Healthcare Information Software Market Outlook:

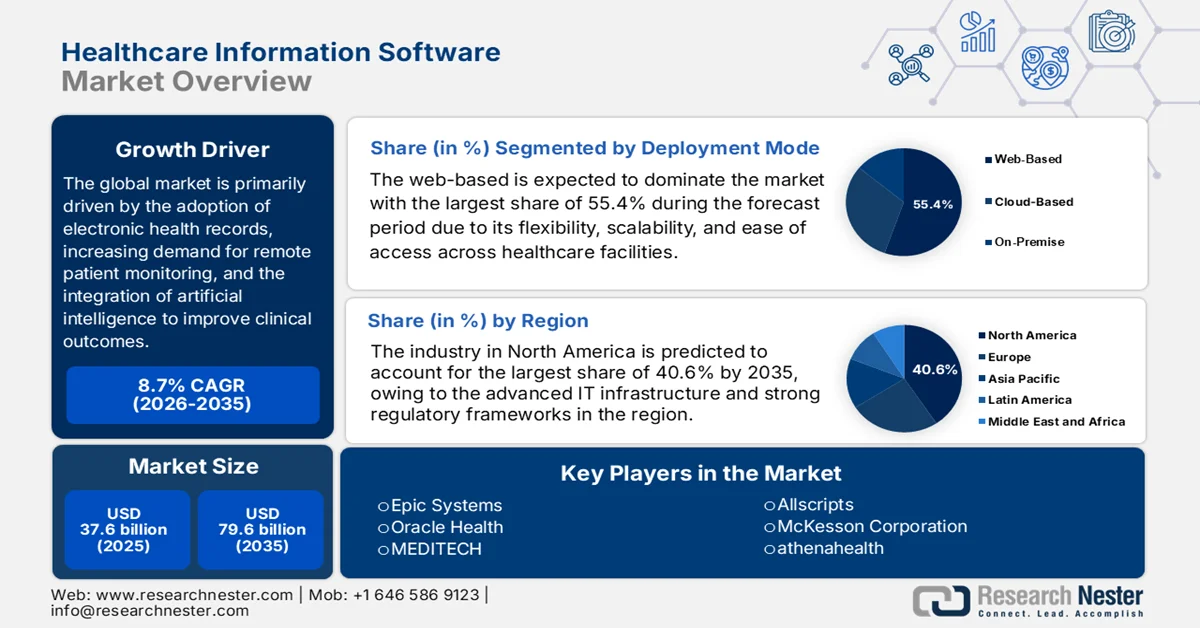

Healthcare Information Software Market size was valued at USD 37.6 billion in 2025 and is projected to grow steadily to USD 79.6 billion by 2035, registering a CAGR of 8.7% during the forecast period, i.e., 2026-2035. In 2026, the industry size of healthcare information software is estimated at USD 40.8 billion.

The global healthcare information software market is undergoing significant transformations owing to the huge need to handle massive volumes of patient data. The industry is making a shift toward hybrid and multicloud strategies with the main goal of enhancing data interoperability. Office of the National Coordinator (ONC) of Health Information Technology in February 2026 stated that the 21st Century Cures Act and its Cures Rule have resulted in increased adoption of standardized FHIR APIs, wherein most of the hospitals are currently enabling patient access to apps of their choice. By 2024, nearly two-thirds of hospitals also supported patient-generated health data submission, which was offered through standards-based APIs, reflecting growing patient demand for digital engagement. At the same time, hospitals are actively exchanging data with third-party technologies for clinical and administrative purposes, though much of this occurs through non-standard APIs or legacy methods. New policies such as the HTI-4 Final Rule aim to reduce dependency on non-standard methods, thereby driving automation and interoperability for prior authorization and strengthening modern health data exchange.

Hospital API Adoption Trends (2022-2024): Patient Access & PGHD

|

Category |

Year |

Standards-Based APIs (%) |

Non-Standards-Based APIs Only (%) |

Total Hospitals Enabling Function (%) |

|

Patient Access |

2022 |

69% |

17% |

86% |

|

Patient Access |

2023 |

70% |

16% |

86% |

|

Patient Access |

2024 |

71% |

16% |

87% |

|

PGHD Submission |

2022 |

45% |

15% |

60% |

|

PGHD Submission |

2023 |

49% |

14% |

62% |

|

PGHD Submission |

2024 |

48% |

16% |

65% |

Source: ONC

Furthermore, the emergence of telehealth and remote patient monitoring is stimulating consistent growth in the healthcare information software market. Moreover, there has been an increased adoption of cloud-native healthcare apps to facilitate personalized care and streamline operations, thus indicating a sustained, long-term shift toward a software ecosystem. As per an article published by Gitnux Organization in February 2026, telehealth adoption has expanded rapidly across healthcare systems owing to the measurable increases in utilization, reimbursement scale, and provider integration. The report also stated that 76% of U.S. consumers used telehealth at least once in 2022. Provider-side adoption is also rising, with 46% of physicians reporting regular telehealth use in 2023 and nearly 96% of hospitals enabling telehealth services post-pandemic. Therefore, these trends indicate that there is a structural normalization of virtual care delivery benefiting the overall healthcare information software industry.

Telehealth Industry Growth Statistics (2019 - 2023): Adoption, Market Size, and Investment Trends

|

Category |

Statistic |

Value |

Year |

|

Consumer adoption |

U.S. consumers using telehealth at least once |

76% |

2022 |

|

Rural adoption |

Rural U.S. telehealth adoption |

37% |

2022 |

|

Hospital adoption |

Hospitals offering telehealth services |

96% |

Post-COVID |

|

Pediatric growth |

Increase in pediatric telehealth usage |

+200% |

2019-2022 |

|

Senior adoption |

Seniors (65+) using telehealth |

55% |

2023 |

|

Workforce coverage |

Employer-sponsored telehealth coverage |

70% |

2023 |

|

Global users |

Active telehealth users globally |

1.2 billion |

2023 |

|

India adoption |

Telehealth users in India |

150 million |

2023 |

|

Market size (global) |

Telehealth market value |

USD 83.5 billion |

2022 |

|

Market projection |

Expected global market size |

USD 559.5 billion |

2030 |

|

Europe growth |

Telehealth market growth |

38% |

2023 |

|

Medicare growth |

Claims increase |

154x since 2019 |

2022 |

|

Cost savings |

Savings per telehealth visit |

USD 50 - USD 100 |

2023 |

|

System savings |

U.S. healthcare savings |

USD 10.5 billion |

2021 |

|

Readmission reduction |

Hospital readmission reduction |

20% |

2021-2023 |

|

Investment funding |

Startup funding in telehealth |

USD 29.1 billion |

Since 2019 |

|

R&D spending |

Global telehealth R&D spend |

USD 5.6 billion |

2023 |

Source: Gitnux

Key Healthcare Information Software Market Insights Summary:

Regional Highlights:

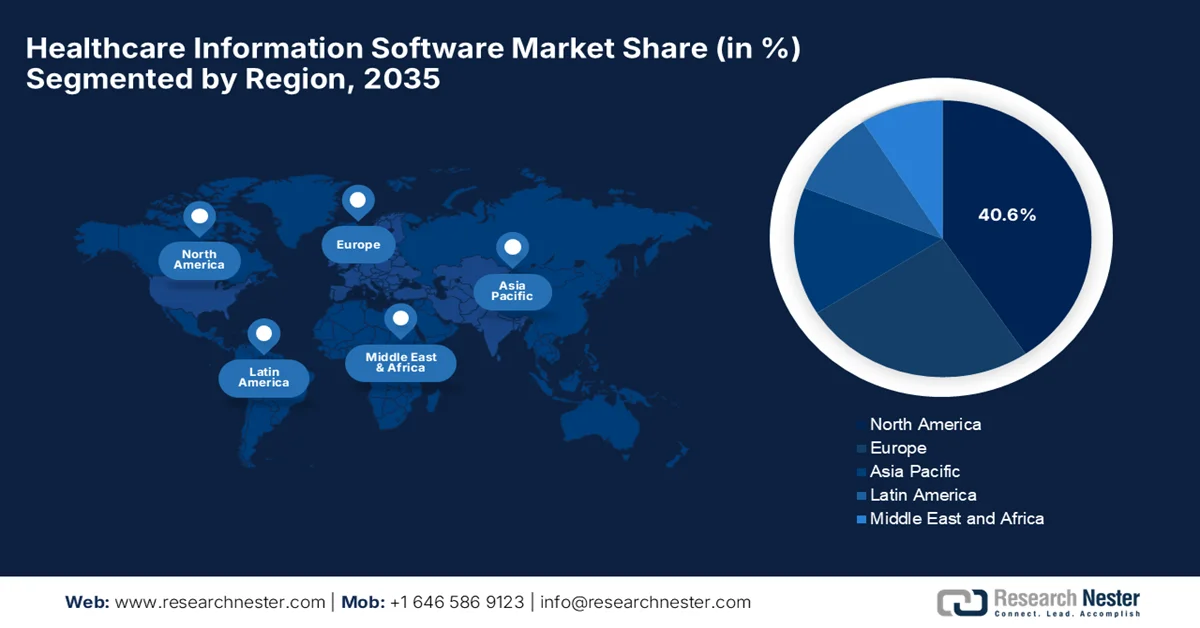

- The North America region is projected to hold a dominant 40.6% share by 2035 in the healthcare information software market, fueled by advanced IT infrastructure, strong regulatory frameworks, and rising AI-based healthcare adoption

- Asia Pacific is anticipated to witness the fastest growth during 2026–2035, stimulated by accelerating digitalization, expanding cloud-based solutions, and increasing demand for advanced patient data management

Segment Insights:

- The web-based deployment segment in the healthcare information software market is projected to account for a leading 55.4% share by 2035, propelled by its flexibility, scalability, and seamless real-time accessibility across healthcare systems

- The subscription-based pricing model segment is expected to expand significantly over 2026–2035, attributed to its predictable cost structure and enhanced scalability for healthcare providers

Key Growth Trends:

- Digital transformation of healthcare systems

- Rising adoption of electronic health records

Major Challenges:

- Data security and privacy concerns

- Lack of skilled workforce

Key Players: Epic Systems (U.S.), Oracle Health / Cerner (U.S.), MEDITECH (U.S.), Allscripts (U.S.), McKesson Corporation (U.S.), athenahealth (U.S.), NextGen Healthcare (U.S.), eClinicalWorks (U.S.), Optum (U.S.), GE HealthCare (UK), Siemens Healthineers (Germany), Philips Healthcare (Netherlands), Dedalus (Italy), InterSystems (U.S.), CompuGroup Medical (Germany).

Global Healthcare Information Software Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 37.6 billion

- 2026 Market Size: USD 40.8 billion

- Projected Market Size: USD 79.6 billion by 2035

- Growth Forecasts: 8.7% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (40.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, United Kingdom, Japan, China

- Emerging Countries: India, South Korea, Singapore, Brazil, United Arab Emirates

Last updated on : 22 April, 2026

Healthcare Information Software Market - Growth Drivers and Challenges

Growth Drivers

- Digital transformation of healthcare systems: Healthcare providers across most of the nations are shifting away from paper-based systems to digital platforms to reap better efficiency and coordination. In this context, healthcare software enables this shift by supporting scalable and integrated IT infrastructure for both hospitals and clinics. As per an article which was published by the National Institute of Health (NIH) in February 2023, digital transformation in healthcare is being positively impacted by technologies such as IoT, cloud computing, AI, wearable devices, and telemedicine, which enhance efficiency in respective categories. In addition, the article also stated that digitalization supports a patient-centric care model by enabling better access to health information, remote monitoring, and personalized treatment options. These innovations are deliberately reshaping the healthcare information software market, improving service quality, and increasing system efficiency through greater acceptance of digital health solutions.

- Rising adoption of electronic health records: The world is facing an incremental use of EHR, EMR, and digital patient records, which is generating massive volumes of healthcare data that require secure, scalable storage and real-time access, making software platforms essential. According to the article published by NIH in June 2023, there are several positive aspects of electronic health record adoption in low-income countries. It states that these EHR systems have the complete potential to improve healthcare quality by enabling better patient data management, supporting data-driven clinical decision-making, and enhancing patient safety. At the same time, they also promote more efficient, timely, and patient-centered care delivery when compared to traditional paper-based systems. Additionally, increasing healthcare providers’ interest in using digital tools is an encouraging factor that supports gradual EHR adoption, thus benefiting the overall healthcare information software market.

- Increasing use of AI, big data, and analytics: Healthcare organizations are using AI-driven diagnostics, predictive analytics, and big data tools, all of which rely heavily on software infrastructure for processing and storage. This factor is prompting a profitable business environment for pioneers in the healthcare information software market. In April 2026, IKS Health introduced MyCareHub, which is a first-of-its-kind agentic AI platform at the AMGA 2026 conference, especially designed to personalize and automate patient engagement across the care journey. The platform is integrated with Epic, and it leverages behavioral modeling, decision intelligence, and adaptive orchestration to improve adherence and reduce costs. Therefore, such constant innovations from the leading pioneers underscore their patient-first approach to care enablement.

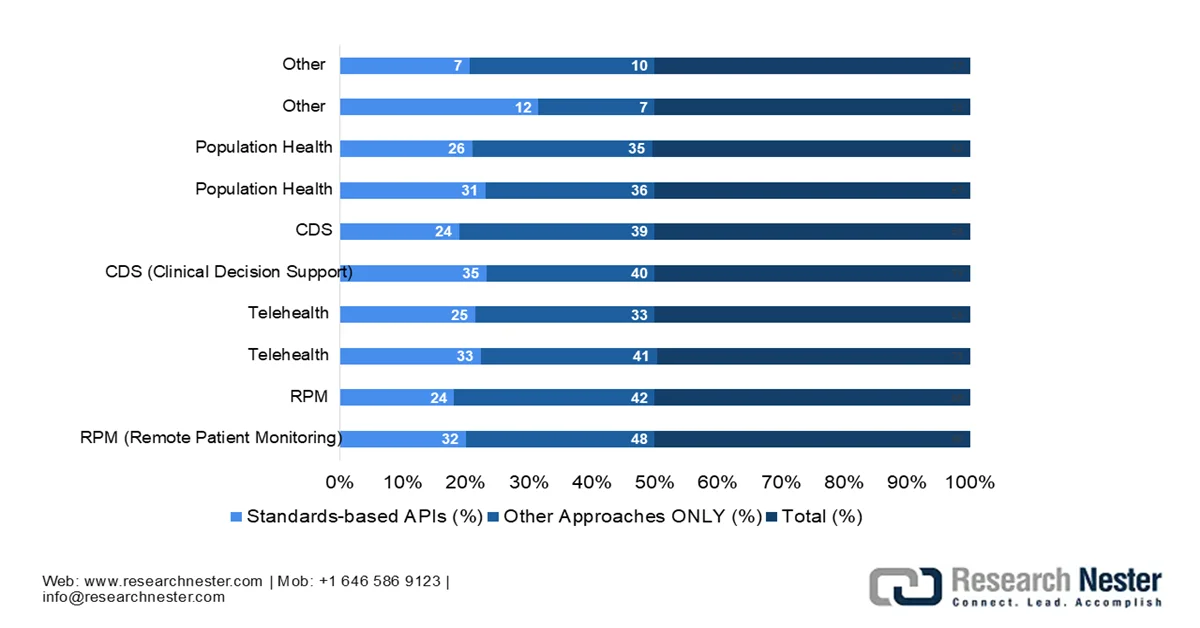

Hospital EHR Data Sharing with Third-Party Technologies (2024): API vs Non-Standard Integration

Source: ONC

Challenges

- Data security and privacy concerns: One of the major burdens in the healthcare information software market is ensuring the security and privacy of sensitive patient data. Healthcare organizations across different nations handle confidential information, which makes it the target for some sort of ransomware and data breaches. Therefore, storing the data on software platforms increases exposure to vulnerabilities, especially if there is no proper encryption, access controls, and monitoring systems. Also, complying with stringent regulations adds huge complexity for pioneers in this field. Any lapse in security can lead to legal penalties, financial losses, and loss of patient trust. Furthermore, as cloud adoption grows, the maintenance of cybersecurity frameworks will be a constant and evolving challenge for healthcare providers.

- Lack of skilled workforce: The aspect of successful implementation and management of cloud computing necessitates a skilled workforce with knowledge in cloud technologies, cybersecurity, and healthcare IT systems. But there is a shortage of professionals with the necessary knowledge and experience in this specialized field. At the same time, training existing staff can be time-consuming as well as expensive, whereas hiring skilled professionals may not always be feasible owing to the existence of budget constraints. In this context, a skills gap can lead to improper system management, increased security risks, and inefficient use of software resources. At the same time, healthcare organizations might find it challenging to fully utilize software capabilities, limiting their ability to innovate and improve patient outcomes, thus negatively impacting the growth of the healthcare information software market.

Healthcare Information Software Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

8.7% |

|

Base Year Market Size (2025) |

USD 37.6 billion |

|

Forecast Year Market Size (2035) |

USD 79.6 billion |

|

Regional Scope |

|

Healthcare Information Software Market Segmentation:

Deployment Mode Segment Analysis

The web-based deployment mode is expected to dominate the healthcare information software market with the largest share of 55.4% during the forecast period. Its flexibility, scalability, and ease of access across healthcare facilities are the main factors driving the sub-segment’s leadership. Also, its ability to support real-time access, reduce operational costs, and integrate smoothly with evolving digital health systems efficiently strengthens its leading position in the healthcare information software market. In April 2026, the U.S. Department of Veterans Affairs resumed and expanded its federal EHR rollout by deploying a cloud-enabled, web-based system across four Michigan hospitals, i.e., VA Ann Arbor, Detroit, Battle Creek, and Saginaw medical centers. This system allows access and sharing of patient records across VA facilities and federal partners, improving care coordination and reducing duplication of tests, thus indicating an optimistic opportunity for the segment’s dominance.

Pricing Model Segment Analysis

In the pricing model segment, the subscription-based category is anticipated to grow at a noteworthy pace from 2026 to 2035 in the healthcare information software market. The segment is growing as healthcare organizations prefer predictable operating expenses over capital-intensive infrastructure. Also, these models offer greater scalability, which in turn allows healthcare providers to easily adjust services based on patient demand and organizational needs. In April 2023, Microsoft and Epic expanded their strategic collaboration to integrate Azure OpenAI Service with Epic’s electronic health record systems, which builds on their existing partnership that already enables Epic environments to run on Microsoft Azure cloud, and this particular initiative is highly focused on embedding generative AI into healthcare workflows to improve productivity, support clinical decision-making, and enhance operational efficiency.

End user Segment Analysis

Under the end user segment, hospitals are anticipated to grow with a significant share in the healthcare information software market during the discussed timeframe. The segment’s growth in this field is largely driven by the increasing need to manage large volumes of clinical, administrative, and financial data within complex care environments. Hospitals across the globe are also under continuous pressure to improve patient outcomes, reduce operational inefficiencies, and ensure regulatory compliance, which encourages greater adoption of integrated digital health systems. At the same time, the rising patient inflow and the expansion of multi-specialty hospital networks are readily accelerating the demand for advanced healthcare information software solutions. At the same time, there has been a growing emphasis on data-driven decision-making and interoperability between different hospital departments, which is solidifying the reliance on these software platforms.

Our in-depth analysis of the healthcare information software market includes the following segments:

|

Segment |

Subsegments |

|

Deployment Mode |

|

|

Pricing Mode |

|

|

End user |

|

|

Service Model |

|

|

Application |

|

|

Organization Size |

|

|

Component |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Healthcare Information Software Market - Regional Analysis

North America Market Insights

The North America healthcare information software market is anticipated to garner the largest share of 40.6% by the conclusion of the forecast period. The region’s dominance is largely propelled by advanced IT infrastructure, strong regulatory frameworks, and high adoption of AI-based healthcare solutions. As per the article published by NIH in October 2024, a study was conducted at the University of Arkansas for Medical Sciences, which highlights a substantial rise in telehealth utilization across multiple specialties after the COVID-19 pandemic, with total telehealth visits increasing by 89% in a span of one year, and it rose to 117,730 in 2021. Around 92.57%, 134,221 of 145,001 telehealth patients were covered by major insurers such as Medicare, Medicaid, and private commercial plans, reflecting expanded insurance reimbursement support. The findings also show improved efficiency metrics, including a reduction in indirect waiting time from 48.4 days to 27.7 days and a decrease in appointment length from 93.2 minutes to 39.59 minutes, thus denoting a huge opportunity for the healthcare information software market to grow in the upcoming years.

The widespread adoption of electronic health records and the imperative for enhanced interoperability are responsibly uplifting the healthcare information software market in the U.S. The country’s market is efficiently driven by increasing digital transformation, the need for advanced analytics, and rising investments in telehealth and revenue cycle management. In July 2025, the White House and Centers for Medicare & Medicaid Services (CMS) announced a national initiative with a main goal to build a patient-centric healthcare ecosystem, which is focused on interoperability, secure data exchange, and integration of EHRs with digital health platforms across the U.S. healthcare system. This particular program involves commitments from more than 60 organizations, including major tech companies, to support CMS-Aligned Networks, FHIR-based APIs, and a national provider directory to enable the sharing of patient data and improve healthcare coordination, thus making it suitable for standard healthcare information software market growth.

In Canada, the healthcare information software market is growing exponentially, owing to the rising adoption of cloud-based solutions to enhance patient care and operational workflows. Key drivers fueling the country’s market are government initiatives aimed at digital transformation, an increasing need for data interoperability, and the integration of AI for improved diagnostic and predictive analytics in clinical settings. In February 2026, the country’s government introduced Bill S-5, the Connected Care for Canadians Act, to modernize health data sharing and eliminate any type of fragmented systems. This particular legislation mandates common digital standards for secure, interoperable exchange of health information, thereby empowering patients with timely access to their own records. Hence, with such continued federal support, the country will witness reduced provider burden and build a more connected healthcare system over the next decade.

APAC Market Insights

The Asia Pacific healthcare information software market is predicted to grow at the quickest rate during the discussed timeframe. The region’s market is mostly propelled by intensifying digitalization efforts, the proliferation of cloud-based solutions, and rising demand for advanced patient data management. The healthcare information software market is making a shift toward predictive analytics, automated workflows, and remote patient monitoring to manage chronic diseases and address the needs of an aging population. In January 2025, the Singapore Ministry of Health confirmed that the next-generation electronic medical record rollout had already been completed at NUHS and NHG, wherein the SingHealth is scheduled between 2026 and 2028. The government will invest almost USD 1.5 billion over 10 years to implement NGEMR across the public healthcare sector. This particular strategic system will replace more than 100 legacy IT systems, thereby improving efficiency and reducing costs, thus indicating a positive market outlook.

The government initiatives, which aim to modernize the medical infrastructure and encourage web-based hospital management, are prompting a favorable business environment for pioneers operating in the healthcare information software market in China. Key trends reshaping the country’s market include the accelerated integration of AI and machine learning for diagnostics and precision medicine, along with growing cloud-based solutions. Based on the government data published in July 2024, the country announced its plans to strengthen IT use in public hospitals by establishing integrated management platforms in all tertiary hospitals by the end of 2027. This particular initiative emphasizes digitizing internal processes, improving interoperability, and leveraging AI, big data, and cloud computing with the main goal of boosting efficiency and quality. Therefore, such instances underscore a shift toward a digital, AI-enabled healthcare system that is driving increased adoption of healthcare information software market in hospitals.

In India, the healthcare information software market has gained enhanced exposure owing to the urgent need for enhanced hospital management and improved patient care. Stakeholders in the country are focusing on data security, scalability, and enhanced, real-time connectivity. At the same time, government-led digital initiatives are accelerating this growth, supporting a digital health ecosystem that includes mHealth and wearable technology. As stated by Press Information Bureau (PIB) in February 2026, India’s healthcare system is extensively adopting AI-based healthcare information software through initiatives such as the IndiaAI Mission and Ayushman Bharat Digital Mission, which support large-scale digital health infrastructure, electronic health records, and interoperable hospital systems. These programs have enabled more than 282 million telemedicine consultations through e-Sanjeevani and expanded AI use in diagnostics, disease surveillance, and screening programs such as TB detection and retinal imaging, thus suitable for bolstering the healthcare information software market’s growth.

Europe Market Insights

Europe healthcare information software market is expected to retain its position as the second largest stakeholder in the global dynamics by the end of 2035. The region’s growth is largely propelled by mandatory electronic health record adoption and the widespread implementation of cloud computing and AI-enabled analytics. Key areas of growth visible in the regional market are population health management, revenue cycle management, and personal health records. As stated by Open Access Government in December 2025, the EU4Health programme is driving digital health forward with new projects that are focused on AI, cross-border data exchange, and stronger national infrastructures. Besides the initiative called COMPASS-AI, which is piloting safe and effective AI use in cancer care and remote regions, it is expanding the MyHealth@EU platform to enable secure access to medical records, ePrescriptions, and lab results across borders, hence contributing to a wider market expansion.

The government initiatives that are promoting reimbursement for digital solutions and boosting the digital health sector, trade, and investment are responsibly driving the healthcare information software market in Germany. The country’s focus on patient-centric care, digital therapeutics, and connected care ecosystems is encouraging healthcare providers to adopt software solutions that readily enhance clinical workflows and support long-term healthcare innovation. At the same time, the country’s policy push, especially through the Digital Healthcare Act, has created a structured reimbursement pathway for digital solutions, thereby accelerating adoption across the healthcare system. The introduction of the DiGA directory ensures that approved digital therapeutics meet regulatory, safety, and clinical benefit standards, fostering trust among providers and patients. In addition, investments in terms of interoperable infrastructure and electronic health records are strengthening data integration and enabling more efficient, evidence-based decision-making.

The healthcare information software market in the UK maintains a strong position in the regional landscape, highly propelled by the integration of artificial intelligence for predictive analytics and enhanced interoperability between care settings. The country’s landscape is characterized by a combination of major global vendors and emerging innovators, with a strong emphasis on cybersecurity and improving clinical efficiency. In March 2026, the article, published by the Health Foundation, reports that digital health policy in the UK is strongly supported, especially for efficiency-driven services. At the same time, about 76% of the public supports using the NHS App for booking hospital appointments, and 73% support functions such as choosing hospitals or accessing treatment information. It also mentioned that support is higher among NHS staff, with 80% backing AI use in patient care when compared to 54% of the public.

Key Healthcare Information Software Market Players:

- Epic Systems (U.S.)

- Oracle Health / Cerner (U.S.)

- MEDITECH (U.S.)

- Allscripts (U.S.)

- McKesson Corporation (U.S.)

- athenahealth (U.S.)

- NextGen Healthcare (U.S.)

- eClinicalWorks (U.S.)

- Optum (U.S.)

- GE HealthCare (UK)

- Siemens Healthineers (Germany)

- Philips Healthcare (Netherlands)

- Dedalus (Italy)

- InterSystems (U.S.)

- CompuGroup Medical (Germany)

- Oracle Health (U.S.)

- Florence Healthcare (U.S.)

- HealthEdge (U.S.)

- Ellipsis Health (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Epic Systems is identified as the global leader in this field, which is best known for its widely adopted EHR platform. The company is well recognized for its highly integrated ecosystem that connects patient records, clinical workflows, and analytics.

- Oracle Health is also one of the largest competitors in the global healthcare information software market following its acquisition of Cerner. The firm provides large-scale health information systems for hospitals, governments, and defense healthcare systems.

- MEDITECH is a long-established healthcare IT provider which is offering cost-effective EHR solutions, and it is especially popular among mid-sized hospitals and community healthcare providers. In addition, the company’s platforms emphasize usability, affordability, and integrated clinical and administrative functions.

- Philips Healthcare is a major global player that is combining medical devices with advanced health information software, especially in terms of imaging informatics, patient monitoring, and population health management. The firm’s software solutions are extensively used in critical care environments and integrated hospital systems.

- Siemens Healthineers leads in terms of digital health platforms, imaging software, and AI-powered diagnostic solutions. The company integrates software with advanced medical imaging systems, thereby enabling hospitals to improve diagnostic accuracy and operational efficiency.

Below is the list of some prominent players operating in the global healthcare information software market:

The healthcare information software market is extremely competitive, which is dominated by global technology giants along with specialized healthcare IT firms. Leading pioneers leverage advanced AI, big data analytics, and scalable cloud infrastructure with the main goal of strengthening their market positions. Companies across the globe are proactively pursuing mergers, acquisitions, and strategic partnerships with a prime focus on expanding geographic presence and enhancing service portfolios. At the same time, continuous investments in R&D and the launch of suitable solutions such as HIPAA-compliant platforms and AI-driven diagnostics are key strategies. For instance, in April 2026, HealthEdge entered into a partnership with Ellipsis Health to integrate Sage, which is an AI-powered virtual nursing voice agent, into its Care Solutions platform, enabling scalable, empathetic member outreach across care management programs.

Corporate Landscape of the Healthcare Information Software Market:

Recent Developments

- In March 2026, MEDITECH introduced new native ambient intelligence solutions for physicians and nurses, seamlessly integrated into Expanse workflows to reduce documentation burden and enhance patient interactions. Complementing these innovations are AI-powered tools like Claim Denial Agents, MyHealth Assistant, and Ask Expanse, all designed to improve care delivery.

- In February 2026, Oracle Health expanded its Clinical AI Agent with automated order creation, enabling clinicians to draft accurate prescriptions, lab tests, imaging studies, and follow-up appointments through ambient listening. This advancement reduces administrative burden and saves doctors over 200,000 hours of documentation time.

- In November 2025, Oracle Health stated that its next-generation AI-powered EHR has earned ONC certification and DEA compliance. It is built natively with AI on a secure cloud architecture, the system streamlines workflows, and reduces administrative burden.

- In October 2025, Florence Healthcare announced that SiteLink, its clinical trial operations platform, is now available on AWS Marketplace, extending digital capabilities to sponsors and research sites worldwide.

- Report ID: 8526

- Published Date: Apr 22, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.