site storage systems directly into Germany’s secondary balancing reserve markets.

In UK, the industrial demand response management systems market is reaping lucrative growth opportunities from strong regulatory backing for demand-side flexibility. Programs that were introduced and evolved under the UK energy regulator Ofgem and the National Energy System Operator are enabling both industrial and commercial users to actively participate in grid balancing by shifting or adjusting electricity consumption during peak periods. Based on the government data published in December 2025, the country’s Interoperable Demand Side Response Programme, which is a part of the USD 82 million Flexibility Innovation Programme, is funding projects to demonstrate smart, secure, and interoperable demand response solutions. Stream 1 was focused on developing energy‑smart appliances such as heat pumps, EV chargers, and home batteries in compliance with PAS 1878 and PAS 1879 standards, ensuring cybersecurity and seamless interoperability, thus contributing to the market’s expansion.

Key Industrial Demand Response Management Systems Market Players:

- Siemens (Germany)

- Schneider Electric (France)

- ABB (Switzerland)

- Honeywell International (U.S.)

- Johnson Controls (Ireland)

- General Electric Vernova (U.S.)

- Enel X (Italy)

- AutoGrid Systems (U.S.)

- EnergyHub (U.S.)

- CPower Energy Management (U.S.)

- Generac (U.S.)

- CPower (U.S.)

- Fujitsu (Japan)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Siemens is one of the most influential players in the industrial demand response management systems market, which is leveraging its strong presence in industrial automation, grid software, and energy management solutions. Besides, the company deliberately integrates demand response capabilities through its digital grid platforms and smart infrastructure offerings, thereby enabling real-time energy optimization for industrial users and utilities.

- Schneider Electric plays a major role in the DRMS ecosystem, propelled by its energy management and industrial automation solutions. The firm assimilates demand response functionality into its EcoStruxure platform, which in turn enables industries to monitor, control, and optimize energy consumption in real time.

- ABB is also a dominant force in this sector, which offers electrification, automation, and digital energy solutions that support demand response capabilities. The company is highly focused on integrating smart grid technologies with industrial energy systems, with the main goal of improving load balancing and operational efficiency.

- Honeywell International is a foundational player in this sector that provides advanced industrial automation and energy management solutions. In addition, the company’s strategy is structured around digital transformation of industrial operations, cybersecurity for OT systems, and expansion of cloud-based energy platforms, making it a key enabler of intelligent demand-side energy management in industrial environments.

- Johnson Controls is a leading provider of smart building technologies and energy efficiency solutions that support industrial demand response programs. The firm leverages an OpenBlue platform, which enables predictive analytics, AI-driven automation, and real-time energy optimization.

Here is a list of key players operating in the global industrial demand response management systems market:

The industrial demand response management systems market is being dominated by global automation, energy management, and utility software providers. Pioneering companies in this field are highly focused on integrating AI, IoT, and cloud platforms with the main goal of enabling real-time load optimization and grid flexibility. Market participants are opting for acquisitions of niche DRMS software firms, expansion of digital energy platforms, and partnerships with utilities to strengthen demand-side management capabilities. For instance, in June 2026, Voltus announced the acquisition of Brightfield AI to accelerate commercial and industrial energy storage deployment by integrating Brightfield’s battery development platform and veteran team into its virtual power plant operations. This acquisition addresses front‑end friction in customer acquisition and complex site evaluations, thus denoting a positive market outlook.

Corporate Landscape of the Industrial Demand Response Management Systems Market:

Recent Developments

- In April 2026, Generac and CPower entered into a partnership to expand access to distributed energy resource technologies across PJM, North America’s largest electricity market. This collaboration combines Generac’s equipment and dealer network with CPower’s VPP and demand response expertise.

- In February 2026, Fujitsu introduced its AI-based software development platform, which fully automates the software lifecycle from requirements to testing using its Takane LLM and agentic AI technology. This platform will revise all medical and government software packages, cutting modification times from months to mere hours.

- Report ID: 8620

- Published Date: Jun 23, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.