Graphic Processing Unit (GPU) Market Outlook:

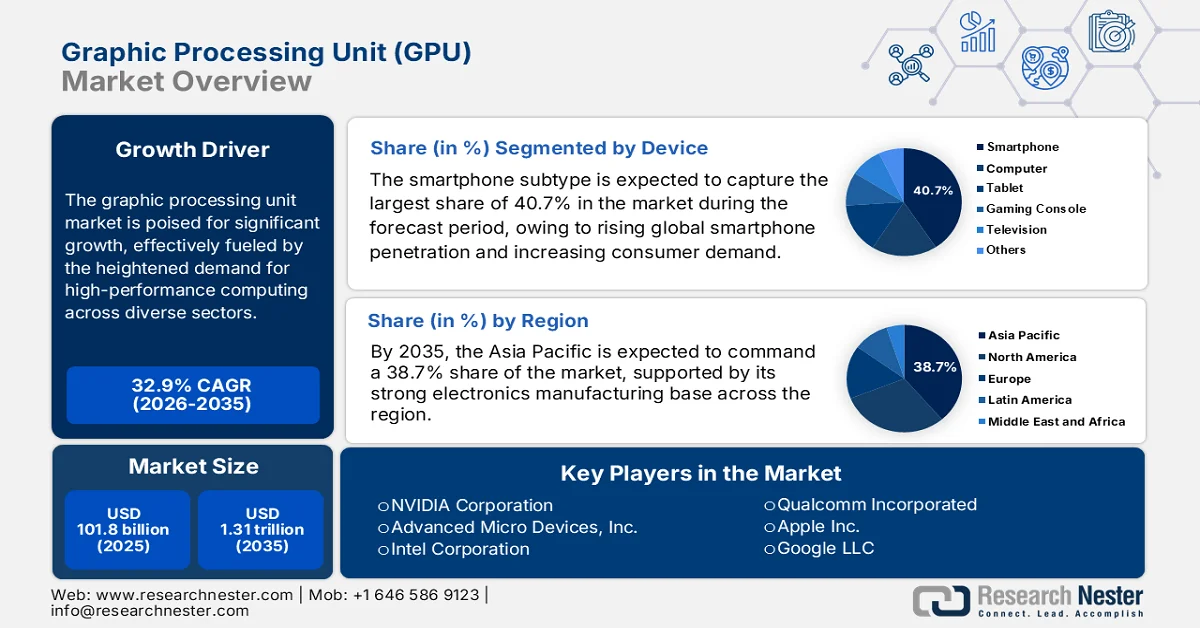

Graphic Processing Unit Market was valued at USD 101.8 billion in 2025, and is expected to surpass USD 1.31 trillion by 2035, at a CAGR of 32.9% during the forecast period, i.e., 2026-2035. In 2026, the industry size of graphic processing unit is estimated at USD 135.2 billion.

The graphic processing unit market is experiencing tremendous growth, which is driven by the expanding demand for high-performance computing across diverse sectors. Innovations in artificial intelligence and machine learning are fueling the need for more powerful and efficient GPUs. The Federal Reserve System in February 2026 revealed that the recent surge in AI investment has boosted global trade, with AI-related imports exceeding USD 272 billion in the first half of 2025, which is up 65% from the first half of 2024. The U.S. leads in AI infrastructure, which is spending more than USD 500 billion on data centers in 2025, whereas China, Taiwan, Mexico, and Vietnam are key suppliers of servers, GPUs, and parts. AI-related goods now account for roughly 2% of total merchandise trade, up from 1% in 2018, reflecting strong demand for specialized hardware, hence denoting a huge growth potential for the graphic processing unit (GPU) market.

Furthermore, the aspects of government-backed initiatives, cloud computing, and virtualization are also broadening applications in the market. In March 2025 Ministry of Electronics & IT, through the Press Information Bureau (PIB), reported that India is emerging as a global AI powerhouse with strategic initiatives such as the India AI Mission and Centres of Excellence, which are constantly driving innovation. The government has allocated a total of USD 1.25 billion to build a high-end AI compute infrastructure with 18,693 GPUs, providing affordable access at USD 1.2/hour compared to the global cost of USD 2.5 to USD 3 per hour. Five semiconductor plants are under construction to strengthen domestic capabilities. The report also stated that India has launched foundational AI models such as BharatGen and Sarvam-1, along with language platforms like BHASHINI, supporting applications in governance, healthcare, and education, hence denoting a lucrative opportunity for the graphic processing unit (GPU) market’s growth and exposure.

Key Graphic Processing Unit (GPU) Market Insights Summary:

Regional Highlights:

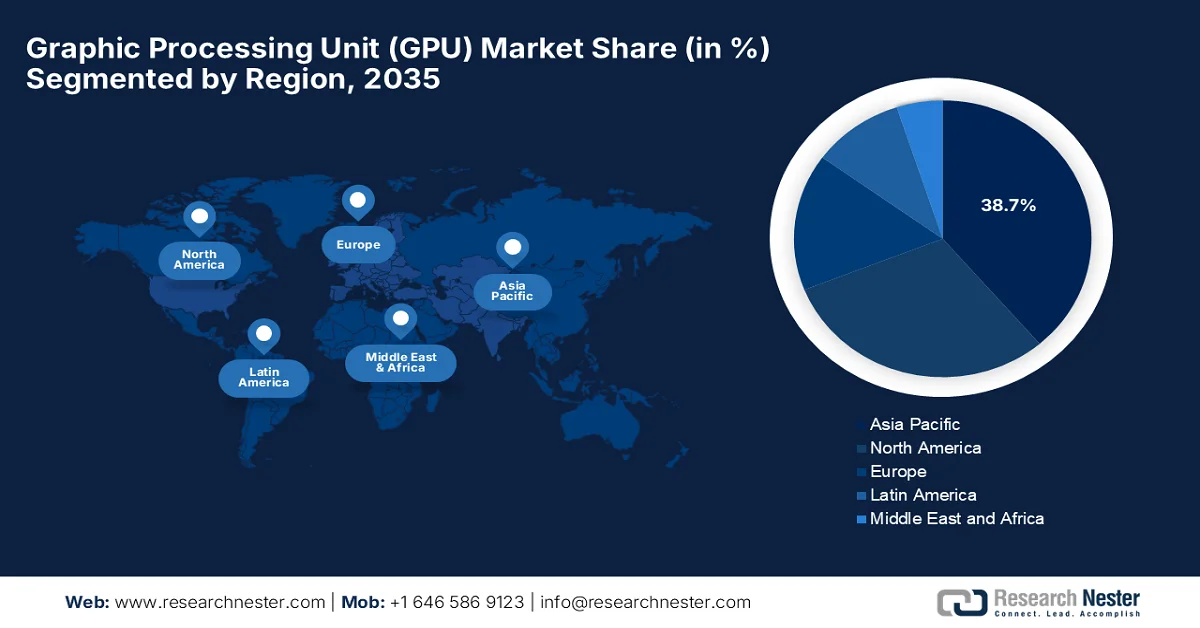

- By 2035, Asia Pacific is anticipated to secure a dominant 38.7% share in the graphic processing unit (gpu) market, attributed to a strong electronics manufacturing ecosystem and large-scale GPU deployment through public–private AI infrastructure initiatives.

- North America is projected to witness the fastest expansion in the market during 2026–2035, stimulated by rising investments in AI supercomputing infrastructure and collaborations between technology firms and federal agencies.

Segment Insights:

- By 2035, the Smartphone subtype is projected to capture a leading 40.7% share in the graphic processing unit (gpu) market, fueled by expanding global smartphone penetration and increasing demand for high-performance mobile gaming.

- Integrated GPUs are anticipated to expand at a notable pace through 2026–2035, supported by their growing adoption across laptops, desktops, and mobile devices because of energy efficiency and cost-effective performance for mainstream computing tasks.

Key Growth Trends:

- Expansion of the gaming industry

- Cloud & data-center deployment

Major Challenges:

- Increasing competition and market saturatio

- Dependence on a few major foundries

Key Players: NVIDIA Corporation (U.S.), Advanced Micro Devices, Inc. (U.S.), Intel Corporation (U.S.), Qualcomm Incorporated (U.S.), Apple Inc. (U.S.), Google LLC (U.S.), Microsoft Corporation (U.S.), Amazon Web Services, Inc. (U.S.), IBM Corporation (U.S.), Arm Ltd. (UK), Imagination Technologies Group (UK), Samsung Electronics Co., Ltd. (South Korea), Sony Corporation (Japan), Huawei HiSilicon (China), Palit Microsystems Ltd. (Taiwan), MetaX Integrated Circuits (China), Lisuan Technology Co., Ltd. (China), Moore Threads Technology Co. Ltd (China), Neysa Networks Pvt Ltd (India), CoreWeave, LLC (U.S.).

Global Graphic Processing Unit (GPU) Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 101.8 billion

- 2026 Market Size: USD 135.2 billion

- Projected Market Size: USD 1.31 trillion by 2035

- Growth Forecasts: 32.9% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (38.7% Share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: United States, China, Japan, South Korea, Taiwan

- Emerging Countries: India, Germany, United Kingdom, Canada, Singapore

Last updated on : 10 March, 2026

Graphic Processing Unit (GPU) Market - Growth Drivers and Challenges

Growth Drivers

- Expansion of the gaming industry: The solid growth in the gaming sector drives heightened demand in the graphic processing unit (GPU) market. The growth in terms of eSports and immersive experiences necessitates powerful GPU hardware for high frame rates and improved graphics rendering. According to the article published by Press Information Bureau (PIB) in February 2026, India’s gaming sector has emerged as a major growth engine within the country’s creative economy, wherein the revenues surpassed USD 2.56 billion in 2024 and are projected to grow steadily. Besides, the report also states that gaming, along with animation, VFX, and XR, drives technology-intensive and globally connected production, thereby fostering a highly skilled talent pool. Hence, this denotes that there is a huge growth opportunity for GPU hardware to support high-performance digital platforms.

- Cloud & data-center deployment: The demand for GPU-powered cloud instances is growing at a robust pace since enterprises and service providers across major nations offer AI, analytics, and graphics-intensive computing as scalable services. Data centers combine CPU and GPU resources to support hybrid AI workloads, prompting a profitable business environment for pioneers in the market. In this context, the article published by the Harvard Kennedy School and Lawrence Berkeley National Laboratory in February 2026 states that the U.S. data center demand is rapidly expanding, fueled by AI, analytics, and graphics-intensive workloads. Hyperscale data centers operated by companies such as Amazon, Microsoft, Google, and Meta collectively spent more than USD 200 billion on CapEx in 2024, reflecting growing investment in GPU-powered cloud and hybrid computing infrastructure, hence denoting a positive graphic processing unit (GPU) market outlook.

Major Tech Giants’ 2024-2025 Capital Expenditure on Data Centers

|

Company |

CapEx 2024 (USD Billion) |

YoY Growth 2023-2024 |

Projected CapEx 2025 (USD Billion) |

|

Amazon |

85.8 |

+78% |

>100 |

|

Microsoft |

44.5 |

+58% |

>80 |

|

|

52.5 |

+63% |

>80 |

|

Meta |

39.2 |

+40% |

Not specified |

Source: Belfer Center

- Industry-wide digital transformation: Several industries are adopting GPU-powered solutions, i.e., the autonomous vehicles, healthcare & imaging, finance & scientific research, denoting a huge demand for these advanced systems. For instance, in October 2025, the U.S. Department of Energy announced the Discovery and Lux AI supercomputers at Oak Ridge National Laboratory, which were powered by AMD GPUs and CPUs, with a collective goal to accelerate AI-based research across energy, manufacturing, medicine, and cybersecurity. In addition, the Lux AI Cluster, which is deploying in 2026, and Discovery, in 2028, will enable large-scale AI training, complex simulations, and scientific breakthroughs, hence benefiting the overall GPU market.

Challenges

- Increasing competition and market saturation: The graphic processing unit market is intensely competitive, which faces pressure from emerging players and specialized AI accelerator companies. In consumer graphics, the aspect of market saturation has slowed growth, whereas the cloud and AI data centers attract new entrants that are offering suitable solutions. On the other hand, startups and regional manufacturers, particularly in emerging nations, introduce alternative architectures that challenge traditional designs. Competitors are also adopting aggressive pricing strategies, making differentiation demanding. Therefore, in order to sustain revenue, companies need to innovate in performance-per-watt, AI optimization, or software ecosystems, making investment prohibitive for players from price-sensitive regions.

- Dependence on a few major foundries: Manufacturers in the GPU market are dependent on a small number of semiconductor foundries for advanced node production. This dependence creates vulnerability to capacity constraints, cross-border tensions, and natural disasters. Any disruption can delay product launches or force costly redesigns. In this context, diversifying fabrication partners is considered to be challenging, influenced by the high technology barriers, proprietary processes, and the limited availability of leading-edge nodes. Besides, the smaller manufacturers in this field face higher risks of being deprioritized. In addition, coordinating production schedules, managing wafer allocation, and ensuring quality across multiple nodes is even more complex.

Graphic Processing Unit (GPU) Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

32.9% |

|

Base Year Market Size (2025) |

USD 101.8 billion |

|

Forecast Year Market Size (2035) |

USD 1.31 trillion |

|

Regional Scope |

|

Graphic Processing Unit (GPU) Market Segmentation:

Device Segment Analysis

The smartphone subtype is expected to register its dominance, capturing the largest share of 40.7% in the graphic processing unit market by 2035. The dominance is highly attributable to rising global smartphone penetration and increasing consumer demand for high-performance mobile gaming. Also, modern smartphones are dependent on these advanced mobile GPUs to support high-resolution displays and augmented reality applications. In September 2025, Qualcomm Technologies, Inc. announced the Snapdragon 8 Elite Gen 5, which is a major GPU advancement for smartphones. The new Qualcomm Adreno GPU architecture delivers a 23% boost in graphics performance, enabling richer gaming, improved power efficiency, and AI-enhanced visual experiences directly on the device. Hence, such continued innovations in mobile GPU innovation are driving higher performance standards in smartphones, solidifying the sub-segment’s growing dominance within the GPU market.

Type Segment Analysis

By the end of the forecast period, the integrated GPUs will grow at a considerable rate in the market. Their increased incorporation into laptops, desktops, and mobile devices due to energy efficiency, lower cost, and sufficient performance for mainstream tasks is the main factor behind this leadership. In January 2026, Intel reported that it had launched the Intel Core Ultra Series 3 at CES 2026, which is the first AI PC platform built on Intel 18A, featuring enhanced integrated Intel Arc graphics. The new X9 and X7 processors include up to 12 Xe-cores, delivering up to 77% faster gaming performance and up to 27 hours of battery life, which reflects powerful yet energy-efficient integrated GPU performance in mobile systems. Hence, such continued innovations are suitable for bolstering the segment’s growth and exposure in the upcoming years.

Application Segment Analysis

In terms of application, the gaming & entertainment will grow, grabbing a significant share during the discussed timeframe. The growth of the sub-segment is largely driven by advancing graphics fidelity, VR/AR support, and esports growth. GPUs power not only consoles and PCs but also cloud gaming and mobile gaming platforms, positioning them as a major revenue generator in the long term. Besides, the rise of real-time ray tracing and AI-enhanced upscaling technologies is elevating visual realism, increasing the need for high-performance GPUs across different platforms. The aspect of subscription-based gaming services and distribution models has also been a major driver, which is expanding access to the gaming content, in turn driving GPU utilization. Moreover, cross-platform gaming integration is encouraging hardware upgrades to maintain competitive performance standards across console, PC, as well as the mobile environments, benefiting the overall GPU market.

Our in-depth analysis of the graphic processing unit (GPU) market includes the following segments:

|

Segment |

Subsegments |

|

Device |

|

|

Type |

|

|

Application |

|

|

Industry Vertical |

|

|

Component |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Graphic Processing Unit (GPU) Market - Regional Analysis

APAC Market Insights

The Asia Pacific graphic processing unit market is expected to lead the entire global dynamics, capturing the largest share of 38.7% by 2035. The region’s leadership is largely driven by a strong electronics manufacturing ecosystem, especially in countries such as China, South Korea, Taiwan, and Japan, which serve as global hubs for semiconductor production and assembly. Public-private partnerships are also a major asset for this region, driving consistent utilization of advanced GPUs. In October 2025, the government of South Korea partnered with NVIDIA and other leading industrial groups to deploy more than 260,000 GPUs across sovereign clouds and AI factories. Besides he Ministry of Science and ICT committed more than 50,000 GPUs to the National AI Computing Center and domestic cloud providers, hence making it suitable for standard GPU market growth.

Massive NVIDIA GPU Deployment in South Korea: Government and Industry AI Infrastructure Investments for 2025

|

Entity |

GPUs Deployed |

Focus |

|

Ministry of Science and ICT (MSIT) |

50,000+ |

National AI Computing Center, sovereign AI infrastructure |

|

Samsung Electronics |

50,000+ |

AI factory for semiconductors, digital twins, robotics |

|

SK Group |

50,000+ |

AI factory, industrial AI cloud, digital twin & robotics workloads |

|

Hyundai Motor Group |

50,000+ |

AI factory for manufacturing, autonomous driving, and smart factories |

|

NAVER Cloud |

60,000+ |

Sovereign AI infrastructure, industry-specific AI models |

|

Total (Government + Industry) |

260,000+ |

National AI ecosystem across cloud, manufacturing, telecom, and automotive |

Source: NVIDIA

The state-led programs to strengthen domestic semiconductor capabilities and AI infrastructure are the major driving factors for the graphic processing unit market in China. The public investments in terms of smart cities and autonomous systems require GPU acceleration, whereas research institutes also leverage GPUs for large-scale language models and scientific computing. In July 2025, Mercator Institute for China Studies disclosed that China is aggressively pursuing AI self-reliance across hardware, software frameworks, and applications, mostly influenced by government strategies and state-backed investments. The semiconductor sector, which is led by Huawei in collaboration with domestic chipmakers, is focused on producing AI chips. The domestic firms, such as Baidu and Huawei, develop machine learning frameworks by contributing to global open-source projects to support domestic GPUs, hence denoting a positive market outlook.

The government-backed digital initiatives and the robust growth of its IT services sector are positively influencing the exceptional growth of the graphic processing unit market in India. Public programs supporting AI in agriculture and healthcare create new applications, whereas private firms in the country are focused on cloud services and fintech solutions. In this context, the article which was kept forward by PIB in February 2026 stated that the India-AI Impact Summit highlighted the country’s efforts to democratize AI by expanding access to around 38,000 GPUs at USD 0.78/hour, 5G connectivity across 99.9% of districts, and national platforms such as AIKosh, which are hosting more than 7,500 datasets and 273 AI models. It also underscores that these initiatives enable startups, researchers, and public institutions to deploy AI across various sectors. Hence, the consistent government efforts position India as the world’s third most AI-competitive nation, fostering both economic and market growth in the upcoming years.

North America Market Insights

The North America graphic processing unit market is forecasted to be the strongest market from 2026 to 2035. The region’s progress in this field is primarily shaped by strong collaboration between technology companies and federal agencies that are highly focused on secure computing infrastructure. Public investments in AI research and defense applications create a heightened demand for high-performance GPUs. In October 2025, NVIDIA notified that, along with Oracle, it had partnered with the U.S. Department of Energy to build the nation’s largest AI supercomputers at Argonne National Laboratory, consisting of 100,000 and 10,000 NVIDIA Blackwell GPUs for the Solstice and Equinox systems. These supercomputers will accelerate scientific discovery, support AI model training, and enhance research across healthcare, materials science, and energy, hence contributing to the overall GPU market growth in the region.

The government-backed initiatives in semiconductor manufacturing and national AI strategies are responsible for uplifting the graphic processing unit market in the U.S. Besides the existence of programs supporting domestic chip production encourage GPU adoption across industries, private firms integrate GPUs into consumer electronics, enterprise solutions, and entertainment ecosystems. In November 2024, the Biden-Harris Administration, through the CHIPS for America program, allocated Intel a total of USD 7.8 billion to expand U.S. semiconductor fabrication and advanced packaging across Arizona, New Mexico, Ohio, and Oregon. This federal investment supports domestic production of leading-edge chips, which also includes those used in AI and high-performance computing, strengthening supply chain security. Hence, such instances drive GPU adoption across industries by enabling private firms to integrate advanced chips into technology, enterprise, and consumer solutions.

The strong emphasis on healthcare innovation and sustainable technology is fueling the growth of graphic processing unit market in Canada. Public health agencies and research institutions use GPU-powered imaging and diagnostics, whereas government support for green data centers also encourages GPU integration into energy-efficient computing. As of the September 2025 reports from the country’s government, Canada’s Beatrix Compute Cluster Facility, which is operated by the National Research Council, is a GPU-accelerated infrastructure supporting AI research across academia, industry, and government. The facility consists of 36 nodes, each hosting 4 GPUs, and it enables high-throughput machine learning, data analytics, and deep learning workloads. In addition, it is backed by a USD 25 million government investment under the Canadian Sovereign AI Compute Strategy, and the facility expands the country’s AI ecosystem, hence denoting a positive GPU market outlook.

Europe Market Insights

In Europe graphic processing unit market is growing on account of strong regulatory frameworks and public-private partnerships. Both the public and private entities in the region emphasize secure and ethical AI development, and research institutes across the continent use GPU clusters for climate modeling and scientific exploration, solidifying Europe’s position in the global dynamics. In January 2026, the Council of the European Union reported that it amended the EuroHPC Joint Undertaking regulation to enable the creation of AI gigafactories in the region by providing advanced computing infrastructure. It also notes that these facilities aim to strengthen the regional industry, competitiveness, and innovation through public-private partnerships with member states and industry stakeholders. Furthermore, the regulation also sets funding and procurement rules while supporting start-ups and scale-ups, hence denoting a positive outlook for the market’s growth and exposure.

Germany graphic processing unit market is growing exponentially based on factors such as the strong industrial base and engineering expertise. Public initiatives that are supporting Industry 4.0 encourage GPU adoption in manufacturing and robotics, whereas research institutions also rely on GPU computing for advanced simulations in materials science and energy. In January 2025, the Gauss Center for Supercomputing announced that it had launched the Gauss AI Compute Competition in partnership with the country’s federal and state funding agencies to promote generative AI model development. The initiative leverages the upcoming JUPITER exascale supercomputer at the Jülich Supercomputing Center, which will host around 24,000 next-generation GPUs. It also notes that researchers will gain access to approximately 15 million GPU-hours to train foundational AI models with societal impact, strengthening Germany’s AI ecosystem and technological sovereignty.

The emerging AI strategies and strong academic research are propelling the growth of graphic processing unit market in the UK. Investments in healthcare innovation and defense applications drive GPU demand, whereas the universities and startups in the country contribute by developing GPU-powered solutions for business-led research. In August 2025 The UK Research and Innovation (UKRI) announced a rapid access route to the Isambard-AI and Dawn AIRR supercomputers by enabling the UK-registered small and medium businesses to access GPU resources for early-stage AI product development. It states that each project can utilize up to 20,000 GPU hours within three months to conduct feasibility studies, industrial research, or experimental development. Moreover, this particular initiative, which is supported by multiple UKRI councils, including EPSRC, MRC, and Innovate UK, is designed to accelerate innovation, hence supporting business-led research through GPU-powered supercomputing.

Key Graphic Processing Unit (GPU) Market Players:

- NVIDIA Corporation (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- Intel Corporation (U.S.)

- Qualcomm Incorporated (U.S.)

- Apple Inc. (U.S.)

- Google LLC (U.S.)

- Microsoft Corporation (U.S.)

- Amazon Web Services, Inc. (U.S.)

- IBM Corporation (U.S.)

- Arm Ltd. (UK)

- Imagination Technologies Group (UK)

- Samsung Electronics Co., Ltd. (South Korea)

- Sony Corporation (Japan)

- Huawei HiSilicon (China)

- Palit Microsystems Ltd. (Taiwan)

- MetaX Integrated Circuits (China)

- Lisuan Technology Co., Ltd. (China)

- Moore Threads Technology Co. Ltd (China)

- Neysa Networks Pvt Ltd (India)

- CoreWeave, LLC (U.S.)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- NVIDIA Corporation is the undisputed leader in the global graphic processing unit (GPU) market, which is pioneering massively parallel processors for gaming, AI, and data centers. The company is well known for its GeForce, RTX, and Blackwell architectures, and its CUDA ecosystem remains a pivotal competitive moat, driving adoption in AI training, inference, and HPC.

- Advanced Micro Devices, Inc. competes strongly with high-performance Radeon and Instinct GPU lines by keeping a target on gaming, professional visualization, and AI data centers. The company benefits from RDNA and CDNA architectures, highlighting both consumer and enterprise graphics solutions.

- Intel Corporation is a central player in this field, which brings a broad semiconductor portfolio into the GPU arena. The organization has been historically dominant in combined graphics through its CPUs, and it is now pushing into discrete and AI compute spaces, leveraging its fabrication capabilities and ecosystem partnerships to strengthen its position across PCs and cloud.

- Qualcomm Incorporated is yet another major player in mobile and embedded GPU tech through its Adreno graphics, integrated into Snapdragon SoCs, which are powering billions of smartphones and XR devices. Besides, the firm is making strategic moves to diversify beyond mobile into high-performance AI hardware.

- Imagination Technologies Group is a specialist GPU intellectual property licensor, which is best known for its PowerVR family that is used in mobile, embedded, and automotive applications. The company is highly focused on energy-efficient graphics cores and AI-optimized designs that partners integrate into their own SoCs, making it influential in devices.

Below is the list of some prominent players operating in the global market:

The U.S.-based players, such as NVIDIA, AMD, and Intel, which lead with high-performance architectures and AI-optimized accelerators, are rearranging the competitive dynamics of the graphic processing unit market. Meanwhile, the major cloud and platform providers such as Google, Microsoft, and AWS are incorporating GPUs into their vast portfolio of services. Mobile and embedded segments are influenced by Qualcomm, Apple, and Samsung, which are focused on power-efficient graphics and AI. In March 2025, AMD reported that it had completed its acquisition of ZT Systems, which is a leading provider of AI and general-purpose compute infrastructure, to create end-to-end AI solutions by combining AMD GPU, CPU, and networking silicon with open-source ROCm software and rack-scale systems. Hence, such tactical strategies from pioneers in this field are suitable for bolstering the market’s growth.

Corporate Landscape of the Graphic Processing Unit (GPU) Market:

Recent Developments

- In February 2026, AMD and Meta announced that they entered into a multi-year partnership to deploy up to 6 gigawatts of AMD Instinct GPUs for Meta’s AI infrastructure, starting with a custom MI450-based GPU that is built on the AMD Helios rack-scale architecture.

- In January 2026, NVIDIA reported that it had launched the Rubin platform, which is an AI supercomputer combining six new chips, i.e., the Rubin GPU, Vera CPU, NVLink 6 Switch, ConnectX-9 SuperNIC, BlueField-4 DPU, and Spectrum-6 Ethernet Switch, designed to reduce inference token cost.

- Report ID: 8430

- Published Date: Mar 10, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.