Healthcare Distribution Market Outlook:

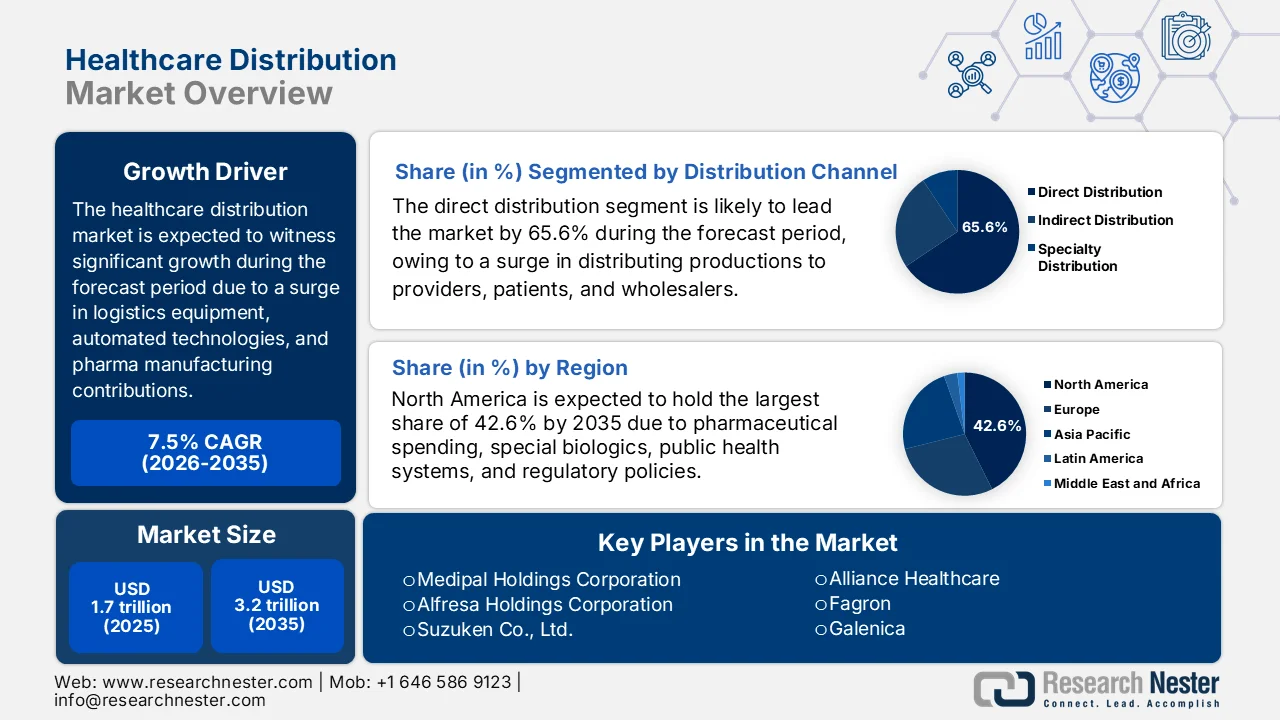

Healthcare Distribution Market size was valued at over USD 1.7 trillion in 2025 and is projected to reach USD 3.2 trillion by the end of 2035, growing at a CAGR of 7.5% during the forecast period, i.e., 2026-2035. In 2026, the industry size of healthcare distribution is assessed at USD 1.8 trillion.

The global healthcare distribution market is continuously gaining increased exposure, owing to factors, including tariff policies on imported logistics equipment, warehouse automation technologies, cold storage systems, an escalation in pharmaceutical organizations expanding manufacturing and active pharmaceutical ingredient (API) supply bases, and heightened regulatory enforcement. According to official statistics published by the Bulk Drug Manufacturers Association of India in October 2025, 72% of API manufacturers serve the U.S. industry. Likewise, Taiwan experienced the highest growth in the latest manufacturing infrastructures globally, with a 326% surge, along with 189 new sites. This is followed by India with a 254% growth and 3,676 facilities, and China achieving a 55% upliftment and an additional 531 manufacturing sites, thus fueling the market expansion.

Global API Manufacturing Facilities, 2024

Source: Bulk Drug Manufacturers Association of India

Furthermore, the artificial intelligence (AI) integration as a core operational facility, a rise in AI-based contract research organizations (CRO) for reshaping clinical supply chains, and the presence of hybrid supply chain models for balancing local and worldwide diversification are a few trends that are responsible for boosting the healthcare distribution market. As stated in an article published by NLM in November 2025, the global CRO industry was valued at USD 16.5 billion in 2007, which later increased by 14% to 16% and reached USD 24 billion in 2010. In addition, the industry experienced expansion by USD 39.7 billion as of 2021, followed by USD 45.5 billion in 2022, and is further projected to surge by USD 115 billion by the end of 2030. This future upliftment demonstrates a 12% growth rate, which denotes an optimistic outlook for the overall market development.

Key Healthcare Distribution Market Insights Summary:

Regional Highlights:

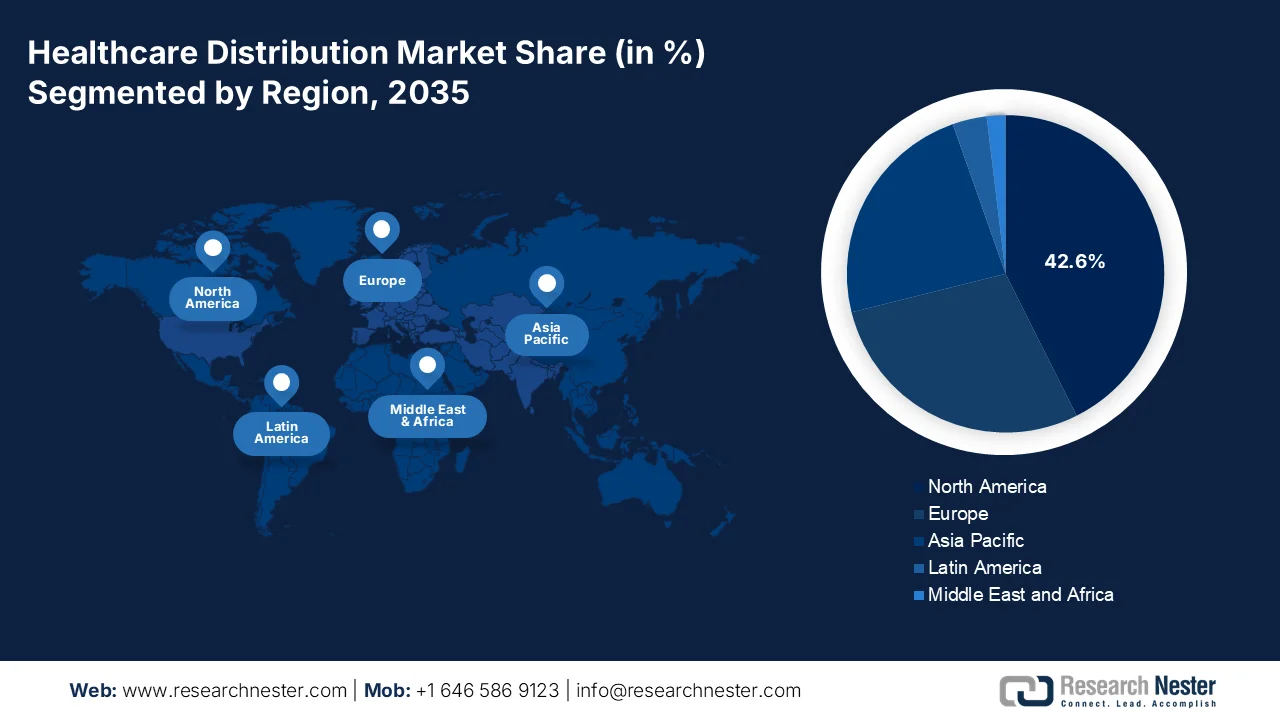

- By 2035, North America in the healthcare distribution market is expected to dominate with a 42.6% share, impelled by high pharmaceutical spending, oligopolistic wholesale networks, and increasing specialty biologics demand

- During 2026–2035, Asia Pacific is projected to be the fastest-growing region, fueled by expanding aging populations, rising pharmaceutical consumption, and rapid localization of biopharmaceutical manufacturing

Segment Insights:

- By 2035, the direct distribution segment in the healthcare distribution market is projected to command a 65.6% share, propelled by its ability to streamline supply chains, enhance patient safety, and reduce costs through direct manufacturer-to-end-user delivery

- During the forecast period 2026–2035, the hospital pharmacies sub-segment is expected to secure the second-highest share, driven by its critical role in managing high-acuity, high-volume medication distribution within acute care settings

Key Growth Trends:

- The patient cliff fueling merger and acquisition

- Expansion in senior care requirements

Major Challenges:

- Fragmented cold chain integrity across last-mile networks

- Margin compression amidst rising service expectations

Key Players: McKesson Corporation, Cencora, Inc., Cardinal Health, Inc., AmerisourceBergen Corporation, Owens & Minor, Inc., Henry Schein, Inc., Medline Industries, LP, Patterson Companies, Inc., PHOENIX Group, Alliance Healthcare, Fagron, Galenica, Amplifon SpA, Sinopharm Group, Shanghai Pharmaceuticals Holding Co., Ltd., Medipal Holdings Corporation, Alfresa Holdings Corporation, Suzuken Co., Ltd., Sigma Healthcare Limited, EBOS Group Limited, Hanmi Pharmaceutical, DHL Group, Cryoport, Cardinal Health, Johnson & Johnson, Novartis.

Global Healthcare Distribution Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 1.7 trillion

- 2026 Market Size: USD 1.8 trillion

- Projected Market Size: USD 3.2 trillion by 2035

- Growth Forecasts: 7.5% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, Germany, Japan, China, France

- Emerging Countries: India, South Korea, Brazil, Mexico, Saudi Arabia

Last updated on : 24 April, 2026

Healthcare Distribution Market - Growth Drivers and Challenges

Growth Drivers

- The patient cliff fueling merger and acquisition: The biopharma patient cliff and merger and acquisitions indicate one of the most structural and significant forces for reshaping the healthcare distribution market globally. For instance, in April 2025, Johnson & Johnson acquired Intra-Cellular Therapies, Inc., and added CAPLYTA® to its strong portfolio of specialty medicines. Besides, in October 2025, Novartis entered into a tactical agreement and acquired Avidity Biosciences, Inc. to boost its commitment to delivering advanced, targeted, and potentially first-in-class medicines to aid progressive and devastating neuromuscular disorders. Therefore, with the presence of such organization mergers and acquisitions, there is a huge growth opportunity for the healthcare distribution market across different regions.

- Expansion in senior care requirements: The aspect of the aging population is gradually enhancing the demand for long-lasting care, specialized geriatric, and assistive living services, and evolving the healthcare distribution market. As stated in an article published by the World Health Organization (WHO) in October 2025, 1 in 6 people in the world is poised to be aged over 60 years by the end of 2030. Likewise, this particular age category is expected to double to 2.1 billion by the end of 2050. Simultaneously, the number of people aged over 80 years is also predicted to triple by the same year and reach 426 million. Therefore, based on this, health and medical systems are eventually expanding and redesigning senior care services, which in turn, is enhancing the healthcare distribution market exposure.

- Increase of value-specific care services: The ongoing expansion of value-driven care programs is unprecedentedly pressuring healthcare distributors in demonstrating outcomes and efficiencies. As per an article published by the World Economic Forum in October 2024, a generous investment of USD 1.3 trillion in social employment, such as the care economy, resulted in a USD 3.1 trillion gross domestic product (GDP) return, along with the development of over 10 million employment opportunities, especially in the U.S. Besides, healthcare providers are demanding just-in-time delivery of medical supplies and suitable equipment to diminish inventory. Moreover, the rise in telehealth services is further proliferating the healthcare distribution market demand, which positively impacts care services globally.

Challenges

- Fragmented cold chain integrity across last-mile networks: The single greatest operational challenge in the healthcare distribution market is maintaining uninterrupted temperature-controlled environments, commonly known as the cold chain, since biologic products move from regional hubs to final delivery points, such as clinics, hospitals, and increasingly, patient homes. While primary and secondary logistics providers have largely mastered warehousing and long-haul transport, the last-mile segment remains the weakest link. Independent couriers, rural delivery routes, and direct-to-patient shippers often lack the specialized infrastructure, real-time monitoring equipment, and trained personnel required to handle sensitive gene therapies and vaccines. This fragmentation creates thermal excursions wherein products stray outside mandated temperature ranges.

- Margin compression amidst rising service expectations: The aspect of wholesale drug distribution has historically operated on exceptionally thin unit economics, but the current environment has intensified the squeeze to unsustainable levels for many mid-tier players. Besides, large-sized pharmaceutical manufacturers and consolidated retail pharmacy chains possess significant bargaining power, routinely pushing distributors to accept lower per-unit fees while demanding more value-added services, including kitting, repackaging, inventory financing, and data analytics. Simultaneously, the shift toward specialty pharmaceuticals requires distributors to invest heavily in cold chain infrastructure, pharmacist-staffed customer support centers, and patient adherence programs, thus restricting the healthcare distribution market growth.

Healthcare Distribution Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.5% |

|

Base Year Market Size (2025) |

USD 1.7 trillion |

|

Forecast Year Market Size (2035) |

USD 3.2 trillion |

|

Regional Scope |

|

Healthcare Distribution Market Segmentation:

Distribution Channel Segment Analysis

Based on the distribution channel, the direct distribution segment is anticipated to garner the highest share of 65.6% in the healthcare distribution market by the end of 2035. The segment’s upliftment is highly driven by its pivotal role to permit manufacturers to distribute products directly to patients, pharmacies, and provides, along with bypassing conventional wholesalers. Additionally, this is essential for optimizing supply chain speed, enhancing patient safety, and diminishing expenses. According to a data report published by OECD in February 2024, the worldwide trade of the pharmaceutical industry increased by 10-fold over the past 30 years, reaching USD 900 billion as of 2022. Besides, in the past 30 years, trade facilities in medical devices also surged by 7-fold in valuation and reached an overall USD 700 billion in the same year, thus positively impacting the segment’s growth.

End user Segment Analysis

The hospital pharmacies sub-segment, which is part of the end user segment, is projected to account for the second-highest share in the healthcare distribution market during the forecast period. The sub-segment’s growth is highly fueled by its functionality as high-volume, high-acuity distribution centers embedded within acute care environments. They are responsible for managing formularies that span nearly every therapeutic category, from routine antibiotics to controlled substances, emergency crash cart medications, and expensive biologic therapies requiring strict temperature control. The operational challenge lies in the just-in-time balancing act: maintaining sufficient inventory to prevent life-threatening stock-outs during trauma cases or intensive care surges, while avoiding overstock that leads to waste, especially for short-dated or temperature-sensitive products.

Product Type Segment Analysis

By the end of the stipulated timeline, the pharmaceutical product sub-segment, part of the product type segment, is expected to grab the third-highest share in the healthcare distribution market. The sub-segment’s development is highly attributed to its importance for modernized healthcare, to treat, diagnose, and prevent diseases. As per an article published by NLM in March 2024, the active pharmaceutical ingredients industry increased to USD 193.1 billion as of 2023, which is further projected to surge to USD 285.2 billion by the end of 2028. In this regard, localized medical production is effectively encouraged, particularly across developing nations, to enable suitable accessibility to pharmaceutical products at a low expense in comparison to products imported from developed economies. Besides, the local production is efficient and cheap, thus proliferating the sub-segment’s development globally.

Global Pharmaceutical Products Export and Import Analysis, 2024

|

Countries/Components |

Export (USD) |

Import (USD) |

|

Germany |

117 billion |

71.6 billion |

|

U.S. |

96.1 billion |

177 billion |

|

Switzerland |

91.2 billion |

66.5 billion |

|

Global Trade Valuation |

869 billion |

|

|

Global Trade Share |

3.8% |

|

|

Product Complexity |

0.8 |

|

|

Export Growth |

3.86% |

|

Source: OEC

Our in-depth analysis of the healthcare distribution market includes the following segments:

|

Segment |

Subsegments |

|

Distribution Channel |

|

|

End user |

|

|

Product Type |

|

|

Technology/Platform |

|

|

Service Type |

|

|

Form |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Healthcare Distribution Market - Regional Analysis

North America Market Insights

North America in the healthcare distribution market is anticipated to grab the largest share of 42.6% by the end of 2035. The market’s upliftment in the region is primarily attributed to the oligopolistic wholesale structure, pharmaceutical expenditure per capita, sustained immense distribution, an increase in specialty biologics, regulatory compliance, and the presence of a unified public health system. According to official statistics published by NLM in April 2022, the total pharmaceutical spending in the U.S. increased by 7.7% and is valued at USD 576.9 billion. This denotes a 4.8% increase in utilization, 1.9% in price, and 1.1% in the latest drugs that fueled the overall surge. Besides, drug spending was worth USD 39.6 billion, demonstrating 8.4% increases, followed by USD 105 billion, which is 7.7% increase across non-federal hospitals and clinics, thus bolstering the healthcare distribution market growth in the region.

The healthcare distribution market in the U.S. is growing significantly, owing to an upsurge in specialty pharmaceuticals, regulatory compliance for technological modernization, automation in distribution centers, the existence of direct-to-patient delivery models, and an increase in prescription drugs. As stated in an article published by NLM in May 2024, in terms of payers’ pricing, discounts and rebates in Medicare Part D doubled from USD 167 to USD 370, indicating a yearly average increase of almost 10% annually. This particular prominence-based rise in specialty drugs resulted in aiding complicated conditions and further required special handling. Besides, branded specialty drugs in the country significantly accounted for 17% of net expenditure in Medicare Part D, which further increased by 54%, thus positively driving the healthcare distribution market demand.

Medicare Part B Drugs Payer’s Pricing, 2026

|

Drug Name |

Dosage |

Pricing (USD) |

|

Verteporfin injection |

0.1 mg |

11.5 |

|

Vyjuvek 5x10^9pfu/ml, 0.1 ml |

0.1 ml |

1,004.5 |

|

Hydroxyzine hcl injection |

25 mg |

15.1 |

|

Thiamine hcl 100 mg |

100 mg |

1.5 |

|

Vitamin b12 injection |

1000 mcg |

0.6 |

|

Hydroxocobalamin im 10mcg |

10 mcg |

0.007 |

|

Vitamin k phytonadione inj |

1 mg |

3.1 |

|

Injection, voriconazole |

10 mg |

0.6 |

|

Hyaluronidase injection |

150 units |

31.5 |

|

Hyaluronidase recombinant |

1 USP unit |

0.3 |

Source: CMS Government

The increased focus on public sector financing, demographic pressures, provincial procurement consolidation, medical distribution roles, a surge in hospital spending, and comprehensive health occupations are certain factors that are uplifting the healthcare distribution market in Canada. As per an article published by OECD in November 2025, the total population is significantly covered by a set of health services, with 50% satisfaction with the healthcare quality. Besides, in terms of financial coverage, 70% of the overall expenditure in the country is covered by compulsory repayment. Meanwhile, 9.1% of the population indicated unmet demands, which is deliberately enhancing the market growth in the nation. Besides, the country has prescribed 11 defined regular antibiotic doses per 1,000 population. Meanwhile, the country spends USD 7,301 per capita on health, which is equivalent to 11.3% of the GDP, thereby fueling the healthcare distribution market growth.

APAC Market Insights

The Asia Pacific in the healthcare distribution market is expected to emerge as the fastest-growing region during the forecast period. The market’s development is highly propelled by an expansion in the economic, aging demographics, the rapid localization of biopharmaceutical manufacturing, an increase in high-volume pharmaceutical consumption, and a rise in rare disease prevalence. According to a data report published by the APACMED Organization in August 2022, 10% to 20% of hospitals in Japan have readily implemented telehealth systems. Besides, the Tokutei kenshin system was established in the country to offer yearly check-ups for adults aged between 40 and 74 years. Moreover, in terms of chronic diseases, out of more than 290 million people with both type 1 and type 2 diabetes in the region, 50% remain undiagnosed and are also prone to long-lasting complications, which ensures the market development.

The healthcare distribution market in China is gaining increased traction, owing to a transition from a fragmented network to an efficient and consolidated system, an increase in mergers between small-sized distributors and large-scale giants, an upsurge in prescription volume, and the demand for tech-enabled and modern distribution channels. As stated in an article published by NLM in September 2025, the chronic disease prevalence has effectively reached 34.3%, with hypertension as one of the major issues, impacting an estimated 245 million individuals. Besides, a clinical study was conducted on 164,857 patients with hypertension, wherein 103,475 patients were registered. This comprised 53.6% of females with 85.5% of Urban Employees Basic Medical Insurance coverage. Therefore, with this disease prevalence and patient registration, there is a huge growth opportunity for the healthcare distribution market.

The aspects of organizational contributions, cost-effective generic drug distribution, increased focus on ultra-cold chain logistics for supporting the booming biotech export sector, generous investments in centralized logistics, and digital tracking strategies are a few trends that are developing the healthcare distribution market in India. As per an article published by NLM in September 2023, the country’s population of 1.3 billion is effectively spread across 3.2 million square kilometers. Besides, the domestic Universal Immunization Programme readily targets 27 million newborns as well as 30 million pregnant women every year. This has resulted in the demand for over 150 million. Therefore, spanning this diversification is the nation’s cold chain network, denoting the ultimate backbone of the overall immunization program, which is ensuring the market expansion.

Europe Market Insights

Europe in the healthcare distribution market is projected to experience considerable growth by the end of the stipulated timeline. The market’s growth in the region is highly driven by pharmaceutical supply chain resilience, regulatory harmonization, an escalation in the demand for specialty biologics, a strong hospital procurement facility, and centralized distribution networks. According to official statistics published by NLM in August 2025, the payers’ pricing of biopharmaceuticals in the region usually ranges from USD 11,696.4 to USD 35,091.6 per patient every year, along with other treatment expenses amounting to USD 584,860. Besides, the most critical healthcare in the region is catered to cancer, with medical expenditure projected to reach USD 409 billion by the end of 2028, which is responsible for driving the market expansion.

The healthcare distribution market in Germany is gaining increased exposure, owing to the presence of a wholesale infrastructure, an increase in the pharmaceutical consumption volume, statutory health insurance, a surge in prescription drug distribution, and the focus on cold chain networks. As stated in an article published by NLM in November 2024, the Drug Prescription Report has analyzed the 3,000 most frequently suggested drugs in the country. In addition, of these, the top 10 essential medicines readily account for nearly 42% of overall defined daily doses as of 2022. Besides, 47,592.3 million defined daily doses (DDD) of these 10 medicines were prescribed in the domestic economy as of 2022. Likewise, at 19,522.1 million DDD, these medicines catered to 41.9% of overall prescriptions, thereby making it suitable for fueling the market growth.

Top 10 Prescribed Drugs Share Analysis in Germany, 2022

|

Medicines |

DDD |

% Share |

|

Ramipril |

4,794.7 |

10.7% |

|

Candesartan |

3,064.9 |

6.4% |

|

Pantoprazole |

2,940.1 |

6.1% |

|

Amlodipine |

1,890.2 |

3.9% |

|

Atorvastatin |

1,782.3 |

3.7% |

|

Levothyroxine |

1,458.9 |

3.0% |

|

Torasemide |

1,023.2 |

2.1% |

|

Simbastatin |

912.3 |

1.9% |

|

Bisoprolol |

853.5 |

1.7% |

|

Metoprolol |

801.0 |

1.6% |

Source: NLM

The presence of a centralized health insurance model, generous government investment for distribution facilities, digitalized health infrastructure, real-time and temperature-based monitoring of biologic drugs, modernizing blood product distribution, and the aging population are certain factors that are driving the healthcare distribution market in France. As per an article published by NLM in October 2025, a clinical study was conducted on 12 gastroenterology and rheumatology prescribers, along with 14 patients, to determine biologics consumption. This study led to 71% of patients, which is 10 out of 14, readily accepting the switch to a particular biosimilar in the country. Additionally, 7 out of 14 patients accepted due to the trust in the physician-patient relationship. Moreover, 89% of prescribers recommended biosimilars, demonstrating a switch from reference biologics, which is positively impacting the market exposure.

Key Healthcare Distribution Market Players:

- McKesson Corporation (U.S.)

- Cencora, Inc. (U.S.)

- Cardinal Health, Inc. (U.S.)

- AmerisourceBergen Corporation (U.S.)

- Owens & Minor, Inc. (U.S.)

- Henry Schein, Inc. (U.S.)

- Medline Industries, LP (U.S.)

- Patterson Companies, Inc. (U.S.)

- PHOENIX Group (Germany)

- Alliance Healthcare (UK)

- Fagron (Belgium)

- Galenica (Switzerland)

- Amplifon SpA (Italy)

- Sinopharm Group (China)

- Shanghai Pharmaceuticals Holding Co., Ltd. (China)

- Medipal Holdings Corporation (Japan)

- Alfresa Holdings Corporation (Japan)

- Suzuken Co., Ltd. (Japan)

- Sigma Healthcare Limited (Australia)

- EBOS Group Limited (Australia)

- Hanmi Pharmaceutical (South Korea)

- DHL Group (Germany)

- Cryoport (U.S.)

- Cardinal Health (U.S.)

- Johnson & Johnson (U.S.)

- Novartis (Switzerland)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- McKesson Corporation functions as a foundational pillar of the U.S. healthcare supply chain, distributing pharmaceuticals, medical supplies, and biopharmaceutical products to a vast network of hospitals, pharmacies, and oncology clinics. The company has strategically pivoted toward specialty pharmaceuticals and biopharma services, investing heavily in cold chain logistics and community oncology platforms to capture higher-margin distribution opportunities.

- Cencora, Inc. has repositioned itself as a global leader in pharmaceutical sourcing and specialty distribution, with a pronounced focus on animal health and global commercialization services. The company differentiates itself through deep manufacturer partnerships and a robust direct-to-patient delivery infrastructure, enabling it to serve complex therapeutic areas, including rare diseases and gene therapies.

- Cardinal Health, Inc. operates as a dual-focused healthcare giant, distributing pharmaceuticals alongside a substantial portfolio of medical and surgical products to hospitals and ambulatory care centers. The company has been actively transforming its distribution network through automation, data analytics, and nuclear pharmacy services, allowing it to handle highly regulated radioactive compounds alongside conventional drugs.

- AmerisourceBergen Corporation historically carved a niche as the partner of choice for independent community pharmacies and specialty drug manufacturers requiring white-glove logistics. The company built extensive capabilities in global pharmaceutical sourcing, manufacturer consulting, and hub services that connect patients to high-cost specialty medications through integrated distribution platforms.

- Owens & Minor, Inc. distinguishes itself by focusing heavily on the acute care hospital segment, distributing medical and surgical supplies rather than mainstream pharmaceuticals. The company has evolved into a healthcare logistics provider that offers inventory management outsourcing, clinician preference card analytics, and procedure-based supply chain solutions to help health systems reduce operating room waste and supply variation.

Here is a list of key players operating in the global healthcare distribution market:

The healthcare distribution market remains highly consolidated in North America, with McKesson, Cencora, and Cardinal Health commanding the largest shares globally. These industry leaders are aggressively pivoting toward specialty pharmaceuticals, cold chain expansion, and oncology services to offset margin compression in traditional drug distribution. Key strategic initiatives include portfolio optimization, such as McKesson’s planned IPO of its medical business, and vertical integration into biopharma services and prescription technology platforms. Besides, in February 2025, Hanmi Pharmaceutical unveiled the latest automated vial dispensing solution in the U.S. and Canada. This launch resulted in market expansion and effectively strengthened the collaboration with Mc, Kesson, the distribution partner, thereby making it suitable for fueling the healthcare distribution industry globally.

Corporate Landscape of the Market:

Recent Developments

- In November 2025, Cencora invested USD 1 billion through 2030 for expanding and bolstering its pharmaceutical distribution network in the U.S., along with launching a second domestic distribution facility in Ohio and an extended presence in California and Alabama.

- In March 2025, DHL Group acquired 100% of Cryoport, Inc.’s CRYOPDP, which is a notable specialty courier service that is highly focused on cell and gene therapies, as well as biopharma and clinical trials. Based on this acquisition, both organizations formed a strategic partnership to strengthen their supply chain offerings for the worldwide healthcare and life sciences industry.

- In January 2025, Cardinal Health launched the Advanced Therapy Connect, which is a first-to-market unified ordering portal for cell and gene therapies, through its very own Advanced Therapy Solutions business.

- Report ID: 8532

- Published Date: Apr 24, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.