Electronic Components Distribution Market Outlook:

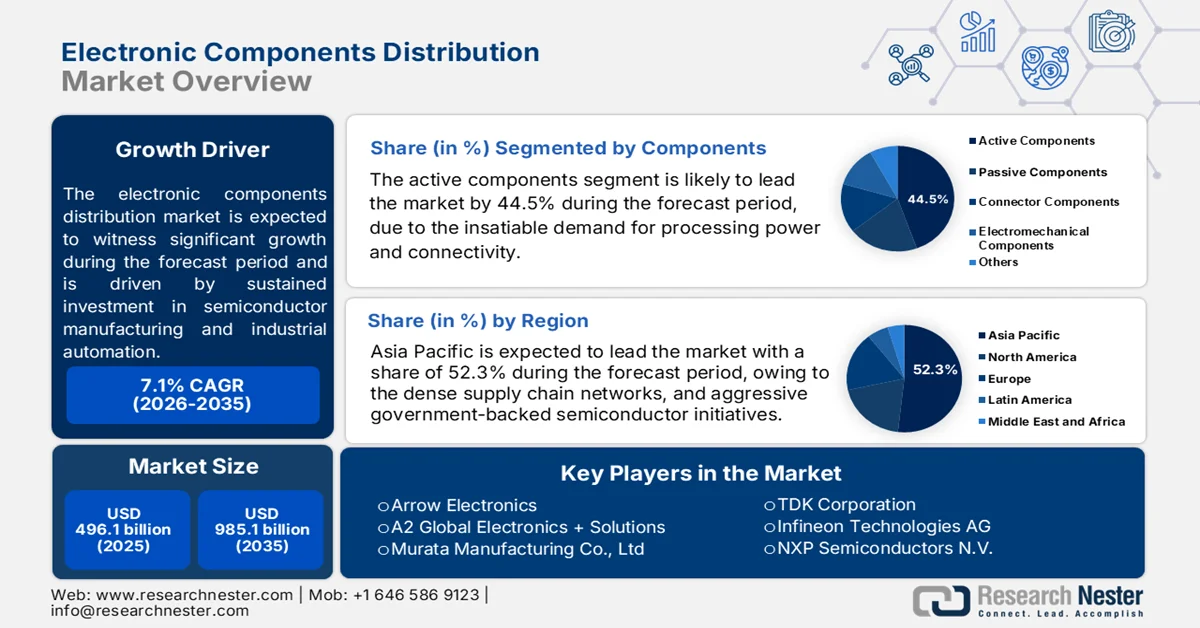

Electronic Components Distribution Market size was valued at USD 496.1 billion in 2025 and is projected to exceed USD 985.1 billion by the end of 2035, expanding at over 7.1% CAGR during the forecast period i.e., between 2026-2035. In 2026, the industry size of electronic components distribution is estimated at USD 531.3 billion.

The electronic components distribution market is being shaped by sustained investment in semiconductor manufacturing, industrial automation, automotive electronics, telecommunications infrastructure, and data center expansion. Distribution partners are increasingly expected to support inventory management, supply-chain resilience, design support, and regional fulfillment as manufacturers seek to reduce procurement risk and improve production continuity. According to the U.S. Semiconductor Industry Association (SIA) February 2025 data, global semiconductor sales reached USD 627.6 billion in 2024, reflecting strong demand across computing, communications, industrial, and automotive applications. At the same time, government-backed capacity expansion programs are strengthening long-term component demand.

Industrial digitalization and electrification programs are also supporting market growth. The International Energy Agency (IEA) May 2025 data reported that global electric car sales exceeded 17 million units in 2024, increasing the demand for power semiconductors, sensors, connectors, passive components, and embedded processing devices throughout automotive supply chains. These trends are encouraging distributors to expand value-added services, strengthen inventory positioning, and develop closer relationships with semiconductor manufacturers and industrial customers. The market outlook remains supported by increasing electronic content across transportation, energy, industrial automation, communications, and computing sectors.

Key Electronic Components Distribution Market Insights Summary:

Regional Highlights:

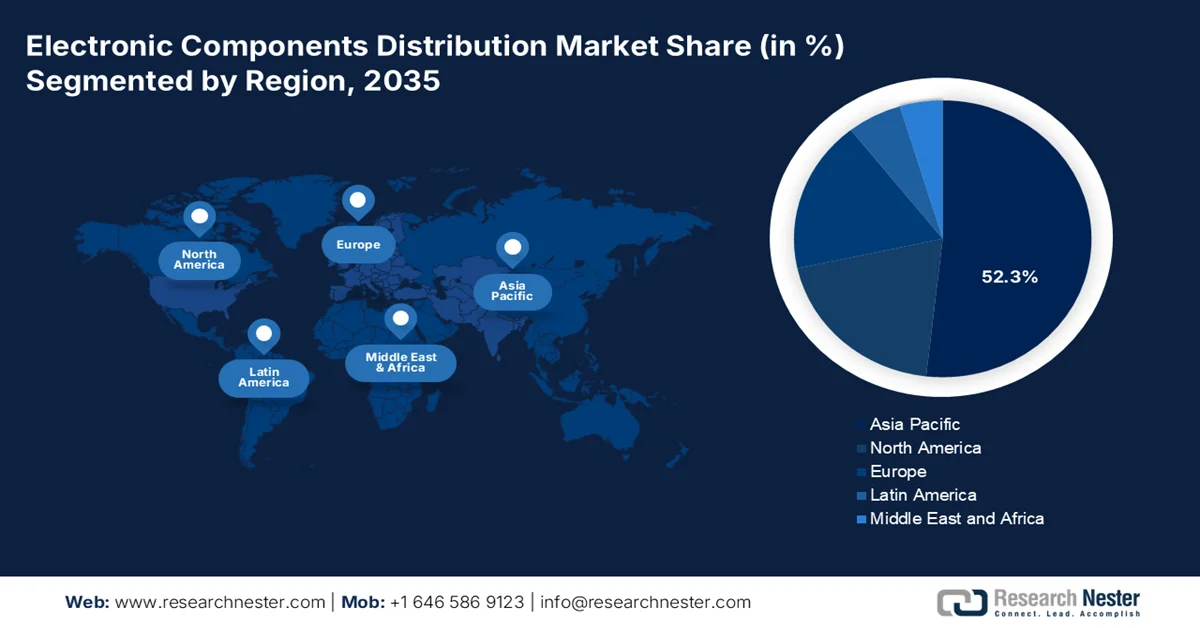

- The Asia Pacific electronic components distribution market is anticipated to account for 52.3% of revenue share by 2035, bolstered by expansive electronics manufacturing ecosystems, integrated supply chain networks, and strong government support for semiconductor and advanced component production

- North America is expected to witness notable growth in the market throughout 2026-2035, fueled by localized supply chain initiatives, rising investments in defense and automotive electrification, and escalating demand from advanced computing and data center applications

Segment Insights:

- The active components segment is projected to secure a 44.5% share of the electronic components distribution market by 2035, propelled by escalating requirements for processing power, connectivity solutions, and supportive investments in SMT components, LED chips, and RFID-enabled technologies

- Data processing is set to remain the leading application segment during 2026–2035, supported by the rapid expansion of cloud computing, artificial intelligence, and big data infrastructure requiring high-performance electronic components

Key Growth Trends:

- Public investment in telecommunications infrastructure

- Growth in data centers and digital infrastructure

Major Challenges:

- Supply chain volatility

- Stringent regulatory compliance

Key Players: Arrow Electronics (U.S.), A2 Global Electronics + Solutions (U.S.), Murata Manufacturing Co., Ltd. (Japan), TDK Corporation (Japan), Infineon Technologies AG (Germany), NXP Semiconductors N.V. (Netherlands).

Global Electronic Components Distribution Market Forecast and Regional Outlook:

Market Size & Growth Projections:

- 2025 Market Size: USD 496.1 billion

- 2026 Market Size: USD 531.3 billion

- Projected Market Size: USD 985.1 billion by 2035

- Growth Forecasts: 7.1% CAGR (2026-2035)

Key Regional Dynamics:

- Largest Region: Asia Pacific (52.3% share by 2035)

- Fastest Growing Region: North America

- Dominating Countries: China, United States, Japan, South Korea, Germany

- Emerging Countries: India, Vietnam, Mexico, Malaysia, Indonesia

Last updated on : 14 July, 2026

Electronic Components Distribution Market - Growth Drivers and Challenges

Growth Drivers

- Public investment in telecommunications infrastructure: Government-supported telecommunications modernization programs are driving demand for electronic components used in network equipment, fiber infrastructure, data transmission systems, and wireless communication hardware. According to PIB March 2026 data, over 5.18 lakh 5G Base Transceiver Stations had been installed across the country, with services available in nearly all districts. Similar network modernization initiatives are occurring across Europe, North America, and Asia. For distributors, the opportunity extends beyond product availability to supporting telecom equipment manufacturers with forecasting, inventory optimization, and supply continuity. As governments continue funding broadband expansion and digital connectivity projects, distributors are expected to play a critical role in ensuring component availability for telecommunications equipment suppliers and infrastructure contractors.

- Growth in data centers and digital infrastructure: Government policies supporting artificial intelligence, cloud computing, and digital transformation are increasing investment in data center infrastructure, thereby driving demand for electronic components. The Congress.gov May 2026 data reported that data centers accounted for approximately 4.4% of total U.S. electricity consumption due to AI-driven computing demand. Expanding server deployments require processors, memory devices, power semiconductors, networking hardware, connectors, and thermal management electronics sourced through distribution channels. The trend also highlights opportunities for distributors offering specialized logistics, demand forecasting, and supply-chain visibility services tailored to data center operators and equipment manufacturers.

Challenges

- Supply chain volatility: Disruptions from geopolitical tensions, natural disasters, and raw material shortages create unpredictable lead times. Manufacturers struggle to maintain consistent inventory levels, risking production halts and lost customer trust. Building resilient, multi-sourced supply chains is essential but resource-intensive for new entrants.

- Stringent regulatory compliance: Navigating complex international regulations like RoHS, REACH, and conflict mineral reporting demands significant expertise and documentation. Non-compliance results in fines, shipment delays, or market bans. New manufacturers must invest heavily in legal and quality assurance teams to meet these evolving global standards.

Electronic Components Distribution Market Size and Forecast:

| Report Attribute | Details |

|---|---|

|

Base Year |

2025 |

|

Forecast Year |

2026-2035 |

|

CAGR |

7.1% |

|

Base Year Market Size (2025) |

USD 496.1 billion |

|

Forecast Year Market Size (2035) |

USD 985.1 billion |

|

Regional Scope |

|

Electronic Components Distribution Market Segmentation:

Component Type Segment Analysis

Under the component type segment, the active components is leading and is poised to hold the share value of 44.5% by the end of 2035. The segment is driven by the insatiable demand for processing power and connectivity. According to the APIIC May 2025 data, the state is actively supporting the active components sub-segment. The policy specifically incentivizes Surface-mount Technology (SMT) components, LED chips, and chip modules for smart cards and RFID applications. Active component manufacturers can avail investment subsidies eligible fixed capital investment for mega projects, along with 100% net SGST reimbursement for five years and power cost subsidies. With a target to achieve USD 50 billion in electronics production and create 5 lakh jobs, Andhra Pradesh is leveraging its industrial clusters in Visakhapatnam and Tirupati to attract active component investments, strengthening India's electronics manufacturing ecosystem.

Application Segment Analysis

Within the application segment, data processing is leading in the electronic components distribution market. The segment is driven by the explosive growth of cloud computing, artificial intelligence (AI), and big data analytics. This sector demands high-performance, specialized electronic components for servers, data storage arrays, and high-speed networking equipment. The relentless push for greater computational power to train and run complex AI models is the primary growth engine. Reflecting this digital infrastructure boom, the IEA April 2025 data stated that global data center electricity consumption is 460 TWh in 2024. This data underscores the massive scale of data center expansion and the corresponding surging demand for advanced power management and cooling components within the distribution market.

Distribution Channel Segment Analysis

Direct Sales remains the leading sub-segment in the distribution channel segment, particularly for complex, high-value electronic components that require technical collaboration and customized solutions. By eliminating intermediaries, manufacturers build stronger relationships with large OEMs, ensure better supply chain visibility, and offer competitive pricing for bulk orders. This model is critical for securing long-term contracts and providing design-in support, which is essential for active components like semiconductors and specialized passive components. The direct approach also enables faster response to market demands and closer alignment with client production schedules, making it the preferred channel for strategic, volume-driven partnerships in the electronics distribution ecosystem.

Our in-depth analysis of the electronic components distribution market includes the following segments:

|

Segment |

Subsegments |

|

Application |

|

|

Distribution Channel |

|

|

Component Type |

|

|

End user Industry |

|

|

Material Type |

|

Vishnu Nair

Head - Global Business DevelopmentCustomize this report to your requirements — connect with our consultant for personalized insights and options.

Electronic Components Distribution Market - Regional Analysis

APAC Market Insights

Asia Pacific is dominating the electronic components distribution market and is expected to hold the regional revenue share of 52.3% by the end of 2035. The region is driven by the massive manufacturing bases, dense supply chain networks, and aggressive government-backed semiconductor initiatives. The region serves as the global production hub for passives, connectors, and discrete devices, with distributors leveraging advanced logistics and digital platforms to serve diverse end-markets—from consumer electronics in China and South Korea to automotive and industrial automation in Japan, India, and Southeast Asia. Distributors focus on value-added services like design-in support, kitting, and just-in-time delivery. Growth stems from 5G infrastructure, EV production, renewable energy systems, and IoT proliferation, though geopolitical trade tensions and raw material costs pose ongoing risks.

The rapid growth in electronics manufacturing, consumer devices, automotive electronics, and industrial automation is shaping the electronic components distribution market in India. Distributors are increasingly supporting OEMs and EMS providers with component sourcing, inventory planning, and supply-chain management as domestic production capacity grows. The PIB October 2025 data depicted that the India’s electronics production reached approximately ₹11.3 lakh crore, reflecting strong demand for semiconductors, passive components, connectors, sensors, and embedded devices. This manufacturing expansion is creating sustained opportunities for distributors across the country.

The extensive electronics manufacturing base, strong exports, and continued investment in advanced technologies such as electric vehicles, industrial automation, and telecommunications equipment is driving the electronic components distribution market in China. Distributors play a critical role in ensuring component availability for high-volume production across consumer electronics and industrial sectors. According to the Global Times April 2025 data, the country’s integrated circuit production reached 451.4 billion units, an increase compared with 2023, reflecting robust semiconductor manufacturing activity and rising demand for related components. This growth is strengthening procurement requirements and expanding opportunities for electronic component distributors across China.

North America Market Insights

North America is projected to emerge during the assessed period, 2026 to 2035 in the electronic components distribution market. The region is driven by the mature infrastructure, a strong shift toward localized supply chains, and heightened demand from defense, automotive electrification, and data center sectors. The region benefits from federal investments aimed at reducing reliance on Asian manufacturing, with distributors increasingly prioritizing inventory buffers and supplier diversification. Sustainability mandates and traceability requirements are reshaping logistics, while consolidation among top players intensifies competition. Growth is underpinned by industrial automation, renewable energy storage systems, and advanced computing needs, though labor shortages and extended lead times remain operational challenges.

The strong demand for semiconductor-related products across computing, telecommunications, automotive, and industrial sectors is shaping the electronic components distribution market in the U.S. The OEC 2024 data depicts that the U.S. imports of parts of semiconductor devices and similar devices (HS 8541.90), which totaled approximately USD 578 million, highlighting the country's continued reliance on global semiconductor supply chains for manufacturing and assembly activities. Growing investments in advanced electronics production, AI infrastructure, and next-generation communication systems are increasing procurement requirements for semiconductor components and supporting the expansion of distribution networks that provide inventory management, technical support, and supply-chain services to manufacturers.

The growing investments in telecommunications, clean technology, aerospace, industrial automation, and advanced manufacturing is shaping the electronic components distribution market in Canada. Distributors are strengthening regional supply networks to meet demand for semiconductors, connectors, sensors, and power management devices used across these sectors. A key indicator of market activity is Canada’s expanding electronics trade. According to Government of Canada June 2026 data, imports in electronic and electrical equipment increased by 6% in 2025, reflecting sustained production demand that relies on a stable supply of electronic components. As manufacturers continue to modernize operations and adopt advanced digital technologies, distributors are increasingly providing inventory management, technical support, and sourcing services to ensure production continuity.

Europe Market Insights

The automotive electrification, industrial automation, and renewable energy integration, with a strong emphasis on regulatory compliance and sustainability is driving the electronic components distribution market in Europe. Distributors face stringent RoHS, REACH, and carbon-footprint tracking requirements, pushing investments in certified supply chains and circular economy models. The region balances domestic production with imports from Asia, while defense and aerospace sectors demand high-reliability mil-spec components. Nearshoring trends accelerate as OEMs reduce dependency on distant suppliers, favoring Eastern European logistics hubs. Labor shortages and energy costs challenge margins, yet value-added services, design support, inventory financing, and obsolescence management, remain key differentiators. Overall, Europe prioritizes resilience, green transition, and localized sourcing over pure cost efficiency.

The strong position in electronics innovation, industrial automation, and advanced manufacturing is driving the electronic components distribution market on Germany. Demand for semiconductors, sensors, connectors, and embedded components is supported by ongoing product development and technology investments across multiple industries. According to Germany Trade & Invest (GTAI) 2026 data, the electronics industry accounts for 23% of Germany’s total R&D spending, highlighting the sector’s role as a key innovation driver. This substantial research activity fuels demand for electronic components used in microelectronics, automation systems, digital technologies, and next-generation industrial equipment. As manufacturers continue to invest in innovation, distributors are strengthening sourcing capabilities and technical support services to meet evolving component requirements.

The electronic components distribution market in the UK is supported by demand from aerospace, defense, telecommunications, industrial automation, and advanced electronics manufacturing sectors. Distributors play a vital role in ensuring the availability of semiconductors, connectors, sensors, and power management devices required for production and system integration. A key indicator of market activity is the growth of the domestic electronics industry; according to the UK Office for National Statistics (ONS) December 2024 data, the manufacture of computer, electronic and optical products generated approximately £36.8 billion in turnover in 2024. This strong industrial base continues to drive procurement of electronic components and supports the expansion of distribution services across the UK.

Key Electronic Components Distribution Market Players:

- Arrow Electronics (U.S.)

- A2 Global Electronics + Solutions (U.S.)

- Murata Manufacturing Co., Ltd. (Japan)

- TDK Corporation (Japan)

- Infineon Technologies AG (Germany)

- NXP Semiconductors N.V. (Netherlands)

- Company Overview

- Business Strategy

- Key Product Offerings

- Financial Performance

- Key Performance Indicators

- Risk Analysis

- Recent Development

- Regional Presence

- SWOT Analysis

- Arrow Electronics, Inc. bridges component manufacturers and system integrators, operating within the electronic components distribution market to supply semiconductors, passives, and wireless modules. Their distribution network supports efficient supply chain management, technical design assistance, and inventory optimization for diverse industrial and consumer electronic applications.

- A2 Global Electronics + Solutions specializes in lifecycle management and sourcing of obsolete and hard-to-find components, playing a key role in the electronic components distribution market to ensure long-term product sustainability. Their services include end-of-life forecasting, alternate part recommendations, and supply continuity for mature electronic systems.

- Murata Manufacturing Co., Ltd. provides miniaturized capacitors, inductors, EMI filters, and RF modules, distributed widely through the electronic components distribution market to enable compact, high-frequency circuit designs. Their components ensure stable power delivery, signal integrity, and noise suppression in wireless communication and automotive electronic systems.

- TDK Corporation offers magnetic components, pressure sensors, piezoelectric elements, and supercapacitors, strategically positioned within the electronic components distribution market to enhance power backup and signal conditioning. Their distributed solutions support robust performance in power electronics, industrial automation, and high-reliability circuit board assemblies.

- Infineon Technologies AG supplies low-power microcontrollers, power semiconductors, security ICs, and GaN devices, available through the electronic components distribution market to enable energy-efficient and secure electronic designs. Their components address thermal management, switching efficiency, and data protection in automotive, industrial, and consumer electronics sectors.

Here is a list of key players operating in the global electronic components distribution market:

The manufacturing landscape for electronic components is highly fragmented and intensely competitive, dominated by a mix of broad-line giants and specialized niche players. The sector is characterized by continuous innovation in miniaturization, power efficiency, and thermal management. Asian manufacturers, particularly from Japan, Taiwan, and China, exert significant influence over the passive components and semiconductor segments. Key differentiators include technological prowess in high-frequency applications, automotive-grade reliability, and supply chain resilience. While a few multinational corporations lead in overall market share, a long tail of specialized manufacturers competes effectively by focusing on specific components or by serving unique end-market verticals such as aerospace, medical, and industrial automation.

Corporate Landscape of the Market:

Recent Developments

- In July 2025, Arrow Electronics, a global provider of technology solutions announced the launch of its new Engineering Solutions Center(ESC) in Bangalore, India. This expansion reinforces Arrow’s commitment to making critical technologies such as AIoT, edge computing, intelligent sensing more accessible, while strengthening the engineering capabilities of domestic technology manufacturers

- In October 2024, A2 Global Electronics + Solutions announced the launch of its BGA reballing service. This service is now available at A2 Global’s state-of-the-art facilities in the United States, the Netherlands, and Singapore, offering quick lead times and comprehensive component support for industries requiring high-reliability solutions.

- Report ID: 8235

- Published Date: Jul 14, 2026

- Report Format: PDF, PPT

- Explore a preview of key market trends and insights

- Review sample data tables and segment breakdowns

- Experience the quality of our visual data representations

- Evaluate our report structure and research methodology

- Get a glimpse of competitive landscape analysis

- Understand how regional forecasts are presented

- Assess the depth of company profiling and benchmarking

- Preview how actionable insights can support your strategy

Explore real data and analysis

Frequently Asked Questions (FAQ)

About this Report

Connect with our Expert

Report, 2026-2035

Copyright @ 2026 Research Nester. All Rights Reserved.