Oncology Information System Market Outlook:

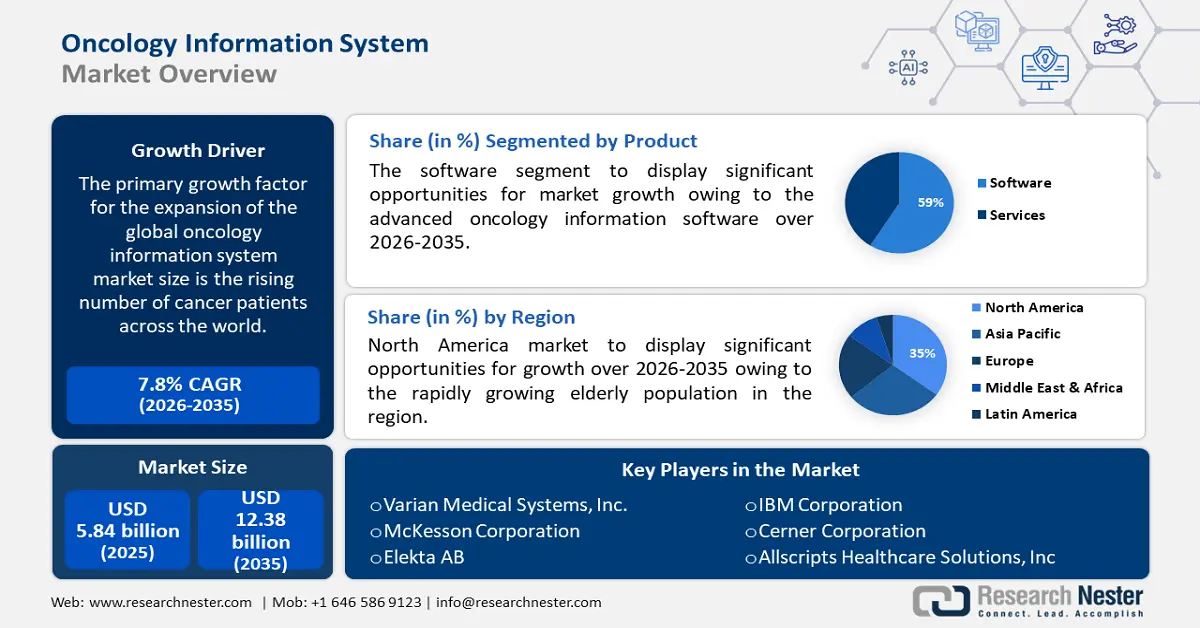

Oncology Information System Market size was over USD 5.84 billion in 2025 and is poised to exceed USD 12.38 billion by 2035, growing at over 7.8% CAGR during the forecast period i.e., between 2026-2035. In the year 2026, the industry size of oncology information system is estimated at USD 6.25 billion.

The primary growth factor for the expansion of the global oncology information system market size is the rising number of cancer patients across the world. Oncology information system aids treatment outcomes, treatment plans, and tracking of cancer patient information across healthcare organizations which is supposed to improve the safety and efficacy of the treatment of cancer patients. Therefore, the rising number of cancer patients across the world is anticipated to bring in lucrative growth opportunities for market growth during the forecast period. As per the statistics shared by the World Health Organization (WHO), it is revealed that cancer is considered to be one of the major causes of death occurring worldwide. Also, cancer was responsible for taking almost 10 million lives in 2020 around the globe.

Apart from the aforementioned factors, the rising awareness level about the advantages of oncology information systems such as a comprehensive information and image solution and an effective way to manage and optimize the profiles of cancer patients and their treatment is anticipated to create a positive outlook for market growth during the forecast period. Furthermore, the availability of a plethora of treatment patterns in healthcare facilities which requires proper documentation, maintenance of patient treatment patterns, and the rising need for the conservation of electronic health records (EHR) or electronic medical record (EMR) along with the requirement of treatment prediction is also expected to positively contribute in the expansion of market size in the upcoming years. In addition, the escalation in initiatives taken by the government to boost the usage of advanced medical devices, digital health, and hospital management system is estimated to boost the adoption rate of oncology information systems in hospitals and clinics.

Key Oncology Information System Market Insights Summary:

Regional Highlights:

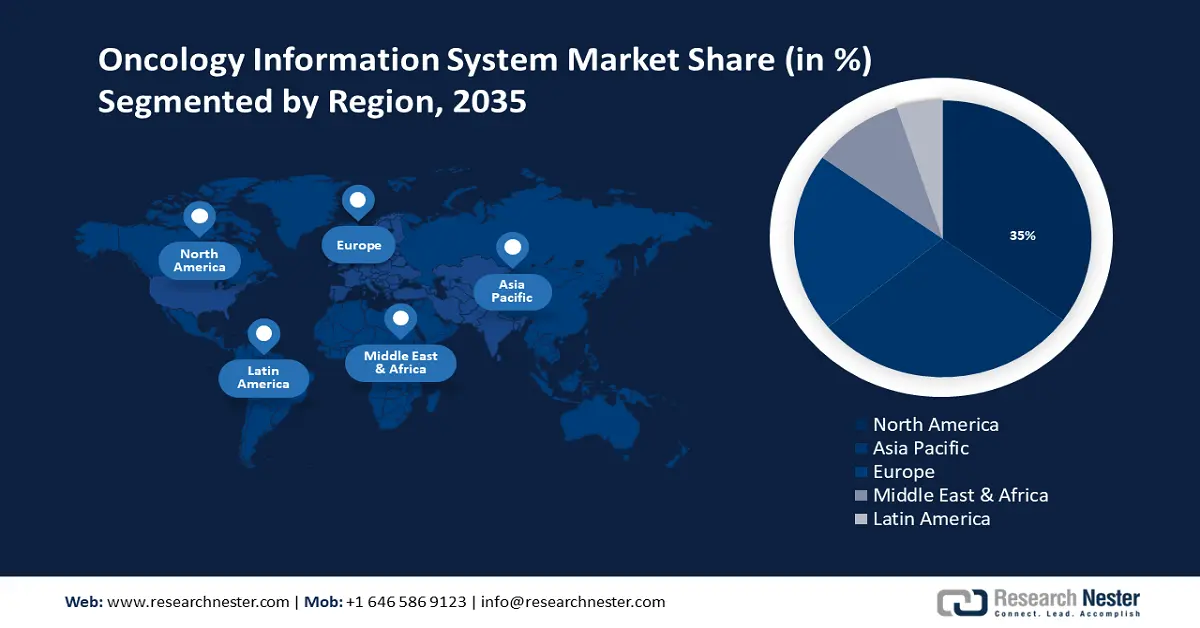

- North America oncology information system market is poised to capture 35% share by 2035, attributed to advanced healthcare infrastructure and growing elderly population.

- Asia Pacific market will achieve a 29% share by 2035, driven by rising cancer incidence and adoption of hospital information systems.

Segment Insights:

- The software segment in the oncology information system market is anticipated to hold a 59% share by 2035, driven by the adoption of advanced digital health platforms to streamline oncology workflows.

- The hospital segment in the oncology information system market is anticipated to hold a 37% share by 2035, attributed to the high influx of patients requiring data management in hospitals.

Key Growth Trends:

- Rising Prevalence of Tumors among Global Population

- Increasing Health Spending

Major Challenges:

- Expensiveness of Oncology Information Systems

- Lack of Awareness about the Advantages of Oncology Information System

Key Players: Koninklijke Philips N.V., Varian Medical Systems, Inc., McKesson Corporation, Elekta AB, Epic Systems Corporation, IBM Corporation, Cerner Corporation, Allscripts Healthcare Solutions, Inc., MICA Information Systems, Inc., EndoSoft LLC.

Global Oncology Information System Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 5.84 billion

- 2026 Market Size: USD 6.25 billion

- Projected Market Size: USD 12.38 billion by 2035

- Growth Forecasts: 7.8% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (35% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Germany, Japan, United Kingdom

- Emerging Countries: China, India, Brazil, Mexico, South Korea

Last updated on : 9 September, 2025

Oncology Information System Market Growth Drivers and Challenges:

Growth Drivers

-

Rising Prevalence of Tumors among Global Population – People around the world are being diagnosed with both types of tumors i.e. benign tumors which are not cancerous and do not spread and malignant tumors which are cancerous and spread or invade into nearby tissues. As the oncology information system helps aid physicians and surgeons to choose the most appropriate treatment process to increase the survival rate of patients and enhance the patient’s experience, the demand for oncology information is expected to increase for efficient treatment of tumors. The data shared by the American Society of Clinical Oncology stated by the end of 2023, almost 18,990 deaths out of which 11,020 men and 7,970 women are estimated to occur in the United States owing to cancerous brain and CNS tumors. Also, as per the American Cancer Society, approximately 24,810 individuals (14,280 males and 10,530 women) are about to be diagnosed with malignant tumors of the brain or spinal cord by the end of 2023.

-

Increasing Health Spending – As cancer cases and other illnesses are spreading over the world are spreading rapidly, people are spending more money on health and treatment for an effective cure and enhanced experience. This has led to an increased utilization rate of oncology information systems in various healthcare settings. According to the most recent expenditure data, global health spending has grown over the past 20 years, doubling in real terms to reach USD 8.5 trillion in 2019 and 9.8% of GDP, up from 8.5 percent in 2000. It is predicted that this boom would continue over the forecast period.

-

Rising Focus for Bringing Advancement in the Healthcare Industry – With the rising cases of cancers and other illnesses, the need for efficient systems for managing patient and treatment information effectively. This factor is anticipated to create favorable opportunities for the adoption of oncology information systems in hospitals, thereby, helping in the expansion of the market size. For instance, it has been calculated that the investment made by the government of the United States in the medical and health research and development (R&D) sector increased by 11% to reach approximately USD 245 billion in 2020 from previous years.

-

Rising Focus on Using Hospital Information Systems – Governments of different nations are focusing on adopting Electronic Health Records (EHR) and other advanced systems and technologies that could help in maintaining medical records, patient treatment processes, and other information. Thus, it is helping doctors to opt for an oncology information system which in turn is projected to drive market growth in the forecast period. Around 97% of doctors electronically recorded BDOH data in 2021, while 85% of doctors electronically recorded SDOH data. Compared to other medical professionals, primary care physicians electronically collected SDOH and BDOH data at a higher rate.

-

Favorable Government Initiatives for Digital Health – The National Digital Health Mission (NDHM) was launched by the Ministry of Health and Family Welfare of the Government of India in August 2020 with the goal of offering essential assistance for the integration of digital health infrastructure throughout the nation.

Challenges

- Expensiveness of Oncology Information Systems – Oncology information systems are technologically advanced with the integration of the latest features that is beneficial for healthcare. As a result, the costs of this technology subsequently increase the costs of the treatment and medical procedure. This factor is anticipated to lower the adoption rate of oncology information systems among the population with middle and low-income and ultimately hamper market growth during the forecast period.

- Lack of Awareness about the Advantages of Oncology Information System

- Unavailability of Skilled Workforce for Efficient Use of Oncology Information System

Oncology Information System Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

CAGR |

7.8% |

|

Base Year Market Size (2025) |

USD 5.84 billion |

|

Forecast Year Market Size (2035) |

USD 12.38 billion |

|

Regional Scope |

|

Oncology Information System Market Segmentation:

Product Segment Analysis

The software segment is estimated to gain the largest market share of about 59% in the year 2035. In the recent period, advanced oncology information software has been recognized as a practical and affordable way to quicken the pace of digital innovation, by enhancing the management of information related to patients, treatments, and medical procedures. Also, the software helps in promoting productivity, increasing revenue, improving care quality and enhancing the experience of both the patient and healthcare professional. For instance, in March 2022, GE Healthcare announced the launch of the Edison Digital Health Platform, which is advanced software that is created to provide holistic views of each patient and support integrated care pathway management by gathering information from numerous sources and vendors to enhance clinical applications.

End-user Segment Analysis

The hospital segment is expected to garner a significant share of around 37% in the year 2035. The major factor attributed to the segment growth is the rising pool of patients visiting the hospital daily which require a highly efficient program such as an oncology information system for the maintenance of a large amount of patient data. As per the data released by the Centers for Disease Control and Prevention (CDC), it was estimated that around 131.1 million hospital visits occurred in 2022. Also, the availability of various advanced technologies, increasing government investments and skilled workforce for the smooth functioning of an oncology information system are other factors that are estimated to positively contribute to segment growth. In addition to other factors, the rising number of hospitals across the globe and the availability of features and facilities for the proper conduction of treatment and procedures is anticipated to increase the utilization rate of oncology information systems in hospitals. For instance, there were over 8,000 hospitals in Japan as of 2020. Korea, by contrast, had about 4,000 hospitals.

Our in-depth analysis of the global market includes the following segments:

|

By Product |

|

|

By Software |

|

|

By Application |

|

|

By End User |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Oncology Information System Market Regional Analysis:

North American Market Insights

North America region is likely to hold more than 35% market share by 2035. The growth of the market can be attributed majorly to the availability of advanced healthcare infrastructure, and the rapidly growing elderly population in the region. As per the Rural Health Information Hub, as of June 2019, 46 million adults aged 65 years and above were living in the United States. By 2050, the number is calculated to reach a value of almost 90 million. In addition, escalating research and development activities for developing patient-centric oncology information systems are also predicted to aid the region’s market growth. Moreover, the presence of a strong healthcare facility in the North American region coupled with the availability of major key players is also estimated to positively contribute towards market growth in the next few years.

APAC Market Insights

Asia Pacific region is estimated to capture over 29% oncology information system market share by 2035. The primary reason for market growth in the region is the escalation in the occurrence of cancer and tumors among the population which needs proper treatment and efficient management of documentation and information. The National Library of Medicine stated that the occurrence of cancer in Asia Pacific was calculated to be 169.1 per 1,00,000, which is equivalent to almost 49.3% of the global cancer incidence in 2020. The most common cancer was lung (13.8%), followed by breast (10.8%), and colorectal (10.6) respectively. Apart from the other factors, the rising favorable initiatives to promote digital health and proper hospital information system is also anticipated to impetus robust revenue generation in the region.

Europe Market Insights

Further, European region is estimated to hold significant revenue share by 2035. The continuous technological advancement is promoting the usage of electronic medical records to use health information and manage big amounts of data related to patients is considered to be the major factor for the market expansion in the region. In addition, the increased healthcare expenditure owing to the surge of disposable income along with the rising focus to modernize healthcare infrastructure is projected to bring favorable opportunities for market growth.

Oncology Information System Market Players:

- Koninklijke Philips N.V.

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Varian Medical Systems, Inc.

- McKesson Corporation

- Elekta AB

- Epic Systems Corporation

- IBM Corporation

- Cerner Corporation

- Allscripts Healthcare Solutions, Inc.

- MICA Information Systems, Inc.

- EndoSoft LLC

Recent Developments

-

Koninklijke Philips N.V. and Elekta AB signed an agreement aimed at strengthening their existing partnership to advance personalized cancer care via precision oncology solutions.

-

McKesson Corporation has launched Ontada, which is an oncology technology and insights business designed for supporting innovation, and effective evidence generation to generate better outcomes for patients with cancer.

- Report ID: 3671

- Published Date: Sep 09, 2025

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

Oncology Information System Market Report Scope

Free Sample includes current and historical market size, growth trends, regional charts & tables, company profiles, segment-wise forecasts, and more.

Connect with our Expert

Copyright @ 2026 Research Nester. All Rights Reserved.