Healthcare Cloud Computing Market Outlook:

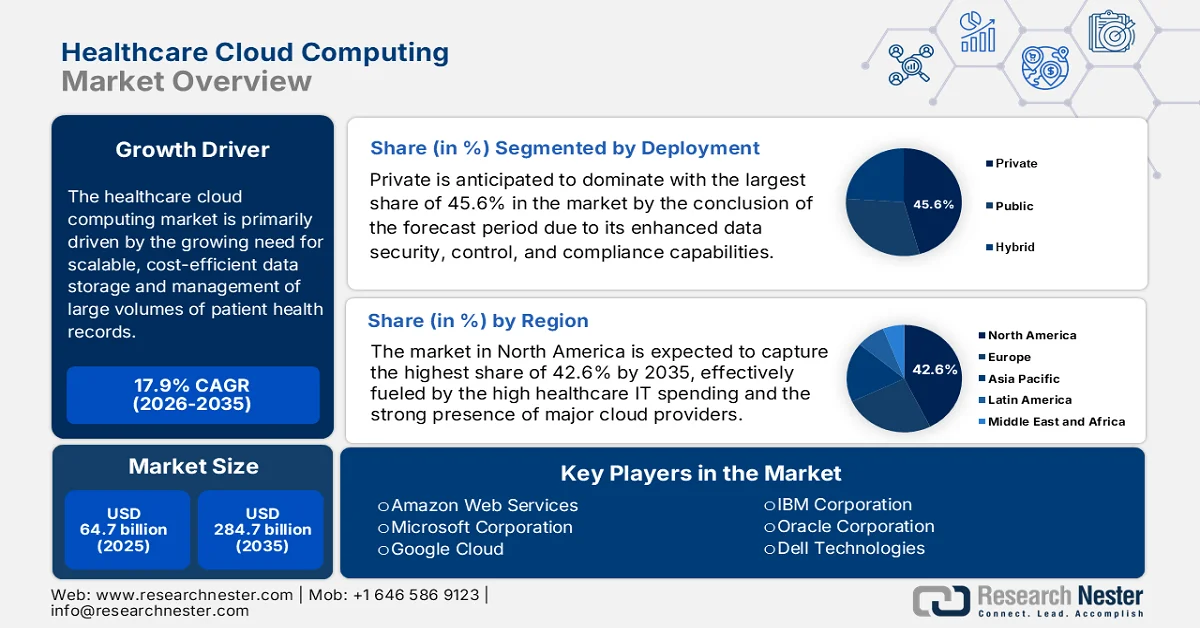

Healthcare Cloud Computing Market size was valued at USD 64.7 billion in 2025 and is anticipated to expand to USD 284.7 billion by 2035, registering a CAGR of 17.9% during the forecast period from 2026 to 2035. In 2026, the industry size of healthcare cloud computing is assessed at USD 76.2 billion.

The healthcare cloud computing market is poised for huge growth in the upcoming years as healthcare providers, payers, and life sciences organizations shift toward digital-first operations. Also, these cloud platforms are enabling better data integration across most of the fragmented healthcare systems, improving care coordination for clinical as well as operational decision-making. As per an article published by the National Institute of Health (NIH) in April 2024, cloud computing is transforming healthcare by providing scalable, on-demand infrastructure for managing large clinical and biomedical datasets. The report states that cloud computing improves data integration across fragmented systems such as electronic health records, telemedicine platforms, and personalized care applications. The study also shows that cloud platforms support real-time access and sharing of medical data, enhancing clinical coordination and decision-making, thus denoting an encouraging opportunity for the healthcare cloud computing market to grow exponentially.

Furthermore, the growing adoption of electronic health records, healthcare modernization efforts, and AI-based diagnostics is driving the need for scalable, flexible, and secure cloud infrastructure, thereby benefiting the overall healthcare cloud computing market. In this context, the Centers for Disease Control and Prevention (CDC) in April 2024 stated that its public health data strategy emphasizes that modernizing data systems is highly essential for seamless integration between healthcare organizations and public health authorities to enable rapid threat detection and response. In 2023, more than 36,000 healthcare facilities were enabled for electronic case reporting, which is up from 25,000+ in early 2023, and 90% of CDC labs electronically shared data with partners to accelerate reporting and outbreak response. It also notes that 78% of U.S. hospital emergency departments provided near real-time data within 24 hours, thereby strengthening early detection and coordinated public health decision-making across the system.

Key Healthcare Cloud Computing Market Insights Summary:

Regional Highlights:

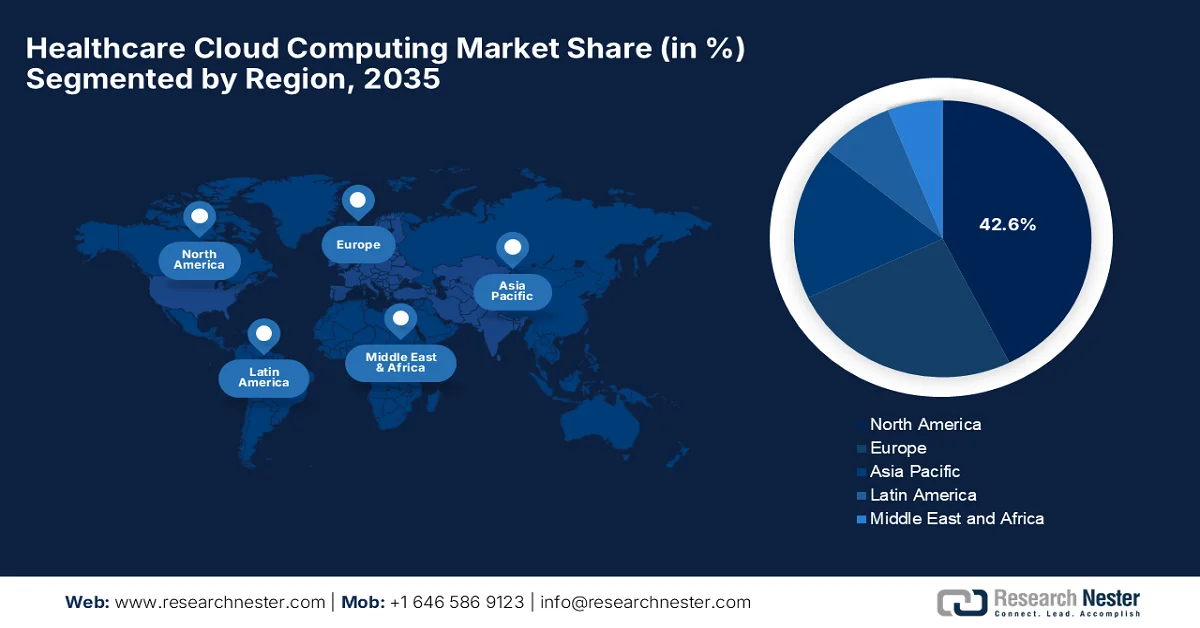

- North America healthcare cloud computing market is projected to hold a dominant 42.6% share by 2035, fueled by widespread adoption of AI-enabled healthcare cloud platforms, high healthcare IT spending, and strong presence of major cloud providers

- Asia Pacific is expected to witness the fastest growth during 2026-2035, stimulated by increasing adoption of digital health technologies such as telemedicine platforms, electronic health records, and healthcare analytics

Segment Insights:

- Healthcare cloud computing market private deployment segment is forecast to account for 45.6% share by 2035, attributed to enhanced data security, control, and compliance capabilities

- Non-clinical information systems segment is anticipated to secure a notable share by 2035, supported by rising demand for administrative efficiency and streamlined operations

Key Growth Trends:

- Explosion of healthcare data

- Rising adoption of telemedicine & remote monitoring

Major Challenges:

- Cloud vendor lock-in and limited portability

- High cost of cloud migration and modernization

Key Players: Amazon Web Services (U.S.), Microsoft Corporation (U.S.), Google Cloud (U.S.), IBM Corporation (U.S.), Oracle Corporation (U.S.), Dell Technologies (U.S.), Salesforce (U.S.), Cleveland Clinic (U.S.), G42 (UAE), CVS Health (U.S.), athenahealth (U.S.), GE HealthCare (U.S.), Cisco Systems (U.S.), Siemens Healthineers (Germany), Koninklijke Philips N.V. (Netherlands), SAP SE (Germany), Fujifilm Holdings Corporation (Japan), NTT DATA Corporation (Japan), NEC Corporation (Japan), INFINITT Healthcare Co., Ltd. (South Korea), Samsung SDS (South Korea), Telstra Health (Australia), Wipro Limited (India).

Global Healthcare Cloud Computing Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 64.7 billion

- 2026 Market Size: USD 76.2 billion

- Projected Market Size: USD 284.7 billion by 2035

- Growth Forecasts: 17.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: North America (42.6% Share by 2035)

- Fastest Growing Region: Asia Pacific

- Dominating Countries: United States, China, Japan, Germany, United Kingdom

- Emerging Countries: India, South Korea, Brazil, Mexico, Indonesia

Last updated on : 22 April, 2026

Healthcare Cloud Computing Market - Growth Drivers and Challenges

Growth Drivers

- Explosion of healthcare data: The large volume of healthcare data, i.e., EHRs, medical imaging, and wearable device data, is growing exponentially. In this context, cloud offers scalable storage and processing power, and it deliberately supports faster and more accurate clinical decisions, thus benefiting the overall healthcare cloud computing market. In November 2025, the article published by the Organization for Economic Co-operation and Development stated that there has been a rapid expansion of digital health owing to the increasing adoption of technologies such as EHRs, telemedicine, and AI. It also mentioned that in 2024, the average availability of online digital health services across OECD countries surpassed a remarkable 82%, which is up from 79% in 2023, reflecting growing data accessibility and infrastructure. Overall, expanding health information systems and interoperability efforts are increasing the volume and use of healthcare data.

- Rising adoption of telemedicine & remote monitoring: The heightened demand for telehealth and remote consultations is a major driver responsible for uplifting the healthcare cloud computing market globally. Increased use of mobile health apps, wearable devices, and cloud enables immaculate data sharing between patients and providers. In this context, an NIH article published in July 2024 evaluated the impact of remote patient monitoring during transitions from hospital to home care by analyzing 29 studies across 16 countries. It found that RPM interventions such as wearables, smartphone apps, and web portals generally improve patient safety, treatment adherence, and functional outcomes such as mobility. The review also mentioned that there has been a reduction in healthcare utilization, including fewer hospital readmissions, shorter stays, and lower overall costs, which is suitable for bolstering market growth globally.

- Rapid digital transformation in healthcare: Healthcare systems across the globe are undergoing large-scale digitalization, which is identified as an important growth driver for the healthcare cloud computing market. Besides, hospitals and providers are opting for cloud platforms to improve patient care, operational efficiency, and decision-making. As per the article published by the NIH in February 2023, technologies such as IoT, AI, and e-health systems are reshaping healthcare delivery as well as patient engagement. Using a systematic review of 287 selected articles from an initial 5,847, the study identified five key themes: information technology in health, e-health education, technology acceptance, telemedicine, and security. In this context, this particular study found that digital transformation improves efficiency, reduces costs, and promotes patient-centered care through better data use and accessibility, thus denoting an optimistic healthcare cloud computing market opportunity.

Challenges

- Cloud vendor lock-in and limited portability: Healthcare organizations mostly face strong dependency on specific cloud providers due to proprietary services, data formats, and analytics tools. If large volumes of clinical data and AI models are deployed on a single platform, the aspect of migration to another provider becomes somewhat technically complex and financially challenging. Also, any type of differences in terms of APIs, storage architectures, and machine learning frameworks reduce portability across clouds. Therefore, the existence of this vendor lock-in limits bargaining power and flexibility in cost optimization in the healthcare cloud computing market. It also creates strategic risk if a provider changes pricing models or discontinues services. Multi-cloud strategies attempt to address this issue, but they in turn lead to additional operational overhead, interoperability complexity, and governance challenges negatively impacting the market’s growth.

- High cost of cloud migration and modernization: Shifting healthcare systems to cloud infrastructure requires substantial investments in terms of migration planning, system redesign, and staff training. Most of the medical providers operate on limited budgets, which makes large-scale modernization financially challenging. Expenses include data transfer, system downtime mitigation, API redevelopment, and cybersecurity hardening. In addition, maintaining parallel legacy and cloud systems during transition periods also increases operational expenditure. Smaller hospitals and clinics face huge and disproportionate financial pressure when compared to large hospital networks. Organizational evidence states that cloud computing offers long-term cost efficiency, but the short-term capital expenditure barrier delays adoption in the healthcare cloud computing market.

Healthcare Cloud Computing Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

17.9% |

|

Base Year Market Size (2025) |

USD 64.7 billion |

|

Forecast Year Market Size (2035) |

USD 284.7 billion |

|

Regional Scope |

|

Healthcare Cloud Computing Market Segmentation:

Deployment Segment Analysis

In the deployment segment, private is anticipated to dominate with the largest share of 45.6% in the healthcare cloud computing market by the conclusion of the forecast period. The dominance of the segment is largely attributable to its enhanced data security, control, and compliance capabilities. In this context, healthcare organizations prefer private cloud environments to manage sensitive patient information, thereby meeting strict regulatory requirements and ensuring data privacy. In February 2026, the Press Information Bureau (PIB) stated that the deployment of AI-based healthcare systems integrated with telemedicine and national digital health platforms. These initiatives, such as the eSanjeevani telemedicine platform, have enabled more than 282 million consultations, reflecting large-scale handling of sensitive patient data within controlled digital environments. In addition, the government also enforces strict frameworks such as ICMR ethical guidelines and federated data platforms to ensure secure, privacy-focused data management, reflecting the preference for highly controlled cloud infrastructures in healthcare.

Application Segment Analysis

Under the application segment, non-clinical information systems are expected to capture a significant share in the healthcare cloud computing market by the conclusion of the forecast period. The segment’s growth is effectively driven by the growing need for administrative efficiency and streamlined operations. Systems such as billing, revenue cycle management, and hospital administration are mostly dependent on cloud platforms to reduce costs and improve workflow management. In March 2026, Epic reported that its AI tools are already transforming healthcare clinicians using Art save time on documentation and catches diseases such as lung cancer earlier, whereas Penny reduces denials and speeds up prior authorizations, improving revenue cycle efficiency. Patients benefit from Emmie, which simplifies scheduling, billing questions, and care plan follow-ups, with high satisfaction rates, thus denoting a wider segment scope.

End user Segment Analysis

By end user healthcare providers segment is predicted to grow with a considerable revenue share in the healthcare cloud computing market over the forecasted years. Hospitals, clinics, and care centers rapidly adopt cloud technologies to enhance patient care, improve data accessibility, and support clinical and administrative functions. In December 2025, Oracle Corporation announced that leading healthcare providers such as billings clinic logan health, Children’s Hospital Los Angeles, and Regency Integrated Health Services adopted Oracle Fusion Cloud Applications to modernize and unify their core hospital operations. The company notes that these organizations moved key functions such as finance, HR, supply chain, and customer service to the cloud to improve efficiency, reduce costs, and streamline administrative workflows across facilities. This reflects the adoption rates among healthcare providers leveraging cloud platforms to enhance both patient care delivery and large-scale operational and administrative management.

Our in-depth analysis of the healthcare cloud computing market includes the following segments:

|

Segment |

Subsegments |

|

Deployment |

|

|

Application |

|

|

End user |

|

|

Service Model |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Healthcare Cloud Computing Market - Regional Analysis

North America Market Insights

The North America healthcare cloud computing market is anticipated to lead with the largest share of 42.6% by the conclusion of the forecast period. The region’s leadership is mainly propelled by widespread adoption of AI-enabled healthcare cloud platforms, high healthcare IT spending, and the strong presence of major cloud providers. In this region, healthcare providers actively encourage patients to use online portals, resulting in higher adoption rates among patients who are regularly guided to access these platforms. The U.S. Department of Health and Human Services in March 2026 announced restructuring of its health IT leadership with a main aim to strengthen enterprise-level cloud, data, and AI systems across the healthcare ecosystem. It mentions that this reorganization places some crucial functions, such as enterprise data governance, AI integration, and cloud infrastructure, under a unified chief information office in order to improve interoperability, data liquidity, and system efficiency across healthcare operations.

The rising adoption of digital health technologies and AI is the main factor behind the growth of the healthcare cloud computing market in the U.S. Besides, the country’s healthcare system is among the most advanced in terms of digital infrastructure, making it a major hub for healthcare IT investments. Strong government support readily accelerates growth, which promotes the adoption of electronic health records and encourages cloud-based integration across healthcare systems. In this context, PBS Organization in July 2025 reported that the White House announced a new private health data tracking system, especially designed to improve patient access to medical records and enable better health monitoring across systems and technologies. The system is maintained by the Centers for Medicare & Medicaid Services, integrates health data from major tech companies and healthcare providers such as Apple, Google, Amazon, and hospital networks, allowing patients to opt in and securely share their records.

In Canada, the healthcare cloud computing market is growing continuously as the healthcare insurance landscape is gradually evolving with increasing adoption of modern telehealth services, which helps reduce pressure on the healthcare system. In addition, Canada’s ageing population is expected to significantly drive demand for mobile health services, as older adults are more prone to chronic conditions. Based on government data published in February 2026, Canada has introduced Bill S-5, which is the Connected Care for Canadians Act, to modernize health data sharing and eliminate fragmented systems such as fax-based records. This legislation mandates common digital standards for IT providers, ensuring secure, interoperable exchange of patient information across clinics, hospitals, and labs. This particular act enables timely, protected access to health data, and it aims to improve patient safety, reduce provider burden, and lay the groundwork for AI-based innovation in healthcare, thus denoting an encouraging opportunity for the healthcare cloud computing market to grow.

APAC Market Insights

The Asia Pacific healthcare cloud computing market is predicted to grow at the fastest rate from 2026 to 2035. The region’s prominence in this field is mainly driven by the increasing adoption of digital health technologies such as telemedicine platforms, electronic health records, and healthcare analytics. Major countries in the region, such as China, India, South Korea, and Japan, are proactively integrating cloud computing into their expanding healthcare infrastructure, thus encouraging more players to establish their footprint in the region. In March 2022, SEADS Organization reported that the COVID-19 pandemic accelerated cloud adoption in the region’s medical sector, and it enabled rapid innovation in telemedicine, digital health, and medical research. The article also mentioned three priorities for governments, i.e., establish clear cloud data governance, adopt cloud-first policies for healthcare, and invest in workforce cloud skills training, hence making it suitable for standard healthcare cloud computing market growth.

The noteworthy government investment in AI-driven diagnostics and the urgent need to upgrade hospital infrastructure are the major driving factors for the healthcare cloud computing market in China. The landscape is dominated by the adoption of electronic health records and cloud-based medical imaging for early disease detection. Based on the government data, published in July 2024, the country is continuously expanding its computing power infrastructure with a main goal to support AI and digital innovation, wherein healthcare is emerging as a key beneficiary. It states that massive data centers and intelligent computing systems are enabling advanced medical research, AI-driven diagnostics, and real-time health applications, whereas green energy integration ensures sustainability. In addition, the country mainly aims to enhance healthcare efficiency, improve patient outcomes, and accelerate the adoption of intelligent health technologies nationwide.

India healthcare cloud computing market is solidifying its presence in the regional landscape, facilitated by the presence of government-led digitalization initiatives and the critical need for on-demand data management and enhanced patient care. The country’s market also benefits from the integration of cloud-based AI, electronic health records, and advanced analytics. Exemplifying this, in January 2025, PIB reported that government initiatives such as the Ayushman Bharat Digital Mission, e-Sanjeevani telemedicine platform, and U-WIN vaccination portal, together enable large-scale digital health record creation and remote healthcare delivery. It also stated that these systems are improving data-driven care by integrating electronic health records, teleconsultations, AI-enabled diagnostics, and interoperable digital infrastructure across the country, denoting a huge opportunity for healthcare cloud computing.

Europe Market Insights

Europe healthcare cloud computing market is expected to experience considerable growth during the discussed timeframe. The region’s prominence in this sector is largely driven by the growing need to modernize legacy hospital IT infrastructure and support increasingly complex clinical workflows. At the same time, cross-border clinical research collaboration and the rising focus on precision medicine are also encouraging the use of shared cloud environments for faster data processing and collaboration among institutions. In this context, the Europe’s Health Data Space (EHDS) Regulation establishes a unified framework for the secure use and exchange of electronic health data across the region’s vast geography. Besides, it strengthens patients' control over their records, supports cross-border access, and enables secondary use of anonymized data for research, innovation, and policy-making. The phased implementation is from 2025 to 2031, and EHDS will harmonize standards for electronic health records, strengthen privacy protections under GDPR, and foster a single market for digital health services.

The healthcare cloud computing market in Germany maintains a strong position in the regional landscape owing to the shift toward integrated care networks, which is encouraging the adoption of cloud platforms that can unify fragmented health IT systems. Growing use of hospital information systems and connected medical technologies is also increasing dependency on scalable cloud environments for real-time data processing and storage. As per the NIH article published in January 2024, the country’s healthcare system is moving toward cloud-based digital ecosystems with a prime focus to improve efficiency, interoperability, and patient outcomes, thereby complying with strict GDPR and national privacy laws. At Charité University Hospital Berlin, the AIQNET consortium demonstrates a model approach, integrating cloud computing with legacy systems through HL7v2, FHIR, and DICOM standards. This initiative enables secure AI-powered medical applications and research, thus driving extensive market expansion.

The digitization of NHS services and the urgent need for scalable data management are fueling the expansion of the healthcare cloud computing market in the UK. The country’s market is utilizing infrastructure as a service and public cloud solutions with a main goal to enhance operational efficiency and improve data interoperability across healthcare providers, thereby fostering a more connected digital ecosystem. In August 2024, an NIH article noted that the UK government and NHS policy strongly support cloud computing through secure data environments in order to enable safe use of anonymised health data for AI, research, and service improvement under national digital health strategies. In addition, it also underscores that NHS–industry collaboration depends on cloud-based infrastructure for interoperability and analytics, although adoption is somewhat constrained by limited technical capacity and strict governance requirements. This showcases the urgent need for stronger infrastructure and scalable implementation frameworks.

Key Healthcare Cloud Computing Market Players:

- Amazon Web Services (U.S.)

- Microsoft Corporation (U.S.)

- Google Cloud (U.S.)

- IBM Corporation (U.S.)

- Oracle Corporation (U.S.)

- Dell Technologies (U.S.)

- Salesforce (U.S.)

- Cleveland Clinic (U.S.)

- G42 (UAE)

- CVS Health (U.S.)

- athenahealth (U.S.)

- GE HealthCare (U.S.)

- Cisco Systems (U.S.)

- Siemens Healthineers (Germany)

- Koninklijke Philips N.V. (Netherlands)

- SAP SE (Germany)

- Fujifilm Holdings Corporation (Japan)

- NTT DATA Corporation (Japan)

- NEC Corporation (Japan)

- INFINITT Healthcare Co., Ltd. (South Korea)

- Samsung SDS (South Korea)

- Telstra Health (Australia)

- Wipro Limited (India)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Amazon Web Services, Inc. is identified as a dominant force in healthcare cloud computing, which is offering scalable infrastructure and services such as HealthLake and HIPAA-eligible solutions. The firm’s strength lies in improved data analytics, AI, and machine learning capabilities that enable providers to manage large volumes of clinical and genomic data.

- Microsoft Corporation is yet another major competitor in this field that benefits from the Azure cloud platform, which is suitable for healthcare with solutions such as Microsoft Cloud for Healthcare. The firm gives prominence to interoperability and AI-based solutions through integrations with tools such as Teams and Dynamics 365.

- Google LLC benefits from its cloud platform and knowledge in artificial intelligence and data analytics, with a main goal to address complex healthcare challenges. The company is more focused on AI-based diagnostics, population health management, and precision medicine.

- IBM Corporation has a significant position in this sector, which is facilitated through its hybrid cloud and AI offerings. The company has its strength in integrating cloud with AI and blockchain technologies, with a main goal to improve clinical workflows, supply chains, and patient data management.

- Oracle Corporation has readily strengthened its position in the healthcare cloud computing category through its cloud infrastructure. In addition, the firm is focused on improving interoperability, real-time data access, and automation within healthcare systems.

Below is the list of some prominent players operating in the global healthcare cloud computing market:

The healthcare cloud computing market is an extremely consolidated landscape, which is being led by hyperscalers such as AWS, Microsoft Azure, and Google Cloud, along with strong healthcare IT specialists such as Siemens Healthineers and Philips. Companies in this field are extensively competing through AI integration, interoperability, and cybersecurity enhancements, which are allowing them to maintain a strong position in this field. Some of the tactical growth steps adopted by the leading players in this field are mergers and acquisitions, regional data center expansion, and partnerships with hospitals to enable telehealth and precision medicine. In May 2025, Oracle, the Cleveland Clinic, and G42 formed a partnership to launch a global AI-powered healthcare delivery platform that leverages advanced analytics, clinical expertise, and sovereign AI infrastructure. This particular initiative aims to transform care by enabling precision medicine, proactive health management, and real-time population understanding.

Corporate Landscape of the Healthcare Cloud Computing Market:

Recent Developments

- In March 2026, CVS Health and Google Cloud announced a strategic partnership to launch Health100, which is an AI-native consumer engagement platform especially designed to deliver personalized, proactive, and connected health care experiences.

- In March 2025, GE HealthCare introduced the Genesis portfolio, which is a cloud-based suite of enterprise imaging SaaS solutions designed to streamline workflows, improve patient care coordination, and reduce operational costs.

- In February 2025, Philips announced the expansion of its HealthSuite Imaging cloud services to Europe, giving radiology departments secure, anytime access to imaging studies and AI-enabled workflows on AWS.

- Report ID: 8523

- Published Date: Apr 22, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.